By: Ted Dabrowski and John Klingner

J.B. Pritzker ran for governor on a generic proposal to implement a progressive income tax in Illinois. Despite calls from the media to release the details of his plan, he repeatedly refused to discuss any specifics.

In response to the lack of details from Pritzker, Wirepoints has calculated what a realistic progressive tax plan could look like. We took estimates of Pritzker’s promised spending plans from the media and combined it with Illinois’ income tax data. He won’t like what we found.

Pritzker’s dual campaign promises – to increase state spending by billions and at the same time protect Illinois middle-income workers from an income tax hike – are simply impossible to keep. The math says so.

No matter how you run the numbers, the progressive tax rates needed to fund Pritzker’s $10 billion-plus in new spending would be harmful. They’ll punish the wallets of both the middle class as well as the wealthy.

Residents were just hit with a 32 percent income tax increase a little over a year ago. They already pay some the highest state and local taxes in the county, including the nation’s highest property taxes. Pritzker’s promises would only add to that burden.

Spending billions more

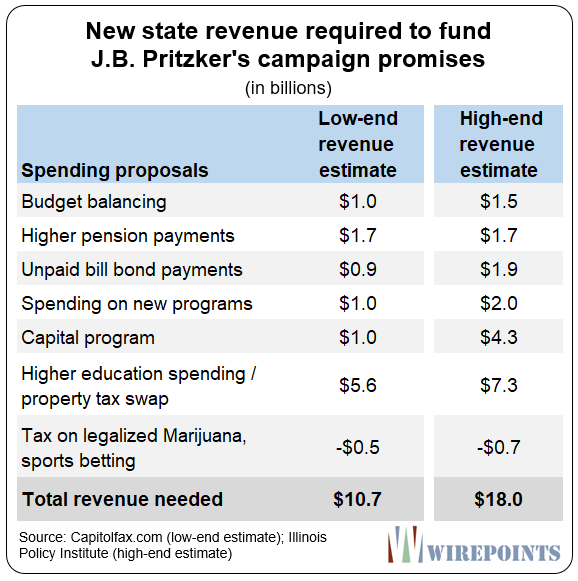

Pritzker wants to increase Illinois’ annual budget by at least 25 percent, spending billions more on everything from education to health care and from pensions to roads. Estimates for Pritzker’s new revenue demands range from Rich Miller’s $10.7 billion to the Illinois Policy Institute’s $18 billion.

And while he campaigns to spend billions more, Pritzker also promises not to hit middle- and working-class Illinoisans under his hoped-for progressive tax scheme (Illinois must amend its constitution to convert the state’s flat income tax structure to a progressive one).

Pritzker has said: “A fair income tax will raise taxes on people like Bruce Rauner and me to support education and help solve the state’s budget problem, while reducing the burden on the middle class.”

But Pritzker can’t just tax wealthy residents like himself and Rauner to pay for all his promises. There are simply not enough wealthy people in Illinois to do so.

It would take marginal rates higher than California’s top rate of 13.3 percent – the highest in the nation – to get the revenues that Pritzker’s promises require. Not many wealthy Illinoisans will stick around to pay such exorbitant rates.

(Im)possible progressive tax scenarios

Wirepoints ran three separate progressive tax scenarios to see how Pritzker’s promises might work out. In all our calculations, we assumed Pritzker will require $10.7 billion in new taxes, the low-end estimate of his promised new spending. (See Appendix 1 for a full list of Wirepoints’ assumptions.)

The first scenario takes Pritzker’s promise at his word – that he’ll only hike taxes on the rich while protecting all other residents from a tax hike. That creates an extreme and improbable case of only two tax brackets: one for filers with millionaire incomes and one for everyone else. It’s a case that can be easily discarded as a nonstarter.

Wirepoints’ second scenario pushes higher tax rates further down the income ladder while still protecting the middle class – those with taxable incomes below $150,000 – from a tax hike. Unfortunately for Pritzker, the marginal rate on residents with incomes above $150,000 remains punitively high in this case. This scenario, too, can be easily discarded as unrealistic and unworkable.

While it’s obvious that Pritzker would never actually propose either of the two above structures, both illustrate the danger of campaign rhetoric that demands “the rich” pay for everything. Such promises can only go so far before they crash into financial reality.

To construct a plan that was more realistic, Wirepoints was forced to use even higher tax rates further down the income ladder. In our third tax scenario, all filers with incomes above $50,000 pay higher taxes. This shows the truth about Pritzker’s promises – that he can’t get all the revenue he wants without creating a progressive tax scheme that raises taxes on the middle class.

