By: Ted Dabrowski and John Klingner

COGFA, Illinois’ official number-crunching group, is out with its state pension reports for both FY 2022 and 2023 and its analysis shows that while record-high inflation has reduced the stress of pension costs on the budget in the short-term, those retirement debts continue to be a major threat to the state’s fiscal and economic stability.

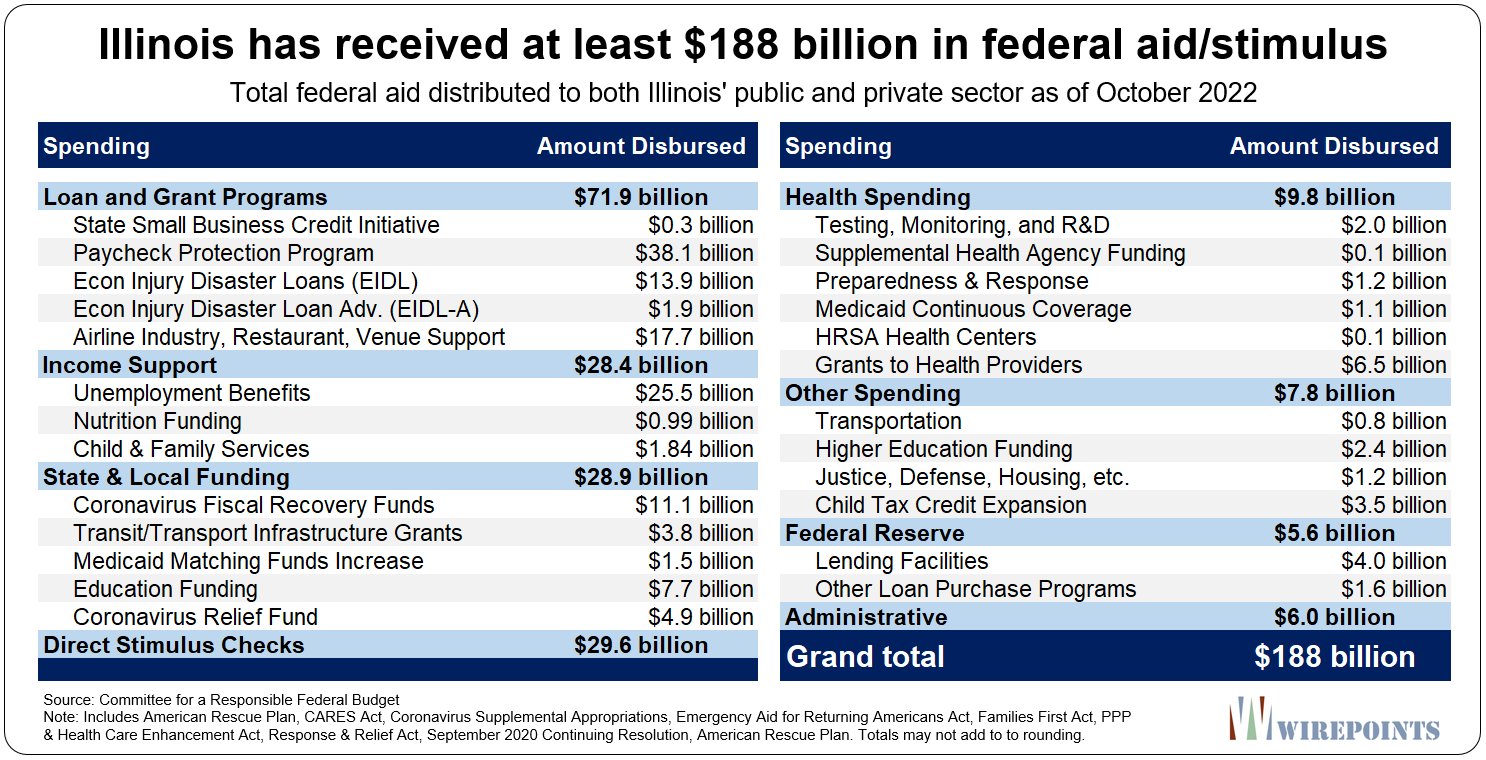

Inflation has ballooned Illinois’ state budget to over $50 billion in recent years, and that’s helped drop pension costs as a percentage of the budget to “just” 20 percent in 2023, compared to 25 percent in pre-pandemic-2019. That’s largely the result of the federal government’s trillions in covid spending, including the near-$200 billion sent to Illinois (see appendix).

