By: Nick Binotti and Ted Dabrowski

Wirepoints recently warned in a Chicago Sun-Times oped that Chicago’s pension mess was going to get worse. As Chicago’s latest annual financial report shows, that’s just what happened.

Chicago’s pension shortfall across the city’s four major retirement funds – Municipal, Laborers, Police and Fire – rose to $37.2 billion total in 2023. That’s a 5% increase from $35.4 billion reported the prior year. Most of the increase is attributed to changes in actuarial assumptions and recent legislation that sweetened the cost-of-living pension benefit for thousands of police and firefighters.

Add in the Teachers Pension Fund’s $15.8 billion shortfall and Chicagoans are on the hook for $53 billion in unfunded pension liabilities. That’s over $45,000 owed per Chicago household to be paid off over time.

The Chicago teachers and municipal pension funds have the highest unfunded liabilities with both just under $16 billion. The police pension fund is next with nearly $14 billion. The fire and laborers pension systems have unfunded liabilities of $5.7 billion and $1.9 billion, respectively.

Chicago’s five largest systems are only 30% funded collectively. Only the Chicago Teachers Pension Fund has a funding ratio above 40%. Chicago’s municipal, police and fire pension systems each have funding ratios around only 22%, among the worst in the country for major pension funds.

Chicago’s pension debt continues to increase slowly and steadily year after year. It’s what we described as a “slow-boil” where Chicagoans are increasingly burdened with higher taxes for the same or less amount of services, disparately impacting the city’s most vulnerable.

Mayor Brandon Johnson Pension Working Group has yet to come up with a plan to cool down that boil. In an open letter to Mayor Johnson and an Oped in the Chicago Tribune, Wirepoints and the Taxpayer Pension Alliance outlined a number of actions the city could take to get some control over the problem.

Here are key measures of Chicago’s crisis we provided to the mayor on January 10, 2024:

Chicago’s pension costs and its unfunded liability make the city the extreme outlier nationally when it comes to the burden it creates on its residents and its budget.

The fixed costs of Chicago’s pension and general debts makes the city uncompetitive vis-a-vis the nation’s other big cities. Those costs will continue to negatively impact taxes and services, further pressuring the city’s out-migration, home values and quality-of-life issues.

Chicago’s pension funds are running out of money and are among the worst funded in the country when measured by the ratio of assets a plan has relative to its yearly payout. Those asset-to-payout ratios have collapsed to single digits over the last two decades, reflecting the funds’ fall towards insolvency. Healthy funds have a ratio of 20 or more.

Chicago can’t increase taxes without inflicting even more damage to its economic competitiveness. Chicago commercial property taxes are already the nation’s highest among big cities.

Chicago can’t increase taxes without inflicting even more damage to its economic competitiveness. Chicago commercial property taxes are already the nation’s highest among big cities.