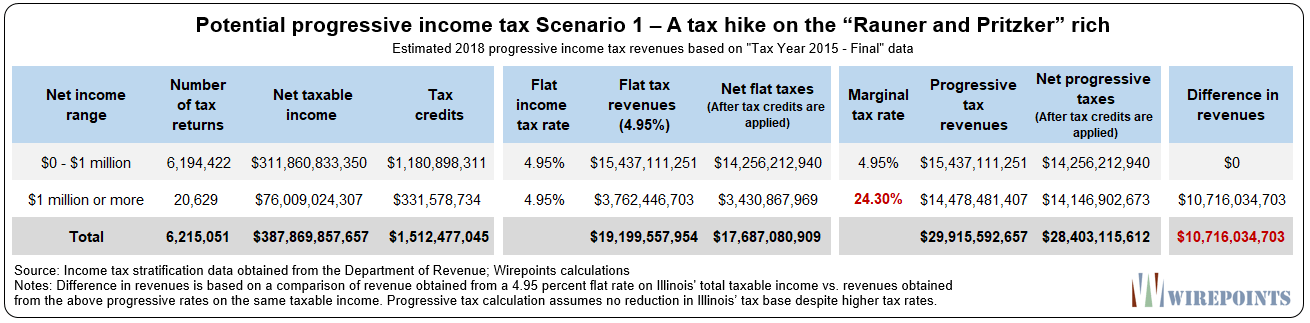

Scenario 1 – A tax hike on the “Rauner and Pritzker” rich

First of all, let’s get out of the way Pritzker’s promise to only raise taxes on the rich people “like Bruce Rauner” and himself. It’s clear from Illinois’ tax data (see Appendix 2) that Pritzker’s promise cannot be part of any real proposal. There simply aren’t enough wealthy Illinoisans.

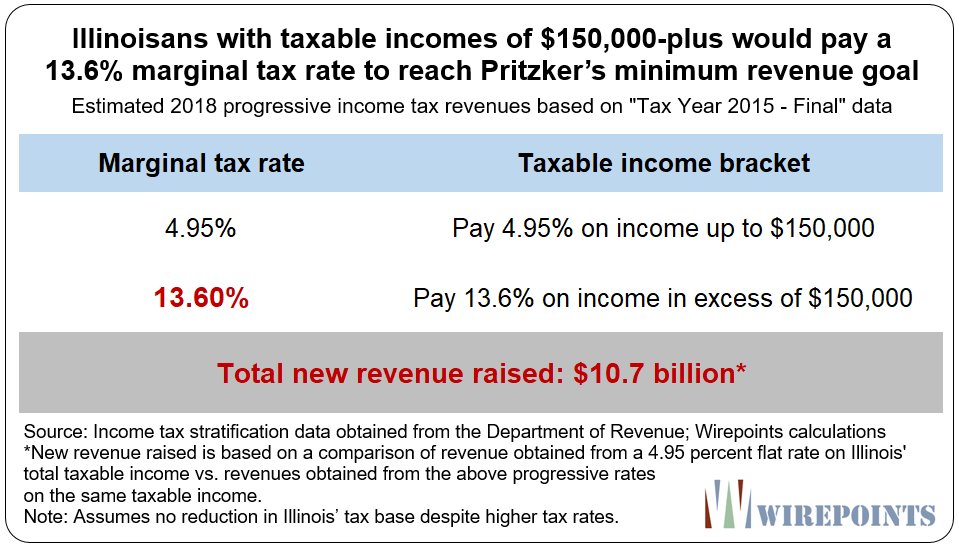

If a progressive tax structure only raised taxes on the truly wealthy – just those with incomes of $1 million or more a year – then Illinois’ top tax income rate would have to reach an absurd 24.3 percent to generate Pritzker’s $10.7 billion in new revenues. That’s almost double California’s top rate of 13.3 percent. (See Appendix 5 for revenue breakdowns by income bracket.)

Obviously Pritzker would never propose something so extreme, but this scenario does serve to exemplify why targeting only Illinois’ wealthiest residents won’t work. Pritzker’s promise to tax only millionaires and billionaires like himself is easily dismissible.

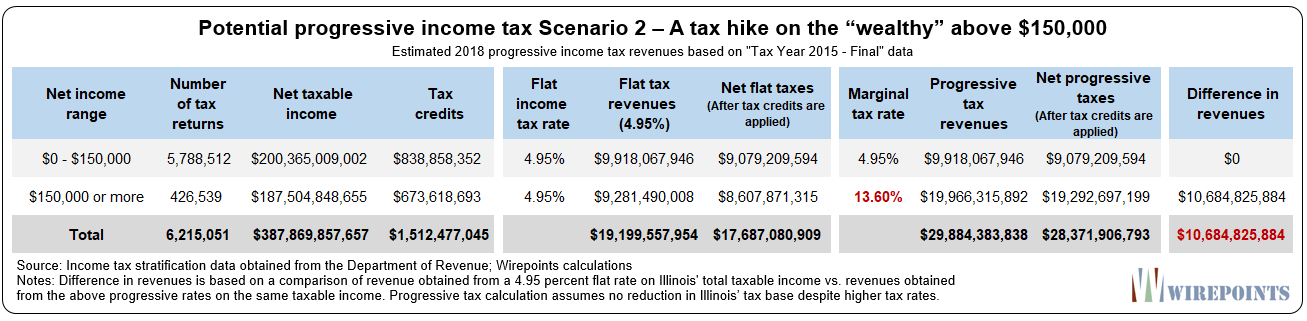

Scenario 2 – A tax hike on the “wealthy” above $150,000

Even if the definition of “wealthy” is pushed far down the income ladder, Illinois’ income tax rates would still have to be punitively high to raise Pritzker’s required new revenue.

