UPDATE 9/11/19: Mendoza’s press secretary has now written a letter to an editor criticizing this article. That letter and our response are linked here.

By: Mark Glennon*

The State of Illinois recently reported its biggest annual financial loss ever. Instead of clear reporting on that, we’ve seen perhaps the most glaring example yet of how the state’s finances can be misunderstood, misreported and intentionally distorted.

The loss of $47 billion for the state’s 2018 fiscal year, shown in audited financial statements released late last month, is an astonishing number. For some perspective, that’s about $7 billion more than the entire, current annual budget.

But most of the regular press downplayed or entirely ignored the loss. Many even saw good news. A Reuters headline, for example, read “Illinois budget deficit shrank to $7.8 billion in FY 2018.” You can find similar headlines from across the state.

Why would media coverage differ so drastically from what the audited financial statements really said? Which is right?

Two factors account for the difference, and both should be understood. This is a lesson in how misunderstanding of our financial crisis is created and propagated.

First, the loss was shrugged off because it stemmed mostly from an accounting change, which we will explain below. But that’s only a partial excuse. In truth, the accounting change exposed a huge liability that has been all but ignored in the past. Second, most media reports seem to have blindly repeated a very misleading press release by the Illinois Comptroller that accompanied the financials.

Some background before we elaborate: The new financial statements are in the state’s recently released, long overdue CAFR — the Comprehensive Annual Financial Report for the fiscal year that ended in June 2018. The $47 billion loss is shown in the statements as a drop in “net position,” which is the government’s rough equivalent of net worth that you commonly see in the private sector. Changes in it are comparable to net income. As the CAFR itself says, “Over time, increases and decreases in net position measure whether the State’s financial position is improving or deteriorating.”

The big loss was overwhelmingly due to an accounting change that had a $42 billion impact. That change was for healthcare costs owed in the future to state retirees, called OPEBs (other post-employment benefits). In Illinois, those benefits are constitutionally protected just like pensions. Unlike pensions, however, they are entirely unfunded. New accounting rules now taking effect require full disclosure of that liability, which the CAFR says totals $55 billion.

But should we dismiss the massive loss as a bookkeeping quirk? Hardly.

While the $42 billion loss didn’t occur in one year, it’s a growing monster that has been hidden for many years, unknown to most reporters and the public. Including it now as part of the state’s financial report card is an admission about how deficient previous reporting has been. The Governmental Accounting Standards Board couldn’t keep a straight face any longer as it watched governments like Illinois hide OPEB obligations, so it issued a new standard requiring better disclosure, which is now fully in effect.

The simple is fact is that the state’s true condition is indeed a full $47 billion worse than most Illinoisans were told a year ago. That’s because the regular media, like the accountants, have long ignored OPEB liabilities. If you know about them it’s probably only because you read about them here or in other alternate sources, or have expertise in the area.

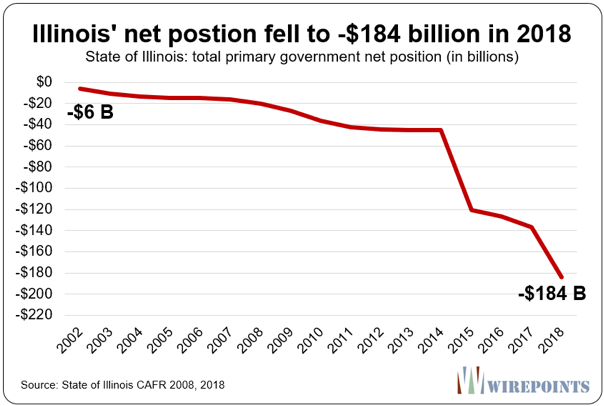

The chart below shows the full story properly over time. Since 2002 the state has lost $178 billion. The big jump down in 2015 was also due to an accounting change. There have been other, smaller ones. However, had the proper accounting rules been in place from the start, the line would still end in the same place. Its downward slope would only have been less jagged.

The second reason why the 2018 loss wasn’t reported properly was misleading spin put on by Illinois Comptroller Susana Mendoza when she released the CAFR. Her press release starts as follows:

ILLINOIS CUT ITS DEFICIT IN HALF IN FISCAL YEAR 2018, ANNUAL CAFR SHOWS

The Comprehensive Annual Financial Report (CAFR) released today shows Illinois cut its general funds deficit by $6.849 billion — from a deficit of $14.612 billion in fiscal year 2017 to a deficit of $7.763 billion in fiscal year 2018. That is largely because of a refinancing of state debt from high-interest to low-interest repayment.

