By: Mark Glennon*

For those of you frustrated by obscure pension reporting, here’s a simple way to look just a few numbers and get a pretty good feel on one important measure: How much would it cost per year just to stay even? That is, what does it take from taxpayers to keep a pension from falling further into the abyss? Then, compare that to what taxpayers are actually putting in. I’ll do that for Illinois pensions, which, as you will see, are falling far short.

Start with the unfunded liability. That’s what’s owed for work already performed but not covered by assets the pension has. Multiply that by the pension’s “interest rate” That’s the assumption the pension uses for how much its assets will earn every year, and sometimes called the “discount rate.” Unfunded pension liabilities don’t literally bear “interest” the way a bond or other debts do, but it works out the same way. For pensions, because the liability is not covered by an asset, the unfunded liability effectively grows at the discount rate.

Then, add what’s called “total normal cost” per year. That’s the additional liability the pension takes on for work now being performed. Finally, subtract out the “employee contribution,” which is what workers are contributing per year. What’s left is how much taxpayers must fund just to keep unfunded liabilities from growing. That’s simplified and leaves out some other items (usually, relatively small ones) but is roughly accurate.

Let’s do it for Illinois’ six statewide pensions combined:

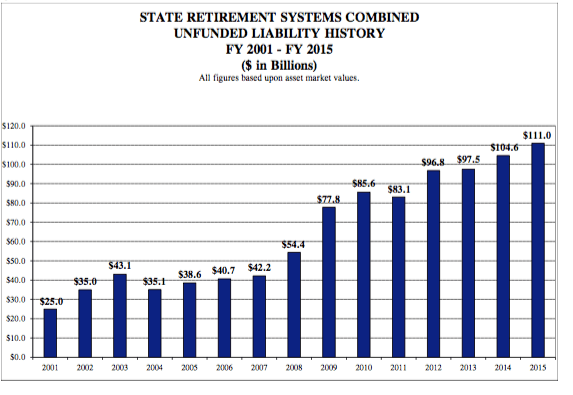

Their total unfunded liability is about $113 billion. Their interest rates range from 7% to 7.5%. Multiply the rates used for each pension by their unfunded liabilities, add them up, and you get about $8.3 billion per year of “interest.”

Now, add the total, annual normal cost, which is about $3.6 billion, and subtract the total annual contribution paid by workers, which is about $1.5 billion.

The result is about $10.4 billion. That’s what taxpayers would need to pay just to keep the six pensions from deteriorating further. But the state in fact is contributing only $7.6 billion this year — more than ever before but $2.8 billion too little.

We will sink that much further into the quicksand, even if all else goes well with state pensions. That’s been going on for years, and it’s a big part of why the history of the state’s unfunded liabilities looks like what you see on the right, despite larger taxpayer contributions every year.

The trend shown will continue.

My numbers come from last month’s report on state pensions by the Commission on Government Forecasting and Accountability and the most recent actuary reports for each pension. That calculation of a $2.8 billion shortfall is actually a bit smaller than found in a more detailed and scholarly calculation addressing the same concept in a slightly different way, published here by an actuary about a year and a half ago. She calculated the built-in shortfall at $3.4 billion.

All these numbers assume pension assumptions are reasonable, which no reputable financial economist does. Most importantly among those assumptions, the shortfall will be worse if pension assets don’t in fact earn 7% to 7.5% per year. On that, keep in mind that the great post-recession bull market ended last summer. Once realistic returns start to show up in the reporting, the numbers will tank further.

Finally, nobody should assume that “just staying even” is how you need to fund pensions. Additional payments are needed to amortize the unfunded liability over no more than thirty years, most actuaries would say. Our failure to do that is just kicking the can to, well, I’m not sure who — whomever would still hang around Illinois in coming decades if this isn’t fixed. Amortizing the liability over 30 years would cost taxpayers another $3.5 billion or so per year.

These shortfalls will not be overcome. Illinois’ pension obligations cannot, and will not, be met in full. The sooner we accept reality and do what’s inevitable the better off all will be. That includes cutting unfunded liabilities — earned pension benefits — through constitutional amendment, bankruptcy or default.

*Mark Glennon is founder of WirePoints. Opinions expressed are his own.

Expect no retraction or apology. This what they do.

Expect no retraction or apology. This what they do. The state’s existing buyout program for its own pensions is the precedent for Chicago, which should be a warning: Look out for similar exaggerated claims and shoddy analysis.

