By: Mark Glennon*

Updated 1/16/15

As if Illinois public pensions don’t have enough problems, it’s becoming evermore apparent that the Tier 2 reforms enacted in 2010 are a mess.

Some background: In 2010 Illinois created a second, lower level of pension beneficiaries for all state and local pensions, except for several Chicago pensions. Employees hired after 2010 became Tier 2 pension participants with far lower benefits. Tier 1 employees who started before that kept the same, more generous benefits they had before. The state’s unfunded pension liability, officially about $106 billion and in truth more like $250 billion, was incurred entirely through Tier 1 employees and retirees.

Overdue candor on Tier 2 unfairness recently came in the Winter 2015 Report from TRS — the state teachers’ pension, which accounts for about 60% of the state pension debt. That report further includes some welcome discussion about a regulatory quagmire looming for the whole Tier 2 reform package. But the report also contains a glaring and irresponsible misstatement. Understanding those three points is essential to fully understanding what a mess the Illinois pension system has become.

The first problem is that public employees in Illinois who started in the last four years are getting a far less generous deal than Tier 1 employees, even though both groups generally contribute the same percentage of salary towards their pensions. Tier 2 employees pay much more than their fair share to subsidize Tier 1 employees, assuming TRS measures the cost of those benefits correctly.

In fact, at least for TRS, which represents over 60% of the state pension unfunded liability, Tier 2 employees contribute more than what it takes to adequately fund their own projected benefits even with no help from taxpayers. An additional 2.4% comes out of their paychecks to help bail out Tier 1’s debt and pay its higher benefits. In that Winter Report, TRS Executive Director Dick Ingram explains it this way:

Tier I member’s pension costs roughly 20 percent of an active member’s salary. Because of the benefit reductions in Tier II, a Tier II member’s pension is worth just 7 percent of an active member’s salary. However, by law, active Tier II members of TRS…pay the same 9.4 percent salary contribution to the System that active Tier I members pay. What all this means is that Tier II members are paying the entire cost of their pensions plus an extra 2.4 percent to TRS. That extra 2.4 percent subsidizes the pensions of Tier I members.

It’s as if a private employee funded his entire 401(k) with no contribution from his employer, and was forced to pay an extra amount to fund some other guy’s much larger account. But there’s a very important caveat here. Pensions understate the true cost of projected benefits. They guaranty those benefits, yet calculate their cost using unguarantied, risky return assumptions. Consequently, though Tier 2 is getting a worse deal than Tier 1, that does not necessarily mean Tier 1 is getting a bad deal.

The second problem for TRS, according to the Winter Report, is that Tier 2 looks like it will run afoul of Social Security rules, forcing members and their school districts to start paying the 6.2 percent federal Social Security tax, and creating a range of other problems. Pension benefits must meet certain minimums to avoid that result, and TRS says it appears Tier 2 benefits soon will be too low. “Because Tier II members will be added to Social Security one at a time,” the report says, “we anticipate it could be an administrative nightmare for school districts, create unexpected strain on local school budgets and impact efforts to hire and retain the best teachers.” Add that to the list of problems for Illinois’ broke towns and cities.

Those doses of honesty from Mr. Ingram at TRS were refreshing, but he goes on to make this misstatement: That the subsidy being paid by Tier 2 employees eventually erases the massive unfunded liability generated to cover Tier 1 employees. He writes,

If Tier II is left alone, it will accomplish its mission. The $61.6 billion TRS unfunded liability will shrink over several decades and eventually be eliminated because the state will pay less to the ever-growing number of Tier II members. In fact, at some point in the future, we estimate that Tier II members actually will help create a surplus of funds for TRS that effectively could eliminate the need for any state government contribution to the System.

With that kind misstatement being sent to pensioners, it’s no wonder some of the cranks among reform opponents might really think that the whole pension crisis is “fabricated,” which many of them often say. You can see their comments saying that in this blog post about the report by one of those cranks.

At least one major lawmaker also has directly made the false claim that Tier 2 alone pretty much solves the pension crisis. Senate Minority Leader Radogno (R-Lemont) regularly says it. Last Fall, she wrote just that, saying the pension system as a whole is projected to return to 90% funding “generally due to recent reforms that established benefit changes for newly hired employees.

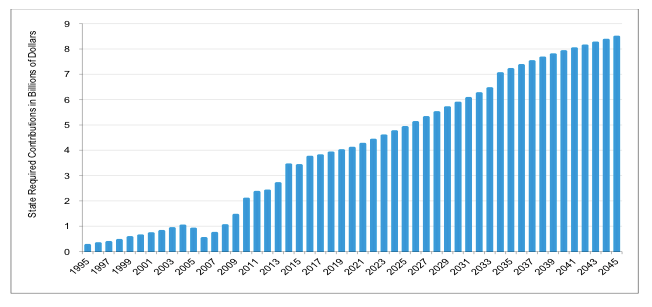

That’s nonsense. To repeat, it’s just $6.89 billion that’s to come from Tier 2 for TRS, compared to $246 billion from taxpayers. It’s the same story for other state pensions. If the state pensions ever approach that funding level under current projections and current law it will be because the state miraculously finds a way to pay the back loaded increases in taxpayer contributions over the next 30 years and the other bad assumptions used in those projections somehow prove right. “We’ll pay it later. Just stick it to the kids.” That’s what those projections really say, and TRS is an example, as shown in this chart of the projected taxpayer contributions to TRS provided on page 19 of its actuary report:

Agreement on solving the pension crisis requires, first, a common understanding of the facts and numbers. Whopping errors like those made by the head of the largest pension and the Senate Minority Leader don’t help.

