By Ted Dabrowski and John Klingner

Chicago Mayor Rahm Emanuel’s team claims its proposed $10 billion pension obligation bond is good fiscal policy. Far from it. The POBs, as the bonds are called, are nothing more than gambling using taxpayer funds. They’re a terrible idea.

But bad policy has never stopped a Chicago politician. Emanuel’s motivation for pushing the bonds is the upcoming mayoral election. He faces ten challengers and they’re slinging all kinds of mud on him, in particular for his record as a property tax hiker and his failures on policing. Emanuel’s looking to deflect those challenges. He thinks he’s found a way using POBs.

Emanuel hiked property taxes by more than $800 million during his first two terms in office, and yet the city’s pension mess continues to worsen. As a result, required taxpayer contributions are set to double to $2.2 billion by 2022. Absent some “solution,” property taxes will have to go up dramatically and Emanuel won’t be able to defend himself on the campaign trail. It’s a loser position.

And Emanuel is still negotiating the city’s police and fire labor contracts that expired more than a year ago. The prickly one, of course, is the police contract. The mayor’s mess there is more than just about pay and incentives. He’s got a real crisis – from the handling of the Laquan McDonald video to transparency and settlement scandals – that has damaged his relationship with the department.

The POB is all about accessing money now to assuage both groups. But all Chicagoans – residents, media and civic institutions – should refuse to buy into this deal. This bond is no different than the Skyway and parking meter contracts or the more recent securitized borrowings. They’re all deals that cause Chicagoans long-term pain in exchange for some politician’s short-term gain.

Here’s how the bonds help Emanuel, and how they’ll hoodwink Chicagoans:

POBs and Emanuel’s short-term gains

Emanuel’s upcoming property tax hike problem

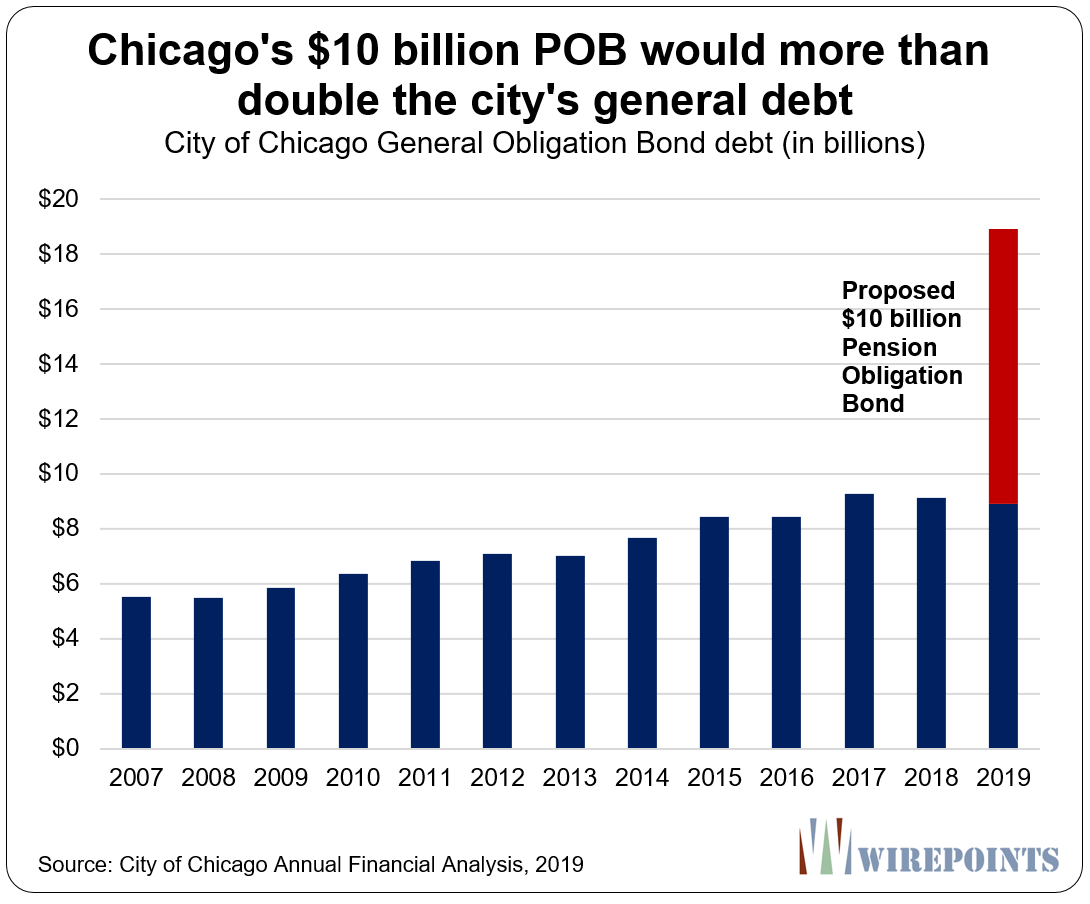

The bonds require the city to reach out to Wall Street banks and borrow $10 billion, which would more than double the city’s general debt. The mayor will promise whatever he needs to promise – including committing the city’s future sales tax revenues – to ensure he can entice the bankers to lend at the most lenient terms possible. (How the city is selling off its financial future is the subject of an entirely different piece – you can read about that here.)

