By: Mark Glennon*

For those of us baffled by why the Federal Reserve Bank continues to flood the nation with money created from thin air, perhaps no aspect is more perplexing than one particular means it is using: the home mortgage market.

The harm may be severe in the long run, especially for Illinois, and particularly for the very people it is supposed to help – the working class.

The red-hot housing market has a number of causes, but a big one undoubtedly is the Fed’s unrelenting mortgage buying. Every month, it’s buying $40 billion of mortgage backed securities, or MBS, which are basically packages of home mortgages. That pushes up the value of mortgages for investors, reducing mortgage rates, which in turn fuels higher home prices. It now holds a stunning $2.2 trillion of MBS, about a third of all MBS outstanding, and it was all bought with money the Fed created.

That the housing market is on fire isn’t just from anecdotal or spot evidence. “In real terms, the home prices have never been so high,” says Nobel prize-winning economist Robert Shiller, co-founder of the S&P CoreLogic Case-Shiller home price index.” My data goes back over 100 years, so this is something.” It’s the “Wild West,” he says. According to a recent report by the St. Louis Fed, the nationwide house price-to-rent ratio, a widely used measure of housing valuation, is at its highest level since at least 1975.

It’s true for Illinois, too, though to a lesser degree. Chicago area home prices rose 9% for the year, according the most recent Case-Shiller Index, though national prices rose by 13.2%.

That’s thrilling news for existing homeowners, and new buyers are taking comfort that higher prices are offset by lower mortgage rates.

So, what’s the problem?

It’s that new buyers may be falling into a trap of high prices that cannot be sustained. To think that buying into a home assures you a nest egg as you approach retirement is old school. Home prices have fluctuated harshly in recent decades in most of the nation, often turning investments therein into losers. It has become a whipsaw; if you are in and out at the wrong time you can lose big.

The effects go beyond single-family homeowners. The binge has spiked construction costs for rental property construction as well. Everybody gets hit. Soaring lumber prices alone have added $36,000 to the cost of the average new home. “A stud that was $4 in April in 2020 was $12 in 2021,” said a Peoria builder. “It’s getting difficult to find anything.” Cement, steel, paint and many other construction elements are in short supply.

Meanwhile, here at home, the State of Illinois and cities like Chicago announce program after program to promote affordable housing.

They are fighting the Fed.

Yet we know for sure is that the Fed’s appetite for mortgages isn’t permanent. Federal Reserve President Jerome Powell has often said that its current purchases of MBS and other securities are “unsustainable.”

That means its upward push on home prices is unsustainable as well. New homebuyers, especially those of modest means who have stretched their credit to the max to make their purchase, are therefore at risk. They may benefit from low mortgage rates for the long run if they have locked in their rates, but values may not hold up.

To check whether that’s too pessimistic, I reached out to Joseph Pagliari. He’s a clinical professor of real estate at the University of Chicago’s Booth School of business. “I don’t disagree with you,” he said, “the Fed’s policy of monthly purchasing massive amounts of mortgage debt seems to have reached its past-due date.” He added:

In general, I’m opposed to the Fed’s willingness to provide persistent “assistance”, “support” or whatever name you/they would like to give to a market distortion. While I’m not the first to say it, the Fed’s willingness to attempt to “correct” seemingly every market “dysfunction” simply contributes to making the next crash worse; it’s like the forest fire analogy: If you suppress all the small fires, the underbrush accumulates, which makes the next fire more dangerous. Moreover, the political pressures to forestall any significant “tapering” seem like another consideration to me.

How much influence have Fed MBS purchases had on prices? That’s probably impossible to say, but it’s no doubt very significant.

Pagliari therefore didn’t venture an estimate, but he pointed me to a 2010 study by two Federal Reserve Board Governors on the impact of Fed MBS purchases during the Great Recession. The study found that the Fed program reduced mortgage rates by 100 to 150 basis points for purchasing houses. That means, for example, that a 3% annual mortgage rate would be 4% to 4.5% without the Fed’s subsidy.

That’s huge. A mortgage subsidy that large clearly enables many buyers, especially in the lower priced market, to qualify for a mortgage and pay up at today’s higher home prices.

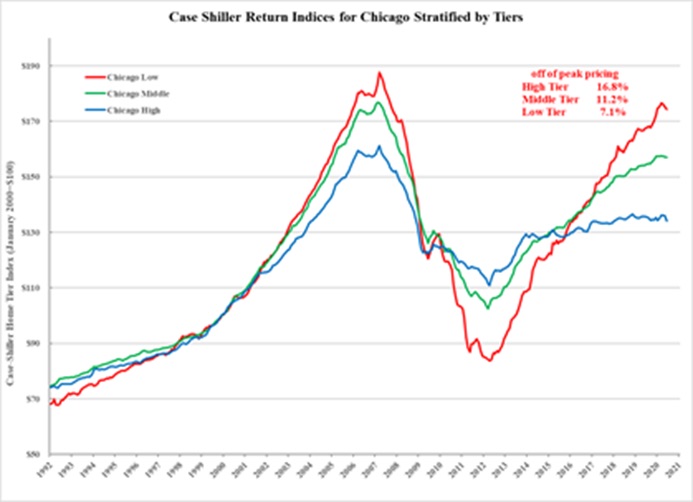

Pagliari affirmed that point about the working class and lower price homes. “Among the potential impacts of lower interest rates – due to the Fed’s policy of mortgage purchases – is the likely adverse impact on the lower tier of home prices,” he said. He sent along this chart as an example, prepared by one of his co-authors, Mitchell Bollinger, an industry analyst:

