View data PDF: Police and fire contributions by city, 2016

Harvey, the first domino in Illinois: Data shows nearly 400 other pension funds could trigger garnishment*

By: Ted Dabrowski and John Klingner

You’d be mistaken to think Harvey, Illinois has a unique pension crisis. It may be the first, and its problems may be the most severe, but the reality is the mess is everywhere, from East St. Louis to Rockford and from Quincy to Danville. A review of Illinois Department of Insurance pension data shows that Harvey could be just the start of a flood of garnishments across the state.

Harvey made the news last year when an Illinois court ordered the municipality to hike its property taxes (already at an effective rate of 5.7 percent – six times more than the average in Indiana) to properly fund the Harvey firefighter pension fund, which is just 22 percent funded.

Now, the state has stepped in on behalf of Harvey’s police pension fund. The state comptroller has begun garnishing the city’s tax revenues to make up what the municipality failed to contribute. In response, the city has announced that 40 public safety employees will be laid off.

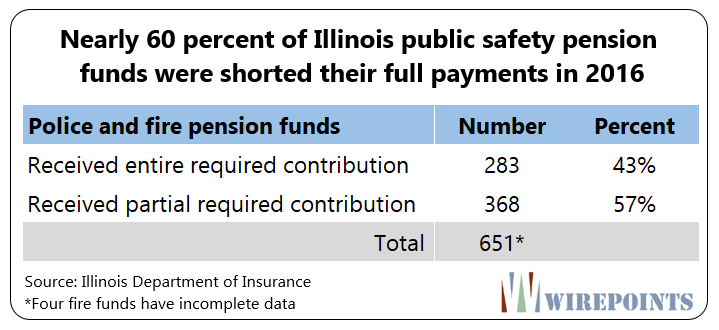

Under state law, pensions that don’t receive required funding may demand the Illinois Comptroller intercept their municipality’s tax revenues. In total, 368 police and fire pension funds, or 57 percent of Illinois’ 651 downstate public safety funds, received less funding than what was required from their cities in 2016 – the most recent year for which statewide data is available.

If those same numbers continue to hold true, all those cities face the risk of having their revenues intercepted by the comptroller.

*Table updated 4/25/18

More on the way

The state comptroller began intercepting Harvey’s revenues – sales, income and other taxes that the state collects on behalf of municipalities – after the city’s police pension fund certified that Harvey had failed to make its required pension contribution to the fund. Once a pension fund certifies a shortfall, the state comptroller must garnish city funds, according to a law passed in 2011 and then further clarified in 2015.

The state has already taken $1.5 million dollars from Harvey since February. Harvey is the first municipality to have its funds intercepted under the 2011 law.

Under the law, a city’s required yearly contributions to each pension fund must cover two parts. First are the normal costs – the cost of benefits created by employees working one additional year. The second is an amount necessary to amortize a portion of the legacy shortfall such that the debt is paid off by 2040.

Harvey’s police fund should have received $1.22 million in 2016. That’s the number found in both the DOI report and the fund’s actuarial report. Instead, the police fund received only $110,000, or just 9 percent of what it was supposed to. That lack of funding persisted over the past decade and continued into 2017, hence the intercept by the state.

Harvey may be the first city to suffer garnishment, but it won’t be the last. Illinois has a $10 billion downstate pension crisis – made up of municipal police and firefighter pension funds – that is separate from the state’s own $130 billion crisis.

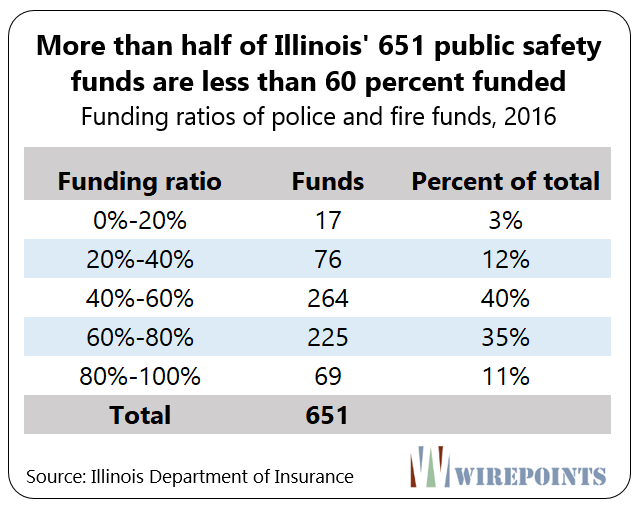

Some public safety funds are in good shape, but the majority are in trouble. And a growing number are approaching total insolvency. More than half of Illinois’ public safety funds are less than 60 percent funded.