But even with the “help” of inflation – which simultaneously crushed the finances of households across the state – Illinois’ pension debts continue to grow and funded ratios remain dangerously low.

Inflation is also a double-edged sword. Budget pressure has been partially deflated for now, but pension costs will rise as politicians continue to meet government workers’ demands for bigger pay hikes and more benefits. In fact, that’s already happening.

Here are a few key takeaways from the COGFA reports:

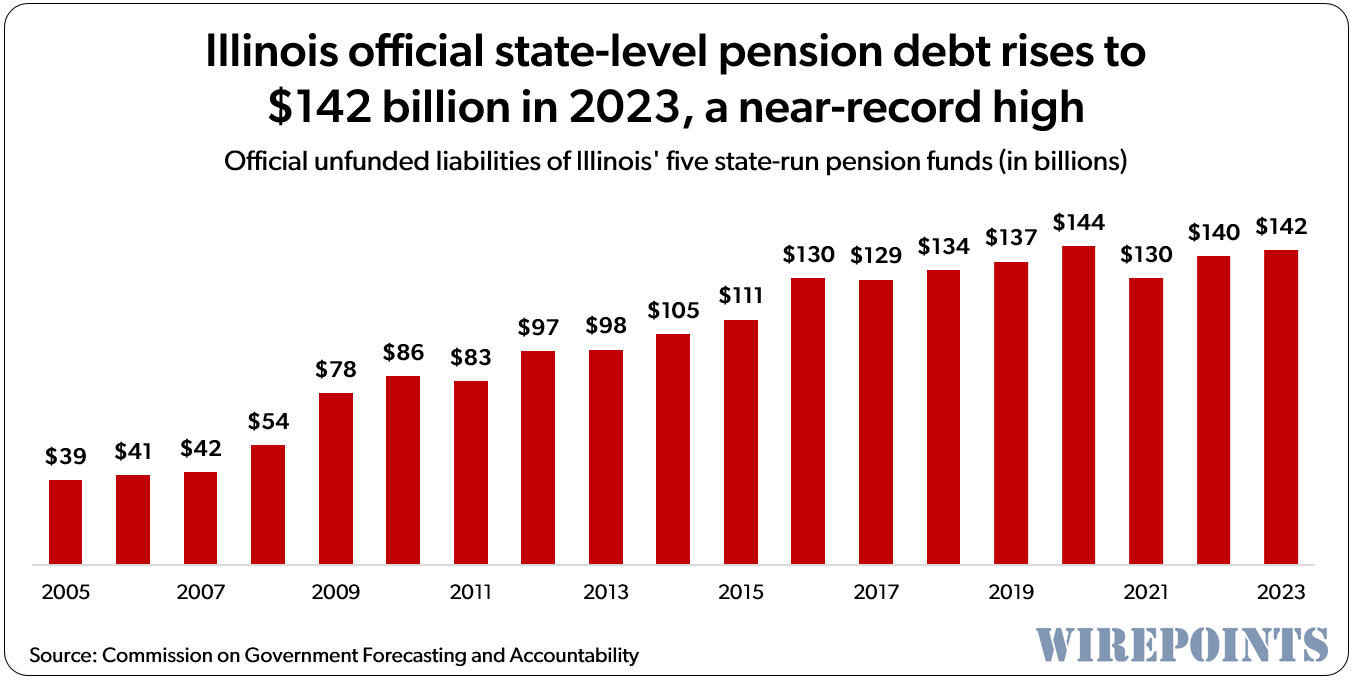

1. Illinois pension debts hit $142 billion – 2nd-highest shortfall ever. This is the 2nd year in a row the state’s shortfalls have grown since 2021’s once-in-a-generation stock market rally helped shrink unfunded liabilities to $130 billion.

2022’s subsequent dismal investment returns pushed debts back up to $140 billion. And now 2023’s lackluster returns have helped increase shortfalls yet again.

That $142 billion is just one part of the total $207 billion Illinoisans are burdened with in official state and local pension debts. That’s $40,000 per household, which we wrote about recently.

That $142 billion is just one part of the total $207 billion Illinoisans are burdened with in official state and local pension debts. That’s $40,000 per household, which we wrote about recently.

2. Illinois’ pension funds continue to have less than half of what funds they need. Illinoisans are on the hook for $142 billion in unfunded state pension debts. That shortfall exists because the five pension funds should have $257 billion in their investment accounts today to ensure they can pay out their future pension obligations. Yet they have only $114 billion in the bank, hence the shortfall. That leaves the state’s overall unfunded ratio at 44.6 percent, the worst in the country.

