By: Mark Glennon*

The best price index for single family homes in major U.S. metropolitan areas is widely regarded as the CoreLogic S&P Case-Shiller Index. We link to it each month for that reason, but some explanation and a look back over time are in order.

It’s more meaningful than other indices because it tracks repeat sales of the same home, or some approximation thereof. Looking at “average” prices in other reports is less meaningful because the averages get distorted by which end of the market is relatively hot or cold. For example, if low price homes are in demand but the high end of the market is languishing, the “average” selling price gets artificially pulled down.

The Case-Shiller Index avoids that problem, and reports both changes in the most recent month from the same month in the previous year, as well as month-to-month price changes.

The most recent Case-Shiller report published Monday is for April and it’s good news for current Chicagoland homeowners, as it has been recently. For the Chicago metro area, prices in April were 4.2% higher than last April, second only to Miami’s 5.2% among the ten major metros in the index. This April’s prices were also up month-to-month for Chicago, increasing 1.8% over this March.

That beat the nation as a whole on both counts. The national average price change for this April compared to last April was a drop of 0.2%, and an increase of just 1.3% from this March to April.

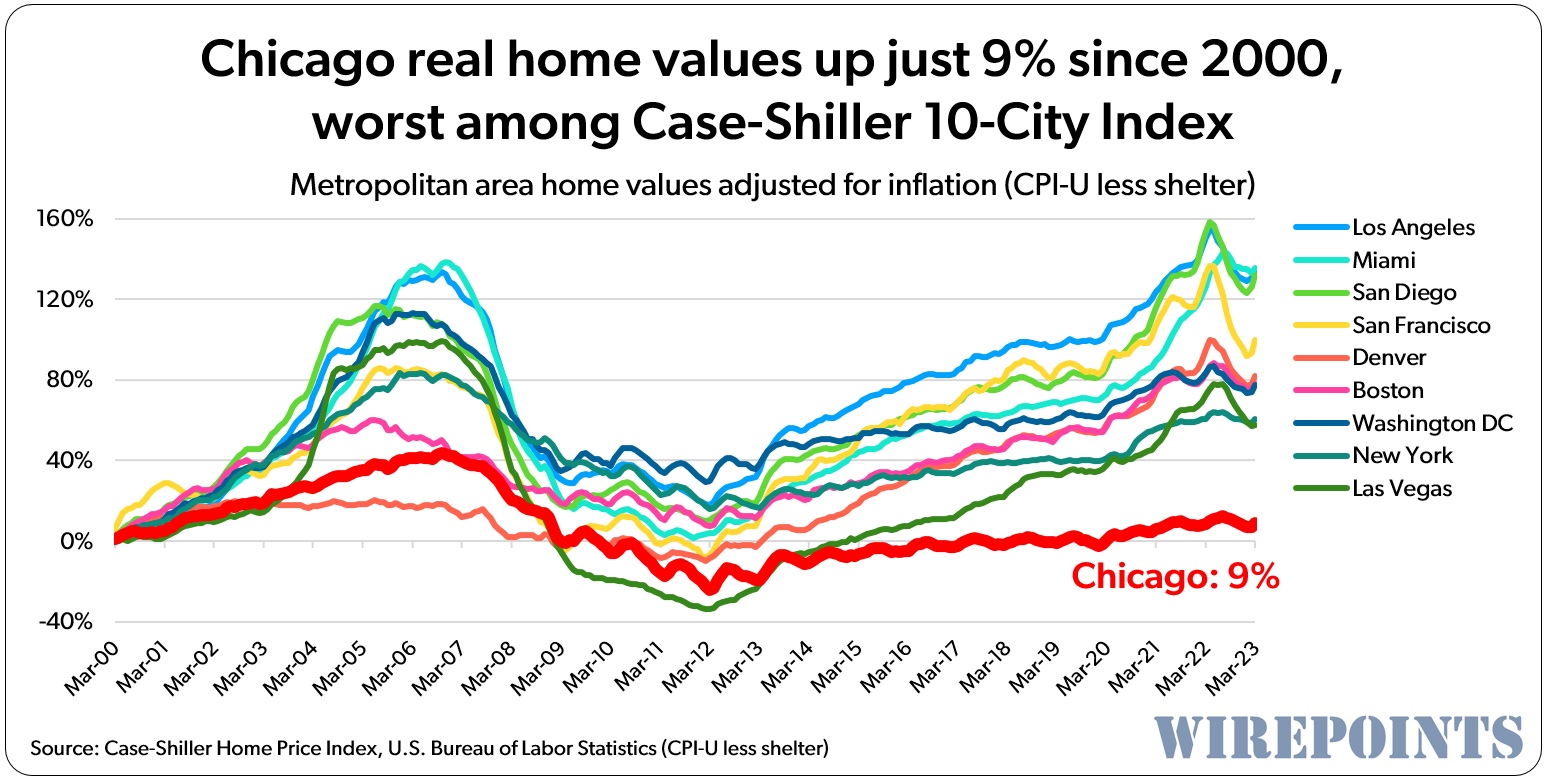

It’s a different story if you look at price changes since 2000. Chicago did not participate in the big, national price surges but was spared from the severe downturn seen in most cities since mortgage rates spiked up about 18 months ago. Netting it out, as you can see in the chart, Chicago metro prices have lagged far below the other largest metros, despite recent gains.

That’s bad news for those who have owned in Chicago for ten or twenty years.

Another positive angle of the long-term price underperformance, one might think, is that the Chicago area is arguably more affordable for would-be homeowners. However, much of the price suppression is undoubtedly due to high property taxes. Illinois’ are second highest in the nation. They’ve soared over the years across Chicagoland and most of Illinois, by any measure. Statewide, for example, they’ve grown over 60% as percentage of household income over 30 years.