For example, take another simple two-tier progressive tax structure that treats all those earning more than $150,000 as “wealthy.”

The structure’s first bracket would continue to protect all filers with taxable income less than $150,000, keeping their taxes at the current 4.95 percent rate.

That means the remaining filers – those “wealthy” residents with taxable income above $150,000 – would all be forced to pay a marginal tax rate of 13.6 percent. That’s higher than California’s highest marginal rate of 13.3 percent.

The big difference: California’s 13.3 percent is only levied on income in excess of $1 million. Illinois would have to apply its 13.6 percent rate on single and joint filers making more than $150,000 to reach Pritzker’s revenue goals.

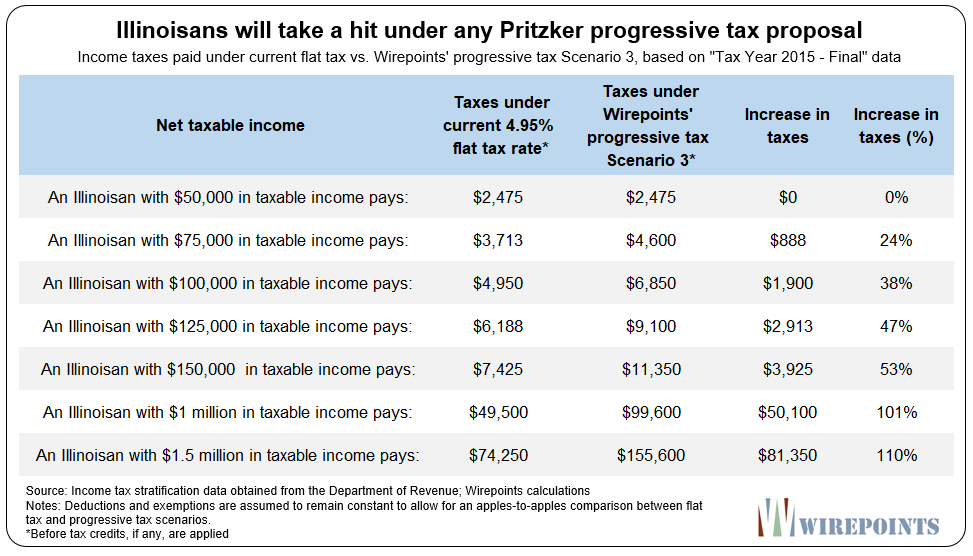

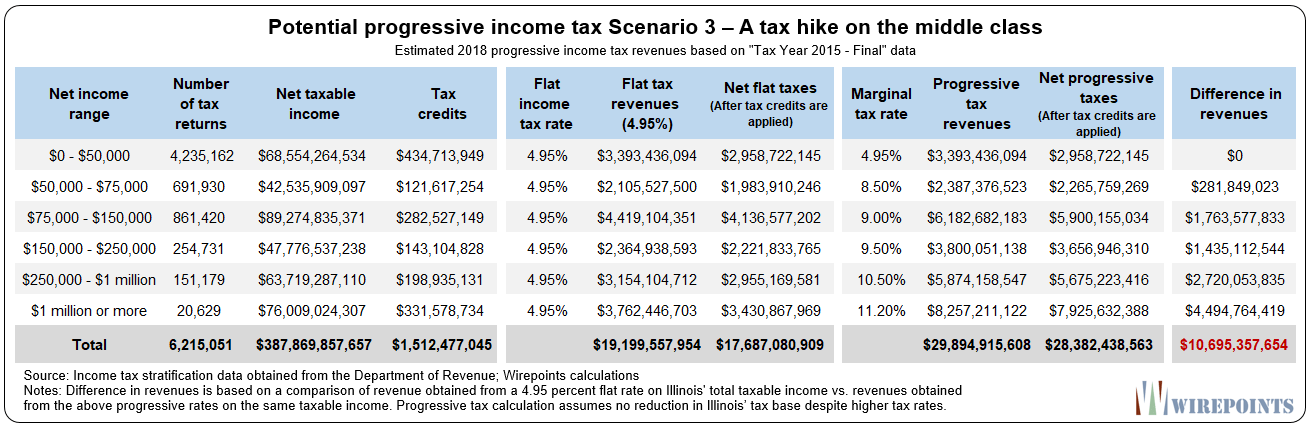

Scenario 3 – A tax hike on the middle class

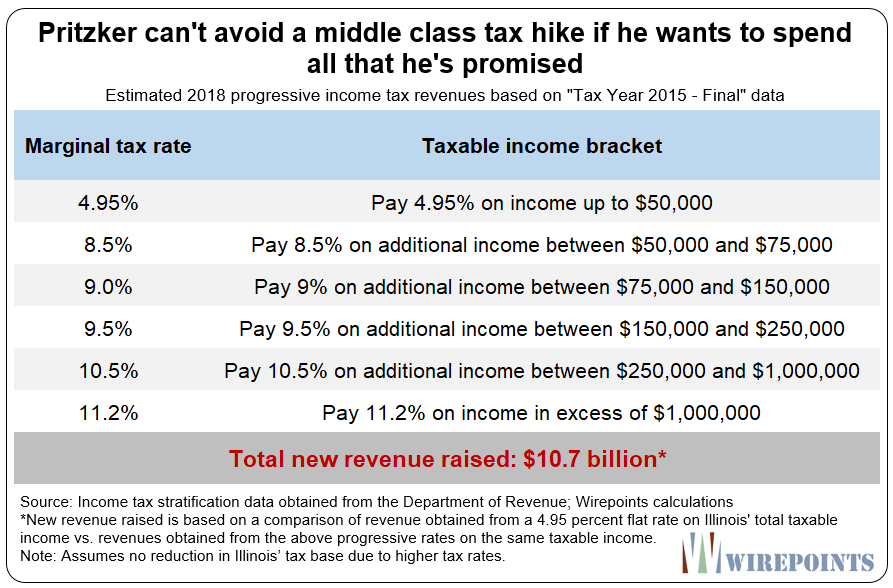

Finally, let’s look at a scenario that shows the truth about Pritzker’s promises – that he can’t get all the revenues he wants without creating a scheme that hits everybody, including the middle class.

In this case, the progressive tax structure has six brackets to help make the tax hikes less extreme. The lowest bracket has a marginal rate of 4.95 percent, protecting all single and joint filers with taxable incomes below $50,000 from a tax increase.

After that, tax hikes start hitting the middle class. Additional income between $50,000 and $75,000 would be taxed at a 8.5 percent rate. And additional income between $75,000 and $150,000 would be taxed at an 9 percent rate. The marginal rates only go up from there, reaching 11.2 percent in the top bracket, the second highest top rate in the nation after California’s 13.3 percent.

