By: Mark Glennon*

Illinois Gov. JB Pritzker last month released a proposal to “fully fund” the state’s pensions. Some in the media celebrated the proposal in particularly irresponsible columns.

In truth, the plan is just another can-kick. It’s little more than expanded promises on pensions, pushed to future governors to deal with.

Here are the details:

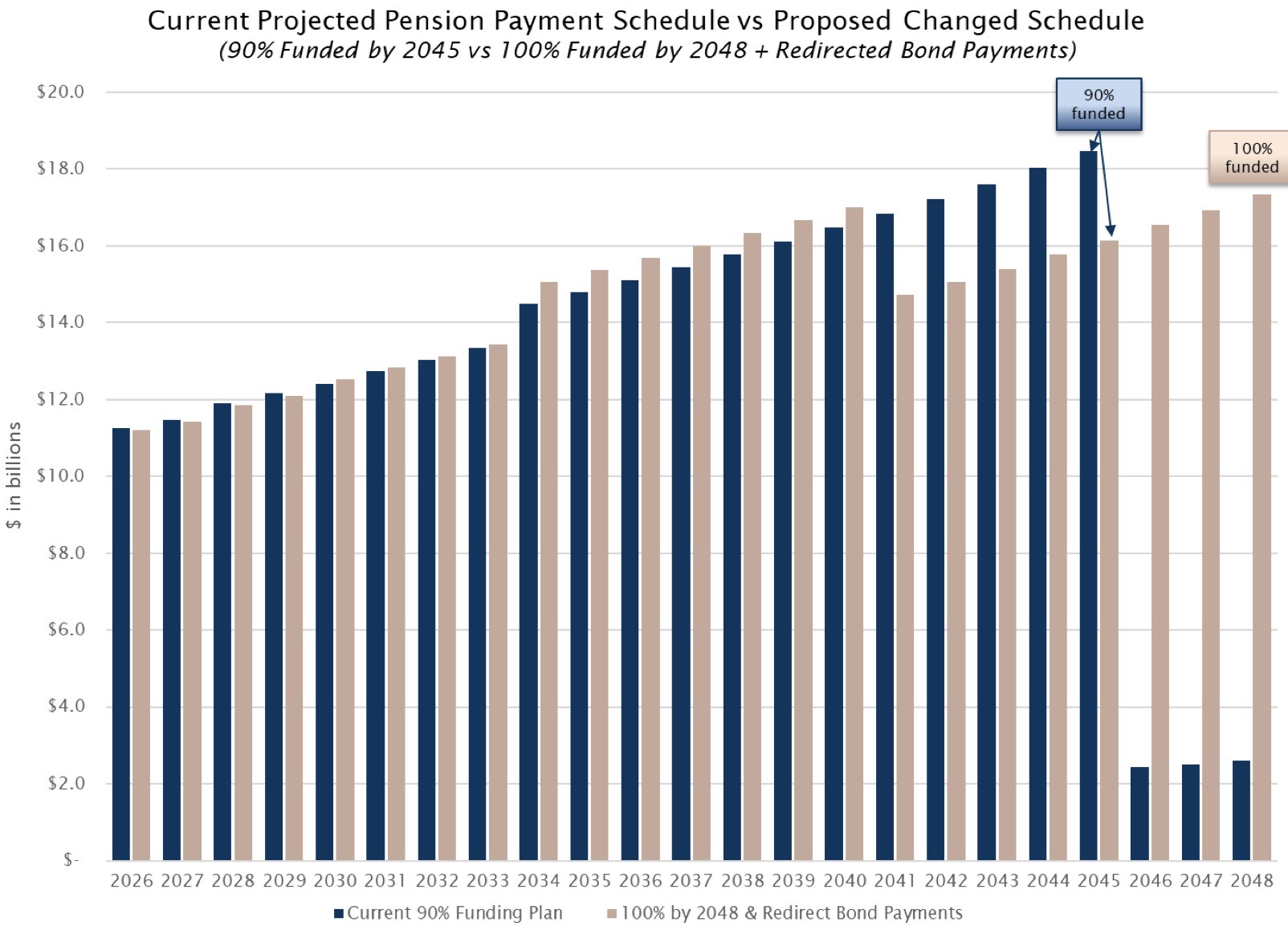

Under the current repayment plan for our underfunded pensions, the goal is to get the plans 90% funded by FY 2045. That’s the infamous “Edgar Ramp” established in 1995 under Gov. Jim Edgar. Today, the pensions are just 45% funded.

