By: Mark Glennon*

Home values in Illinois have lagged behind national averages in recent years, but the staggering total dollar cost to homeowners is never calculated.

Today, we’ll put some numbers on the aggregate amount forfeited by homeowners and discuss the cause. We will do that by comparing home values here to national averages over the last ten years. That is, how much worse off are homeowners here than if their homes had appreciated at the national average?

We start with Chicago because the data for it are more complete than for the rest of the state.

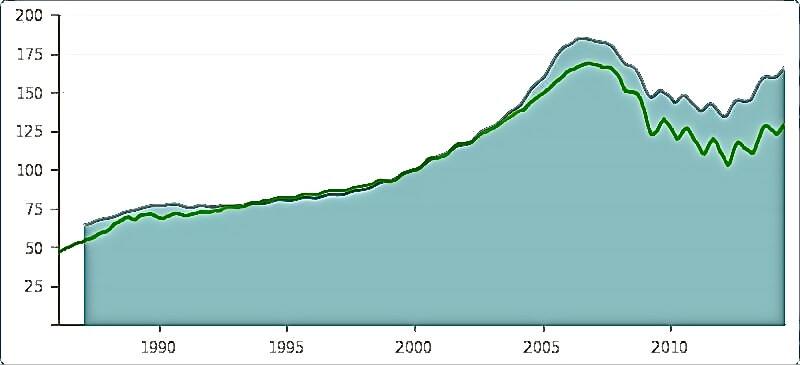

The most respected measure of changes in home values is the S&P/Case Shiller Index, which measures monthly and yearly changes for major metropolitan areas and the nation as a whole. Its Chicago metropolitan index shows that prices have declined by about 6% while its national index has risen by about 17% over the last ten years.

The chart to the right shows that comparison.The top line is the national average and the bottom line is Chicago.

In other words, Chicago homeowners on average are about 23% worse off than if their homes had appreciated at the national average rate since 2004.

Now, what is the total value of all homes in Chicago? Two sources are available.

First, the Civic Federation annually studies the full value of residential property excluding apartments in Chicago. Their total value in 2004 was about $163 billion and is $152 billion according to its most recent study for just the City of Chicago. That’s a decline of about 6.7% — very close to what Case-Shiller says. So, if Chicago homes had instead appreciated at just the national average rate of 17% the total would be 191 billion, or $39 billion more than today.

That’s a massive hit that Chicago homeowners have suffered. For a little perspective, the total budget for the City of Chicago is only about $9 billion.

It may be much worse than that. The Civic Federation works off appraised values for property tax purposes. It estimates the full value of property by dividing the median level of assessment into the total assessed value. That method probably produces total values that are lower than true market values for both 2004 and now.

Another data source is Zillow, which has recently begun estimating total home values for major metro areas. It estimated total home values for the entire Chicago metro area at $687 billion at the end of last year. From July 2004 to August 2014, Zillow’s data say home values in the Chicago metro area dropped 17% while the nation’s rose 7% — a 24% difference. Those numbers seem exaggerated and their methodology is not as sound as Case-Shiller’s. But by those numbers homeowners for the entire Chicago area may have lost out on over $165 billion of appreciation.

For the rest of the state, total home values are not available so we cannot make the estimate directly, but there’s no reason to think that the story is any different than Chicago. Case-Schiller does not calculate values for the whole state, but Zillow says home prices overall for Illinois are down 10% for the last ten years while their national average is up 7%, a difference of 17%. Unquestionably, Illinois homeowners outside of Chicagoland have also lost out on tens of billions, probably hundreds of billions, of dollars of appreciation.

None of these numbers is exact and there are questions about the methodology that might be fair, but they would not materially change the conclusion: Had Illinois homes appreciated over the last ten years at just the national average rate, homeowners would be tens of billions — probably hundreds of billions — better off.