It’s important to point out that the billions in windfall tax revenues as a result of the covid bailouts did little to get Illinois out of its pension hole. The funded ratio only improved by 4.3 percentage points, up from 40.3 percent in 2019. Those federal funds have now largely dried up.

It’s important to point out that the billions in windfall tax revenues as a result of the covid bailouts did little to get Illinois out of its pension hole. The funded ratio only improved by 4.3 percentage points, up from 40.3 percent in 2019. Those federal funds have now largely dried up.

3. Illinois politicians are set to short pensions even more than last year. Last year, COGFA began publishing the difference between what the state should be paying into the pension funds (Actuarially Determined Contribution) and what the state is actually contributing – something we’d wanted them to do for years.

The state’s statutory requirements for pensions (decided on by lawmakers) require a payment in FY 2025 of $11.3 billion, but the pensions’ actuaries calculate Illinois should be paying $16.1 billion.

That’s a funding shortfall of $4.8 billion, even bigger than last year’s $4.4 billion gap.

Add in the annual underpayment of retiree health insurance costs – in the past it’s been $1 to $3 billion – and the state’s total underpayment of retirement costs is more than $5 billion, or about 10 percent of Illinois’ general fund budget. Keep that in mind when Illinois lawmakers claim yet again they’ve passed a balanced budget.

Add in the annual underpayment of retiree health insurance costs – in the past it’s been $1 to $3 billion – and the state’s total underpayment of retirement costs is more than $5 billion, or about 10 percent of Illinois’ general fund budget. Keep that in mind when Illinois lawmakers claim yet again they’ve passed a balanced budget.

4. Salary hikes boosted unfunded liabilities by more than $1 billion. As mentioned above, inflation cuts both ways regarding Illinois’ pension crisis. Yes, the state’s debt is inflated away, but costs will also grow as government unions demand pay hikes to catch up with all that inflation.

2023 was a record year for the impact of salaries on the pension funds, as contracts got renegotiated and workers got pay hikes far larger than actuary estimates. Oversized raises were responsible for over $1 billion of the state’s $2.6 billion increase in the unfunded liability. That’s the single largest negative impact raises have had on pension debts since at least 1996.

Expect big raises to continue as more teacher and other government contracts are renegotiated in the next couple of years.

Worst is still worst

Worst is still worst

Count on many Illinois officials to point to the latest pension data and say things are better. In the state’s FY 2019 report, pension costs were projected to remain at 27 percent of the budget through 2045. Now, costs are projected to fall to 17 percent over time. That’s not a drop to ignore.

But there are four things to keep in mind:

But there are four things to keep in mind:

- Illinois politicians have done nothing in the last decade to reduce the burden on taxpayers or improve retirement security for pensioners. Any improvement has come strictly from the windfall tax revenues as a result of covid aid.

- At 20 percent, Illinois will still contribute more of its budget to pensions than any other state. Illinois will remain uncompetitive for decades.

- The state’s pension projections are based on rosy assumptions that may never be met. That means debts – and costs – are likely to grow in the future.

- Some of the savings from Tier 2 are already being unwound and there’s increasing pressure to boost benefits for Tier 2 workers. Any real increase could boost pension debts significantly.

The simple reality is state lawmakers have done nothing to solve the nation’s worst pension crisis. Until they do, it will remain the worst.

Read more from Wirepoints:

- Illinoisans burdened with $207 billion in official state & local pension debts, $41,000 per household

- Changed assumptions knock $25.1 billion off Illinois’ unfunded healthcare liability

- Johnson’s next headache. Chicago’s pension funds are running out of money

Appendix.

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

As PPF noted many times, there are many areas where IL can increase taxes (and fees, I would add) or create new ones to help fund pensions. As I noted, people have their thresholds of pain. For some, their threshold of pain may be IL taxing retirement income. For others, it may be a PT of three percent of their property values. When they exceed their thresholds of pain, one obvious way to significantly reduce or even eliminate the pain would be to relocate out of state. If IL continues to mismanage taxpayer funding on a greater scale, expect higher… Read more »

When the Fed lowers interest rates the discounted value of the pension liabilities willl increase, leaves the pensions even more underfunded.

Pension funding levels are not determined by current interest rates. The pension funds use a fixed rate of expected return (currently 7%) and it’s not tied to interest rate fluctuations. This rate is determined by a conservative expected rate of return. I say conservative because over the last 40 years, TRS has averaged over 9% during that time period.