Contribution shortfalls

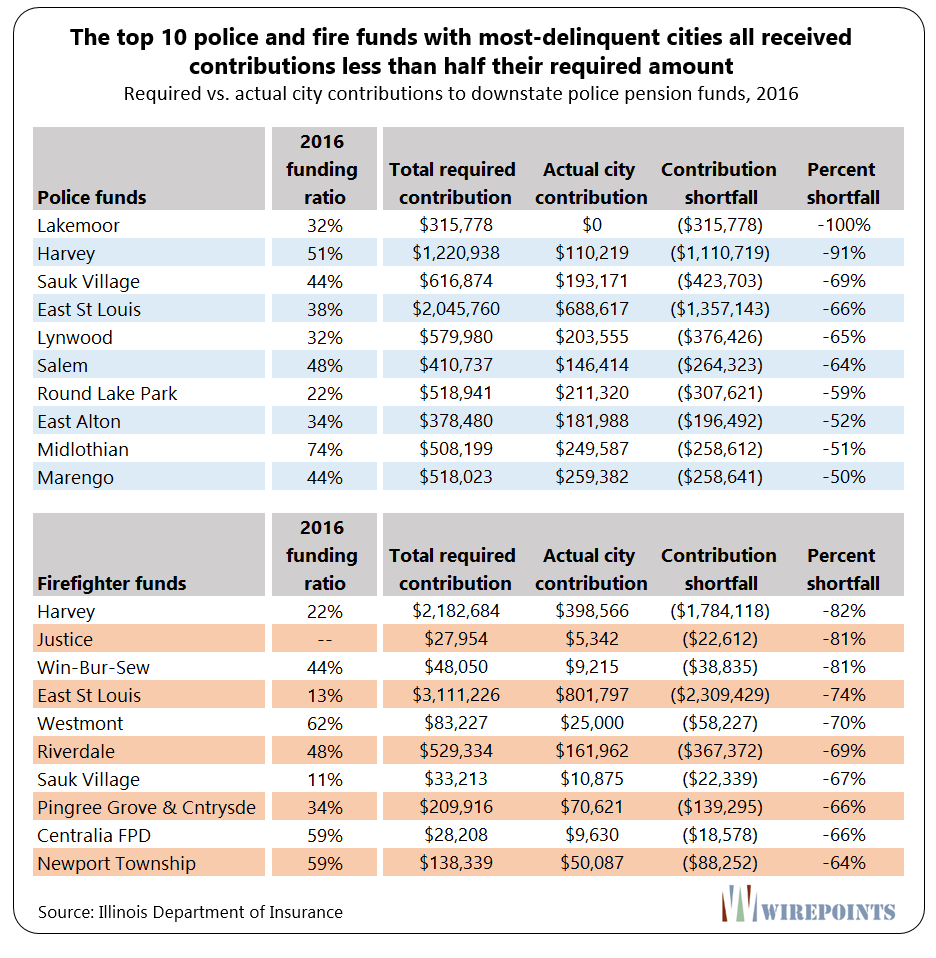

Harvey’s pension funds were among those facing the largest contribution shortfalls. The ten public safety funds most impacted, in percentage terms, received less than half their required amounts in 2016. Communities like East St. Louis, Round Lake Park, Sauk Village and Riverdale were among the top ten.

*Table updated 4/25/18

Overall, nearly 60 percent of Illinois’ 651 pension funds got less than their required contribution from their cities/localities in 2016. All those funds could potentially go after their cities and request a state-comptroller intercept of local revenues. However, pension funds under Fire Protection Districts will have a much harder time benefitting from the intercept law.