The state’s existing buyout program for its own pensions is the precedent for Chicago, which should be a warning: Look out for similar exaggerated claims and shoddy analysis.

I would like to comment on what I believe are some very misleading statements on this board. 1) Steve-Oh: I cannot speak for the other systems, but SURS’ compound annual investment return from June 30, 2000 to June 30, 2015 was 5.58% per year, well above the 4% you claim. More importantly, as you are no doubt aware, use of the year 2000 as a starting point is extremely misleading, because that was the peak year of a 6-year bull market. During that 6-year run, SURS’ compound annual investment return was 16.57%. Far more representative is that over the past… Read more »

Well said Andrew…..and I am gratefull I ecaped your sharp fact-finding critiques. Your vision is clear.

I’m grateful that I can spot “delusional”, and you and Andrew are hard-core delusional

Professor Szakmary- Regarding the portion directed to me, sure, we could raise enough new revenue to cover the $10 billion stay-even-on-pensions number. But you are, like so many others, focusing on just a tiny part of our consolidated disaster: 1. Even with the horrendous spending cuts now in place and with the too-small pension contribution, Illinois is running $6.2B/yr in the red, according to the Comptroller. Any tax/spending plan has to address that, too. Another $8 billion or so in revenue to fix that? 2. You are cherry picking the state out of our massive overlapping crises. CPS, Chicago, and… Read more »

You can quote adequate ROI numbers all you want, but at what (and whom’s) expense were those gains made? Will SURS be refunding the profits gained from the housing bubble? Because guess who bought most of the toxic securities back then: the pension funds. Every negatively-impacting employee-related decision companies have made in the past few decades (ie outsourcing) has been in response to chasing profits to appease Wall Street’s biggest investors: the pension funds. Pensioners seem to have no issue with how these profits were obtained in the past even though there is a direct correlation to the income disparities… Read more »

Andrew: The market crash in early 2000 and the market flat-line in last 9 months, is PART of the reason I hold to my stmt: Since 1/1/2000, that is 16.25 years, the stock markets have been awful. Nasdaq has grown about zero compounded in the period ! S&P 500 has grown 2-3% and 10-yr bonds have done best, over 5%. The past 16 years has been very important for ANY DB plan at that time that was well-funded, around 100%, but it would have been a terrible time (given the 16 years that followed) for any DB pension plans to… Read more »

Andrew, I should have stated it thusly: ” Tell us why private sector taxpayers working an living in Chicagoland, should have their wealth and home values unduly diminished even more than they already have been ! ” And don’t forget these key numbers, private sector working taxpayers are already paying $5.5B for Payroll of the 80,000 active govt ees covered in the five major citywide pension plans — and the unfunded liability is either $30B or $45B depending on net inv returns for the next 10-20 years. How is that possible without taxing the residents into oblivion ? Mark and… Read more »

I will get down in the mud I guess. You ask: (I paraphrase) Why should taxpayers have thier wealth diminished… 1. The law says you have to pay taxes. The government needs more revenues. This concept is not really hard is it? The court ruled, the LAW says the bill MUST be paid. Until the feds step in, or we fail to follow the LAW, we must pay. 2. Taxpayers are allready paying the payroll for 80,000… well dont we want our Cops/Firemen etc on the beat? Yes we do so we pay people to do work for us taxpayers.… Read more »

It’s a shame these arguments are always taken to the extreme. When someone asks about the # of state employees or the salaries or benefits offered, it always comes back as “Don’t we want our Cops/Firemen etc on the beat?” or “I guess you want lead in your drinking water.” A better question is “Why are the Cops/Firemen hired in 2010 allowed to retire at the same age in ones hired in 1960?” Funny, you’d think medical advances, better living, and job safety would have lengthened at least a year or two of a career over 50 years, right? When… Read more »

So is legalized theft from the private sector to enrich the govt class, a law that should be changed ?