In practical terms, that means single and joint filers with more than $50,000 in taxable income will pay higher taxes.

For example, an Illinoisan with $75,000 in taxable income will pay nearly $900 more in taxes, up 24 percent compared to the current flat tax. That’s on top of the 32 percent income tax increase he or she got hit with just last year.

And for two married, career teachers earning a combined $138,000 in taxable income (the average Illinois teacher salary is nearly $71,000 according to COGFA), the progressive scheme would hike their taxes 50 percent, to $10,270 a year, from their current $6,831.

The above scenario is, of course, just one of an infinite number of potential progressive tax structures. One can play around with the brackets and the rates a lot. But the fundamental problem remains the same: Pritzker can’t realistically collect $10.7 billion in new revenues just by hitting the wealthy. There is no scenario where that works. He’d have to break his promise and impose higher taxes on the middle class to pay for all his promised spending.

Millionaire outmigration

The above scenarios are actually generous to Pritzker. They don’t take in account the reality that many wealthy and ordinary residents will leave rather than pay such high rates.

It would be especially devastating if Illinois’ limited number of “Rauner” and “Pritzker” wealth-level residents left. When they go, a large portion of Illinois’ tax base goes with them. New Jersey and Connecticut are perfect examples of what happens when states chase out their biggest taxpayers. Those states lost billions in taxable income when just a few uber-wealthy residents left.