The city will then take the $10 billion and pour it into its four city-run pension funds. The funded levels of the pension funds will increase from a collective 26 percent to more than 50 percent – a dramatic jump. By pre-funding the pension funds with such a large amount, the higher funding ratios will lower the city’s required taxpayer contributions over the next few years significantly, thus removing the pressure for tax hikes.

But this plan won’t work if the massive taxpayer pension contributions disappear only to have them replaced by equally big repayments toward the $10 billion borrowing. So expect Emanuel to structure the repayment of the $10 billion debt so it’s far, far off into the future.

With all the financial engineering in place, Emanuel can then run on the promise that he won’t hike property taxes his next term. Problem solved.

Emanuel’s unsigned police contract

Emanuel needs serious leverage if he’s to put his police contract negotiations to rest in a way that gives him power going into the elections. He’s got that power in the POBs.

The police plan is just 23 percent funded. Fire is just 20 percent funded. By any measure those systems are broke. Most analysts give the plans just a few years before insolvency hits. Public safety workers, and the unions that represent them, know this. Pensions haven’t been a priority in negotiations for years. But now that pension checks are close to bouncing, they’re the hot topic.

If Emanuel can offer to take the two plans’ funded ratios to 50 percent by putting in billions of fresh money, he gets the real leverage he’s been looking for. “Sign the labor contracts and I’ll take your pensions away from the brink,” he can tell the unions.

And he can tell those public safety workers near the end of their career that the money will be there for them in retirement. With that, Emanuel can buy labor peace with the police and fire unions right before the elections.

The pitch to Chicagoans and the truth

To make the bond deal happen, Emanuel has to sell it hard. Listen to his CFO Carole Brown and other surrogates like Ralph Martire of the CTBA and you’ll hear nothing but how POBs are good policy.

They’re saying Chicago can borrow more cheaply. That the pension crisis will be defused. That this makes city finances more healthy. And all at little-to-no-risk to Chicagoans. “If I can create a structure that can re-fund some of my higher cost pension debt with lower-cost bonded debt, then I can save money for taxpayers,” said Brown.

None of that is true.

1. Borrowing more money to pay down debts doesn’t solve anything, especially when you have a borrowing problem. Don’t think that borrowing $10 billion and putting it into pensions solves any of the city’s problems. At its core, the POB only moves $10 billion in debt from one pile (pensions) to another (the city). Chicagoans will be just as indebted as they were before. Playing financial shell games like this is especially galling considering Chicago is a junk-rated mess with a borrowing addiction.

Emanuel claims he’s ended the irresponsible practice of “scoop and toss” borrowing. But the pension bond is scoop and toss in everything but name.

2. There are no guaranteed savings from issuing the bonds. They’ll try to sell it that way, but it’s simply not true. Instead, the bond requires taking a massive risk with taxpayer dollars. The word “if” in Carol Brown’s quote above tells why the bonds are a bad idea for Chicagoans. The whole POB proposal is a gamble with taxpayer money. Officials hope to borrow at 5 percent, invest it in the stock market and make a profit. The problem is, the market can go the other way and the funds can lose money in the process. And taxpayers will be left holding the bag.

Many other governments have gambled on POBs and ended up losing money in the markets. San Bernardino, Detroit, New Jersey and Puerto Rico all issued bonds that cost their residents hundreds of millions. Closer to home, the CTA issued a $1.9 billion pension bond in 2008 that turned into a debacle when the recession hit.

3. What it does for the pension plans is illusory. Pension obligation bonds do not address the real problems with defined benefit plans. They are not reforms. Instead, they just hide and perpetuate the underlying problems. Illinois’ $10 billion and the CTA’s $1.9 billion pension bonds are two good examples of can kicking where the pension funds only got worse afterward. Their failures were covered in Wirepoints pieces here and here.

4. The expected tax hikes don’t disappear. They just get shoved further into the future. If the POB goes through, Emanuel will be more than happy to tell Chicagoans he saved them billions in near-term tax hikes. What he won’t tell Chicagoans is that they’ll pay those tax hikes later. That’s because he’ll push the bond repayments far into the future – and way past his tenure.

