By: Ted Dabrowski and John Klingner

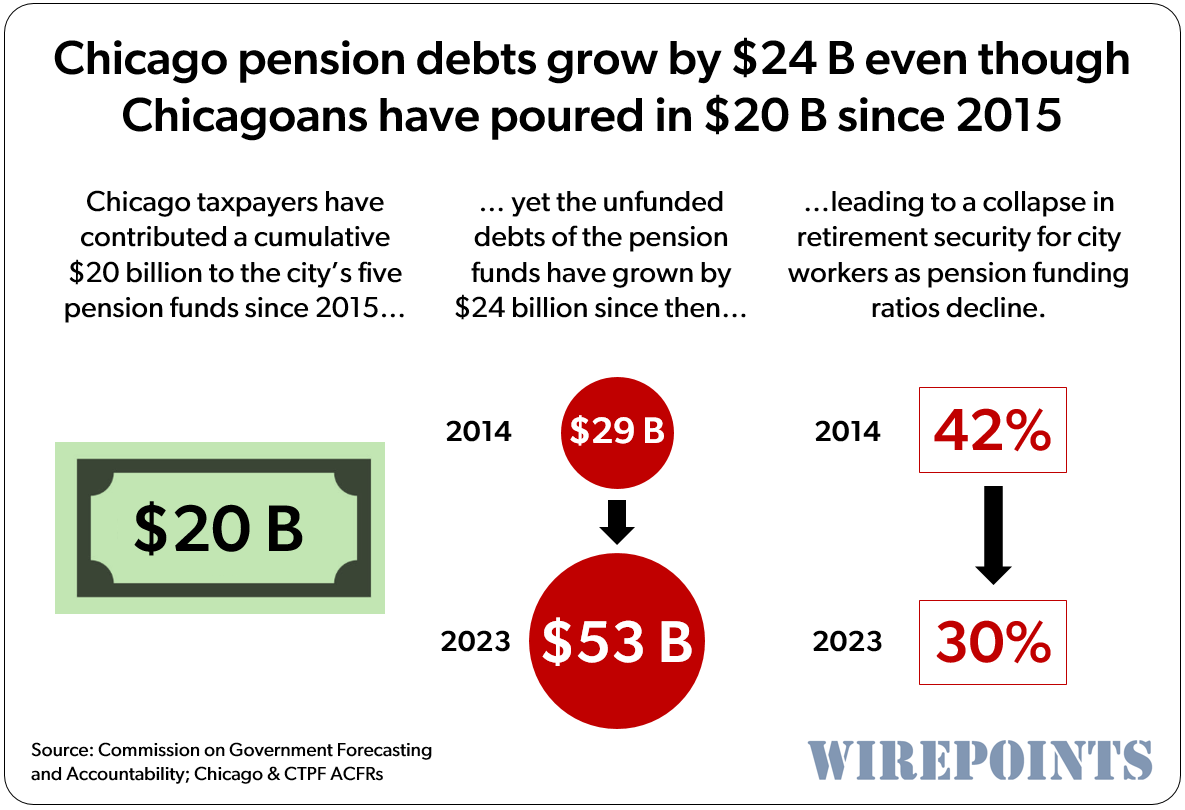

It’s been an absolute mess for Chicago taxpayers and the retirement security of the city’s government workers. Ever since Chicago’s pension funding laws began requiring larger contributions around nine years ago, both the city and Chicago Public Schools have poured a cumulative $20 billion in taxpayer money into the city’s five major pension funds – a massive increase compared to the $5.7 billion contributed the previous nine years – only to get nothing for it.

On the contrary, Chicago’s collective pension debts actually increased to $53 billion, a jump of $24 billion. Chicago residents – on the hook to pay down those debts – are now much worse off than before. At the same time, the retirement security of Chicago government workers has collapsed. Combined, the five pension plans were 42% funded in 2014. By 2023, that-already dismal percentage had fallen to just 30%. All the new money did nothing, as if it had been swallowed by a black hole.

Chicago pensions remain the worst funded of any big city in the country, according to the rating agency S&P, and neither the mayor, the governor nor the legislature have a plan to fix the mess. As Chicago’s slide continues, it should become increasingly obvious that Illinois urgently needs a constitutional amendment that allows pensions to be reformed.

