Ted’s remarks at the City Club of Chicago event: “Chicago’s $838 Million Shortfall: Hard Choices Ahead”

Download Wirepoints’ accompanying handout: “Chicago’s Financial Crisis”

Today, we are here to talk about the city’s 2020 budget, but I’d argue that’s the wrong way to look at this crisis.

It seems to me that everybody, every year, treats the city’s one-year budget deficits as if that’s the real issue. As if that’s the real problem that needs to be solved. In fact, everybody breathed a sigh of relief when Mayor Lightfoot didn’t resort to a property tax hike to close the gap. That shouldn’t have been the big achievement.

That’s the problem. By focusing on-one year budgets, it’s like we’re treating an intensive care patient with aspirin. Chicago’s problems are far larger than a one-year deficit. Its problems are multi-year, multi-government and structural.

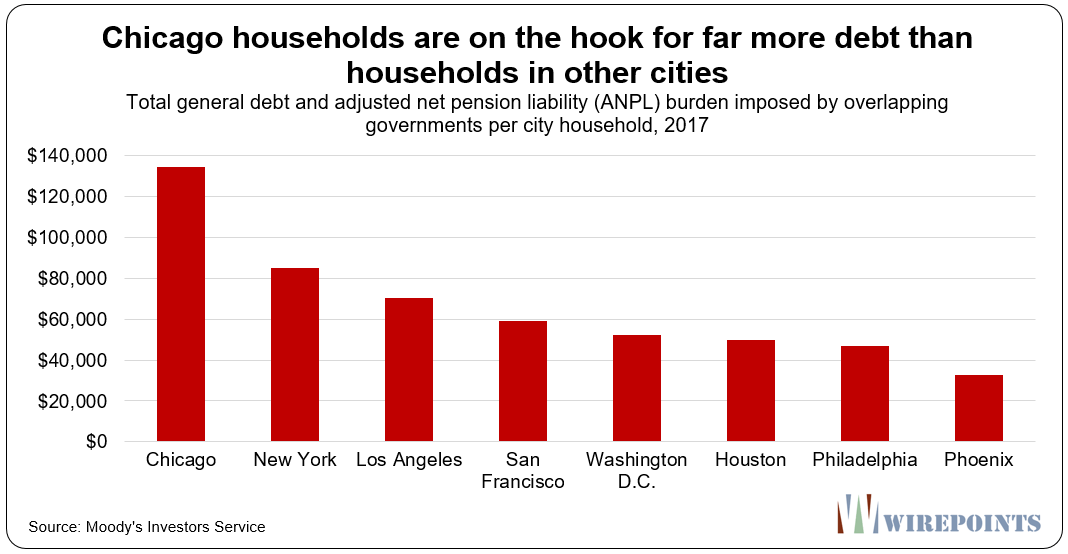

When you add them all up, Chicago’s problems make it an extreme outlier nationally. Chicago households are burdened with far more debt than any other major city in the country.

