Opponents of reform like to blame the pension crisis on “underfunding” – that for decades taxpayers haven’t paid enough into the pension funds. But pension promises to state workers have grown so fast, and have become so generous, that taxpayer contributions could never keep up.

In fact, total pension promises owed to state workers have grown by more than 1100% since 1987, four times faster than Illinois’ economy.

Overpromising, not underfunding, is the real cause of Illinois’ pension crisis.

Illinois lawmakers are to blame for the state’s overwhelming growth in pension promises.

In 1970, lawmakers added a clause to the Illinois Constitution that banned any reduction to pensions, but didn’t add any language to stop future politicians from doling out more, and bigger, benefits.

State workers’ overgenerous benefits

Illinois government workers can expect millions in retirement benefits thanks to a combination of:

Early retirements, generous cost-of-living adjustments, salary spiking, pension pickups, sick leave service credits, and more.

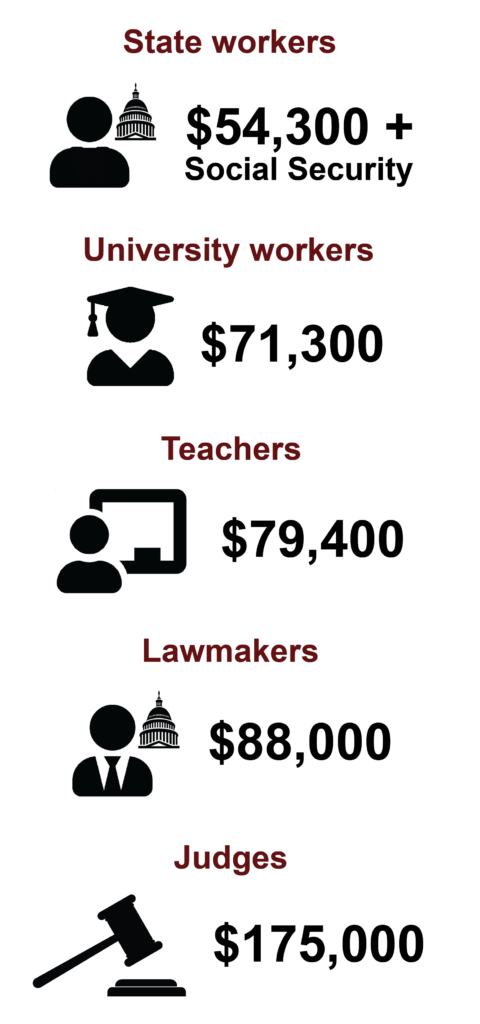

The average annual pension for a recently retired, career state worker is:

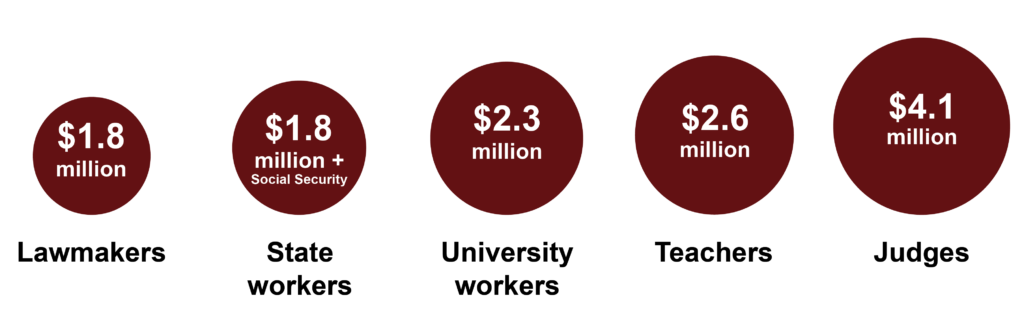

The result is a lifetime pension benefit ranging from $1.8 to $4.1 million for the average career state worker. By comparison, private sector Illinoisans would need $1.5 to $3 million in their retirement accounts to receive similar sized-benefits.

At the top of Illinois’ pension list are superintendents, professors, judges, lawmakers and more who receive millions in benefits over the course of their retirements.

Whether it’s the average career pensioners or the top earners, the retirement benefits offered to state workers are far more than ordinary Illinoisans can afford to pay for.

Illinois lawmakers’ long history of failure

Illinois politicians have never actually tried to solve the state’s pension crisis. Instead, all they’ve ever done is pass “fixes” that perpetuate the problem.

Gov. Edgar created an irresponsible pension funding ramp in 1997 that pushed the state’s debt onto future generations.

Pension obligation bonds, issued by Gov. Rod Blagojevich in 2003 and Gov. Pat Quinn in 2010/2011 did nothing to reduce Illinoisans’ overall debt burden.

Lawmakers’ 2011 reduction of pension benefits for new workers – called Tier 2 – did nothing to reduce already-existing debts and may yet be unwound for legal or political reasons.

And massive income tax hikes in 2011 and 2017 failed to solve the crisis despite the billions of taxpayer dollars that were poured into the pension systems.

Illinoisans can’t afford another “fix” from politicians. The pension crisis has already done too much harm to Illinoisans.

Wirepoints’ pension solution

Learn the basics of how Illinois got into this mess: