By: Ted Dabrowski and John Klingner

For years, the state’s political elite has blamed ordinary Illinoisans for the state’s pension crisis.

The unions, politicians, the media, civic groups and pundits all say that the state – and by extension taxpayers – have failed to put enough money into government-worker pensions to keep them solvent. That story has been repeated so often it’s become the accepted cause of Illinois’ pension crisis.

We’ve always been suspicious of that claim, given the power of Illinois’ public sector unions, the willingness of politicians to appease them, and the generosity of Illinois’ pension benefits.

As it turns out, we were right. Illinois’ pension crisis isn’t due to too little money in the pension funds. Instead, politicians’ over-generous pension promises are what’s been bankrupting Illinois.

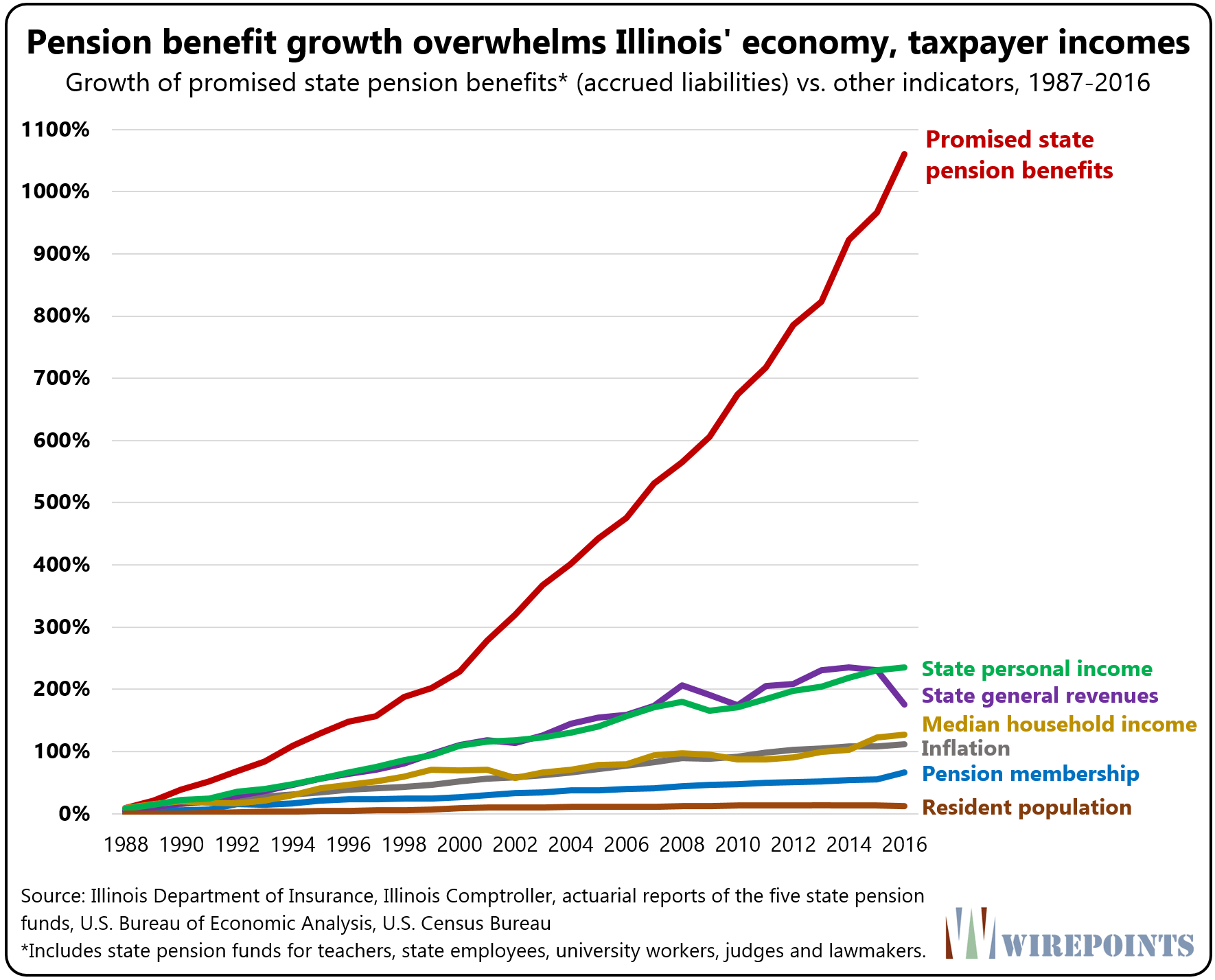

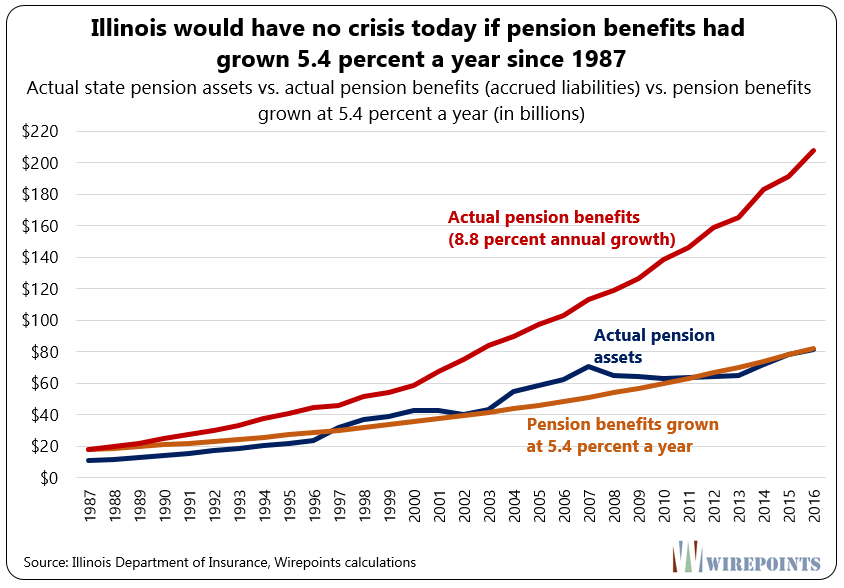

Wirepoints looked at the total amount of pension benefits promised to today’s workers and retirees, then went back and looked at the amount of benefits politicians had promised three decades ago.

Promised pension benefits are now more than 1,000 percent higher than they were in 1987.

As the graphic shows, no other measure of Illinois’ economy comes even remotely close to matching the growth in promised benefits.

Those benefits are overwhelming the state’s economy and taxpayers’ ability to pay for them.

Benefits overwhelm economy, taxpayers

Total pension benefits have grown at an annually compounded rate of 8.8 percent over the past three decades, or 1,061 percent in total.

That’s six times more than the state’s revenue growth over the same time period, eight times more than median household income growth; and nearly ten times more than inflation.

That’s not normal. Don’t let any politician or union official tell you otherwise.

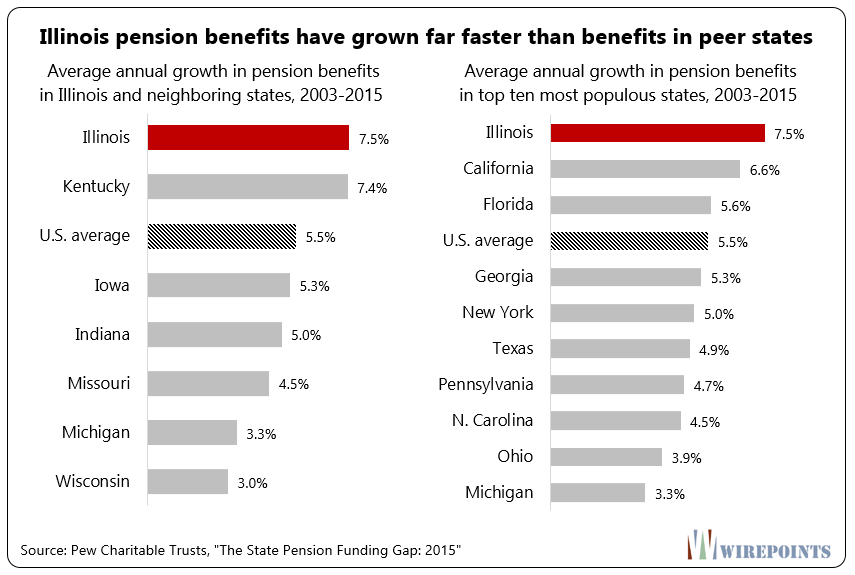

Illinois’ pension growth is an outlier among states. In fact, Illinois’ benefits grew the third-fastest of any state between 2003 and 2015 according to data we analyzed from the Pew Research. Only New Jersey and New Hampshire’s pensions grew faster.

The growth in promised pension benefits has been extreme by any measure. They’ve grown multiple times faster than Illinoisans’ ability to pay for them.

Yet the media, lawmakers and unions still blame the current crisis on “underfunding.”

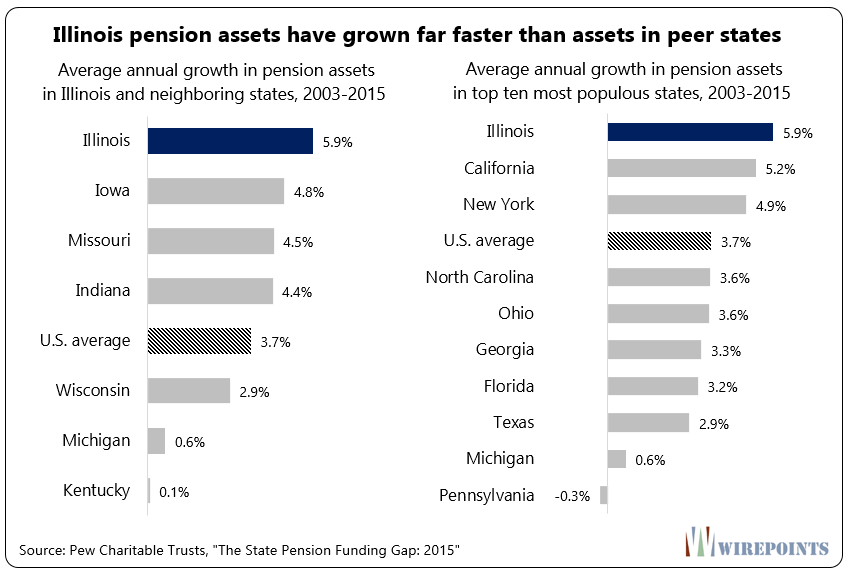

What they don’t mention is that Illinoisans have put a lot into pensions already.

Pension assets have grown 7.2 percent a year for three decades, or 644 percent in total. They’ve grown five times more than household incomes over the entire period and nearly six times more than inflation.

Between 1996 and 2017, taxpayers put $24 billion more into pensions than what Gov. Jim Edgar’s 1996 pension plan, “the Edgar ramp,” originally asked for.

Those additional contributions helped Illinois pension assets grow the seventh-fastest in the nation between 2003 and 2015.

What this means is Illinois’ out-of-control pension crisis wasn’t inevitable.

If pension benefits had simply grown at the more moderate rate of 5.4 percent – still more than twice the rate of inflation – from 1987 on, Illinois pensions would be fully funded today. There would be no crisis.

Fixing the crisis

Politicians and unions should stop trying to guilt Illinoisans into paying more to pensions through ever-higher taxes. The real problem is, and always has been, the enormous growth in benefits that politicians promised to workers.

If Illinois is to regain control of its finances, retain its taxpayers and grow its economy, pension liabilities need to be cut significantly.

But with recalcitrant unions and an inflexible constitutional clause standing in the way, Illinois lawmakers must employ a new tactic.

Pension benefits themselves are untouchable, but lawmakers can still freeze salaries, reduce headcounts, cut the subjects of collective bargaining and pass bankruptcy laws in order to cut down on future payouts.

Illinois’ government unions will then have a choice. They can either negotiate with lawmakers to restore those cuts in consideration for a reduction in pension benefits, or they can live with the changes.

It’s time to end the narrative that forces taxpayers to shoulder the entire burden of fixing the pension crisis. That’s the start to restoring the balance between the state’s pensions and the Illinoisans who pay for them.

Download PDF of the full report View the report’s key findings

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

next up– is taxing retirement income– 401ks, ira’s & ss. all other revenue sources are max out. will love to see the cc dems & apologists- guilt trip the tax payer spin that one.