See PDF of Illinois police and fire funds and their funding shortfalls for 2016 below:

- Police and fire contributions by city, 2016

- Police and fire contributions by percent shortfall, 2016

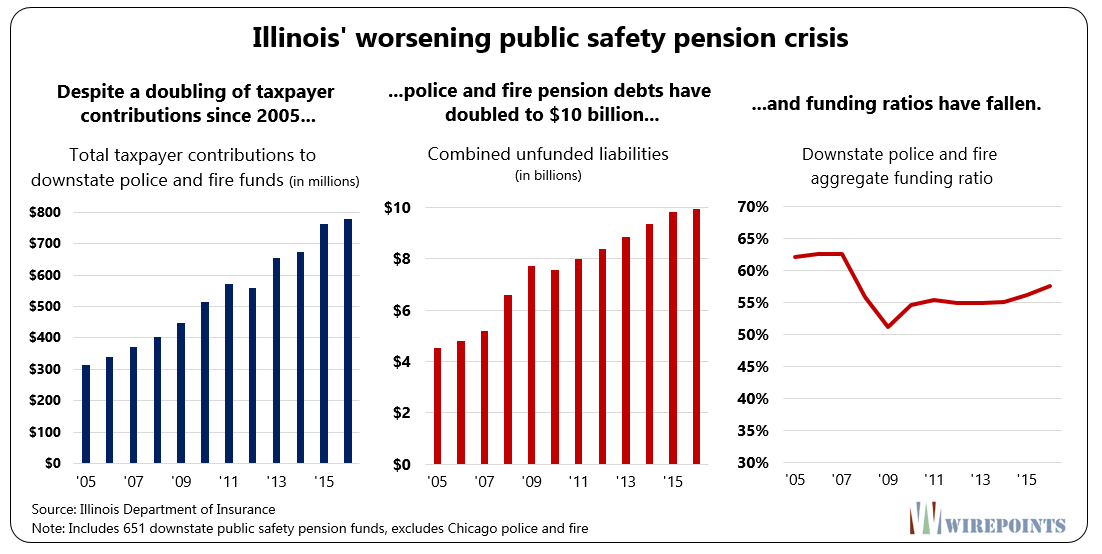

It’s foolish to think that garnishments are going to solve anything. Taxpayers in municipalities across the state – who already pay the highest property taxes in the nation – have been putting more and more money into pensions, only to watch the funds continue to deteriorate.

Despite a doubling of taxpayer contributions since 2005, police and fire pension debts have doubled to $10 billion instead of shrunk, while funding ratios have fallen.

Many will want to blame historical underfunding as the cause of this mess. But it’s really ballooning pension promises that’s the culprit.

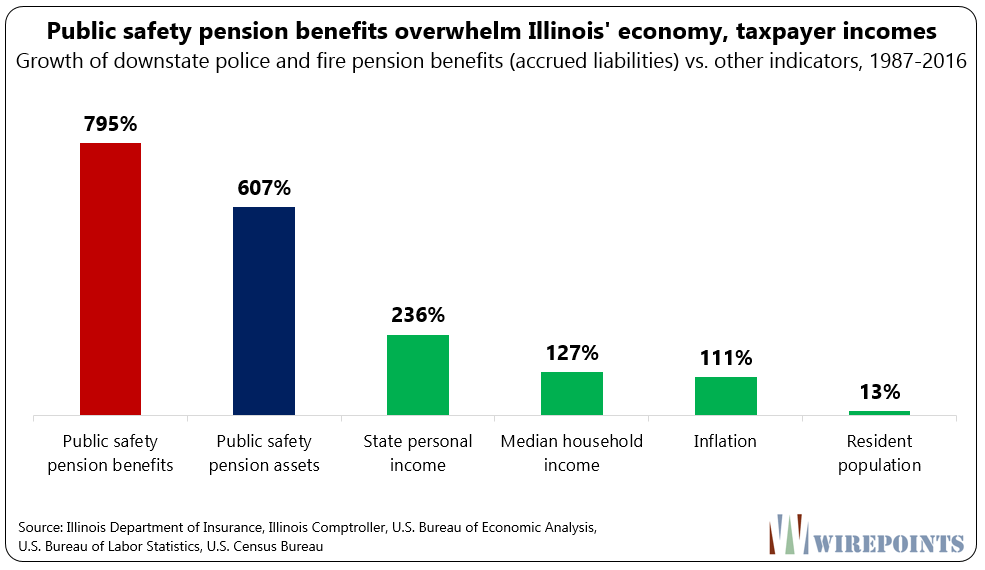

In 1987, municipalities owed a total of $2.6 billion in benefits to public safety workers and retirees across the state. Today, that number has jumped to $23.4 billion. That’s nearly an 800 percent increase.

