By: Ted Dabrowski and John Klingner

Illinois politicians can’t have it both ways. They can’t claim they pass “balanced budgets” each year and then repeatedly report that Illinoisans are on the hook for ever-higher levels of debt. A balanced budget, by definition, shouldn’t burden Illinoisans with more debt if the state doesn’t spend more than it takes in.

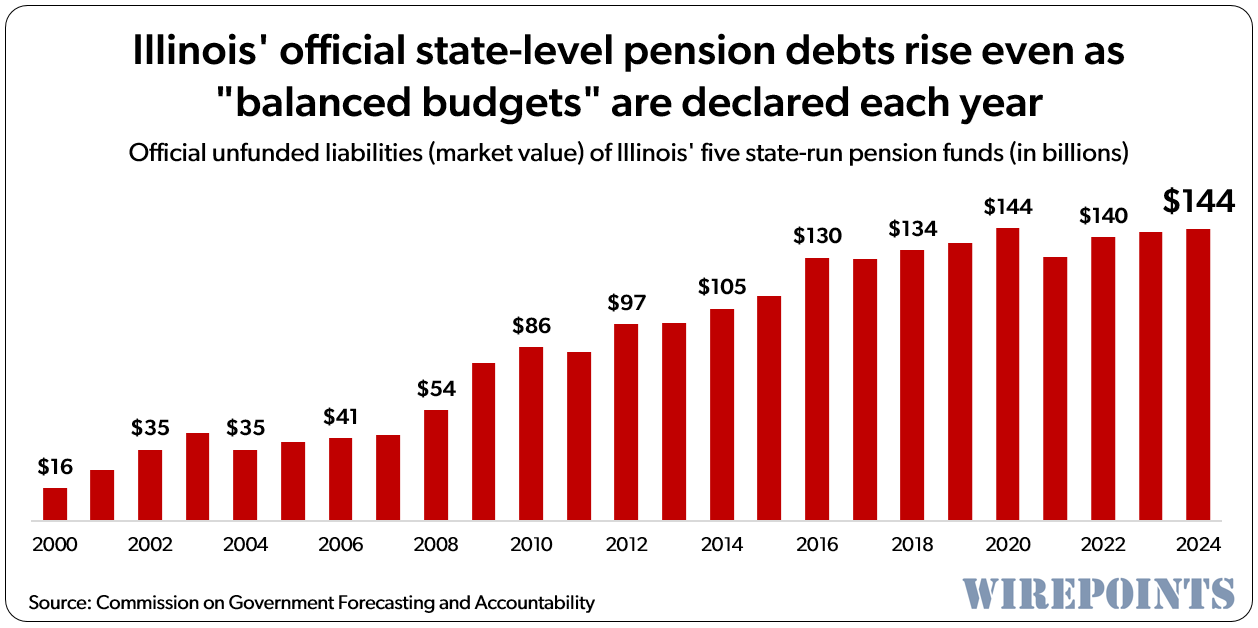

But this is Illinois, and for more than two decades continuous “balanced budget” claims have been accompanied by a meteoric rise in the pension debts of the five state-run funds – for downstate teachers, university employees, state workers, judges and lawmakers.

Those debts have jumped to $144 billion today from just $16 billion in 2000, according to the pension report just released by COGFA, the legislature’s financial arm. That increase has transpired despite the state’s constitutional requirement that says “Appropriations for a fiscal year shall not exceed funds estimated by the General Assembly to be available during that year.”

Lawmakers have gotten away with their “balanced budget” claims by making the statutory pension payments that they themselves set. By definition, lawmakers pay “what’s required” each year.

But those payments have consistently been artificially low, based on rosy assumptions far different than what more market-based actuarial standards call for. By ignoring those standards, lawmakers have been effectively underpaying for at least three decades – and racking up debt over that time.

This financial sleight of hand, perpetuated by Illinois’ political class and largely ignored by the media, has made a mockery of taxpayers. In 2000, Illinois households were on the hook for, on average, about $3,500 in pension debts. Now, that amount totals nearly $30,000 per household. And that’s only for the shortfalls in the five state-run pension funds. There are billions more in shortfalls in the municipal pension funds of Chicago and cities across the state.

Still more debt to reveal

The state still isn’t done revealing the full extent of its pension debts, according to major financial institutions like Fitch Ratings.

Fitch uses more realistic market-return assumptions (6%) than Illinois does (6.5% to 7%), putting the agency’s total shortfall calculation for Illinois at $172 billion for 2023, far higher than the $142 billion Illinois officials report. That’s $30 billion that, for now, goes unreported by the state.

And it’s not just the debt itself. As the Fitch data shows, Illinois is the nation’s extreme outlier when it comes to overall state pension debt. That makes it non-competitive compared to every other state in the nation, especially its neighbors.