If the fund managers believe they won’t be able to get the expected rate of return they can adjust the rate but it’s not tied just to interest rates.

I do believe that therein lies a part of the problem as well namely the TRS system. I don’t know why, and may soon become educated as to why, the TRS simply doesn’t invest in indexed funds with annual rebalances. John Vogle had plenty of data to show that fund managers do not outperform the indexes after taking into account expenses related to these managers. I cant even imagine that Illinois managers can outperform the private sector professional managers Bogle was referring to. Low cost funds, per Vogles research, and eliminate all of the TRS investor overhead, brokerage fees and… Read more »

Take a look at the last sentence in the third paragraph. Multiply that figure by 10 and see how much is spent on fees every decade.

https://www.civicfed.org/iifs/blog/study-examines-public-pension-investment-costs

Wrong, PPF. Interest rates most certainly do have a place in how the funds set their rate.https://www.ncpers.org/blog_home.asp?display=206

How am I wrong Mark? “but it’s not tied just to interest rates” Completely factual. The expected rate of return is not tied JUST to interest rates. “Pension funding levels are not determined by current interest rates” Completely factual. As I’ve noted they are tied to expected rate of return but they don’t fluctuate up or down every time interest rates move. Ok Mark. So interest rates have risen drastically. How much has the assumed rate of return for TRS pensions changed? If they didn’t change when they went up why would they change as they come down. It’s not… Read more »

OK fine. It’s not just interest rates. I had wrongly focused just on your first line.

Is this rate of return before or after expenses?

actual returns contain a statement of whether they are before or after expenses, expected returns are hardly ever adjusted, so before or after expenses are probably not addressed by pension boards. The new statewide boards may mention it.

Not talking about expected returns, rather the calculation of the present value of the liabilities.

Mr. Palermo, seems like only yesterday when we were sounding the alarm about Forest Park pensions.

https://www.forestparkreview.com/2014/09/09/police-and-fire-pension-funds-report-00000-shortfall/

According to this article if correct life expectancy is now lower due to Covid deaths especially for men. So long term liabilities should be lower overall. I have seen many recently who have died in their 60’s and early 70’s. We still don’t know how factual the deaths from the vaccine are but based on insurance payouts death rates seem to be somewhat higher from a variety of reasons. Are these articles true? Who knows. https://insurancenewsnet.com/innarticle/covid-19-mortality-spike-hits-insurers

https://www.statnews.com/2023/11/13/life-expectancy-men-women/

Mortality tables are adjusted infrequently an only in the last 10 years or so have Illinois municipalities moved away from the 1971 tables.

And yet it seems like decades ago…

Very Unlikely that the Federal Government will bail out Illinois pensions. The Federal Government is just a broke.

And SS and Medicare are just as bad off. Something that needs to be pointed out. But far less attention is devoted to that concern and I am not certain why. SS will go bust in a dozen years- probably faster than our state pension systems. And Medicare is draining vast amounts of general revenue funds that was never intended as it was supposed to be self financing.

Social Security will see benefits reduced if there are no changes made, but it won’t go bust. Medicare will also need to see changes. Ultimately there will be additional means testing, tax increases and premium increases. If Biden doesn’t close the door all of it gets worse.

You are correct and that is basically my point. All pension systems State or Federal are in bad shape and SS may have more unfunded liability than do our bad State pension systems.

Pretty obvious the members of TRS, SERS, SURS, JRS, and GARS should be contributing more to cover their plans shortfall. If they won’t do that, then what is the point of all this – its not a pension plan but state welfare.

It’s not “their plans shortfall” but rather it’s the states plan that is shorted. No need for members to pay any more as it’s the responsibility of all the taxpayers. “The United States Supreme Court has made clear that the United States Constitution “bar[s] Government from forcing some people alone to bear public burdens which, in all fairness and justice, should be borne by the public as a whole [citations].” (Internal quotation marks omitted.) United States v. Winstar Corp., 518 U.S. 839, 883 (1996). Through Public Act 98-599, however, the General Assembly addressed the financial challenges facing our State by doing just that. It made… Read more »

Wouldn’t is be easier if instead of the state being the strong armed collection agency for pensioners that you and others send out bills to your neighbors for your pension? You can send a $1,000.00 bill to 135 neighbors or so or whatever your pension is and send a note saying that this is their obligation as it is written in the constitution for the unfunded part. Of course they are only obligated to pay the unfunded part so they would need to find a good CPA and contact the pension fund managers. I wonder if anyone will pay? The… Read more »

Sounds like a lot of work and it’s not my responsibility. No thanks. I’ll let Illinois government handle collection of their taxes. They have a whole department for that and have the backing of the law to ensure collection takes place.