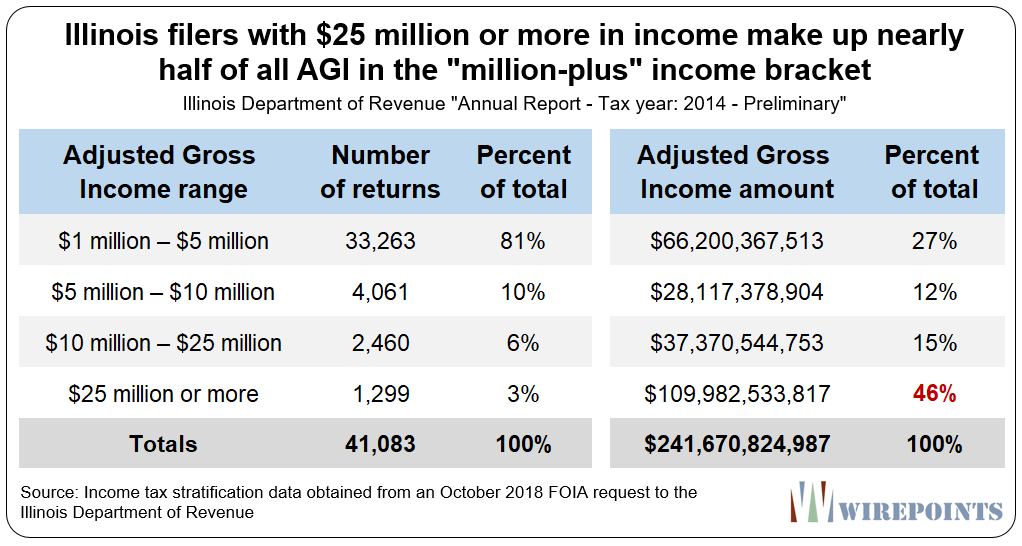

In Illinois, approximately 600 filers make half of the $76 billion in taxable income earned by the “$1 million or more” bracket. (See Appendix 5 for the assumptions behind this calculation.)

A loss of just some of those top filers to other states would seriously dent Illinois’ tax base. For example, if just 20 percent of the net income in the “$1 million or more” bracket disappeared, Pritzker’s progressive tax plan would lose about $1 billion of what he needs to raise. That loss would require politicians to increase tax rates yet again to reach Pritzker’s desired revenues, creating a vicious cycle of more outmigration and higher taxes.

Focus on reforms, not a progressive tax

The reality is that Pritzker’s promises – to spend billions of additional dollars and to only tax the rich – simply won’t work. They’re a distraction that’s taken attention away from what’s really needed to fix Illinois: comprehensive spending reforms.

Illinois politicians should be showing how they’ll bring the cost of government in line with what Illinoisans can afford, not promising to grow their tax burdens further.

****************************

Appendix 1: Assumptions

- Wirepoints assumed a single progressive tax structure for both single and joint filers.

- To create a base case for comparison, Wirepoints applied the 2018 flat tax rate of 4.95 percent to the latest full year of final, net taxable income (2015) from the Illinois Department of Revenue, obtained via an Oct. 9, 2018 FOIA request.

- All progressive tax revenue scenarios are compared to the above flat-tax base case. Those scenarios were also calculated using the latest full year of final, net taxable income (2015) obtained from IDOR.

- Deductions, exemptions and tax credits are assumed to remain constant to allow for an apples-to-apples comparison between flat tax and progressive tax scenarios.

- Wirepoints calculated its progressive tax scenarios based on Pritzker’s “required” $10.7 billion in new tax revenues, the low-end estimate of his campaign promises. Bigger revenue demands would require even higher progressive tax rates than what Wirepoints calculated in its base cases.

- Wirepoints assumes no new tax breaks for the middle and lower incomes. If implemented as promised by Pritzker, tax breaks would require even higher progressive tax rates than calculated.

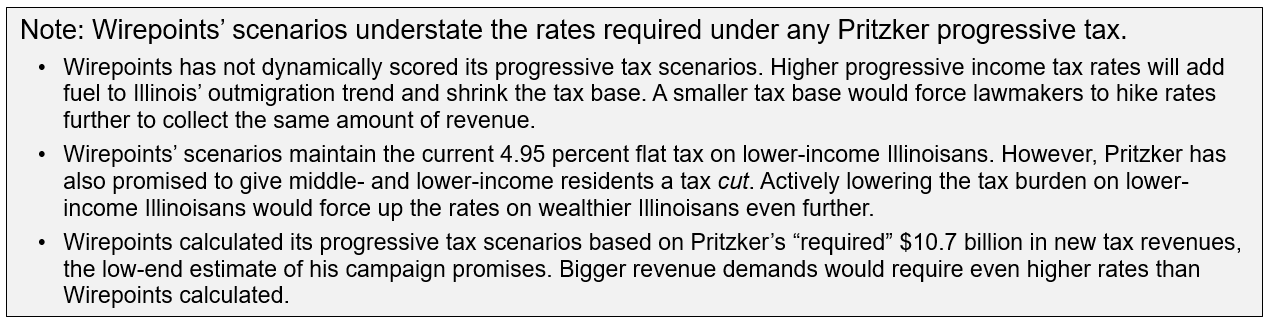

- Wirepoints assumes no reduction in Illinois’ tax base despite the higher marginal rates under a progressive tax scheme. Depending on how many wealthy Illinoisans actually leave, progressive tax rates will have to be even higher than calculated to achieve Pritzker’s revenue goals.