****************

So that’s how it works. Politicians hide the truth with “balanced budgets.” But pension debts keep going up. Taxes keep going up. And Illinoisans pay the price.

The only way to halt this mess is to boot the politicians that refuse to support a constitutional amendment for pension reform.

(For more on why those debts keep growing, see Illinois state pensions: Overpromised, not underfunded – Wirepoints Special Report.)

Read more from Wirepoints:

- Chicago’s black hole: Pension debts jump even though taxpayers pour billions into city funds

- This one graphic explains why Illinois is such a financial mess

- Illinois government’s $100K salary and pension club: 140,000 members and rising

- Look for Chicago’s pension mess to become worse. That’s a bad sign for taxpayers

- Illinois state pensions: Overpromised, not underfunded – Wirepoints Special Report

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

And Illinois keeps shorting the systems compounding the problem and trying to steal earned pensions. Pensions are like education loans: pay up!

Upset about pension payments getting shorted? Talk to the public employee unions about the need for them to forego raises so pension payments can be made. I’m sure they will be happy to sacrifice on your behalf. They are your union brothers, right?

If you are on Social Security how about you and others that would like retired public system workers to forgo raises etc, do the same thing. Give up your SS increase or take a cut to save Social Security. That sounds like a real plan.

When Tier 1 public pensioners agree to cut back their benefits to SS levels, and pay back all of the tax dollars they got as “pension pickups” so they contributed almost nothing to their cushy retirement, I would say that your “plan” should be considered. Until then, you are trying to create equivalence between apples and gorillas.

Put the Ripple bottle down sport. Didn’t pay into the pension funds, wrong as usual, but then again I suspect the Ripple effect has been going on for years.

Completely agree Pensioner. The state doesn’t pay their bills on time and low life scum wants to blame the workers. Good news may be on the horizon with the Social Security Fairness act. Many of us will see increased social security on top of our pensions. A nice little bonus for all of the aggravation we put up with concerning the attempted theft of our money. I’m looking at a $1300 monthly increase. They try to steal from us and we end with even more. Love it.

January 6th may be the day SS fairness is signed into law

Signing it soon but they are making it retroactive to December 2023. Some nice lump sum retroactive payments for people that have been cheated for far too long.

I have paid into SS for over 60yrs from multiple part time jobs. I worked in the public sector and 9.75% of my gross pay was sent to the pension plan for 33 yrs. We did not pay SS from the public sector job. My accumulated SS benefit would have been around $550.00 based on my SS payments. I get $200.00 a month after getting hit with the WEP/GPO penalty. I pay for Medicare and get a monthly check for $44.00. Where is the rest of my earned benefit of $550.00 going?I only want what is due to me, nothing… Read more »

The real kick in the balls is knowing that a great many who receive an Illinois funded pension are spending it other states.

Why be concerned about pension debt, or any debt, if the elected officials aren’t? IL’s motto is ‘What, me worry?’

Here’s a great idea. Devolve the total debt to a per household debt. Then enact a law that creates a mortgage for that amount in every property in Illinois. When the homeowner goes to sell, they have to pay the debt. Of course, that additional lien will probably result in many first mortgages being called and probably several foreclosures and bankruptcies, but who cares? The important people (You know the public “employees”) will get theirs. Who cares what happens to your house? The slaves inhabiting Illinois will love it because it is making their masters more secure. Just shut up… Read more »

In 2018 three economists from the Chicago Fed proposed that all property owners pay an additional 1 percent tax per year to go towards pensions. The authors reasoned that there was no other reasonable way to draw down the debt. And given who the voters elect, they argued the burden should fall on property owners who decided to stay in Illinois. My reaction to these economics experts was odd. I didn’t take their proposal seriously as property taxes are already high in Illinois (see the reaction to raising them in Chicago) but rather I thought their piece illuminated the huge… Read more »

Great work as usual. A real resource for us Illinois peasants. Suggestion. You should caveat all these posts by noting that they are estimates that vary by source. Also, remind your audience that pension debt can’t be looked at alone. We MUST also consider pension debt, unfunded healthcare liabilities, the elephant in the room, and payables. Keep it up. Comparing all of the above at the state level vs the local level is also quite informative.

It is so bad it will never get paid off. It is like a “Forever bond”. Get use to paying higher taxes for less services for generations.

Ted- One question, what is the assumed return on investments to reach that number? I am guessing it is too high compared to reality and the debt is actually worse.

Larry, Fitch used 6% to get to its $172 B for 2023. Illinois uses 7%, 6.75% and 6.5% discount rates for the teacher, state worker and university employer plans, respectively. State calculates $142 billion for 2023. That’s a $30 B gap.

You can use AI to feed in the data for Present Value and it will give you the answer.

The arrogant and abrasive cheerleaders for public unions believe they are fighting a political battle. They will find that they have been at war with the undefeated champion: reality. There won’t be much sympathy for them at their inevitable defeat.