I’ll tell you what though. I’m feeling generous so this is what I’ll do. I’ll make sure my bank collects the direct deposit along with ensuring a 3% increase is attached each and every January. Don’t worry, I’ll double check to make sure that increase is compounded. No simple interest for me. Hey, I’m doing my part.

As least I tried but seriously have you tried to contact the fund managers to ask them to get a better return on investments? Getting 15% or so in returns in this market is not that difficult. 5% in money markets is easy and it would mean a 2% profit on the 3% compounding alone. There is more than enough money to pay current liabilities so I am not concerned about the long term. None of us are guaranteed tomorrow so make the most of it today. Enjoy what you have for it can be taken away with a diagnose… Read more »

Back to the Marie Antoinette act, I see. Worked out well for her.

Pensions will be paid first before you will receive any cake.

Our country club towards the end of the year sends out a surcharge if the fund balance isn’t what they thought it should be. Members pay the gap. Don’t see any difference here – you are part of a closed fund, and as a member need to support it properly.

In your example of your country club, public pensioners were the employees of the club. You hired them to do the work and you owe them more money based on deferred compensation. You don’t collect a surcharge from the people that performed the service but rather the members of the country club. In this case that would be the Illinois taxpayers. So go ahead and send out that bill at the end of the year but it’s ALL the taxpayers that are getting the bill not the people that are owed the money. The courts have been clear. The responsibility… Read more »

The people who have a claim need to support their pension. Taxpayers have no claim. The members need to pay their fair share, and then some more if that’s not enough.

Nope. Pensioners have paid their contractually required amount. Anything additional is all on the entire tax base. It has already been decided by the IL Supreme Court. “The United States Supreme Court has made clear that the United States Constitution “bar[s] Government from forcing some people alone to bear public burdens which, in all fairness and justice, should be borne by the public as a whole [citations].” (Internal quotation marks omitted.) United States v. Winstar Corp., 518 U.S. 839, 883 (1996). Through Public Act 98-599, however, the General Assembly addressed the financial challenges facing our State by doing just that. It made no effort to… Read more »

This public pension is a big conflict of interest…how do we get this pension case moved to a higher court…class action suite against the state and city…these public pension millionaires are laughing at the middle class…don’t give up battle.

A class action lawsuit for following the constitution of Illinois? A clause in the constitution that the people of Illinois voted on? Paying people according to a contract provided by the state? You’re adorable.

Contracts are made to be broken…it’s an amendment.

That’s what they said the last time the state tried to steal from pensioners. The IL Supreme Court smacked it down then as well. “In addition, because the state’s self-interest is at stake whenever it seeks to modify its own financial obligations, the United States Supreme Court has made clear that it is not appropriate to give the state’s legislature the same deference it would otherwise be afforded with regard to whether the impairment is reasonable and necessary to serve an important public purpose. “A governmental entity can always find a use for extra money,” the Court observed, “especially when taxes do not have… Read more »

Canary in the coal mine:

California faces record $68 billion budget deficit, nonpartisan legislative analyst says

https://finance.yahoo.com/news/californias-nonpartisan-legislative-analyst-says-173316625.html

Saw that. More taxes and/or less services. Let me know what they choose.

Most of these union jobs can be replaced with replacement workers from over the border and non-union personnel. The unions will run themselves out of a job they claim to protect. While Illinois has the perfect scheme to continue the charade, the financials show it is unsustainable. So based on the math, it will be easier for larger employers to move and cease operations in Illinois and move to a neighboring state if location is a factor. The public sector pensions are bleeding because not enough new pensioners are being hired in lieu of payments to existing retirees who are… Read more »

“Illinoisans burdened with $207 billion in official state and local pension debts, $41 000 per household” What a joke. It’s unrealistic and means nothing. How does this household then afford to purchase and maintain an EV and replace gas appliances by the deadlines, support immigrants, buy groceries, fund daycare, feed and clothe their family and pay for medical care? They can’t live as well as those collecting pensions because they have to pay them. There is NO WAY to tax the plan into solvency. That much money doesn’t exist in Illinois. Even if you took everybody’s everything evergrowing pensions still… Read more »

Don’t worry it’s not all due at once. We will put the taxpayers on a payment plan with a 7% interest rate. Just like the student loan people that complain about their debt, perhaps you should cut back on all the Starbucks and avocado toast.

