By: Ted Dabrowski

It wasn’t discrimination that bothered us most about Bally’s Chicago’s public offering for shares in its new casino project. What really got us were the claims that this investment, restricted to women and minorities, was sold by Chicago as an opportunity for investors to build “generational wealth” and as a “benefit to the black community.”

Hogwash. The offering is complex and risky as hell, from everything we can calculate. It’s impossible to tell what the payoff will be, given the structure of the deal and the company’s 40+ pages of “risk factors,” from construction to crime in Chicago. The payoff for the type of the shares I was trying to buy could be as far out as 20 years, if ever. If you have tons of money and can stand to put on some risk in your portfolio, then that’s one thing. But if you’re a low-income minority investor with little money to risk, then watch out. Bottom line, this isn’t an investment for unsophisticated investors, minorities or not.

The effort to bar white males from the right to purchase shares only made the offering worse. That was clearly unconstitutional, as my colleague asserted in court. Bally’s finally removed that prohibition, which has already been reported.

As an ex-finance guy, I wanted to see exactly what Bally’s was offering. So I went to Bally’s website with the purpose of buying my own share. My mother is from South America, making me a qualified minority, so that gave me access to the offering. I applied to buy one share for $250, subject to Bally’s getting approval from the SEC for the original minority-based offering (which it never got).

And that’s where things got interesting.

I was effectively buying a share with a supposed valuation of $25,000 even though I was only putting up $250.* That’s because in the structure, Bally’s “lent” me the remaining $24,750 bucks at an 11% annual rate, with interest compounded quarterly. (The loan was “non-recourse,” meaning Bally’s couldn’t come after me for that money.)

Under the structure, the company would first have to use its cash flows to pay off my “loan,” and I would only get a dividend on my investment after my loan was paid off in full.

The problem is, for every year that the company didn’t have cash to “pay off” my loan, the outstanding loan amount would grow by 11% each year, making the probability that I would ever get a return on my investment extremely low.

The details

The company estimates it might take 3-5 years for the casino to generate cash flow: “Given the capital intensity of developing, constructing, opening and operating a casino resort project of this scale, we currently expect that Bally’s Chicago OpCo will not have any OpCo cash available for distribution until approximately three to five years after our permanent resort and casino begins operations.”

And that matters because the loan, if unpaid, grows dramatically each year. Don’t take it from me. The company provided three payout examples in its registration statement Form S-1.

We show below only the projections for those buying one $250 share. FYI, Bally’s does say these “illustrative examples are not projections, goals or targets.” But as prospective examples, they’re the only information I had to go by. And there’s not much promise.

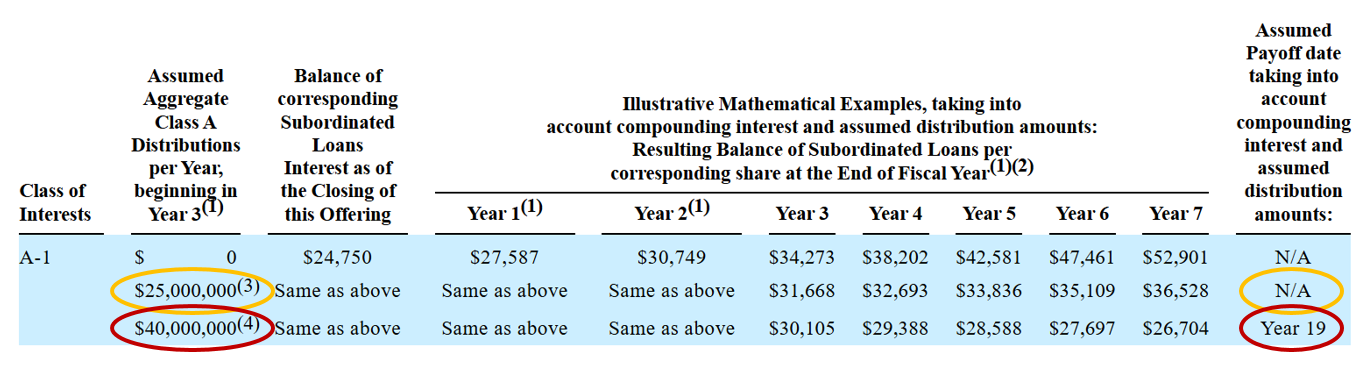

Scenario 1

In the first example, the company assumes the soonest it will have cash flow for distributions is in Year 3. The good news in that best-case scenario, assuming the company has $40 million a year in distributions going forward (circled in red), shows that my loan would have finally been paid off…by Year 19! Only then would I start to get a return on my now $25,000 investment.

But if the company could only distribute $25 million a year (circled in orange)… then I’d never get a return on my investment.

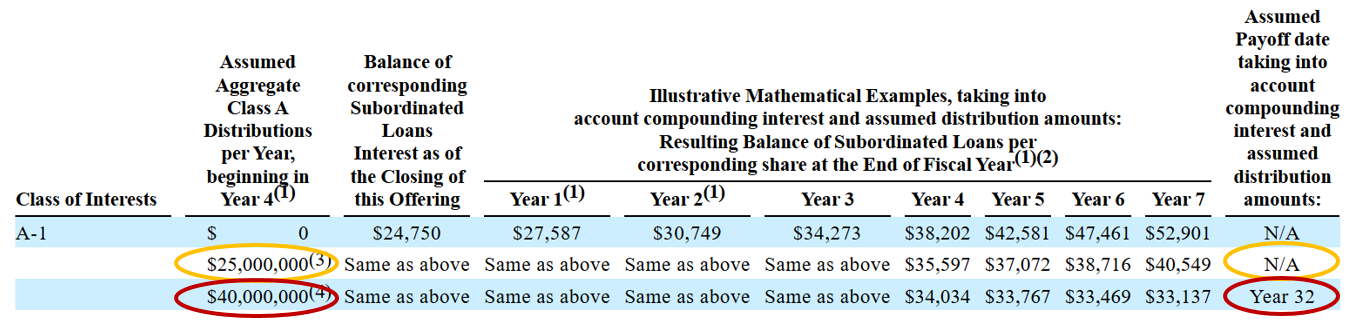

Scenario 2

My chances to see a return are even more grim in the second example. The company assumes it can make distributions beginning one year later, in Year 4. Again with $40 million to distribute each year, the example shows I have to wait until Year 32 to get a payoff.