Those total owed pension promises have grown at a pace that’s swamping the state’s economy, inflation and household incomes. Inflation has risen by just 111 percent and household incomes by 127 percent over those 30 years.

And it’s not as if taxpayers didn’t try to keep up with the funding. Illinois police and fire pension assets, buoyed by taxpayer contributions, grew 607 percent over the past 30 years. That growth, too, was multiples faster than the growth of the economy, inflation, and resident incomes.

Not surprisingly, no matter what taxpayers put in, their payments could never catch up with the state’s out-of-control benefits. And with benefit and labor rules out of communities’ control, cities have had few ways of cutting the burden themselves.

Protecting the status quo

With nearly 60 percent of pension funds not getting the contributions they require in 2016 and a $10 billion shortfall already in place, it’s a wonder more cities haven’t had their revenues garnished.

The answer lies in city and union officials’ protection of the status quo. Even union officials don’t want the state to garnish city revenues because they know what will result: layoffs and pay cuts. They’d rather sacrifice pension funding to grow current payrolls because that’s where their power comes from – dollars right now.

And if the pension funds collapse, they’re gambling that the constitutional protections will bail them out – that an ever-shrinking number of taxpayers will be forced to pay no matter what.

Harvey was the perfect example of this for nearly a decade. The public safety unions there accepted raises at nearly double the rate of inflation.

At the same time, their retirement security was being gutted, the incomes of Harvey residents were collapsing, poverty grew by 7 percentage points, and the city lost 10 percent of its population.

But now that the crisis has deepened to the point where the state and the courts have stepped in, the game Harvey’s played is nearly over.

Paradox

The root of Harvey’s problems are the same ones driving cities and towns all across Illinois into crisis. They’re all stuck on the same path, dealing with the same impossible pension math. It’s just that Harvey managed to get to the end of the path first because of its deep economic plight and criminal mismanagement.

It all comes back to local control, and in Illinois munis’ case, a lack of it.

As one of Wirepoints’ readers commented recently:

“Harvey has no bond market option. No more room to tax option. No constitutional option to reduce their obligation. No ability to outright default option as they are now garnished. No cash flow option. No sellable asset option as the town is a wreck. What’s left to do? Bankruptcy. The problem is who will run that process?”

Cities in Illinois can’t reform pensions, cut labor costs, or (as of yet) declare bankruptcy. The state sets the rules that define pension benefits and the collective bargaining laws that must be followed. If Illinois cities are to get out of this impossible situation, that has to change.

It may seem paradoxical to supporters of the status quo, but bankruptcy, a constitutional amendment, pension reforms and changes to collective bargaining rules are what’s needed if Illinoisans really care about those who risk their lives for their communities. Otherwise, those workers will be out of a job, and maybe their pensions, to boot.

See PDF of Illinois police and fire funds and their funding shortfalls for 2016 below:

- Police and fire contributions by city, 2016

- Police and fire contributions by percent shortfall, 2016

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

This is the results of not controlling your Governors, combined with the Evil of Confidentially

The situation is actually much much worse, the states have been “cooking the books”, my state CA placed a 15000 tax lein on me, and presumably counts that claim as an asset, unfortunately it’s not, they made up an income for me because I didn’t file a return, I didn’t file a return because I broke my back and neck and didn’t have an income-for several years, then the state borrowed against their fabricated assets to issue bonds committing securities fraud on top of perjury, fraud and theft, they also stole some money out of my checking account.

Here’s my solution:

https://drive.google.com/file/d/0B90sU3A85q46OE9BZHJFSWEzbGM/view?uspdrivesdk

Thoughts?

I had to stop reading because your basic assumptions are not correct. 1) Public pensions have three sources of income: employee, employer (i.e. taxpayers), and investment returns. Your assumption did not include investment returns. 2) There are still defined benefit pensions in private industry. It may not be as prevalent as it used to be, but there are still pensions in private industry.

Please correct your basic assumptions, then I will be able to take your ideas seriously.

Harvey not only did not make it’s contributions it did not send wages deducted for the purpose of employee contributions. If someone could explain how this is the firefighters fault I would appreciate it .

It really doesn’t matter whose fault it is, at this point. It is the responsibility of public employees to check their pension fund’s website to see how it’s doing. If it is 70% funded or worse, then you better be doing your own retirement savings. Private sector employees are expected to monitor their 401K’s.

welcome to the ghost town and zombie town state.