Plenty of money for pensions just not all the other discretionary spending. If not, raise taxes.

Plenty of money for pensions? But, but but…what about money for the immigrants…

“ We will “ ..”Cut back on..” You pension pigs are arrogant beyond belief.

Is it arrogant when a vendor expects payment from the state of Illinois for services rendered? How about when you cash a tax refund check from the state? No. It’s just people expecting to be paid what they are rightfully owed.

It is arrogant when liberal hacks go against the intent of “Not to be impaired or diminshed” and then add a COLA. Not to be impaired or diminshed’s intent was that no one’s pension will be reduced. So not only have mental disordered liberals twisted that they also added to it with COLAs.

“Not to be impaired or diminshed’s intent was that no one’s pension will be reduced.” You have no idea what you are talking about. During the 1970 constitutional convention, the amendment was established to ensure that a new employee would receive at least what was promised on their first day of employment. If a better formula was offered at a later date then you could not reduce the pensioner to a less favorable formula. The 3% annuity increase (it’s not tied to COLA) is part of that guarantee. It’s the formula that can’t be altered. For a guy that claims… Read more »

Also, keep in mind that amendment was sponsored by Republicans, passed with bipartisan support and voted on by the people of Illinois.

Government workers are wired differently than private sector workers. That’s why they are so sensitive in these discussions because they are butthurt if you take their pension away when all they may have had was a high school diploma or political juice to get the job anyway. It’s a tough way to live and that’s why so many less people work in steel mills, mines, auto assembly, it takes many less people than it used to. Public sector unions for people who push paper? Most ridiculous thing I have ever heard. There is a place for organized labor but it’s… Read more »

The voters of Illinois disagree with that sentiment as they have enshrined the right to join a union and collectively bargain within the state constitution. Your opinion was noted last November and dismissed by the rest of the state.

I knew I’d hear from Pensions Paid First and he would disagree with me. Sorry you are still raping the middle class. If your problem is with how the government spent your money, then go after them and leave us alone.

Pension pigs don’t care. As in the movie “ Goodfellas “ — you! Pay me!

No different than bondholders or vendors. People expect to get paid what they are owed.

You’re still not understanding the issue. It’s not pensioners responsibility to figure out how they will be paid. It’s up to the voters of the state. If YOU have a problem with how the government spent your money, then go after them and leave pensioners alone. Pensions will be paid by all Illinois taxpayers.

How much are you going to contribute to my retirement? Many of us agree you should contribute. So you say making sure the money is there for you to collect is not your responsibility it’s mine. Are you delusional? As I said a long time ago, the plan will never be solvent, your money, my money, tax dollars, whatever, there is nothing that can fix this. Not even your annual increase will save you.

Why would I contribute to your retirement? I offered you no such deal for the work you performed. Unlike the state who forced employees to join these pensions and guaranteed that they will be paid.

Your union forced you to join these pensions and guarantee that they will be paid.

Take the non tax payers out of the equation…we have no idea how much we are on the hook for…interest on this debt is close to a billion dollar…Why is this our problem!

Because it is the same as any other debt or bond. In the case of the pensions, the courts have already ruled, ca 1975 or so, that the obligation is to pay the deferred amount of compensation (i.e. the pension), and how/whether the state does or does not prepare to meet that anticipated deferred compensation in a responsible way was not relevant to the court. Now, it is prudent to fund a pension plan ahead of time to meet that anticipated future obligation; otherwise, the state would have to (partially) adopt a “pay as you go” plan, which is to… Read more »

You are one of the rare adults here. Bravo!

Heron, here at Wirepoints we’ve always agreed that GO bondholders and all other unsecured creditor should, ideally, suffer proportionately with any cuts to pensions. They’ve assumed risk. https://wirepoints.org/got-a-problem-with-hedge-fund-trying-to-profit-by-invalidating-certain-illinois-bonds/.

Very importantly, it should be noted, however, that bondholders just aren’t that big a part of the picture. Something like $35 billion of state bonds are outstanding compared to $142 billion in pension debt, and some of those bonds are secured and therefore have priority by law. Other unsecured debt is trivial. So, making them share in the losses would not help pensioners that much,

Pensions are secured by the state of Illinois and have priority based on both state and US constitution.

The language of the amendment you’ve offered doesn’t try to take away contractual rights of bondholders but rather it’s specifically targeted at pensions only.