Pritzker’ proposal purports to get the systems 100% funded by changing the ramp and extending it to 2048.

Here is the key chart from Pritzker’s budget documents, where the proposal appears, comparing today’s Edgar Ramp to his new ramp. The dark blue lines are the current Edgar Ramp and the beige lines are Pritzker’s proposed ramp.

Here’s why it’s deceiving:

The new ramp is “overly backloaded, with annual payments increasing at unaffordable rates over time.” Who said that? Some “carnival barker,” as Pritzker calls his fiscal critics? No, that’s from none other than very progressive, tax-and-spend, Pritzker-friendly Ralph Martire of the Center for Tax and Budget Accountability, criticizing Pritzker’s plan in a Chicago Sun-Times op-ed.

Backloading is another term for kicking the can. It’s bad because pension debt effectively bears interest, so lower early payments mean bigger later payments. It’s a means of sticking the next generation with the cost of our generation’s recklessness.

You can plainly see that backloading in the chart above.

Note first that the new ramp apparently would actually decrease state pension contributions a bit each year through 2033. Pritzker no doubt figures he will be on to bigger things than Illinois governor by then.

After 2033, where will the state get the additional money for higher contributions?

That’s where the biggest gimmick is embedded. Specifically, Pritzker’s proposal is for the state to dedicate half the savings the state will get when two particular bond offerings are paid off in 2030 and 2033. Dedicating half of that money then would allow the state’s contributions to drop significantly in 2041, Pritzker claims.

But that’s just an empty promise about where a particular chunk of money would supposedly be used. A dedication to use half the savings from when a few particular bonds are paid off is no more meaningful than promising to use half the money from any other source. It’s no different than saying “We’ll pay lots later.”

That’s because a promise to use those future savings for future pension payments is ephemeral. It would not bind future governors and lawmakers. Even if the promise were made by law, the law could easily be changed with a few lines in any of the thousands of pages of budget bills or other legislation that come out each year. Nothing would stop future lawmakers from doing just that – as they would, assuming they behave like Pritzker, Edgar and so many other past lawmakers. They’d spend the bond savings on something else and kick the pension can again.

Finally, Pritzker’s ramp would push the full funding deadline out by three years, which is another can-kick.

However, Pritzker’s proposal would eliminate the charade of pretending that 90% funding is the appropriate funding level. Targeting less than 100% funding has long been criticized by pension actuaries, being little more than an effort to assume part of the problem away. Looked at it in a vacuum, it’s therefore good and overdue to change the debate to 100% funding. The problem, however, is that Pritzker’s means of getting there is shambolic.

Another gaping problem with Pritzker’s plan is that it ignores the Tier 2 pension mess. Tier 2 pensioners are those hired since 2010 who receive far lower benefits than Tier 1s – so low that they risk being less than Social Security benefits, which breaches federal rules. The state has never published a reliable estimate of the cost of fixing that problem, but it’s widely agreed that the cost will be high and will materially alter any pension contribution schedule.

Some of the press reaction to Pritzker’s proposal continues the tradition of poor reporting and commentary on pensions.

First is an op-ed in the Chicago Tribune by David Greising, president and CEO of the Better Government Association, praising the proposal. The BGS does plenty of good work, but Greising botched this one. Pritzker’s proposal “makes him the first Illinois governor in 30 years to propose a way out of this seemingly insurmountable pension problem,” Greising wrote. But Greising addressed none of what’s written above, apparently being captivated by the 100% funding goal.

Patrick Keck of the State Journal-Register also wrote approvingly of the plan, again seeming bamboozled by the 100% funding thing. “Shifting the goal to fully-fund pensions by 2048 would follow suit with states like Wisconsin and South Dakota that already have met those marks,” he wrote.