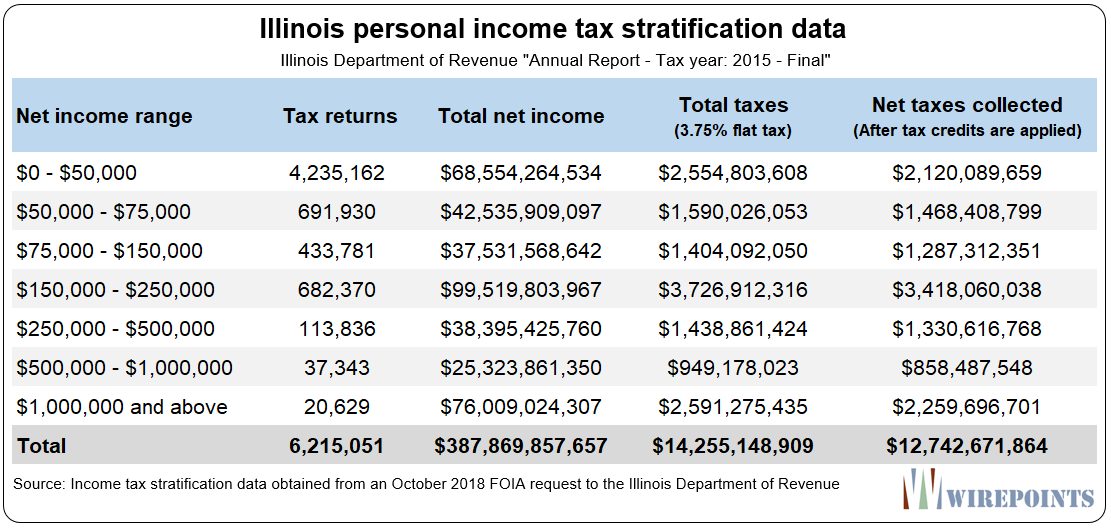

Appendix 2: Illinois income tax stratifications

According to the latest, finalized data income tax data from the Illinois Department of Revenue, Illinois had over six million income tax returns filed in 2015 with a combined total net taxable income of $388 billion reported. Illinois’ flat income tax of 3.75 percent brought in $12.7 billion in net revenues that year.

The below brackets and net (taxable) income totals are used as the basis for calculating revenues under Wirepoints’ progressive tax scenarios.

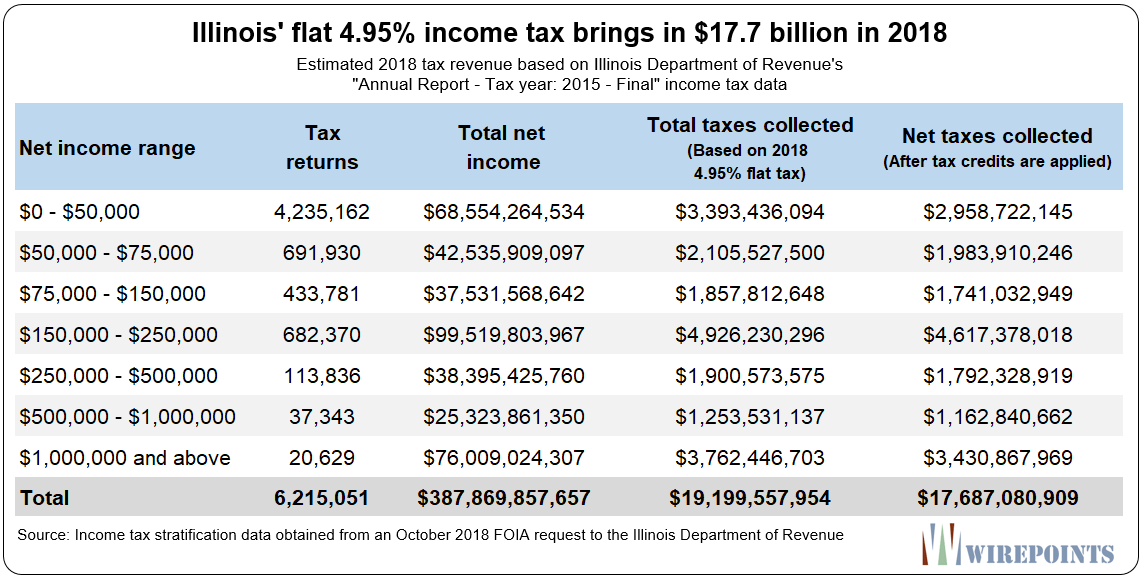

Appendix 3: 2018 flat income tax revenues

Applying Illinois’ 2018 income rate of 4.95 percent to the latest, finalized data from the Illinois Department of Revenue (see Appendix 2) results in net tax revenues of $17.7 billion dollars. This amount serves as the comparison base for all other progressive tax revenue scenarios included in this piece.

Appendix 4: Details of Wirepoints’ progressive income tax scenarios

Below is a breakdown of the net income brackets and the tax revenues generated by each progressive tax scenario.

Appendix 5: Breakdown of incomes $1 million and above

The Illinois Department of Revenue did not provide Wirepoints with a detailed breakdown of those earning more than $1 million in its 2015 net taxable income table.

As a proxy, Wirepoints used Illinois’ 2014 adjusted gross income (AGI) tax bracket data, which included the “$25 million or more” bracket. That bracket has just 3 percent of the total filers in the broader “$1 million or more” bracket, but makes up nearly half of the broader “$1 million-plus” bracket’s total AGI.