The state has appointed a task force to study Tier 2 problems, but we haven’t heard anything from it yet, which is no surprise. I would imagine their tentative conclusion is, “OMG!”

Finally, it’s probably only a matter of time before Tier 2 members start suing or their unions aggressively challenge the disparity. For now, Tier 1 members are the majority and union leadership is Tier 1. That reverses, eventually.

To summarize what the 2010 reforms brought us: A comparatively unfair system for younger employees who are paying into a black hole that lacks even the funding to pay for the older workers they are subsidizing, a looming regulatory mess with Social Security, and a horribly wrong perception that Tier 2 reforms, if they hold up, will solve our pension crisis.

We’ve said it before and we’ll say it again: The pension system in Illinois is incompatible with any fundamental notions of fiscal responsibility and open government. It’s corrupt, corrupting and hopelessly opaque. Get rid of it as fast as fairness and the law allow.

Mark Glennon is founder of WirePoints.

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

The solution is simple. Move out of Illinois. Just leave.

The chart attached to this article shows required state contributions to TRS increasing from about 3.5 billion dollars in 2015 to 8.5 billion dollars in 2045. If you had even a basic knowledge of finance and math, you would realize that this represents a compound annual growth rate of 3 percent. In what way is this “unsustainable” when nominal GDP will grow at least 4 percent annually over that time frame? For those of you carrying on about “TRS 1970,” I fail to see the relevance to the issue at hand. Yes, benefits were increased between 1970 and 1989, in… Read more »

Andrew- Perhaps you have been away from Illinois too long because you are missing the point, which is that Illinois does not have the money to fund the pensions even at current levels, much less another billion every five years or so in the back years, even if that’s just a 3% annual increase. And the broader point, which is the one I actually made, is that the assumptions behind the state’s projections are not sound and considered in aggregate they are ridiculous. On that, you know full well that there is no reputable financial economist of any political stripe… Read more »

The higher contributions did not cover the higher benefits, that’s one of the main problems. Plus faulty assumptions are used in calculating the required contributions. Not every change effects every person. SURS Tier 1 is a very generous pension fund. As of 1990 there was no reason for further widespread hikes, but there were tweaks, choices, pension bonds (kick the can), plus legislation to reign in abuses. The Edgar Ramp most definitely affected SURS. The Edgar Ramp, Senate Bill 0533 (SB 0533), which was signed by Jim Edgar on August 22, 1994 into Public Act 88-0593 (PA 88-0593), created a… Read more »

House Joint Resolution 27 (HJR 0027) in the 98th General Assembly unanimously passed the House and Senate in May 2013. It created a Teacher Recruiting and Retention Task Force to work with the Illinois State Board of Education (ISBE). Since the task force is only focused on TRS Tier II pension benefits, the task force name is a ruse. The real purpose of HJR 27 and the Teacher Recruiting and Retention Task Force is to hike TRS Tier II benefits. Furthermore administrators receive TRS Tier II pension benefits also. Doesn’t Illinois want to recruit and retain the best administrators along… Read more »

There is a comparison of TRS Tier I to TRS Tier II on the TRS website. EZ Guide to Tier I and Tier II Retirement Under Public Act 96-0889 Tier I – Members Who First Contributed Prior to Jan. 1, 2011 Tier II – Members Who First Contribute on or after Jan. 1, 2011 http://trs.illinois.gov/pubs/EZguide.pdf Using the above document with the above comment, here is a comparison of TRS Tier 1 1970 to TRS Tier II 2011. Full Benefit ———————– 1970 ———————— 2011 Retirement Age —————— 66 ————————— 67 Years Worked ——————–45 ————————— 35* Accrual Rate ——————– .015 ————————- .022… Read more »

There are several other points to make about TRS in the context of this article. First, the notion that someday TRS Tier II members may have to contribute to Social Security. Well, members in the state worker pension fund, SERS, already contribute to Social Security, and that’s not portrayed as a negative by SERS or SERS members. State workers retire with very generous benefits. It would be a worthwhile exercise to compare the rules and benefits of TRS Tier II to SERS. Next, the formula and rules to calculate TRS Tier I pensions became more lucrative to the employees benefit… Read more »

You can’t trust TRS. In the majority of school districts in Illinois, thanks to board paid TRS aka pension pickup, the teachers contribute little or nothing to TRS. Ingram foregot to mention that. He would just say that doesn’t matter to TRS, because TRS gets the money from the school district irregardless if there is board paid TRS or not. Except if there is board paid TRS, most of the time that increases gross pay, I think most of the time it’s a Federal Tax shelter. TRS has a document about the scheme on their website. There is a culture… Read more »