But there’s a universe of difference between being fully funded now, as Wisconsin and South Dakota are, and Illinois lawmakers saying they’ll be fully funded in 24 years. It’s as if Keck suggested to somebody deeply behind on their credit card debt to “follow suit” with those who are current on their credit card by promising to do the same by 2048.

Then there’s columnist Rich Miller, who turned to former Republican Rep. Mark Batinick to support Pritzker’s plan and tell us to chill about pensions. He quoted Batinick saying, “Republicans need to realize that while pensions are still a big line item in the budget, the problem is getting better, not worse. Pension costs are declining as a percentage of the budget. We are healing. Democrats need to realize that much of the money that has been available for new spending the last few years has come from that healing, not budget magic.”

But that decline in pension cost as a percentage of the budget (from about 25% to 20%) is only because the budget has exploded, rising 25% (from about $40 billion to $50 billion) from 2019 to 2024. Under that percent-of-budget reasoning, Illinois could get the percentage down to 5%, making Illinois close to competitive on pension burdens with other states, if we’d just raise the budget to $400 billion. Some comfort.

It’s not the first time Batinick has peddled pension deceipt. We ridiculed his 2018 pension proposal as such here and here. Republicans and Democrats alike saw through it and never considered it seriously.

Eleven years ago Democrats and Republicans agreed that our pension problem was so severe that only real pension reform would end the crisis. They said that in legislative findings and argued that in court. It was true then and it’s more true day. Then, the state’s unfunded pension liabilities were $98 billion. Today they are $143 billion.

But our leaders abandoned that effort and reverted to their traditional pension policy, which is deny, delay, extend and pretend. Pritzker’s new proposal is nothing more than that.

*Mark Glennon is founder of Wirepoints.

All Wirepoints research and commentary on Illinois pensions is collected here.

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

There is a 30%+ vacancy rate on the Mag Mile. Carloads of Bandits crash through the plate glass windows and loot profitable retailers. Just drive along West or South from the Loop to the city limits along any arterial city street and study the businesses you see And by the way, lock your car doors. Is there any hope that the sales taxes and property taxes can continue to support day to day Chicago services let alone future pensions? The only solution to pension solvency currently is the Biden solution; issue emergency proclamations and send money from all states to… Read more »

Hey everyone, things are going to be great in Illinois…….in 2043! Alas even that isn’t true because the value of the pension debt continues to grow ($2.2 Billion in FY 2023) in a year with greater than 15% return in the S&P 500. What will happen in the next down market year or when Covid money finally runs out in 2026?

Upon taking office as Governor, JB immediately wanted to kick the pension can and not make the required pension payment. Unfortunately for him the Trump economy was already roaring and state revenues were higher than expected, so JB had to back down. There were some who postulated at that time that Pritzker’s broken leg was a result of trying to kick the pension can, but whiffing. No surprise that he wants to give it another go. The guy has no shame, and no fear, as he knows the weak mainstream media won’t call him out.

True pension reform would include ending pensions after a certain date and offering new workers 401k with matching as in most of private sector. But the democrats power base in public unions will never permit that. Instead public pensions are more deeply enshrined by Pritzker and his party. Never talk of budget cuts and reallocation of funds, just tax increase and shell games.

Reform needs to include reduction of health care benefits, too.

Down votes on true pension reform? Speak up, why oppose it?

It’s very safe to assume that folks from the political establishment and far left come here routinely and just pound away on the down button, no matter what.

Which are also the same people – doing Democrat Dirty Tricks – posting the overtly racist racist/antisemitic rants here.

I am sure that the ilk from the liberal left are using multiple log ins and the true number of down votes is much less

Santa Pritzker is out on the prowl with a bag full of nice warm fuzzy feel good spending programs to secure Illinois votes. Never mind that the pension problems continue to grow hidden in the background as Illinois voters seemingly could care less preferring to focus on more welfare, more Medicaid, more furnishing of sanctuary to the world’s immigrants, and of course more funding for the Chinese to build plants that may or may not happen. It is the Illinoisans utopian dream that Pritzker is peddling and surprisingly so many believe it. Perhaps it is the math challenges of it… Read more »

What a quick downvote that is even quicker than the downvotes I get when replying to a Rich Miller article. I just wonder, considering the article is about Pritzker, if he himself monitors the posts here to quickly downvote any post that is not favorable to him. Imagine the anger as he can not delete a post but can only quickly downvote one. Have a nice day JB…we know its you.