Many news stories repeated that or something like it with happy headlines like “Annual report: Illinois cuts deficit in half in fiscal year 2018.” Most of those stories buried the huge loss and the OPEB issue or didn’t mention them at all A notable exception was The Bond Buyer, with a more appropriate headline, “Illinois CAFR arrives, late and covered in red ink.”

In truth, Mendoza cherry-picked an extremely unrepresentative element of the CAFR. Note that she referred only to the “general funds” to claim the deficit reduction. The general funds are only part of the picture, and they effectively count borrowed money as if it is income!

It’s like claiming you cut your losses in half by putting that half on a credit card. During the year, Illinois sold bonds to pay down $6.5 billion of its huge backlog of unpaid bills. Refinancing from one debt to another in that manner has little genuine impact, aside from some interest savings that, for 2018, would be a tiny portion of the supposed deficit reduction.

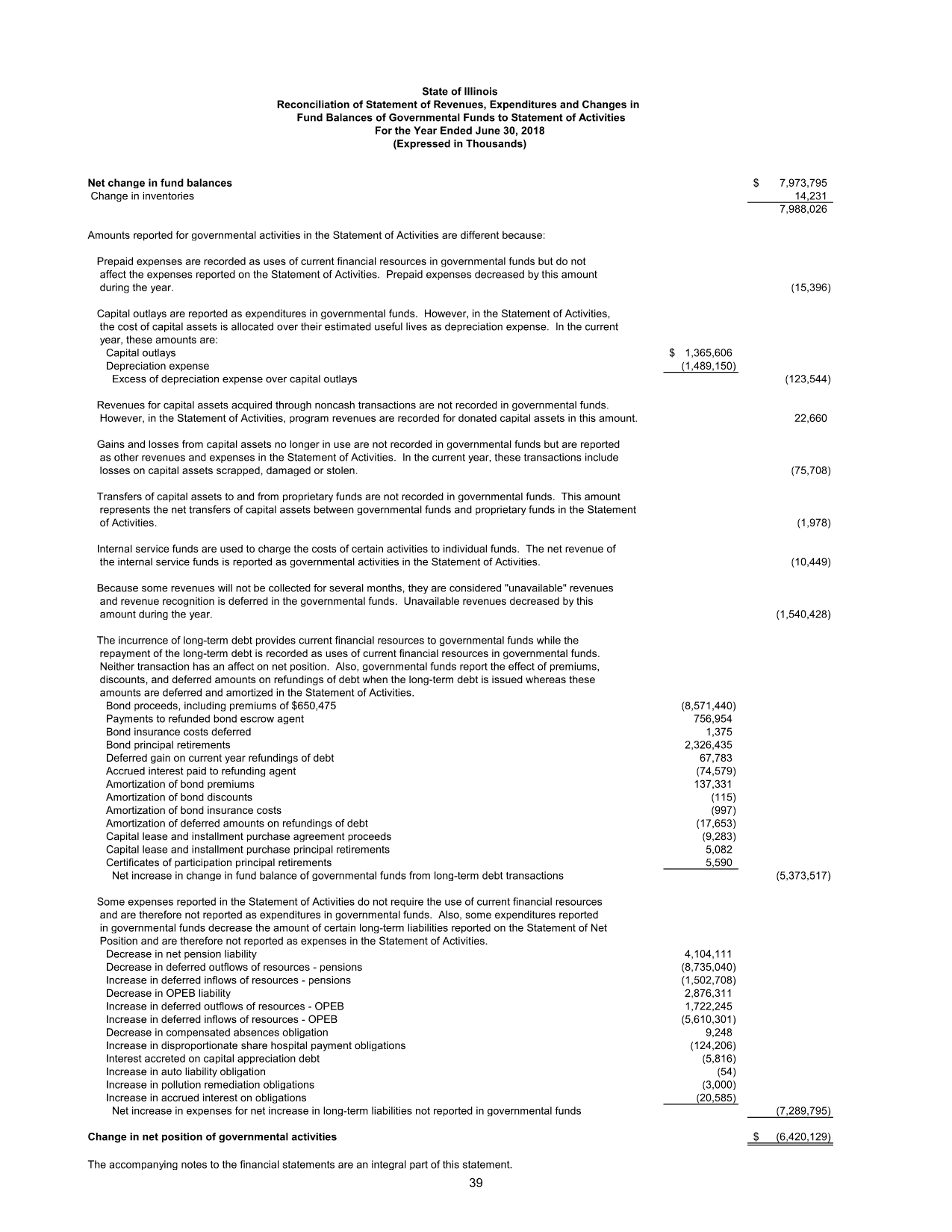

This is a common trick politicians use. I checked in with Sheila Weinberg, CEO of Truth in Accounting, about the Illinois CAFR issue. She repeated what she has long taught: “General fund accounting is incomplete and misleading, for many reasons including the fact that bond proceeds are accounted for as income.” (For those interested in the details, see the page from the CAFR reproduced below listing all the items ignored in the Governmental Funds, which include the general fund, which is why it is so misleading.)

Mendoza certainly had a different lens on CAFR numbers two years ago when we had a governor she didn’t like, Bruce Rauner. Her press release for the 2016 CAFR started as follows, focusing on the entire net position instead of just general funds:

With no relief in sight, Illinois’ finances deteriorated at an alarming rate in fiscal year 2016 as net deficit totals spiked to a staggering $126.7 billion…. The State’s [CAFR] paints a worsening outlook for the State’s financial future on this unsustainable path. Mendoza said the CAFR findings reflect a lawless fiscal climate.

Well, that “staggering” negative $126.7 billion is now negative $184 billion. It had worsened by $5.8 billion under that “lawless fiscal climate,” which is about the same as last year if you ignore the OPEB loss. No moral outrage now from Mendoza, however.

I called Abdon Pallasch, Mendoza’s press director, to comment on why I thought her most recent press release is so misleading. “It’s all in the CAFR” that was published, he said, adding that they selected the parts they did, focused on the general fund, and that those wishing to write about other aspects can look at the other sections.

Yes, literally read, Mendoza’s press release is correct. I say it’s also grossly misleading.

Keep in mind that the 2018 fiscal year was an unusually good year in the markets, which temporarily reduced the state’s deficit. Stocks returned some 14% that year, about twice what the state pensions assume they will return per year. That allowed the pensions to actually improve a bit – the net unfunded pension liability shrank by $4 billion to $134 billion. Had they deteriorated as rapidly as they typically do, the overall report would have been far worse.

Finally, if you’ve been wondering how much the recent state income tax hikes would solve, you now have the answer. Those increases took effect at the start of the fiscal year covered by the new CAFR. They obviously didn’t materially change the state’s direction downward, even if you ignore the OPEB issue.

*Mark Glennon is founder of Wirepoints.

Page 39 from CAFR, listing matters not recorded in Governmental Funds that do impact change in net position:

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

“Our wonderful courts have made clear that these obligations are exactly like pension benefits. So, they cannot constitutionally be cut, and if the benefits ever weren’t paid, the retirees could sue the state directly, just as they could for their pensions.”

This is wrong. Public Pensions in themselves are unconstitutional. No government employee wants to refer to the original pension agreements, because those contracts will clearly show that the framers exceeded their constitutional authority. So where are those original contracts? Who was at the table? Let’s see them.

One August 20, 2019, two days prior to releasing the State CAFR for the fiscal year ending June 30, 2018 on August 22, 2019, the Illinois Comptroller’s office published its most recent YouTube video titled, “2019 State Fair Video.”

Oddly titled since the video is not about the State Fair.

In the video Susana Mendoza states, “…I serve as your fiscal watchdog.”

https://www.youtube.com/watch?v=kz2ifyRI8i0

Here is the channel’s playlist of 44 videos beginning with the March 6, 2017 video titled, “Governor Rauner, #DoYourJob.”

https://www.youtube.com/channel/UCrgG0yQBYsUvYFmn_KjfVxw/videos

Not a single video about a CAFR.

In fairness to Reuters, they did explain what happened fairly clearly–“State Comptroller Susana Mendoza attributed the improvement mostly to proceeds from the 2017 sale of $6 billion of general obligation bonds that were used to shrink an unpaid bill backlog, which had ballooned to a record $16.67 billion as a result of a budget impasse. The state’s bill pile totaled an estimated $6.44 billion on Thursday.” If readers need to be hit over the head and told that it’s like taking a cash advance on your credit card to pay off some bills, that’s the job of sites like this… Read more »

What they did was report accurately what Mendoza claimed, which, taken literally, was correct. But a news source like Reuters, which has financial expertise, should be expected to go beyond just stenography. They knew or should have known that what Mendoza claimed was very misleading. I can’t see why they wouldn’t have gone further, emphasizing some other numbers from the CAFR that were more meaningful, just as Bond Buyer did.

“If readers need to be hit over the head and told that it’s like taking a cash advance on your credit card to pay off some bills,”

Surveys show that many people think this is a good idea, especially if paying those bills means dipping into your emergency savings. The question should be how did we get into this situation in the first place.