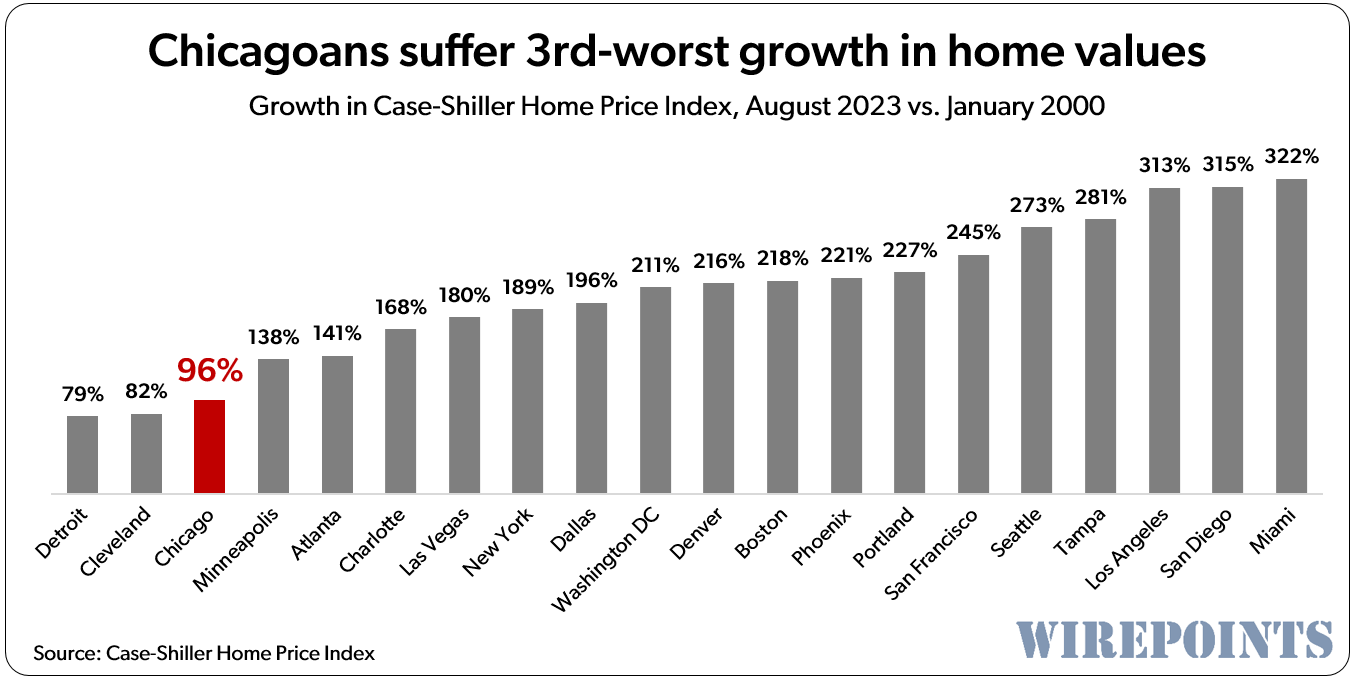

The city’s lack of competitiveness across fiscal and quality-of-life issues, including crime and education, has had a dramatic impact on Chicagoans’ home values. The expectation of higher taxes and cuts in services will continue to put pressure on Chicago home values.

The city’s lack of competitiveness across fiscal and quality-of-life issues, including crime and education, has had a dramatic impact on Chicagoans’ home values. The expectation of higher taxes and cuts in services will continue to put pressure on Chicago home values.

The catch-all impact of the burdens and quality-of-life issues Chicagoans face is reflected by the city’s long-term population decline. When compared to the turn of the millennium, Chicago and Detroit are the only major cities to suffer a loss of people.

The catch-all impact of the burdens and quality-of-life issues Chicagoans face is reflected by the city’s long-term population decline. When compared to the turn of the millennium, Chicago and Detroit are the only major cities to suffer a loss of people.