The chart shows Chicago area home prices stratified by price. Lower-price homes are the red, which you can see have been whipsawed the most.

Pagliari added this:

Over the last 20 or so years, the volatility of the low tier of home prices is self-evident: the peaks are higher and the troughs are lower than both of the other two tiers. I suspect that average homeowner’s leverage ratio is higher in the low tier of home prices. If so, does the Fed’s mortgage-purchasing policy contribute to the whipsaw of homeowner’s equity? And if true, it would seem likely that there’s a “contagion” effect by which the adverse effects of one or more properties lost to foreclosure (or at least financial distress) casts a pall upon neighboring properties, once there’s a significant downward market correction in home prices.

The Fed’s failure to state its reasons for buying mortgages is particularly frustrating. It “doesn’t have a satisfactory answer for why it’s throwing billions of dollars at mortgage bonds at this point,” as a Bloomberg columnist wrote last month.

Here’s Fed Chairman Powell’s answer when asked to state his reasoning. Read it and ask if he isn’t just saying, “Oh, I dunno. We’ve been doing it so we’re still doing it.”

Yeah. I mean, we started buying MBS because the mortgage-backed security market was really experiencing severe dysfunction, and we’ve sort of articulated, you know, what our exit path is from that. It’s not meant to provide direct assistance to the housing market. That was never the intent. It was really just to keep that as, it’s a very close relation to the Treasury market, and a very important market on its own. And so, that’s why we bought as we did during the global financial crisis. We bought MBS, too. Again, not intention to send help to the housing market, which was really not a problem this time at all. So, and, you know, it’s a situation where we will taper asset purchases when the time comes to do that, and those purchases will come to zero over time. And that time is not yet.

Thinking about Illinois in particular, our home price growth has lagged badly behind national averages. In just one ten-year period, subpar home appreciation cost Illinois homeowners a quarter trillion dollars.

On one hand, maybe that will help. Without the price bubble other states have, there’s less to deflate in Illinois.

On the other hand, the causes of Illinois’ poor home appreciation persist. High property taxes, structural government deficits, corruption, crime and all the rest go on and on with no reforms in sight, so taxpayers continue to flee.

I am not comfortable making predictions on this, but I am about calling out risks. New Illinois homebuyers, particularly at the low-cost end, may end up realizing that they bought into a surge created artificially and temporarily by the Fed. When the Fed’s largess ends, Illinois’ traditional problems, and their impact on home prices, may return with a vengeance.

*Mark Glennon is founder of Wirepoints.

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

The long and short of it – We are in a massive bubble. Greenspan was an economic menace and fostered the mortgage bubble of 2008. But that, with all it’s devastation and pain, pales to what we face now. Powell and Yellen are out of control, and are acting malevolent! The PPI is double digit. Powell gives no reasonable explanation for why the Fed says this to be temporary. People intuitively know America is playing with a firestorm.

The real fear starts when interest rates rise.

Take a $120,000 house at 3% interest. A homeowner will pay on average per year $3,600 in interest and $4,000 in principle for 30 years. People purchase a house based on monthly payment. If interest rates increase to 5%, the house value drops to $90,000 to maintain monthly payments.

Monthly payments rise as property taxes rise.

As property taxes rise, property values fall.

As property values fall, property tax rates rise.

Property values fall off a cliff when the pool of potential buyers excludes median income households who cannot qualify for mortgage loans because of insufficient debt-to-income ratios (monthly mortgage payments, including property tax escrow, exceed 43% of gross income).