Wirepoints applied that 3 percent share of filers to Illinois’ 2015 tax data to arrive at an approximate 600 filers with net taxable incomes above $25 million (3 percent of the 20,629 filers in the 2015 “$1 million or more” net income bracket).

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

Can’t get blood from a turnip. Take a look at Chicagos latest demographics.

https://www.breitbart.com/politics/2019/02/25/study-chicagos-middle-class-almost-gone-majority-either-rich-or-poor/

In light of the fact that cities in Illinois do not impose income tax on top of the state rate, as they do in many other states, combined with the fact that a considerable portion of the $10.7 billion revenue increase will be used to reduce property taxes, the (likely realistic) tax rate structure you outline in scenario 3 appears quite reasonable compared with other jurisdictions. For example, a single individual earning $100,000 per year in New York City pays a marginal tax rate of 10.526% (6.65% state and 3.876% city). A similar individual in Washington DC pays 8.5%. So… Read more »

1) Only 15 states have a city income tax, most of those their rates are quite low, and all are in states with very low property taxes. 2) A single individual earning $100,000 in NY is like someone making $60,000 here. Are you saying someone making $60,000 in IL should pay 10.5% income taxes?! 3) Washington DC’s property tax rate is a half-percent, nearly 5x lower than IL. A person earning $300,000 who owns a $500,000 house in DC has the same total tax burden (income and property) as he would in suburban Chicago. Will our property taxes drop to… Read more »

nixit, you cracked me up with your retort. What a hilarious and factual post – thank you.

This

I think you will see Pritzker try to make money from legalizing pot, legalizing sports betting,

AND allowing the city of Chicago to establish a gaming district near downtown.

After all of that is factored in, the burden on the income tax will be reduced significantly.

California shows that revenue coming from legal marijuana was ummmm disappointing as everyone looked at the prices charged by the licensed outfits shrugged and went their usual supplier.

gambling is a tapped out market see this.

https://features.propublica.org/the-bad-bet/how-illinois-bet-on-video-gambling-and-lost/

Lowering property taxes if the income tax is passed? Good luck with getting the propert tax lowered. The issue is uncontrolled spending and no matter how you slice it…a total tax burden hike is the issue…not how it is derived

I still say that you will see toll booths on Michigan Avenue sidewalks in the near future.

Remember, no SALT write off for income or property taxes as well.

You can deduct up to $10,000.00 per year.

Can someone explain how in 2014, there were 41,083 $1 million-plus tax returns with over $241 Billion in total income in 2014, but only 20,629 $1 million-plus tax returns with only $76 Billion in income in 2015? That’s a huge difference and has big implications for this analysis. Thanks!

Rob, the two tables deal with different measures of income, that’s why they’re so different.

The 2014 table uses “Adjusted Gross Income,” which is income before state tax deductions and exemptions are applied. The 2015 table, which we use in our main analysis, uses “Net taxable income” which is income after tax deductions and exemptions are applied.

Deductions and exemptions remove a great deal of filers’ gross income. That’s why

the “$1 million-plus” net income bracket is so much smaller than the AGI bracket.

I thought that might be it, but not sure. Thanks!

I would love to see how the breakdown looks for AGI vs net taxable income with respect to the different income ranges. Not sure that my meager salary ever reflected such a great difference between AGI and net taxable. If you could point me toward source data, I would appreciate it! Thanks again!

You can find the income tax bracket data at IDOR: https://www2.illinois.gov/rev/research/taxstats/IndIncomeStratifications/SitePages/IITStratifications.aspx?rptYear=2015

And all of this is to pay for those ridiculous and obscene pensions.

Obscene is a rather mild phrase when you look at the ridiculousness for the Illinois public sector pension system.

Under insolvency circumstances, I believe the progressive taxes are to keep government jobs. This would mean the salaries are being paid with debt.

Rauner should have done this analysis (or paid Wirepoints to do it) a year ago and sent it to every Illinois voter. The numbers don’t lie.

Rauner is a “delegator” not a doer, that’s why he didn’t write this article. He is a huge disappoijtment, I can’t remember a single speech he gave since elected, I can’t remember him as a leader in any way. He made commercials in a home wood shop that had all brand new tools on the walls and no sawdust on the floor or wood scraps on the bench, in a new pressed flannel shirt. That’s not a wood shop, it was to deceive. That commercial says the whole story, he was a fraud. Not really a conservative, he just paid… Read more »

Without too much exposition I’ll just say Rauner always has always been a Democrat and pretty much set IL up for the great fall. I am not sure all of this was not orchestrated. I tend to think the only thing that surprised Madigan is how complacent the residents of IL have been, he got to test the voters resolve and found it wanting, so he no longer needs a thinly republican veneered puppet to do his bidding, he can drop the cloak and have full fledged half-wit Democrat back in charge to do his beckoning. My read is, we… Read more »

I would like to upvote this but it says you must be logged in. How can one log in?