Regarding OPEB, the CAFR states “Because plan benefits are financed on a pay-as-you-go basis, the single discount rate is based on …” If it’s pay-as-you-go, why use a discount rate at all?

Yup, there is no sense to that. When we eventually get the resources we need and have the time, we want to really expose the whole OPEB story. Their rationale for discounting the liability is that they are applying pension-like thinking, and asking “how much money should we really have set aside to cover this obligation”? That makes no sense for a pay-go system. The liabilities should be discounted at the projected inflation rate, and no more. Instead, they’ve been using 4.5% or so.

Mark–dumb question, do the OPEB benifits have any manditory required payments like supposed actuarial calculated pension payments? Are unions, like thier pensions, panicing anout OPEB benifits so far in the whole? And do they have any legal recourse to demamd payment,,or have suzie m start confiscating municiple taxes?

As a pure pay-as-you-go system, there is no required contribution to cover future costs. Instead, the state just pays current medical bills as they come in. You’d think somebody would be panicking about how they will be paid. Nobody has because, as we’ve been writing, nobody has been covering this. Yes, the retirees sure do have a legal claim. Our wonderful courts have made clear that these obligations are exactly like pension benefits. So, they cannot constitutionally be cut, and if the benefits ever weren’t paid, the retirees could sue the state directly, just as they could for their pensions.… Read more »

Hi Mark,

Isn’t this as unsustainable as the pensions? I don’t see taxpayers being able to pay this long-term just as I don’t see taxpayers being able to pay for the pensions long-term. I am hoping the next recession forces all this to collapse. Thoughts?

Poking around the Comptroller site, I noticed pension payments into SURS last year were oddly staggered:

SEP $10M, NOV $40M, JAN $47M, FEB $8M, APR $110M. Contributions seem to be made arbitrarily. Other pension systems had a consistent monthly amount (basic amortization).

https://bit.ly/2kDGbmy

Looks like you triggered somebody, Mr Glennon. Funny thing is, whoever’s doing this is simply confirming what you’ve written. Dems will never understand the Streissand Effect. lol

Mark, I’m afraid that your comments section for this article is under attack from the friggin alphabet. Someone from Mendoza’s office must have just gotten into work and is having fun with their keyboard.

That’s from a state employee dropping their donut on the keyboard. The crumbs are causing misfires.

“Oh $&%@, Glennon’s onto us!” lol

A thousand thank you’s to you, Mark, for pulling together this article.

Mendoza is a complete POS.

Excuse me, but that’s just being rude… to the POS.

When will IL be forced to use GAAP standards when creating, managing and reporting on our budget?? All this “creative” accounting just keeps perpetuating the lies from our Governor & Legislators. And how do we force them to eliminate all the fake “unfilled” jobs across all government units and counting them as a liability? Until they are forced to tell the truth these are some of the reasons why we should vote against the graduated income tax.

That will require defeat of something like the military-industrial complex. Here, it’s the muni bond-politician-accountant-actuary-pensioner complex, and it’s mighty formidable.

And what shred of integrity can the press or outfits like civic fed possible have at this point by just goobling up all the mendoza/machine spin, especially crains–if your a fincial reporter at crains, like hinz. Wouldnt you be the least bit embarrassed

Journalists and reporters don’t have any shame. They’re all scum. I’ve always despised the main stream news media. SO glad when Trump came along and said what every one of us was thinking.

If Illinois can cut its deficit in half under the current flat tax structure, there’s no need for a constitutional amendment. Why mess with success?

Mark and or Ted,

So when will Madigan and Cullerton be forced to allow bankruptcy for cities and towns in Illinois? We know they will have to sooner than later, but what is it that forces them to do it in your opinions?

Enough with the numbers! Just tell me how much weed does each Illinois household need to smoke to eliminate the deficit.

Don’t forget, Illinois households with incomes below $50,000 can’t afford weed, so the more wealthy will have to smoke extra to make up the difference.

That’s why the city is proposing “reparations.” Reparations is just a code word for money for flat screen TV’s and marijuana.

Now we know why the new Governor wants (desperately needs) to amend the Constitution to impose a new graduated income tax. It is a cynical patch for continuation of the same kind of unbalanced budget deficit spending that has reduced Illinois to essential bankruptcy . If this open door tax change were ever to be approved, there aren’t enough fat cats who haven’t yet left town to hit with the confiscatory new rates that are needed, and EVERY average taxpayer in Illinois , now with lost Constitutional protection , will be personally hit with ever growing tax rates until everyone… Read more »