Illinois Treasurer Michael Frerichs has a new boast he wanted us to know about.

Respecting Illinois’s two college savings programs, which his office administers, he recently said this:

The balance was $7 billion when I was first elected in 2015. Because of changes that we championed, especially a reduction in investment fees, we have more than doubled the balance and saved families $100 million dollars in fees.

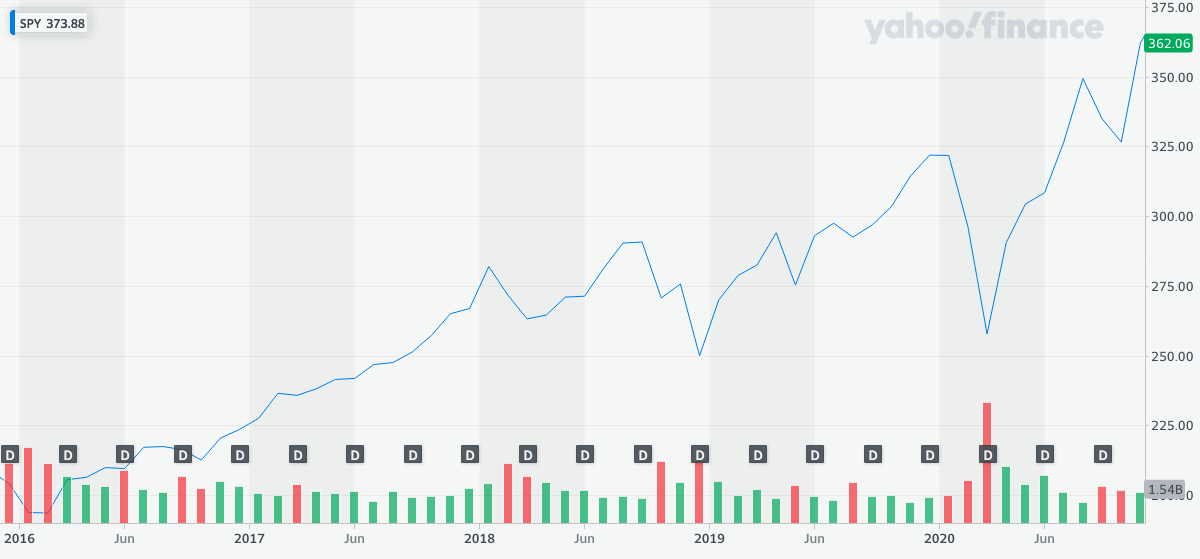

Now, hold on a minute. The stock market during that period is up roughly 84%, plus another 8% or so from dividends. That is, if the accounts were invested in a simple S&P 500 ETFs or mutual funds they would be up about 92% during the period. The balance would have nearly doubled just from that.

Yet Frerichs says the doubled balances are because of the changes he championed.

The full story is more complicated because there were also deposits and withdrawals into those college savings accounts. And they aren’t invested entirely in stocks, though most of them probably are, and bonds, too, went up nicely during the period since he was elected.

Unquestionably, however, a very strong market accounts for most of the reason the balances have soared. And the savings Frerichs claims in $100 million in fees, even if that’s true, wouldn’t have made much difference, being something under 1.5% of the balance.

So, please Treasurer Frerichs, unless you think the market’s exuberance is due to your presence in the financial world, don’t claim doubled balances are because of changes you championed.

A big challenge for us at Wirepoints is distraction. Really. I sit down do some administrative chore, research or something particular but all too often I get an email or news alert on something else, something that makes me think, “Oh, jeez, I have to write about this.”

And so it was with this. A reader sent me the Facebook page where Frerichs boasted about this and linked to the article. Please, readers, make it stop! I’m trying to get stuff done!

(Just kidding. Keep it coming.)

-Mark Glennon

Expect no retraction or apology. This what they do.

Expect no retraction or apology. This what they do. The state’s existing buyout program for its own pensions is the precedent for Chicago, which should be a warning: Look out for similar exaggerated claims and shoddy analysis.

The state’s existing buyout program for its own pensions is the precedent for Chicago, which should be a warning: Look out for similar exaggerated claims and shoddy analysis.

Anybody that puts funds into any plan or scheme with the word “Illinois” in it is asking for it.

On another subject look at the returns generated by an index fund with minimal costs yet the Illinois expensive pension funds still maintain their empire of wasteful spending.

Isn’t the bigher picture, is why save in any of these plans, or scrimp & scrap like i did to pay for you or your kids college if Biden’s going to majically make all college free going forward? Your pretty much a chump if you save or saved. Would savers get their money back from ferich if, for example, as they are proposing congress picks up the tab and makes all state univs free? A giant bailout to all the undercompensated folks @ u of i

What are the funds total fees? If yes, why do the funds need managers making big bucks when they could simply be invested in zero fee index funds. Just as all the pension funds could be as well saving big taxpayer $bucks$ as advocated by rauner appointie to trs ,marc levine.

Wait a minute – it is a big deflection from the real problem which is that College Illinois! the pre-paid tuition plan was woefully underfunded just a few years ago and should be closed forever. I’d like to hear a discussion about that since it is backed by the taxpayer and last time I checked was in debt over $500 million.

Yup, we haven’t heard much about College IL, which is different from the two 529 plans, and was foolish from the start.

Keep pushing back on this guy and exposing him.

He hurt this state years ago by being the final vote to increase taxes and drove his cousin Gayle Frerichs trucking from our state.

This guy French’s wants a higher post and he doesn’t deserve it.

Do not trust this man.

Maya Angelou who said it best: “When someone shows you who they are, believe them the first time.”