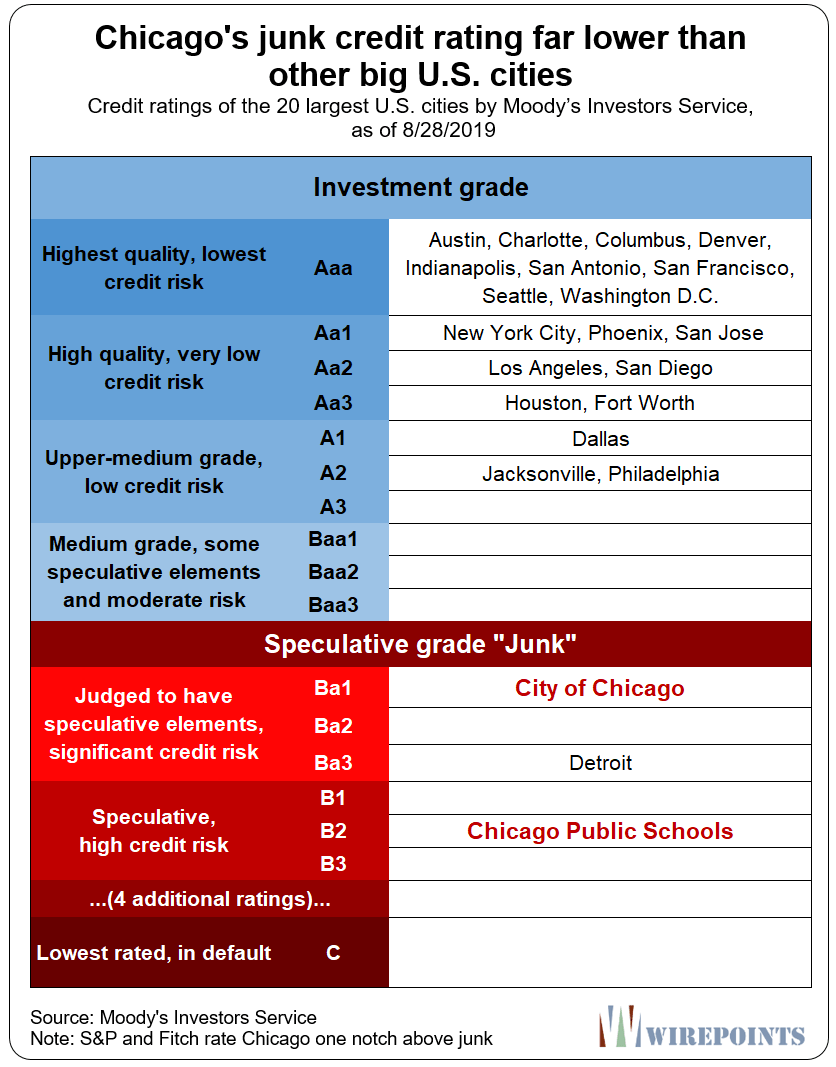

The city’s credit rating sits alone with Detroit at junk. CPS is even worse than Detroit.

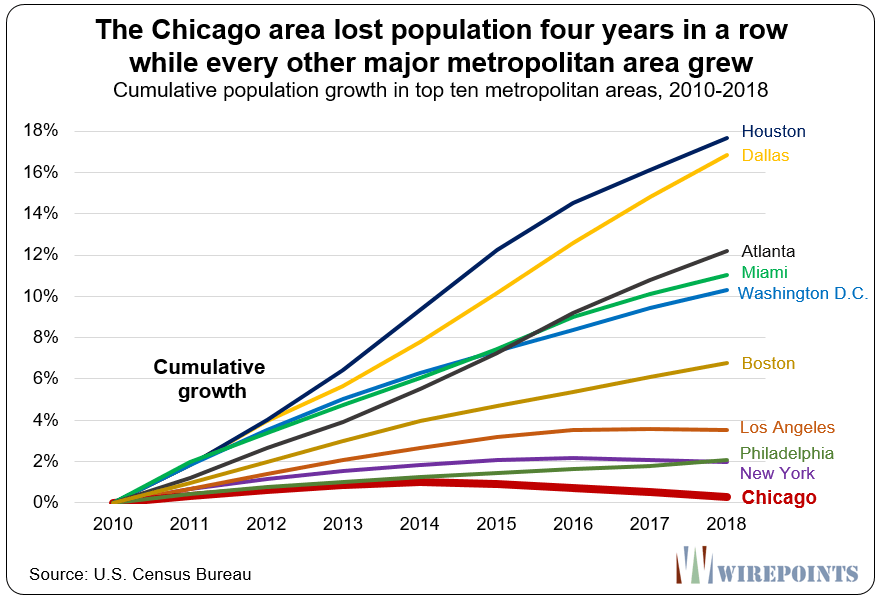

Chicago is also an outlier among the big cities in its population drop – nobody else has lost people four years in a row.

Chicago is also an outlier among the big cities in its population drop – nobody else has lost people four years in a row.