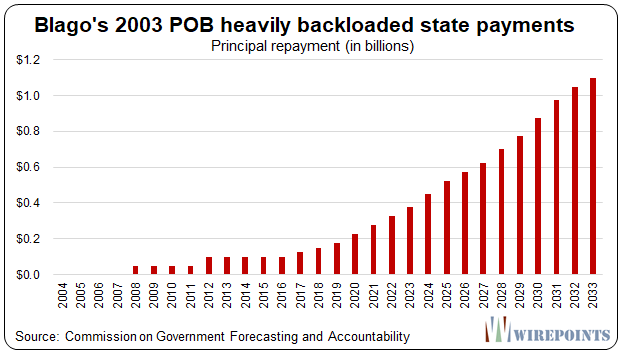

Just look at how former Gov. Rod Blagojevich’s POB was structured. In 2003, the state borrowed $10 billion to fund pensions. Today, 15 years later, the state still owes $9 billion in principal, never mind the interest still owed. Illinoisans will be paying off that debt through 2033. If the graphic looks a lot like Gov. Edgar’s failed 1996 pension payment ramp, that’s because it does.

Mortgaging Chicago’s future

If it wasn’t clear how self-serving this whole plan is, consider the fact that Emanuel is doing this at what could be the worst possible time to play the arbitrage game. The U.S. is experiencing its longest ever bull-market and it’s not unreasonable to expect a correction.

But that’s how selfish Chicago politicians are. Emanuel is willing to gamble with taxpayer money just to win the election.

For him, it’s “heads I win, tails you lose.”

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary

Gone and totally forgotten

Emanuel can only hope for an outcome like Cermak.

Ted: Fantastic article !!!!! I’ll add this, but you know it all too ! Yes, it’s madness — right now the 4 pens plans have Accd Liabs of $38B assuming 7% return on assets, but only $10B assets, thus Unfunded Accd Liabs = $28B. Just 7%/year interest on UAL is $2B which is nearly 60% of $3.6B Payroll…unaffordable. The “Presentation” shows projected Contributions next few years less than that. If they borrow $10B, then still have to pay 7% int on $18B UAL, then also (5%?) int on $10B loan, plus principal on the loan. They need to throw in… Read more »

His mission here was to funnel as much of the cities money through some kind of usury instrument as he could, which he did. The money that could and should be going to service our debt, TIF money, has become his Shakman exempt patronage tool. Every dime needed to right this ship is in those TIF accounts, but the press is just another branch of government now. Our only hope is a Republican US Attorney that can find fault with 142 TIF checkbooks that have been in the hands of drunken sailors (Democrats) for what they thought would be forever.… Read more »

Every day Chicago waits to borrow that $10 Billion and plow it into the stock market is another day of missed profits. /sarc

Good luck Chicago.

The fucking dems need to go and stop blaming Rauner for not passing a budget!!soend, spend and spend and NOT pay it forward? They just kick the debt down the riad! Raise taxes to pay their debt and Rahm will be out of office with a big fat pension! Fuck that guy ! Get him out NOW ! , Madigan and his pack of pricks have insulated themselves from any responsibility because the own the same system that won’t prosecute them! Let’s vie ourselves a raise ! All in favor? This is what taxpayers should concern themselves with ! Not… Read more »

Easy on the language. My kids read this. Well, at least I ask them to.

I abhor the idea of these politicians kicking the financial burden can down the road. I’m also not a financial wiz so I don’t know what is the best financial pension reform plan for all parties involved. I did “Serve and Protect” this great city and its citizens for two months shy of 34 years and so I’m counting on my pension especially since former Congressman Rostenkowski pushed through legislation to change the Social Security system payout for individuals receiving a pension. So even though I paid into the Soc.Sec. system for about 15 years before joining the CPD, my… Read more »

Rahm is just kicking the can down the road, so someone else will have to handle the problem. This is the problem with Democratic politicians, all they know how to do is tax, tax, and tax. The last Democrat I remember that balanced a budget was Bill Clinton, and he did this through robbing Peter to pay Paul and the IT boom also helped. Democrats seem to be incapable of fiscal responsibility and balancing budgets and do not appear to care since they will use other people’s money (taxpayers) to make up for their fiscal incompetence. Makes one angry when… Read more »

Here’s a few long term backloaded bills passed in Illinois General Assembly that were signed into law by Governors in the last 29 years: – 2008’s 25 yr $10B backloaded Blagojevich / Madigan / Emil Jones Jr POB which included a pension holiday and modification of…. – 1994’s 50 year backloaded Edgar / Madigan / Philip state pension contribution schedule to reach 90% funding which replaced… 1989’s 47 year backloaded Thompson / Madigan / Rock state pension contribution schedule which included converting the 3% simple interest COLA to 3% compound interest. None to date have reduced the unfunded state pension… Read more »

Just a reminder, the very second you cross the Illinois state line in a moving van, you will not owe 1 red cent on those ridiculous and obscene pensions.