More money from taxpayers

In 2015, just when the funding laws began to change, the city and Chicago Public Schools paid a combined $1.6 billion into the police, fire, municipal, laborers and teachers funds. By 2023, annual payments had grown to more than $3.4 billion, a 110% increase.

Add up all those contributions and they total more than $20 billion in taxpayer contributions to pensions during that 9-year period, partially funded by Mayor Rahm Emanuel’s record $543 million property tax hike in 2015, along with a host of other tax and fee increases.

All that new money didn’t stop Chicago’s unfunded pension debts from growing at a rate of about $2 billion a year. In 2014, Chicagoans were burdened with $29 billion in pension debts, or about $28,000 for every city household.

Nine years later, the combined debt has grown to more than $53 billion, or $45,000 per household.

Not only are Chicagoans on the hook for more debts than ever – meaning more tax hikes in the future – but city worker retirements are also less secure.

The teachers funded ratio has dropped ten percentage points since 2015, to 43%. The funded ratio for the laborers’ plan collapsed by more than 25 percentage points, to just 39% The other funds are dismally funded at just 22%.

The true cost of pensions is even higher

Chicago’s pension troubles are even deeper than they appear. The reason why the city and CPS’ debts keep growing year after year is that the money taxpayers contribute still isn’t enough, according to the pension funds themselves.

Chicagoans paid $3.4 billion into the five pension funds in 2023. But the Actuarially Determined Contribution (ADC) – the amount the pension actuaries say is truly needed – was actually $4.4 billion that year.

So Chicagoans would have to fork over a billion more dollars a year – 30% more than they’re already paying in – to keep Chicago’s public retirement funds from getting worse. That’s the same as the city adding another two property tax hikes like the one Mayor Emanuel imposed in 2015.

A long-time burden

Some city officials may point out that the rapidly growing pension contributions of the past decade are coming to an end. That the funding ramp-up forced by Chicago’s pension reform bills has finally ended, so the city and school district’s pension costs won’t grow as rapidly in the future.

Perhaps. But that ignores the fact that Chicago’s pension costs are likely going to remain some of the most expensive among the nation’s big cities for literally decades. S&P says a third of the city’s budget, 32%, is swallowed up by pensions and other fixed costs.

That’s 50% higher than New York’s own 21% of budget. And cities like Philadelphia and Denver have just 15% of their budgets going towards pensions.

Chicago will continue to find it hard to compete for when so many other big American cities can offer people and businesses far lower taxes, and better services, because their own pension issues are far less of a problem.

Chicago’s pensions are a drain on Chicagoans’ wallets and the city’s dynamism. If nothing is done – if the constitution isn’t amended to allow for pension reform and if bankruptcy isn’t made an option for Illinois’ municipalities – don’t be surprised if Chicago’s slide accelerates.

Read more from Wirepoints:

- This one graphic explains why Illinois is such a financial mess

- An Open Letter to Mayor Brandon Johnson on the forthcoming recommendations of his Pension Working Group

- City of Chicago budget revenues have ballooned by $6 billion since 2019. Why the $1 billion deficit?

- Detroit’s bankruptcy offered key lessons. Chicago has ignored them all.

- Detroit and Chicago: Trading places

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

Isn’t it possible to dissolve the corporate status of Chicago, and revert political control to the county?

(65 ILCS 5/Art. 7 Div. 6 heading)

DIVISION 6. DISSOLUTION

(65 ILCS 5/7‑6‑1) (from Ch. 24, par. 7‑6‑1)

Sec. 7‑6‑1.

The elephant in the room here is the fact that the S&P 500 is up more than 182% in the past 10 years!!! The state has missed a period of very rich returns (that likely won’t be repeated the next 10 years) on the shortfall in these funds. It also means these funds would be in an even deeper hole with more ordinary recent returns.

every Ponzi Scheme ends when they run out of OPM (Other Peoples Money). There is no escaping this.

Chicago and Illinois have been making the $20/month minimum payment on their credit card for years, and now they’re both past the tipping point and are in death spirals where the balance is so large that the interest service is greater than their income. It’s not fixable, it’s over, they’re just coasting to a stop. In the private sector, we have bankruptcy. The bizarro world of Illinois won’t allow that. The whole thing is going to collapse, it’s just algebra.

You forgot that most civic leaders in Chicago never passed Algebra and most citizens can’t spell it. So the minimum payment analogy is correct. The deadbeat bust out similarity is astounding. Add drugs, booze and gambling and the analogy is complete.