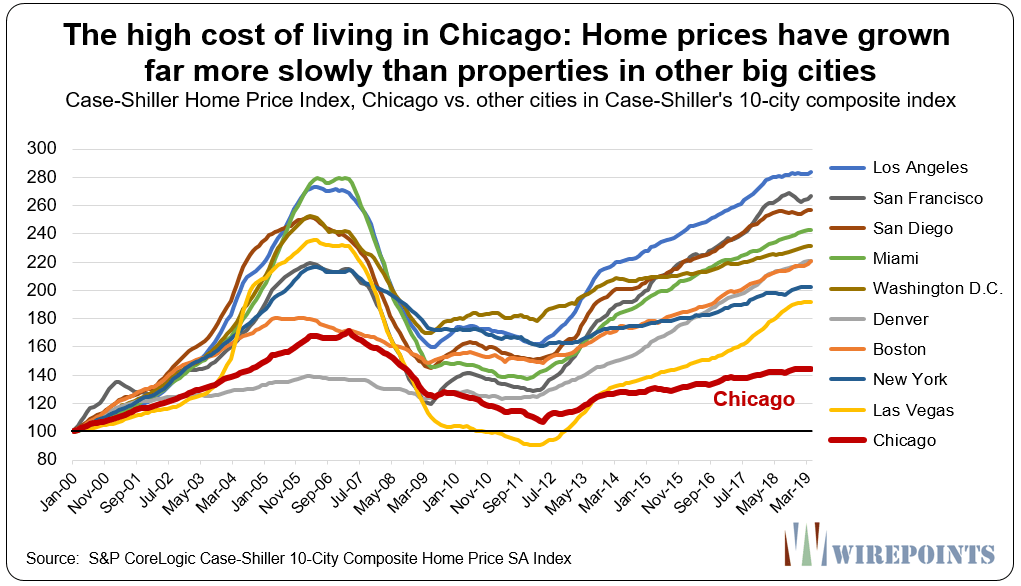

And property values, in real terms, are worth less today than they were in 2000. Chicago’s growth drags far below that of other big cities.

Focusing on one-year budgets only perpetuates those problems.

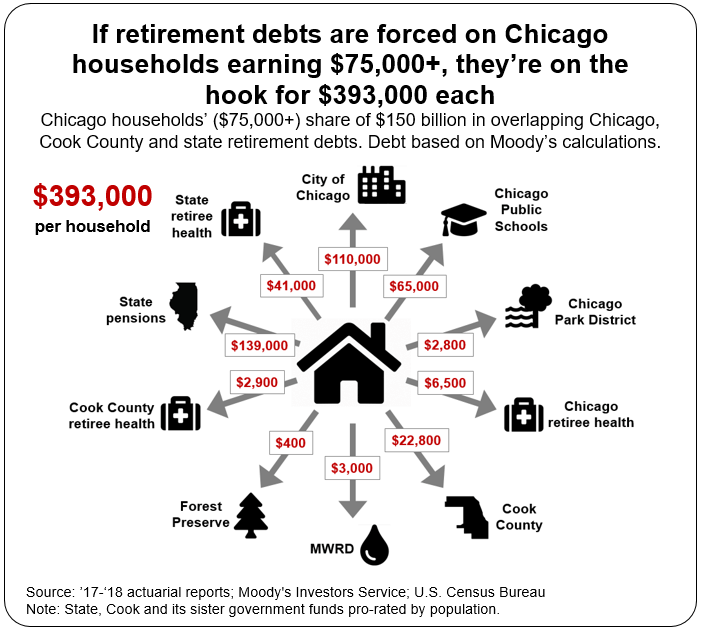

Our position at Wirepoints is that Chicagoans are stuck with more retirement debts than they can ever repay. Add up the debt of overlapping governments and put that burden on those households with the means to pay – say those making $75,000 or more – and you’re looking at a burden of $400,000 per household. That’s an impossible amount.

That burden will force more Chicagoans to flee, joining the 200,000 residents who already left between 2000 and 2010. And the city’s downward spiral will continue.

Chicago is in a mess because its politicians have failed to attack the city’s long-term problems: the cumulative, overlapping debts and the collective bargaining laws that end up inflating those debts year after year.

That’s why we’ve got to stop looking at these problems on a short-term, piecemeal basis. Because when we do it that way, one government in isolation, it allows lawmakers to get away with things that make no sense.

How else do you explain Mayor Lightfoot going to Gov. Pritzker to ask for a state takeover of city pensions, and then right after that, she offers what she calls the most lucrative contract in the CTU’s history?

If you are an ordinary Chicagoan, that doesn’t make any sense. And it shouldn’t. But it’s the system that we have. It enables the bad behavior by both politicians and the unions.

Every year it’s the same thing. Politicians try to put a patch on something that’s fundamentally broken.

But if they were to try and do things right, Mayor Lightfoot would change course and put together a workout team – a restructuring group – that determines how to reduce Chicago’s debts so that the city can become competitive again in taxation, services, and its economic environment.