On your first point, no, I meant “secured” in the legal way that distinguishes unsecured from secured debt. Secured debt is protected by a mortgage or lien of some kind and is far more difficult to cut even in bankruptcy. Only the funded portion of pension debt is secured in that way. Some bonds are secured that way and some are not. On your second point, it’s true that the pension amendment we proposed would not address bonds. That would be impossibly complex and not make a big difference for the reason we said. And keep in mind that’s one… Read more »

“That would be impossibly complex and not make a big difference for the reason we said.” So changing the language of the constitution that would allow you to steal from bondholders would be too complicated but stealing from retirees who worked a job is perfectly fine? That’s funny. No, the reason you wouldn’t suggest it is because it would be laughed at on its face. Who would lend the state money if you put in the constitution that the state reserves the right to change the terms of the contract as it sees fit? If you can’t justify stealing from… Read more »

Retrospective cuts to already issued bondholders would help future bond sales and lower rates. And as I said, which you ignore, the ideal solution would do just that.

The ideal solution would be to fund the pensions with actuarial payments each and every year. You seem to ignore the right thing to do is pay your bills and not steal.

Also, those future bondholders wouldn’t be too keen buying bonds from Illinois if the state reserved the right to adjust how much they owe so they can spend that savings elsewhere or reduce taxes.

The above data does an exceptional job of defining the challenge. Two points that interest me. How much of the Federal aid remains unspent? I believe there is still a fair amount of money to be wasted which can be used to mask the dire financial position many public entities face. Second, while inflation has helped state coffers to an extent, what will a recession of any magnitude do to damage the state revenue stream? Economists continue to talk of a soft landing, but that remains to be seen.

Never a good sign when retirees outnumber active participants in your underfunded pension system. SERS hit that milestone last year and it’s only gotten worse.

State Employees’ Retirement System:

Active members = 61,056

Total Retirees = 63,319

That comparison is meaningless if the pensions were 100% funded. That’s the real issue.

Comments like this show little you really understand the pension system, and disregard basic math, in favor of the ignorance of 7 politically connected Judges in Springfield all of whom voted in their own self-interest.

The ratio is meaningless. I could lay off half of those employees and start outsourcing the work to private contractors that don’t pay pensions. The ratio of active members to retirees would look even worse but the state could also be on better financial footing. I could also hire 2500 more employees and make the ratio look better but it would cost the state more money.

Do you understand now? That comparison is meaningless as it doesn’t relate to the states ability to pay. Also, pensioners aren’t backed by current employees but ALL Illinois taxpayers. Again, meaningless.

I believe Amendment 1 slammed the door on any hope taxpayer/voter could or would have of outsourcing gov services to private sec or consolidating the 7,000 units of gov

Wrong.

If you have a problem with how the government funded and spent your pensions cotributions, take it up with them and leave the taxpayers alone.

Did you fund you entire pension plan 100%

Pension members have funded their contractual portion at 100%. The state has not.

The amount in the pension fund is irrelevant. Pension benefits are guaranteed by the state not the pension funds themselves. You really seem lost on this issue and it has been covered extensively.

If the amount in the pension fund is irrelevant, why are you going nuts? Not my fault the government spent your pension cash on other things. You reject what they spent it on, right? I reject what they spend most of our money on most of the time. Seems like the government “rolled over” you guys and you think all of us who are not you should be punished.

I’m not going nuts. I’m pointing out that it will cost more if we delay funding. You’re the one that complaining about the cost of an EV, daycare, replacing appliances, buying groceries and supporting migrants. Your opening statement was one long rant. I’m trying to help taxpayers save money in the long run.

Fund pensions or don’t. That’s up to the voters. Either way pensions will be paid.

Write a check…0 balance in your account…game over.

The state collects over 50 billion per year. Plenty to write a check for pension payments and other debt. Not so much for other wants. Game over for those other services or more taxes.

Nothing will change until public pension payout checks start to bounce. Hopefully that happens soon.

Sure if you want your taxes to massively increase to cover the pension payments out of the general fund. They will be paid first and what’s left can be spent on other services. Check out Harvey Illinois if you doubt me. Massive layoffs of police and firefighters while the pension intercept law takes the money from the state first.

Pay more now or pay even more later. Voters choice.

Hypothetically, let’s say it happens as you suggest, when Illinois loses all of it’s services because it has to pay your pensions, what state will they be sending your check to? Oh well, as long as you get yours. You must honestly believe you’re the only person who has been screwed by Illinois.

Pensioners haven’t been screwed one bit. They have consistently been paid and the state guarantees their benefits. The state has vast ability to raise revenue through taxes and if they don’t have enough money they are free to increase taxes.