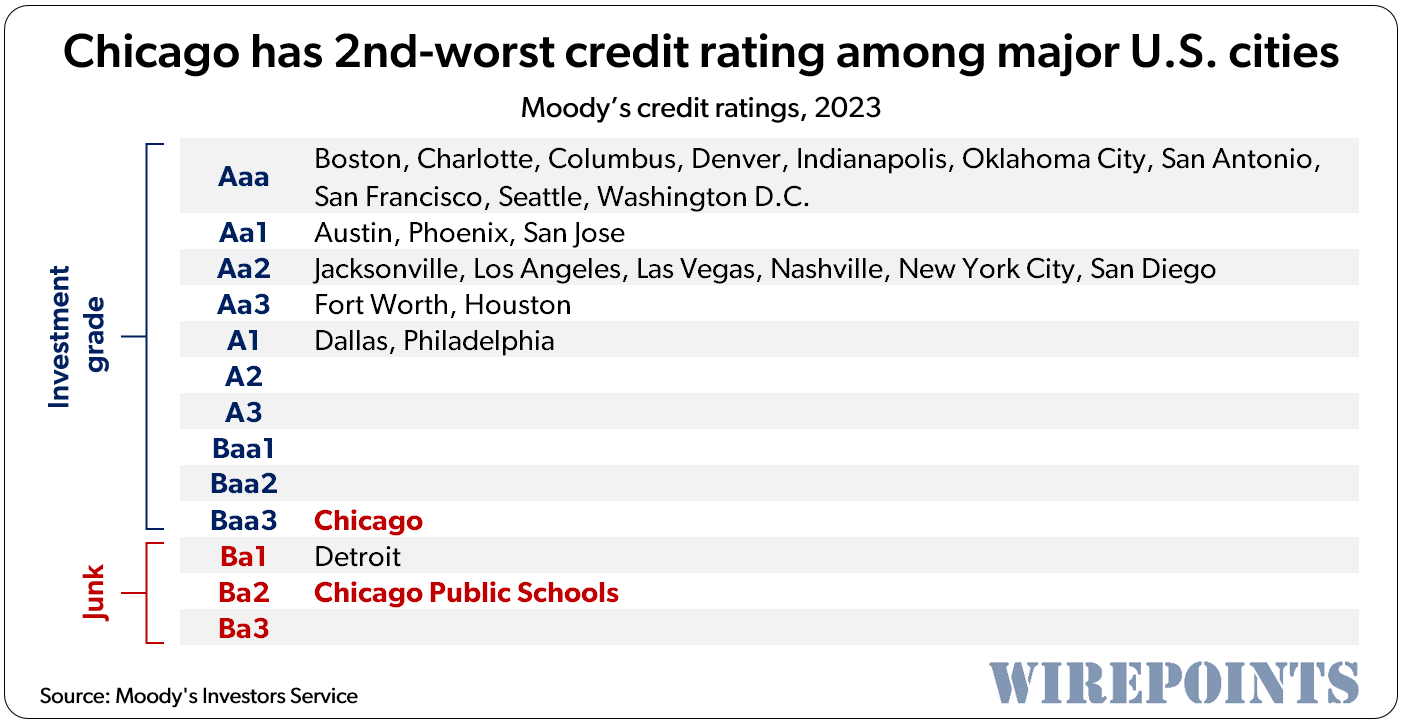

Chicago has the worst credit rating in the country among big cities with the exception of Detroit. Chicago was able to shed its junk rating only because of the billions in federal public and private aid during covid. The city’s pension crisis will reemerge as those federal funds dry up.

Chicago has the worst credit rating in the country among big cities with the exception of Detroit. Chicago was able to shed its junk rating only because of the billions in federal public and private aid during covid. The city’s pension crisis will reemerge as those federal funds dry up.

******************

Chicago’s pension crisis will not be solved via more reamortizations, pension obligation bonds or tax hikes. Such “fixes” will only prolong and further exacerbate the city’s housing, migration and quality-of-life issues. Instead, a comprehensive, long-term solution, based on actuarial best practices, is essential to restoring confidence and competitiveness to Chicago.

Read more from Wirepoints:

- South and southwest Chicago suburbs to be hammered by massive property tax increases

- The great exodus continues: Fresh IRS data shows Illinois loses residents to 40 other states

- IRS migration data: Big blue states biggest losers of people, wealth. Big red states biggest winners. – A Wirepoints 50-state survey

- If you’re shot, robbed or assaulted in Chicago, there’s a 50/50 chance there’ll be no police to respond to your 911 call

Audio and summary

Audio and summary  If this bill passes, say goodbye to local control over all Illinois parks and expect to see open drug and alcohol use, needles, no sanitation and fire hazards, but no ordinary park users.

If this bill passes, say goodbye to local control over all Illinois parks and expect to see open drug and alcohol use, needles, no sanitation and fire hazards, but no ordinary park users.