That is all.

Toot-a-loo

Remember though, once you move you need to get involved in local and state politics and fight to keep your new home fro being transformed into another liberal paradise. the reason is, it is not just conservatives who are moving. Liberal and progressives don’t want to pay the freight for the very policies they vote for. They are fleeing Illinois also and spreading the liberal pathogen into their new communities. You need to seize the reins when you move and steer your new community, through your activism, around the siren song of the left.

As a poster in some Tennessee forum said (paraphrasing) “Liberals move here with their ideology and spread it the way a beer fart spreads in a car with the windows rolled up. Go back!”

Sadly I am rethinking my retreat in the mountains of TN. I really fear what former IL residents may do to that state. I have been planning on becoming a TN resident for decades, carefully watching them chip away at ta nasty dividend and interest tax which is being fazed out), as an interim step I became a FL resident. I follow several TN city council meetings ad am distressed by what I see, the same crap that happened in IL. More and more “help the poor” assistance and demands for diversity positions, all that does is attract more poor… Read more »

I’m no finance expert, but I think assuming an average annual rate of return of 7% is not the same as actually earning 7% interest annually. Investments earning the same rate per year every year yields more gains than an investment that fluctuates +/- from that average rate but maintains that average rate over time. For example, a $10B single investment in the stock market earning 7% annually over 30 years (what I’m assuming will be the bond term) yields $76B. But if the rate fluctuates, say 14% one year and 0% the next or 21% one year and -7%… Read more »

Don’t forget the one economic fact that is unmentioned in this proposal. The banks and bond dealers, friends of Rahm with whom he has dealt before (white collar patronage), who would create and service this “Pension Bond” issue will make money from the very start, which the Chicago taxpayers will be under the extended burden of 30 years of new increased and unfunded public debt while also paying the annual increased budget cost of the debt service. How does that economic truism go ? if you borrow $100 you owe the bank. But if if you borrow $10 billion, the… Read more »

I think the plan here is to issue the bonds and then sometime in the future to declare bankruptcy and stiff the bond holders as has happened in Stockton and elsewhere.

When your pension system is only 20% funded you are already headed for bankruptcy so you might as well try a Hail Mary.

I really doubt that the bonds will sell. Not even Wall Street will take on that amount of risk for a 5% return. .

I think the plan here is to issue the bonds and then sometime in the future to declare bankruptcy and stiff the bond holders as has happened in Stockton and elsewhere.

My thoughts EXACTLY. Leave the BOND HOLDERS holding the bag. And ANYONE who buys these is a fool. As in “Puerto Rico, Stockton, Vallejo, Detroit Foolish”. And ANY brokerage that underwrites or sells them will be looking at fraud charges in a civil lawsuit, massive lawsuits against any underwriters.

But keep in mind that the city wants to use that new securitization scheme for these bonds, under which full ownership of a chunk of future revenue is sold to secure the bonds. The whole purpose of that is to be bulletproof even in bankruptcy.

Mark, has there ever been a public bond structured to be bulletproof in bankruptcy and actually proved to be bulletproof in bankruptcy or insolvency of that public institution?

Bonds secured by traditional mortgages and security interests have generally held up very well in public bankruptcies. The muni bond folks, however, are concerned about what will happen when things are truly put to the test in a situation where the covered assets are essential for providing basic government services. So, they wrote authorization for this new securitized form of bond structure very, very thoughtfully and carefully and got it through the IL legislature. It, too, however, has never been put to the test so, no, we don’t know if it will turn out as bulletproof as intended.

I’d be willing to bet that a federal bankruptcy judge would see that scheme as corrupt and would not hold the taxpayers to it.

I have communicated this before, but I don’t think a federal bankruptcy judge would be unaffected by the politics of the mob. While the lender’s property rights (liens) should be respected, the prospect of having pensioners left destitute (with the concomitant threat of being thrown on welfare) may make for unpredictable bankruptcy rulings. In fact, if the left cannot get a federal bailout, which is clearly what they are counting on, they are likely hoping on an anti-property rights decisions in the courts when it all gets bad enough. Thrilling, isn’t it?

Hey Chicago, if borrowing 10 billion is a great idea, why not borrow 100 billion?