A few thoughts: Before the Dems and unions get too much grief for wanting to re amortize the debt. (kicking the can down the road), let us all remember that the father of this is Jim Edgar, whose administration came up with the major re amortization that we are still suffering with. It’s noteworthy that it passed unanimously. His so called pension ramp truly kicked the can down the road and cost we taxpayers billions in interest. As for the reasons for the deficit, it’s probably fair to say a little more than 50% of the deficit is the state… Read more »

T.H. – You are absolutely right about Edgar and plenty of other Republicans. Edgar still does not understand pensions, as we wrote here: https://wirepoints.org/why-jim-edgar-has-zero-credibility-on-illinois-budget-and-pensions-wp-original/ To be clear about by views on can-kicking and reamortization, we now probably have no choice but to continue to do it, as we are doing, pending real reform (which requires a new legislative majority). There’s no way taxpayers would stand for the needed tax increase to cover full funding plus the horrible structural deficit we have now. More importantly, I disagree about why they were never funded properly. They are simply unaffordable, which is why… Read more »

Cheers Mark !! Excellent !! And notwithstanding what the NYTimes and other economic illiterates abounding in the media……say……the problem is NOT that contributions haven’t been large enough for last X years…………the problem is that the pension promises, too much and paid too early, and with too much COLA……were NEVER affordable in the first place !! A governmental entity promising luxurious pensions paid too early, should NEVER have costed out the affordability assuming 7.5% net inv egns per year. That was and is utterly reckless. Any shortfall from that leads to catastrophe………and since 1/1/16 the average annual compounded return has been… Read more »

Meant 1/1/2000 in the last sentence. So far, this century has been horrific for investment returns.

I’m sorry, there is no realistic way to make the liability go away. There is no legal ability to retroactively change the contractual obligations created by the Constitution, except by the State exercising its police powers, which the ISC just ruled against. States can’t file for bankruptcy, and as for default, that’s not a legal remedy.

You are mistaken. A broadly worded constitutional amendment would likely hold up. Chapter 9 can be amended to cover states. Defaults happen when there is no money. We’ve covered all that extensively in earlier articles here.

I’ll offer the opinion that you are on very thin ice claiming I am mistaken. The contracts clause in the U.S. Constitution would negate any attempt to retroactively reduce benefits by changing the Illinois Constitution. If you really think the federal bankruptcy statutes are going to be amended to allow states to go bankrupt, well….

Even in Bankruptcy, bondholders protected by statute vrs pensioners protected by a CONSTITUTIONAL guarantee… who wonders who will get more protection in bankrupcy? Until Illinois Starts defaulting, on non pension related obligations, going to the bankruptcy court in order to fix its pension mess will be seen as an obvious ploy to use a bankruptcy court for unconstitutional pension reform. So you want to go to Bankruptcy court to fix your pension problem?….you got to also defund other Vital state obligations AS WELL…and create a HUGE HUGE fiscal and SOCIAL mess statewide…to make the case for Bankruptcy. To show insolvency.… Read more »

Advocate- I think you have some fundamental misconceptions about bankruptcy. First, it does trump the constitutional pension protection, Second, it’s primary purpose is to assure that vital services are continued. In my opinion, some have already been sacrificed for pensions. More fundamentally, I repeat the eternal challenge nobody will answer: What possible combination of tax increases and spending cuts do you propose that can solve the overlapping state and municipal insolvency we now have, without cutting pensions? There is none. Here’s what will actually happen: We will continue with a partial “just don’t fund the pensions” approach. That’s what we… Read more »

That underfunding approach got us to where we are now.

Doubling down on the underfunding approach is the continuing evil of kicking the can to our children.

How dare anyone suggest that.

“How dare anyone suggest that”? That’s been exactly the policy of unions and Dems for years. Again, that’s what the article shows. That’s exactly the proposal of union-funded CTBA and Ralph Martire under their “reamortization” bunk. See https://www.youtube.com/watch?v=bCi2eZcMxrM. That’s what Rahm wants with the bill Rauner just yesterday said he would veto. That’s what unions have sometimes supported in the form of pension holidays they lobbied for.

Pension hollidays are OVER. No more can kicking to OUR children.

Pension debt re-amortization is can-kicking to our children. Pension debt re-amortization is a pension holiday.

Tax. Retirement. Income.

Yes I agree Nixit. Tax retirement Income asap as a step in the right direction….as long as it continues to be revenue positive.

Well said btw.

There should be a pause for reality check. Constitutional amendment is required to enact graduated income tax. Simple increase in flat income tax rate requires a legislative enactment not vetoed by the governor. Courts can’t mandate this. Voters (largely taxpayers) elect legislators and the governor. We may know in five years or ten where our process of democratic government will lead us. More taxes into the leaking bucket may be the only political solution, but it’s just another form of kicking the can to our political and biological descendants. The result of tax increases is likely to be a few… Read more »

Add Ben Frankin to those quotes: “When the people find that they can vote themselves money that will herald the end of the republic.”