That’s what cost us a hefty (nearly $45K) haircut selling our house in 2017. At the time our property taxes were $1K/month and were MORE than our mortgage payment (principal + interest). It was quite literally like taking a second mortgage payment for a buyer. So we had plenty of people back out of buying our house until we finally found a buyer who would commit. And that’s a loss off the purchase price. That doesn’t count the cost of the upgrades we added to the house during the thirteen years we lived in it. And have the taxes gone… Read more »

The right question to be asked: how many State-employed defined-benefits-entitlement workers does it take to completely destroy a community? The answer is: 10% of the community. When 10% or more of (working population of) an Illinois community is comprised of sociopathic predators who gain so much value from commanding the State-guaranteed pension/insurance/OPEB entitlements of Illinois jobs (teachers, government workers, and to a lesser degree—because these Americans actually put themselves at mortal risk–firemen and cops), the community is doomed. The anecdotal evidence of this assertion is 20 year economic history of Woodstock Illinois, It is not the only relevant Illinois case… Read more »

You can’t re-fi a property tax rate. Note the importance placed on the effect of a 1.5% difference in mortgage rates. In collar counties the property tax rates often exceed Chicago p-tax rates by more than 1.5% nominal difference. Woodstock p-tax rates are 3.5%, compare that to Indiana which has a p-tax rate cap of 1%. In Woodstock the rates rise as non-TIF property values fall steadily as measured against homes all over America and compared to inflation. Woodstock p-tax rate of 3.5% is off recent high of around 5%, but is expected to begin rising again as mayor and… Read more »

What’s that again, those who don’t study history a doomed to repeat it….

I can’t believe we’re repeating the same housing shenanigans from the 2000’s. We learned nothing.

Even if you sell your house at a “profit”, you still have to live somewhere. This might help if you’re downsizing, but works against you if you upsize. So while you made a $30K profit on your home sale, you paid $40K extra to live in your larger new home. And buying a rehab won’t save you money because the materials needed to rehab are now too expensive.

Every generation ends up learning the hard way how markets work. I can only hope a few young people get the warning.

The woke Federal Reserve.

Policy in the name of compassion.

Great article Mark. The financial education in our schools does not bring most of our population to this level of analysis. It is the buyers of lower priced homes and the young adults I have the greatest concern for here. The investors know they are investing in a habitually corrupt state, and just think it will all work out over time. Caveat emptor.

Young adults saving for their first down payment are getting 1% interest at their bank while home prices are appreciating 10%. They are effectively being priced out of the market until a correction or normalcy returns.

Exactly, anyone buying home today is speculating that the price will increase. Gimme dat sweet equity. But when prices fall (and they must sooner or later) they’ll be sending back the keys saying “The bank should have never lent me this money!”

Maybe you are right and home prices will crater back to “normalcy”, but there is also a good chance that the value of the US dollar has suffered a permanent and steep decline in value. We can raise the minimum wage to $15/hr, but workers will still face a reduction in buying power. Also consider that few new “affordable” homes are being built while we import more than 100k poor and needy arrivals every month. We already have a large homeless population.

There is a nationwide housing shortage that has not been seen for years and is expected to exists for a few years. Many young people sat on the sidelines after the 07 housing crash and now are in the market. Demand has increased and supply can’t be fixed easily. Also with the current price of lumber and other home building costs, building a new home is costing even more money. Sure building costs may return to “normalcy” but none of that will quickly fix the supply issue.

Real estate prices over long periods of time tend to appreciate near the rate of inflation or just slightly better. People make the mistake of putting their entire net worth into their homes and ignoring other investments like the stock market. Stocks historically perform much better than the rate of inflation.

Nationally, the home appreciation rate (end Q1 2020-2021) was 12.6%. The rate for Illinois was 9.6%, or 3% less than the nation as a whole. Suppose your Illinois home was worth $250,000 a year ago. It would now be worth $274,000. If your home was instead in Indiana (13.1% appreciation rate) your home would be worth $282,000. In other words, you lost out on $8,000 dollars simply by living in the wrong state. Indiana property taxes are approximately half of those in Illinois. From experience I know that taxes on a $250,000 Illinois home can approach $10,000. In Indiana your… Read more »

Oh, but we have all thiis “equity” here.

“Nationally, the home appreciation rate (end Q1 2020-2021) was 12.6%. The rate for Illinois was 9.6%, or 3% less than the nation as a whole.”

“They are effectively being priced out of the market until a correction or normalcy returns.”

So it sounds like you are saying that Illinois is doing a better job than the rest of the nation helping young buyers not get priced out of the market.

This is true. Lower home prices are a good thing for buyers.

But it is unfortunate that most of the country equates higher home prices with more desirability, which is why IN and TN and CO are experiencing an influx of new residents (one of my son’s friend’s family is moving to TN this month!) and IL attracts fewer new residents.

I’m now in Tennessee in a home of comparable value to what I left in Illinois. My real estate taxes are $6,000 less on my modest 1600 sq ft home. For a young person in Illinois, you not only have to worry about saving enough for the down payment but also saving enough to pay the yearly tax. The latter is much less of an issue in Tennessee.

Hey PPF, I appreciate you sticking it out with comments here despite the heat we usually give you. And you do a better job than most on your side to make your case.

Mark,

I appreciate you hosting this website and allowing people to make comments including those that disagree with your platform.

PFF, have you been drinkin’ again?

Based upon buyers mainly buying based upon “how much down and how much a month” is a great equalizer to other markets. Yes Illinois home prices have not kept up with the nation but the monthly payments do thanks to the escrow payments to the Illinois tax system and insurance escrow payments.