Those taxes impose a cost that cancels out at least some of the affordable prices. Property taxes are essentially a wealth tax. That is, high property taxes aren’t just an annual bill. They reduce home value.

*Mark Glennon is founder of Wirepoints.

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

This phenomenon is explained by ‘tax rate capitalization’ formula. A property is simply an asset with net revenue generation potential. If one owns one’s home, one can quantify the ‘rent’ one pays to oneself. That can then be normalized for comparison with America, by treating the rent as a percentage of household income. Household income in America is paying less than 4% for property taxes. Household income in Woodstock Illinois is paying more than 9% for property taxes. Household income can only add up to 100%. The additional 5%+ of household income paid to property taxes is not available to… Read more »

Neighbors across the street moved to Orlando area, and built a new retirement home – He did a lot of the inside finish work. In 5 years their home market value doubled. A real estate bubble – sure. But their net worth has increased dramatically, in retirement! Homes I looked on in NC and passed were back on the market in 3 years for 20% more. Real-estate/ a home in IL is most definitely not an investment of any kind.

By moving to SC in 2021, our net worth increased by the $10K a year we saved in property taxes. Plus the area we are in, because of an expansion of Ft. Gordon, there is a demand for 25,000 new homes by 2030. Housing starts booming, existing houses in the $500K range sell in days and ours appreciated by 40% in 2 years. Would be nice to take the profit, but too happy to be out of IL.

Left for Charlotte NC 10 years ago, as I expected this exact housing trend back in 2013.

Best financial decision I ever made. Still gets me angry how much equity they stole from me previous though.

Why are people leaving Chicago — here’s why:

‘Please Don’t Shoot!’ Woman Says She’s Moving Out Of Chicago After Being Robbed At Gunpoint In Lake View – CWB Chicago

“ We voted blue!” people cry as they are robbed blind by criminals with and without guns.

Wow, glad I voted with my feet and got out of Sheeetcago over 20 years ago.

House in Denver has been my best investment for the past 10 years.