-- Connecting the dots between our economy, government and business --

-- Connecting the dots between our economy, government and business --

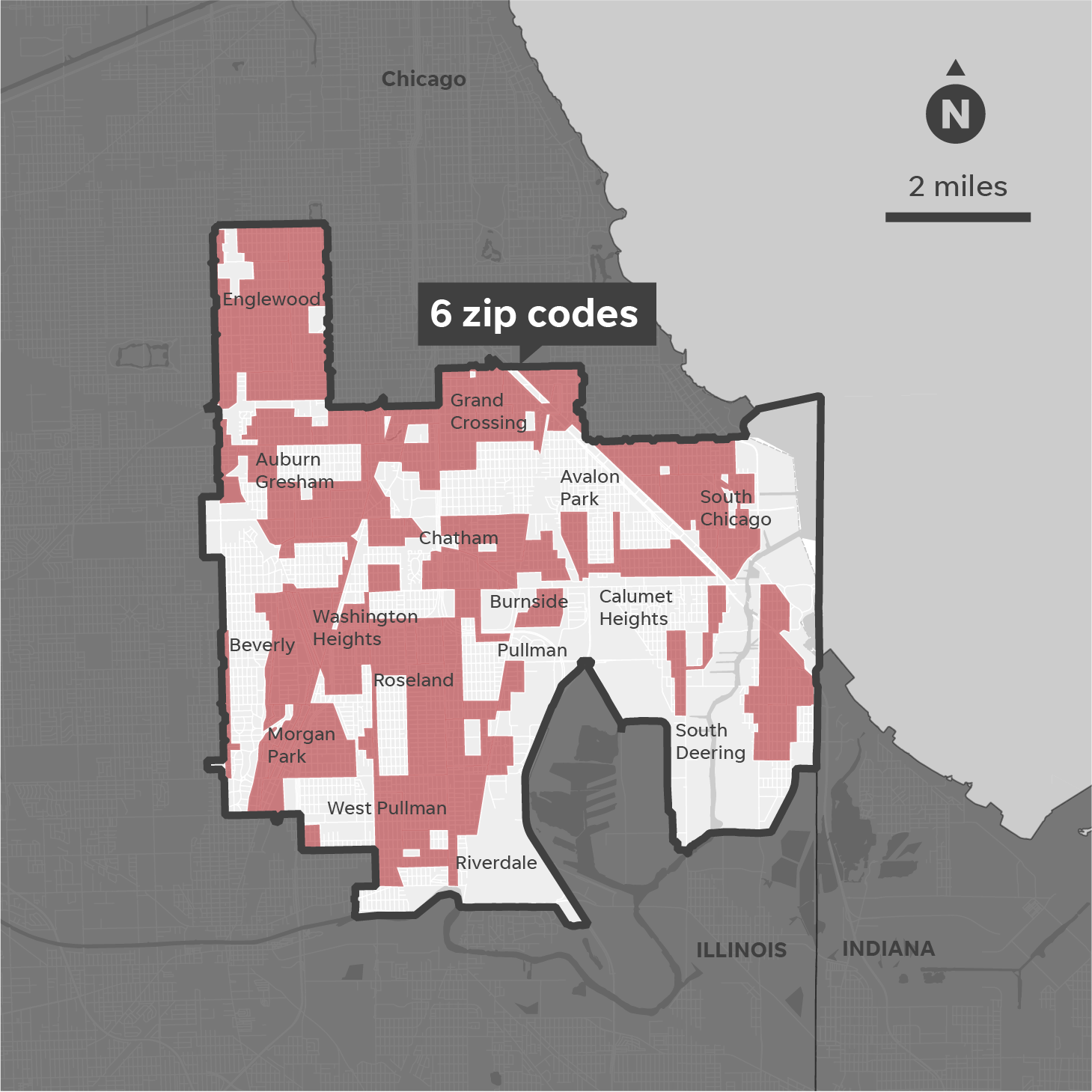

Chicago among the places hardest hit. "The scar reverse mortgage failures leave on neighborhoods can be seen on a drive through Chicago’s South Side with longtime resident and community organizer Pat DeBonnett. A cluster of six ZIP codes together have endured more than 1,000 reverse mortgage foreclosures over the past five years – higher than many entire states. Boarded up homes and empty parcels followed."