The federal government is in the same predicament. Retirement? It won’t be long until people work until they drop — like most of human existence since Adam.

Some thoughts: This article doesn’t include as assessment of what the unfunded liability would have been without the additional contributions. Yes, the current levels are tremendous, but what would they be today without the additional contributions? Is there a source of “error” here–were the actuarial assumptions significantly in error as regards projected salaries, retirements or new employees? Were the investment assumptions too high as compared to actual returns? Are the current actuarial assumptions reasonable? Is this assessment of unfunded liability reasonable? For example, given the CTU’s salary demands (for which they won’t themselves pay pension increases) is the Teachers’ Fund… Read more »

Chicagoans love it. They just voted for more of the same. So just jump on board. The bus is presently careening off the cliff and will slam into the ground shortly.

A full and predictive explanation for the fiscal mess was provided in a superbly written white paper published by Wirepoints six years ago (I don’t know if it was the same organization but at least the same name). If, and only if, the issues identified and explained therein are addressed will any headway be made. Else, everyone would be better off if the state and the City of Chicago were to declare bankruptcy and reorganize now. Pain? What about those currently employed who will find there’s nothing there when they retire?

What’s going to happen if & when state passes Martwick’s SB2024–TIER II fix?…..as the few dopey taxpayer/homeowners who even read the news get ZERO reporting in mainstream press.

The enormous liabilities described above will simply increase with the Tier II fix. While concerning, the math is really hopeless at this point. 20 billion over 9 years and the liability increases from 29B to 53B? I suspect I will get downvoted for merely restating facts.

The state will need to start paying for proper pensions again instead of cheating the new hires. We will demand fair wages and pension benefits. The days of screwing over new hires will be coming to an end. Time to pay your fair share. Union Strong!

Dream on. Public sector unions are unconstitutional and that fact will soon be legally tested and your little grifter’s club busted.

Just making up more lies scab. Keep saying it’s unconstitutional and we will continue to collectively bargain for the best possible contract. It’s a great system. You get to play pretend and we keep getting paid with better contracts. Each and every negotiation. Hahahaha.

When Chicago, Cook County and Chicago become financially insolvent the Public Sector grifters will get their fair share: Maybe 10 cents on the dollar if they are lucky and the bankruptcy boards are generous. There will be no Federal bailout because the grifters will simply rinse lather repeat. CTU vermin should kjss that Florida houseboat goodbye. A house trailer along the Mississippi is the realistic retirement.

Bwahahahahahaha. Don’t think so scab. We will not only get our full pension but will also restore tier 2 benefits to their proper amount. Don’t forget the 9% raise every year for CTU members. Just kidding, we will settle for 6% if we are feeling generous. Dig deep scab. Time for you to pay up.

Two points, both likely beyond a CTU member’s IQ: 1. The math is inexorable. I know that anything involving math is incomprehensible for a CTU member but know that soon you will run out of other peoples money. 2. Hubris. Likely beyond your vocabulary but look it up. It foretells your future.

The problem is that taxes cannot be raised and collected in sufficient amounts to get pension ratios anywhere near sustainable. Who will pay the $45,000 per City household debt attributable to pensions? And the $41,000 attributable to like state liabilities? The Chicago family bringing in $90,000? I don’t think so. They need every cent of their income to survive. So how much burden must the family bringing in $300k to $1M pay? 500k? But that doesn’t come close to drawing down the debt (remember we have an income tax and this slice pays a majority of taxes). The numbers just… Read more »

People like JShark don’t worry themselves about mere financial details. They have a guaranteed contract, their brothers and sisters, union strong. Slogans will fix everything.

The downvotes are laughable. I ask questions that most everyone who is reasonable are asking. The pension liabilities are a huge millstone around the neck of Illinois government units, with Chicago being the most ominous and depressing. My friend from college represents several public labor unions in Long Island. The most difficult thing he has had to do is to persuade the unions the money isn’t there any longer.

Pension holidays and agreed to by pension board members who were appointed by the mayor along with “loans” to certain relatives of political bosses have cost the pension funds billions of dollars when compounded investment interest is figured in over a 30yrs time frame. Who is accountable for this mess, the politicians, and in Chicago it’s democrats, in the county it’s democrats, in the state it’s democrats. Does anyone see a pattern here?

It’s Trumps fault?