The numbers are so out of line that there is little hope of solving the problem. The public sector unions knew they were doing this to the Chitty and did not care about the taxpayers. Now both will have to live with the results of this negligence.

Go woke go broke, go broke for those foreigners you stupid braindead democrat voters hahahahaha

Excuse my ignorance on this subject but I understand that this pension study was conducted on the five largest Chicago pensions. Chicago is a subset of county Cook. What is the relationship between Chicago’s pension issues and those of the county?

Is there pension data for the county ex Chicago?

Chicago Fed white paper predicted there is no way out for the state. It recommended keep raising taxes until no one can sell because they are too high for buyers. Property system gets frozen until market crashes values plummet lives are ruined but then the state can start from scratch.

Can you provide link to that paper?

Mark Glennon – there was a paper 5 or 6 years ago put out by Chicago Fed researchers which proposed that Illinois apply a special annual assessment of 1 percent or more statewide on all properties to pay pensions. The theory as I remember it is that those who choose to live and buy property in Illinois were the best source of revenue as they were in essence stuck with their properties. In other words, tax things which cannot move. Given the property tax burdens in Illinois, I thought the authors were disconnected from reality but there is an alternate… Read more »

I tried to comment on another article. I assume for all practical purposes, Amendment 1 closed the door for pension debt funding solution where city could competitively bid (outsource) services to private contractors with supposed savings to be dedicated to existing legacy pension debt. For example, similar to current existing city recycle collection contracts (1 man per truck), Streets & San trash collection could be competitively bid (no more 3-4 man Streets & San crews) with dedicated % or $ amount of contract going to existing pension debt. Similarly, Amendment 1 has made consolidation of any city services or departments… Read more »

Not sure why you assume that. Sure, the union could collectively bargain to limit outsourcing but that doesn’t mean management needs to agree to it.

Correct. That’s why I stated “for all practical purposes”. IPI had several articles on Amendment 1 closing the door on any hopes of outsourcing and/or consolidation of services. But maybe worth revisiting for hopeless Chicago at this point?

Absolutely true and the government / union goons watching this site don’t like you making this public.

Individual Retirement Accounts are easier to understand than pensions.

Nobel Memorial Prize in Economic Sciences Award Winners have recommended for several years now that Chicago immediately stop digging and declare bankruptcy, it’s the only fix, taxpayers can not solve this. All the union pension contracts need to be reset to reality.

Wait for the increasing negative effect of commercial property vacancies and the associated decline in commercial property taxes. The commercial property tax shortfall will be added to residential properties. The forecast calls for pain.

Pretty certain Pritzker and the Leftist Democrats will be looking for state taxpayers to bail out Chicago as they recently did with the CTA. Every homeowner in IL outside of Chicago has effectively a ‘Chicago surtax’.

I’ve been saying this for years: Nothing will be done on this until the first pension checks start to bounce.

JPM – one thing Mark Glennon has illuminated is what happens when pensions hit pay as you go status. The government entity must pay under state law, and in the case of Chicago, their operating budget would go entirely to pensions. The City is liened up, meaning an asset free bankruptcy is a possibility, making it not worthwhile to enter it (unless one believes judges will ignore the law and property rights). The people who run the City must think the feds will bail them out.

I am very confident that the quiet hope of many Dems who ignore the pension crisis is that it will be “federalized” — that’s the term they use for federal bailout. One individual whom I trust heard Rahm say that in private years ago.

No chance of that happening. None, zero- the Federal Government is broke and the congress has many other ways to spend money. Illinois is shrinking fast and so is its political clout.

That was the game the local school boards played for years that has brought us to where we are today. Systematically juice those end of career salaries, and the resulting pensions, before passing the bill onto Springfield.

Our friend Squeezy the tax python keeps tightening

His coils and the taxes keep going up.

It gets harder to live and soon it will be over for

Chicago.

Chicago is such a doomed dump. High taxes, high crime, high corruption, and on its way to bankruptcy.

Don’t forget reparations.