Perhaps that’s some of what Thornley does now for Pritzker.

The sheeppeople of Illinois believe this stuff because the parrots in the Illinois press, as pointed out the Mark Glennon, come out in unison to dishonestly declare victory over squeezey the pension python.

This is all political theater for the “Pritzker For President 2024” campaign. JB will claim to have fixed Illinois pensions and the Pravda national media will parrot his press release and proclaim the silver spoon to be a financial genius.

the story of Pritzker’s “toilet Bowl caper” must get out to other cities where El Gordo

is trying to position for a presidential run. Voters must find out what a putz he is.

tell the sory far and wide to torpedo his chances.

Never thought he would make gov. after that caper……..hmmmmmm…..makes you wonder how he did!!

Please Obiden has been bad enough…….we DO NOT need this guy in the WH!!!!!!

It’s the combine. Republicans, especially in IL, are merely Democrats in better suits. They’re just looking for their cut. Mark, this silliness will not stop by electing Republicans. Most are better fiscally, but only marginally as so many feast at the trough too. Term limits, public financing of campaign’s, consolidate government taxing bodies, use referendums for advisory purposes to set policy. Eliminate “career legislators, pensions, lifetime health insurance, and ban them from lobbying. In fact, curtail; organized lobbying altogether. Clowns like the Trumpers and Tea Party people are only marginally better than the dems. We need the equivalent of a… Read more »

Also, pensions need to be aligned with reserves and revenues. There must be a formula to adjust the payouts so the system remains solvent long term.

cap payouts at 100,000. Index to same % as social security

eliminate ;lifetime BCBS coverage for legislators and all state employees.

legislators should get same level of coverage Medicaid grove while in office.

if their relative gets a job above a certain. Level, they must resign.

Term limits

shutn off the campaign money spigot.

Public ally fun d the campaigns Mark

With the possibility of Tier 2 benefits being enhanced even beyond the safe harbor minimum, it would behoove the pension system actuaries to perform what-if analysis on any enhancements to the pension systems. They should forecast what the liability would increase to if the retirement ages or employee contribution rates were lowered. Or if the final average salary or service year multiplier was enhanced in favor of the employees. They need to get ahead of this so when the usual suspects come around, we already have an answer of what that will cost and what impact it would have on… Read more »

Excellent article WP – You are the ‘rosetta stone’ of IL pensions it seems. Sadly Pritzker and IL Democrats, along with their many minions in the MSM, are largely just budget and pension Hucksters.

Of course it’s flimflam. There will never be enough money to pay the pensions. Any proposal that pretends otherwise is just a new fairy tale.

First think Illinois needs to do is STOP DIGGING.

Billions in COVID funds just went to more new programs need future funding.

Other than significant pension reform, i.e. cut cut cut, this state is headed to some kind of new state bankruptcy.

Charging a service fee (10%) on all state pensions to non-state residents would be a great start as well.

Largest generational theft in history.

It is the taxpayer’s fault, so shut up and pay the highest taxes for declining services.

The Public Sector Unions can brag about this one for decades to come.

Not mentioned is healthcare costs. Recently a retired teacher I know had her ‘eyes lifted’ vs simply losing weight. They do not hesitate to have surgeries done. The rest of us are forced into Obamacare, which is an abomination.

This reminds me of the public discussions and political proposals for “solutions” to the COVID problem or climate change. Few voters (or legislatures of judges) have the breadth of knowledge or the patience to evaluate what might work — let alone the insight to predict how future developments might bear on outcomes. The Detroit bankruptcy ruling (2013) required approval by a large percentage of active & retired employees. To get the approval, the “expert guardians” of the public interest manipulated mortality assumptions to make the pension haircuts low enough to secure that approval. Now Detroit is looking at more kicks… Read more »