John Marshall was much more on point guys: “The principle asserted is, that one legislature is competent to repeal any act which a former legislature was competent to pass; and that one legislature cannot abridge the powers of a succeeding legislature. The correctness of this principle, so far as respects general legislation, can never be controverted. But, if an act be done under a law, a succeeding legislature cannot undue it. The past cannot be be recalled by the most absolute power. Conveyances have been made, those conveyances have vested legal estates, and, if those estates may be seized by… Read more »

You’re talkin’ about Fletcher v Peck; that’s what you’re talkin’ about. That’s the venerable basis of most discussions about impairment of contract. I’m talkin’ about payin’ what is owed. Bankruptcy can modify a “contract” debt. Failing that, states and municipalities must default on contract debt if they can’t raise the money to pay the debt. States raise money primarily via taxes which are enacted by the legislature subject to veto by the governor. Courts don’t (and can’t) raise taxes. That’s called “separation of powers” and that’s what I’m talkin’ about. Beating the drum or stamping the feet for contract rights… Read more »

Is taxing retirement income, on par with a graduated income tax in that in can only be done through Const. amendment? Heck if I know that one. Sounds to me like broad taxing state authority would allow the gen assembly to do it.

We will NOT have our children pay EVEN more of the bills WE choose to postpone. We will pay our bills and not ourchildren. Our children for the first time in American history face a decline in standard of living as compared to thier parents. Can kicking is over, the trickle-down, Gotta help the Corps economics, No-tax Norquist economics, less tax means more revenues has failed our governing ballance sheets. We will pay, not our children, we will start by raising our state income tax. Even Rauner knows this tax MUST be raised. Why delay. The delay hurts ourchildren When… Read more »

Yes, taxes will be raised, and they should be. But it won’t put the state or pensions on a sustainable path. Do you have the slightest idea how huge a tax increase would be required to have our generation and not the next pay for this mess?

No, our kids won’t pay for it, and either will we.

Lots of people “dare” to think about it and some few of them “dare” to speak about it. Nay, to make “suggestions” as to how to fix it. Think about other problems that disrupt peoples’ expectations: Three Mile Island, 9-11 attacks, earthquakes, climate change. Think that some of these result (in part) from human activity — in some instances from government activity. Advocate’s premise is that the “promises” must be kept. WirePoint’s responds that they can’t be kept. Think again about explicit government promises such as looking after military veterans. Then talk to a veteran about his/her experiences at the… Read more »

Judging by your comments it’s apparent you enjoy having the poor and blue collar class pay more and more of their limited income so you can continue to collect (steal) your undeserved and unsustainable pension. In addition to working ‘till 75yrs. old to do it. It’s NOT a pension, it’s extortion. I got news for you, you’re on borrowed time. You keep up with the B.S. constitution argument. There is NO constitution when legislators pick and chose what they like and don’t like. BTW, you’re an a—h—.

Lets not get personel.

Civics lesson in case ya missed class. The Constitution trumps the legeslature. We make Constitutions so WE THE PEOPLE BIND our elected officials…….elected officials dont SUPERCEDE the constitutional laws that WE THE PEOPLE mandate.

BTW, I respect your free speech.

Advocate, both the Detroit court and the Stockton court said Chapter 9 preempts state constitutional pension protection, and that position is now widely accepted.

Yes Mark, I am sorry if I left some doubt that Federal Law, or Bankruptcy law, Superceeds State law. Yes federal bankruptcy laws superceed even state Constitutions, this is fundemental. We fought a very bloody and painfull war to solve that states-rights arguement that lawyers argued over fot years. We know that the Federal Court has the final power. Yes we know that the Judge will have final say as to who gets more, or who gets less. And that Judge will decide amongst secered creditors and unsecured.creditors, and those creditors with a State Constitutional mandate. Bond holders will be… Read more »

Eric- Please keep it reasonably civil here. Swearing and insults are fine if directed to me, but we like guests with other viewpoints.

T.H. – On the U.S. contracts clause, as we have written often before, the answer is not at all clear. I personally think it would go all the way to the US Sup. Court, and I could not have seen the former conservative majority striking down pension reform. With the balance of the Court now up for grabs, we don’t know. On the possibility of changing Ch. 9 to cover states, lots is now being written about that and it’s serious enough that somebody is now running TV ads against Ch 9 for Puerto Rico because they fear it’s a… Read more »