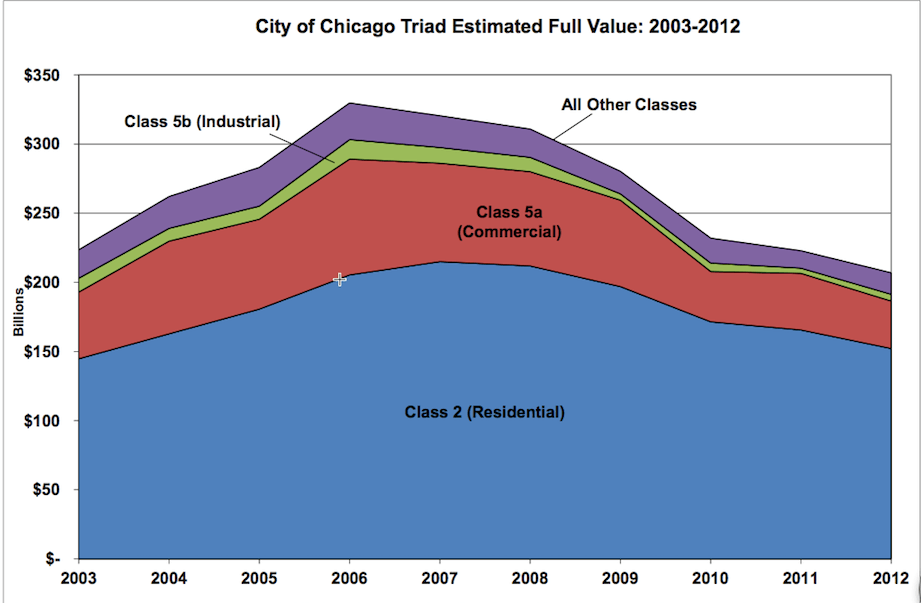

Owners of other properties — apartments and commercial — probably have suffered a similar fate. While downtown commercial property has recovered nicely, the Civic Federation analysis shows that the decline in values since 2004 is fairly similar for all property classes, as shown on the right.

Now, why have home values in Illinois suffered so badly compared to the rest of the nation? Isn’t it safe to think the answer is failed government, both state and local?

High property taxes, flight out of the state, unwillingness to invest in a weak local economy, the income tax increase, half of Illinoisans telling pollsters they want to leave, corruption, crumbling infrastructure, chopped spending on social services, class warfare, loss of faith in the property tax assessment process, overhang of massive liabilities for unfunded pensions…. Surely these are primary causes and bad government is at the core of each of them.

There’s nothing inherently wrong about Illinois that would provide a different explanation or excuse, except perhaps the weather, and we’ve always had that. We have splendid assets — great universities, transportation facilities, central location, major corporate headquarters and the like, but those are all legacy assets that today’s government inherited.

High and growing property taxes are certainly the primary cause of the lag in Illinois home appreciation. Unquestionably, high property taxes directly suppress property values, and Illinois now has the second highest property taxes in the country, according to the Urban Institute.

Importantly, there is a major upside to suppressed home prices, provided you are not a homeowner: Illinois is increasingly inexpensive, especially Chicago, which is very cheap compared to other major international financial centers. That affordability no doubt accounts for the popularity of Chicago among young professions, which is one of our few bright spots.

Depressed home prices may even help stem the flight out of Illinois. As discussed in a recent Crain’s article, homeowners thinking about selling out and heading to the Sunbelt might find that to be an expensive proposition.

Decide what you want about the benefits of making Illinois a cheaper place to live, but make no mistake: Homeowners have paid an astronomical price to make it cheaper.

*Mark Glennon is founder of WirePoints.

*****************************

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

That last comment on stemming the flight out of Illinois isn’t really accurate. If real estate taxes go up, they will push down home prices. But the total monthly payments might not change. Monthly payments are what most homeowners care about: principal, interest, taxes, etc. So an increase in real estate taxes is pretty much a total loss from a seller’s perspective, and a buyer should be neutral if home prices fall accordingly.

My homes value has gone down 55% since the housing crash. It continues to go down every month. WHILE property taxes have gone up every assessment because of the formula and the multiplier that is rigged to feed the beast called IL govt. If I could move I would but I can’t sell it for even CLOSE to what I paid for it 29 years ago.