Chicago among the places hardest hit. "The scar reverse mortgage failures leave on neighborhoods can be seen on a drive through Chicago’s South Side with longtime resident and community organizer Pat DeBonnett. A cluster of six ZIP codes together have endured more than 1,000 reverse mortgage foreclosures over the past five years – higher than many entire states. Boarded up homes and empty parcels followed." Chicago’s political leadership is floating a pension buyout program as evidence it is seriously addressing the city’s thirty-six-billion-dollar unfunded pension liability, but Mark Glennon, founder of the Illinois policy research organization Wirepoints, said that the proposal moves debt from one column to another rather than reducing it, and that the broader fiscal picture facing the city continues to deteriorate across every measurable dimension. Audio here.

Expect no retraction or apology. This what they do.

Expect no retraction or apology. This what they do.

The state’s existing buyout program for its own pensions is the precedent for Chicago, which should be a warning: Look out for similar exaggerated claims and shoddy analysis.

The state’s existing buyout program for its own pensions is the precedent for Chicago, which should be a warning: Look out for similar exaggerated claims and shoddy analysis.

SIGN UP HERE FOR OUR FREE WIREPOINTS DAILY NEWSLETTER

So Magnum P.I. and Fonzie have been lying to us all these years?!

I read this article with much interest noting that it is an apparent attempt to try and turn the reality into one of racism. I too have witnessed the same situation in other areas not just the cherry picked ones selected by the authors at USA Today. The common denominator, as pointed out, in many of the situations is written “When they missed a paperwork deadline or fell behind on taxes or insurance, lenders moved swiftly to foreclose on the home.” The borrowers in these cases have not protected the collateral, their now mortgaged homes, as they agreed to do.… Read more »

Years ago I was in a county treasurer’s office and there was an old lady in front of me at the counter. She was there to ‘investigate’ – from her perspective I guess – her back taxes bill. She kept saying that she didn’t understand why her back taxes were tens of thousands of dollars. She repeated like four or five times to the lady behind the counter that her 30 year mortgage was paid off years ago, she didn’t understand why she owed all this money because her mortgage was paid off. The lady behind the counter didn’t really… Read more »

So, the likely remedy is require more pages of disclosure forms to be signed or initialed at closing to “prove” she was informed by the lender. What happened to the presumption that a citizen knows the law? … or that they read their mail?

To be sure, the Nanny State provides us with seat belts and safer meat and medicines. I guess my essential issue is with written disclosures that nobody reads. We need 10,000 more MSWs to go to closings and ‘splain stuff in “plain English” or whatever the operative language of the borrower may be.

The remedy is to ban reverse mortgages entirely. They’re a defective product that is causing losses for the federal government that guarantees them, like the article says “Reverse mortgages are insured by a Federal Housing Administration fund, which is in the red more than $13.6 billion” The only reason these products exist is because the federal gov. insures against the stupidity of borrowers. $13.6 billion would solve Chicago’s budget gap 13x over. Instead it’s going to lenders who made foolish loans to dumb people who can’t be bothered to pay the taxes or insurance on their paid off homes. End… Read more »

These are terrible financial products, sold to desperate and unknowledgeable people. This reminds me of the option plus mortgages or whatever silly brand names outfits like Countrywide were calling their toxic loan products where people could choose their payment, with any monthly shortfall in principal being added to the amount of the loan, and where they could only work with massive and unheard of increases in the housing market. Lots of allegations of racism with these loans as many were sold in Hispanic areas of Southern California. The truth is that money must be treated well, or it leaves its… Read more »

Worse than loans to go to college? I like your fix prospectively however if lenders need to be bailed out again on the basis of having made loans to unwise borrowers, well … at least the borrowers can go bankrupt. How much equity do most borrowers have these days, anyway? If, in fact, the collateral is concentrated in poor neighborhoods, it begins to sound like Detroit revisited. Banks won’t want to foreclose and not many taxes can be extracted from abandoned homes. Time to re-read some books on the Dust Bowl.

So then are you asserting that people that do not understand real estate taxes are allowed to vote on them?

(just asking)

hahahah