With just $25 million to distribute…again zilch.

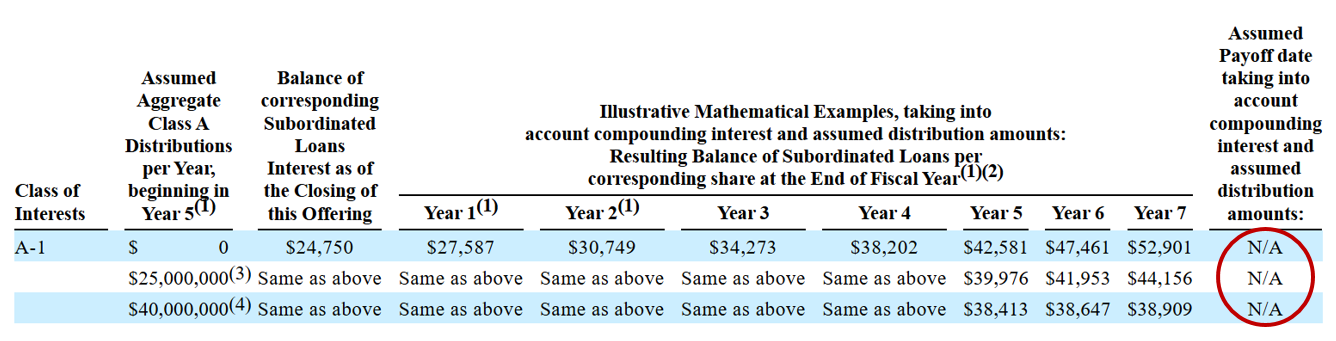

Scenario 3

In the third example, the company assumes distributions begin in Year 5. The good scenario? There is none. My loan balloons so much by Year 7, to $38,909, that it seems there’s not enough money for me to ever get dividends. I lose out.

To understand how messed up this investment is, if the company has no money to distribute toward our group of investors for the first seven years, my loan, which starts at $24,750, will have ballooned to $52,901.

Ripoff

Talk about creating “generational wealth”… even under the best case scenario presented by Bally’s, it would take a generation to see some returns. Yes, we understand that those aren’t formal Bally projections, but what’s a nonprofessional investor to do? After all, they were the targets of the city’s officials.

I am not an investment advisor, so do as you will, but one thing is for sure: If you don’t fully understand all the details in the revised public offering, it’s not for you.

*There were three other tranches in the offer for minority investment, each with increasingly less risk. Here is a link to the S-1.

Read more from Wirepoints:

- The Real Scandal in Bally’s Chicago Deal: Exploiting Minorities While Pretending to Help

- No White Men Allowed in Bally’s Chicago Casino Share Offering Promoted by City Officials

- Lawsuit filed by Mark Glennon against City of Chicago, Mayor Johnson and Bally’s alleges blatant discrimination

- Update on discrimination lawsuits against Bally’s Chicago and City of Chicago

Audio and summary

Audio and summary  If this bill passes, say goodbye to local control over all Illinois parks and expect to see open drug and alcohol use, needles, no sanitation and fire hazards, but no ordinary park users.

If this bill passes, say goodbye to local control over all Illinois parks and expect to see open drug and alcohol use, needles, no sanitation and fire hazards, but no ordinary park users. Expect no retraction or apology. This what they do.

Expect no retraction or apology. This what they do.

Could anybody imagine that a billion dollar project negotiated with democrats from Cnicago, Cook County and Illinois would be rife with corruption? Who would think such a thing…..everybody with less than an ounce of common sense.

I assume Bally’s is getting some sort of subsidies/tax write-off for all this?

I didn’t dig as far as you did, but the minority-come-on sounded like a great way for minorities to lose money…. I mean, wtf? How is this helpful at all?

It;s truly appalling how the regular media has ignored this aspect of the story. It’s the Illinois establishment exploiting blacks in the name of affirmative action, yet they ignore it.

Thanks for this info that no one else seems to be covering.

What’s even more nutty is Melissa Conyears-Ervin has turned City Treasures Office into some kind of bizarre hip-hop black wealth building site with her BWTT with black celeb /investor huckster speakers, etc (https://chicagocitytreasurer.com/bwtt/) (https://youtu.be/IushTQpWG2k?si=OMJxC2QOAjlJZ7Mo). Is what she’s doing even legal?? Truly unbelievable!!

Ted, thanks for analysis. Looks like a complete scam. Are any of the local media explaining this to Chicago residents? If it’s such a good deal maybe the pension funds should invest….lol

Good point. The investment staffs at the pensions are generally good, smart finance professionals. I’ve known quite a few of them. I assure you they would ridicule the daylights out of this “investment” if they could speak freely.

Sounds like just another way for liberal democrats to keep their favorite victim class in place and under control to maintain the tax cash flow for the never-ending programs…while sounding like they are doing them a favor.