You shouldn’t have to be. We will check it out.

Good to see this exposed. About 26% of Illinois residents are age 62 or over, most of them are exempt from state tax. Considering that the vast majority of other “progressive” tax states do tax retirement income. And pritzker is using them as a model. I believe pritzker has taxing retirement income up his sleeve and not telling us. Adding in that “tax the retired too”revenue, I wonder how much he can lower the overall numbers? Another question… Would taxing retirement income violate the diminishment clause?

There’s no doubt JB will be taxing retirement income. Retirees are the fastest growing segment in Illinois, so JB can’t afford to exclude them if he wants to accomplish anything. Best case scenario for the average retiree: Assume JB taxes half of your retirement income.

Taxing retirement income would not violate the diminishment clause if you taxed ALL retirement income. The state could exempt social security and not violate the clause either as many state employees with a pension pay into social security as well.

Hmmm….would not the accursed IL Constitution forbid taxing the income of public sector retirees, as it would diminish the value?

If you singled out public pensions only, it might be considered a diminishment, but we’re talking ALL retirement income. Taxation after the pension has been calculated isn’t a diminishment.

Imagine the uproar if the widow living on the IRA her husband left her had to pay state income taxes but the retired principal did not. Springfield would be burned to the ground.

Everyone should get the same level of deduction. If half your retirement income is taxable, then only half your paycheck should be too. There was talk last year about making the first $50K of pensions not taxable, and they should give everyone a $50K exemption if that’s the case. What’s fair for one is fair for all.

That’s a valid argument, especially for an avowed progressive like JB. How would he justify giving a $50,000 tax exemption to some retired dude sitting around all day living on his $100,000 pension when some working stiff making $60,000 had to pay full freight in taxes? Me thinks the blue wave millennials with massive student debt won’t take too kindly to that.

How many “retired dudes sitting around all day living on his/her $100,000 pension” do you think there are. I retired in management from a large manufacturing corporation in Illinois, and headquartered in Illinois, and only receive $36,000 in pension. I do know retired grade school teachers that receive $80,000 because they qualified for the 25% increase their last 3 years of teaching. That has since, rightfully so, been substantially adjusted.

Salaries, pensions, taxes are all a never ending circle. Spending is the only solution. Government checkbook balancing is no different than yours or mine.

You blinked your eyes and need to take another look at the magnitude of retired teachers’ pensions. That $80K per year is now over $100K due to the three percent annual compounding. Furthermore, for what many suburban Chicago teachers are currently retiring at, their pension in the first year of retirement is more than $80K.

Taxing retirement income will cause a spike in residents exiting IL. How will that lost tax revenue be recouped? Tax the remaining residents even more. The death spiral continues.

Realistically, that is the best outcome. The sooner the state defaults the sooner we can justly reduce the outrageous benefit packages of the public sector.

By the way this week I was in Nashville, Chattanooga, and tonight Louisville : )

Ah, a soon-to-be-former IL resident – good to get out before Pritzker and the free-fall

I was scouting a new location for a business concept. I just ruled Louisville out. I cannot believe how liberal the downtown is there – flaming democrats who want to help the homeless, green PC this and that..one government handout to business owners after another, crony-capitalism at its finest. No thanks Louisviile, far to liberal for my liking. Nashville seems pretty liberal also. I am strongly favoring Chattanooga but I am going to look at Crossville, Cookville and Knoxville. I have not opened a unit in IL in over 20 years and will not.

You’re best off staying away from Ky. Watch the video linked below. Nashville is liberal, because that’s where all the Chicago ex pats are moving. Haven’t been to Knoxville in quite some time so can’t say what it’s like. There’s plenty of room here in Cincinnati suburbs though.

https://www.pbs.org/video/the-pension-gamble-hzokyh/

In the end the consideration is no state income tax. The plan is to convert as much as I can from IRA and traditional 401K to ROTH status wile keeping the tax rate at the 12% federal rate before RMDs begin thus spending down taxable to pay the taxes on the conversion. What remains will stay in cashflow generating dividends in order to take advantage of the lower dividend tax rate. This means I have to wait for the dreaded Hall tax in Tennessee to fully go away before retiring and becoming a TN resident. It is amazing how much… Read more »

do you have a self directed IRA, or just an IRA? Why convert to a Roth?

The idea is to retire well before age 60 in order to do 401K and Traditional IRA conversions to a ROTH 401K and ROTH IRA(regretfully rolling the ROTH 401K into a ROTH IRA in over to avoid the RMDs on the ROTH 401K). My current marginal tax rate is 32%. Under current law you a couple can convert $101,400 (24,000 standard deduction + 77,400 in income) at the 12% tax rate. So I want to convert as much as possible in order to avoid RMDs, in part to avoid taxation of my Social Security, but also as an estate planning… Read more »