She’d also use the bully pulpit as mayor of the nation’s 3rd-biggest city to demand an amendment to the pension protection clause and a rollback in collective bargaining laws. After the strike, she may consider that.

What I’ve just said is unlikely, yes, but I’d argue entirely necessary. And inevitable. The alternative is collapse. And nobody wants that.

Download Wirepoints’ accompanying handout: “Chicago’s Financial Crisis”

Read more about Chicago’s financial crisis:

- Lightfoot’s budget won’t stop Chicago’s downward spiral

- Chicago’s Pitch For New Bond Refinancing Is Mighty Fishy

- Chicago teachers strike: Why is no one talking about pensions?

- Here is the list of benefits Mayor Lightfoot is offering to the teachers’ union and why it’s terrible for Chicagoans

- Why Chicago’s Lightfoot should push for a pension amendment, not tax hikes

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

She has the biggest pair of glasses I’ve ever seen in my life. I have dinner plates smaller than her lenses.

Did anyone bother to confront the rating agencies and how they are continually rewarding the abuse of taxpayers? Why on God’s earth was S&p on the panel. They run the ponzi that prevents bankruptcy now. Funny how every tax increase results in a reward from raters. S and p needs to be clAss action sued. The market for Illinois debt needs to dry up not get rewarded. Then a cure can start. Raters need to be locked up.

Did anyone bother to confront the rating agencies and how they are continually rewarding the abuse of taxpayers? Why on God’s earth was S&P on the panel? They are the enemy of the People. We live on borrowed money and The whole existence of this ponzi can be blamed on the raters. Until the rating agencies are clAss action sued the cure of bankruptcy is impossible. So right now the borrowing ponzi needs to stop, the market for Illinois debt needs to dry up. Then we can start the cure.

It was especially disappointing to hear Carol Spain of S&P say two things. First, that Illinois’ population loss is mostly about weather. We’ve documented repeatedly how our neighboring states have no such problem. Second, she endorsed the horrible myth that Tier 2 reforms gradually eat away at the problems. Our unfunded pension liabilities are entirely for Tier 1 work already performed, and there is no connection other than a small subsidy that Tier 2s are forced to pay for the Tier 1 problem.

Mark – If I may add that Tier 1 retirees before 2010 had the ability to spike basically unlimited $$ compared to the rules of 6% after 2010 whereas a penalty is administered and school districts are notorious for exceeding the 6% cap (Rockford dist 205 over $3Mil in pension spike penalties). How much additional costs to taxpayers were incurred prior to 2010 vs after? Also if normal rules were applied to pensions (like the “average” salary of total years worked not the highest 4 years how much money could have been saved. Maybe we would not be nearly in… Read more »

“Also if normal rules were applied to pensions (like the “average” salary of total years worked not the highest 4 years how much money could have been saved.”. To some extent Social Security does that at least, although there’s no exact equivalence in how it’s done. I’m referring to the “inflationary adjustment” to wages earned during a career when the private employee’s initial Social Security benefit is calculated. Essentially there is an attempt to convert wages earned earlier to their inflation-adjusted equivalence today.

James-You probably know more about this than I do. I believe there is a safe harbor provision that if someone opts out of S.S. and Med an equal but not less than pension must be provided on a state or local level? It does not say more than but there are penalties for less than. Seems like anything offered above the equal should have been put into a 401K/Roth/etc. The maximum taxable S.S. salaries has changed thru out the years now being $132,900. How many school supers-professors/etc far exceeded that figure mostly picked up by the schools (taxpayer or thru… Read more »

If you want to understand why the city will opt to run into a brick wall before avoiding the brick wall, look no further than this panel. The Alderman and Spain are completely vacuous in the face of overwhelming evidence of the city’s dire fiscal situation. Bought and paid for shills, they get up in front of a crowd and spout the most inane nonsense about how the city’s attempt to trim a few million here and there will put the city on a path to fiscal salvation. Ted, you’re awesome and bring a gun to a knife fight with… Read more »

Well said. Unfortunately, when only one of three speakers is prepared to speak to the full scope of the crisis, the audience doesn’t know how to react. Ted speaks math fluently but getting in peoples faces or being confrontational isn’t his style. Maybe Ted should instead prepare someone like a Dan Proft for these type of discussions.

Glennon does that well. Gets in their faces and fights. He and Ted are great team for that reason.