You continue to act as if this is a problem for pensioners when you refuse to understand that it is the responsibility of the taxpayers as a whole.

And when the taxpayer is tapped out, what then?

They are far from tapping out. Plenty of taxes remain. Plenty of areas to cut spending.

I predict the state will issue IOU’s first. An IOU’s is full compliance.

Last time the state did that with vendors they also paid the vendors a 12% return or 1% per month for the late payment. As I state, pay more now or pay even more later.

One vendor I know waited 3 years to be paid. So, there you have it.

I’m good with a 12% rate of return. Unfortunately that sweet deal will only be for vendors as pensioners will be paid first.

Hopefully all the working class pensioners are as well off as you and can wait a long time. My Vendor friend nearly went out of business. The State was unconcerned.

I would hope that someone doesn’t retire without at least 3 years of expenses in reserves. You’re right that many won’t. Probably why the courts will demand that pensions are paid first. Go back to the Rauner budget stand off and take note how the courts required that state employees were paid while vendors waited.

Your concern for pensioners is noted but they will be just fine despite your prediction.

I sense a recurring theme in your posts – anger and intolerance. You need to work on that.

You think?

I’m not angry at all. I’m trying to get people who claim they are for responsible government spending to understand that this problem will not go away on its own. Pay more now or pay even more later. It’s up to the voters how much they want to pay.

How about going back to the Edgar Ramp? Why did Union members allow that to happen?

They had no choice. The courts had already ruled that pensioners only had a right to their check when it’s due and not any right to any set level of funding.

The underfunding is the result of Illinois leadership. Leadership that was elected by the voters of Illinois. Why did the VOTERS allow that to happen?

So you didn’t vote for Edgar and the Unions had no choice, they couldn’t stop him. I have been in Illinois for decades and more often than not, the Democrat union gets what the Democrat union wants. So you screwed up on the Edgar Ramp?

Edgar was a Republican. I don’t remember if he had union support. Did you vote for him? Does it matter? The majority of voters did and he kicked the can down the road and cost all taxpayers more money. It doesn’t matter who voted for him because the state is still ultimately responsible.

I had nothing to do with the ramp so I didn’t screw up any more than you did.

Former GOP Gov. Edgar says he’ll vote for Biden Former GOP Gov. Jim Edgar said Monday that he is voting for Democrat Joe Biden for president this year. “The biggest thing … was the issue of character,” Edgar said in an interview. “I just think Joe Biden is a very decent person.” And he said that while he thought GOP President Donald Trump “might grow into the job” after the 2016 campaign, “I don’t think he’s done that.” “I have been very disappointed,” Edgar said. “We’ve had chaos for four years we didn’t need to have. I mean, there’s always… Read more »

Of course you’re good with a 12% rate of return! Says alot that you admit it. You obviously don’t care what it costs as long as you get what you want. Even if vendors get it, it’s because you didn’t do anything to stop the outrageous spending.

I support candidates that want to reduce spending where allowable. Cutting pensions isn’t allowable. Why didn’t YOU do anything to stop the outrageous spending? It’s not my responsibility any more than it is yours.

Or, don’t pay at all. It’s your money, you figure it out

You could try that Marie but the courts will merely step in and force payment. Don’t think they can’t as they certainly had no problem mandating spending during the Rauner budget stand off.

Why do you care how it’s done as long as the rest of us support you?

I care because the longer we wait to actuarially fund the pensions the more it will cost all the taxpayers. While pensioners will get paid either way it will be even more expensive for taxpayers. If you actually cared about taxpayers in Illinois you would be demanding full actuarial funding. Unfortunately, you and others think this problem won’t impact you and somehow pensioners will get cheated. You may hope for that but that’s not what will happen.

And yet we have comrade Flintstone and other assorted Marxist minions always tooting their horns about this fund has a surplus, that fund has a surplus, etc. The real kicker is Captain Toilet Seat crowing about the upgrade of IL financial rating “ nine times since I took office!”. Nine steps away from the cesspool is still a pretty rotten place to find oneself.

The numbers are so high, it is bound to fail.

PPF say not so. High income earners are fleeing to Texas and Florida in huge numbers. Their replacements are the immigrants from Central America. Low paying jobs at best, have no money to pay the huge taxes needed. The quality of life has been destroyed by the public sector unions for most citizens in Illinois. The courts will sort this out one day in the future.

Best advice for a family is to start all over in another state and enjoy your newfound prosperity.