“The problem with Socialism is the you will eventually run out of other people’s money.”

“Defined benefit” is just another way of saying “Ponzi scheme.”

The Indiana tax payers are slowly, only slowly, learning that the courts have in fact made them slaves.

because judges get pensions too

Surely Trump and Bush are to blame. Somehow.

Surely. /s

Or Koch Brothers, racism, fascism….

Nope its the Union Boss’ I thought.

Those mysterious individuals who control even Madigan, leaving us the electorate disenfranchised and without a republic/government. (Looking forwards for more on this from Wirepoints, lest Mark has eluded to such.)

I thought this was our mantra? I though those were the villains pushing their socialist agenda upon us. A social affliction.

Dont Unions and their Dem shrills have us the electorate prevented from voting for more conservative policies and politicians?

And there’s more than enough evidence that the democrat party takes advantage of the people who have less brain power than the average person.

Politicians and union leaders bear plenty of blame, but ultimately the responsibility for the debacle playing out across the country is squarely on the shoulders of voters who for decade after decade kept voting for irresponsible government. Now everybody gets to suffer the consequences.

Quote: Under state law, pensions that don’t receive required funding may demand the Illinois Comptroller intercept their municipality’s tax revenues. More than 400 police and fire pension funds, or 63 percent of Illinois’ 651 total downstate public safety funds, received less funding than what was required from their cities in 2016 – the most recent year for which statewide data is available. One of my neighbors is getting a Illinois pension from a contract that let him retire as a prison warden at 50. What did he do afterward? He left high-tax Illinois for low-tax Alabama, where his money goes… Read more »

Stipulating that pensioners must reside in IL does not diminish they value of their pension in any way. They should enact this as a requirement. Soon all IL would be is public servant pensioners taxing each other to pay for their pensions. This is the singular law we, as taxpayers, should demand; you have to be an IL resident to receive your pension.

Not all pensions have that ability. IMRF does and they are one of the best run pensions in the nation. The police and fire pensions are only now being able to intercept monies to insure proper payment. If you have a chance to attend any seminars or informational sessions on the history and management of pensions you will better understand the current situation.

IMRF had the distinct advantage of being the ONLY pension system to do that. If all other pension systems were run like IMRF, they’d all be bouncing pension deposit checks and IMRF might not look as well run. It’s easier to make a full pension payment where no one else is.

Not mentioned here is the comment recently made by the City of Harvey’s attorney that Harvey’s property tax collection rate is less than 50 percent and there are $12M in delinquent (and likely uncollectable) taxes owed. What, raise taxes? One could easily see delinquencies increase with revenues decreasing even more than in the recent past. Then who will be left to pay any bills, bearing in mind that the State steps in to effect a rescue the list of similarly situated municipalities is quite long? It is easy to explain Harvey and North Chicago as aberrations given their manifest problems,… Read more »

fantastic writing. once again, the state decided to pick and choose and bail out cps/ctu/-pensions ( & chi home owners) with latest school funding bill–so if your a harvey firefighter, homeowner, taxpayer don’t you have to demand the state gives you the same deal (how can state pick and choose who gets bailed out)? eventually the states going to have to step in. watch the flood gates open for #1 in country for underwater property sw burbs simply leave there homes for nw ind and beyond–and liberal/ dem will say nothing. where’s rauner or jb madigan on this-shameful.

As police and fire protection go down, insurance premiums probably increase. However, home values also decline so the insurance companies have less equity to protect — except for the fact that many dwellings probably have more mortgage debt than equity and the banks will expect to be paid. Who protects the citizens when the city no longer is able to do so? Presumably the county sheriffs but I’m not aware of any county-level fire departments. Who protects the citizens when the counties are broke? This thins-out State Police coverage to an alarming extent. Of course taxpayers (many of whom are… Read more »

Kvetch22, Your solution of locking a bunch of decision makers in a room isn’t as easy as it sounds because of the conflict between actives and retired workers. In many plans, funding levels are so low that there isn’t enough money to meet the benefit needs of those already retired, meaning that the contributions of the active workers AND the municipalities aren’t going to those currently on the job, rather, it goes to those who are no longer working. And when you realize that also in many plan the benefits paid exceed the worker and muni contributions, many retirement plans… Read more »