By: Ted Dabrowski and John Klingner

There’s a graphic that Brandon Johnson’s pension committee should take a good, long hard look at if it really wants to understand the depth of Chicago’s financial crisis. It shows just how little funding the city’s pension funds have to pay out future pensions. Chicago’s pension funds are running out of money.

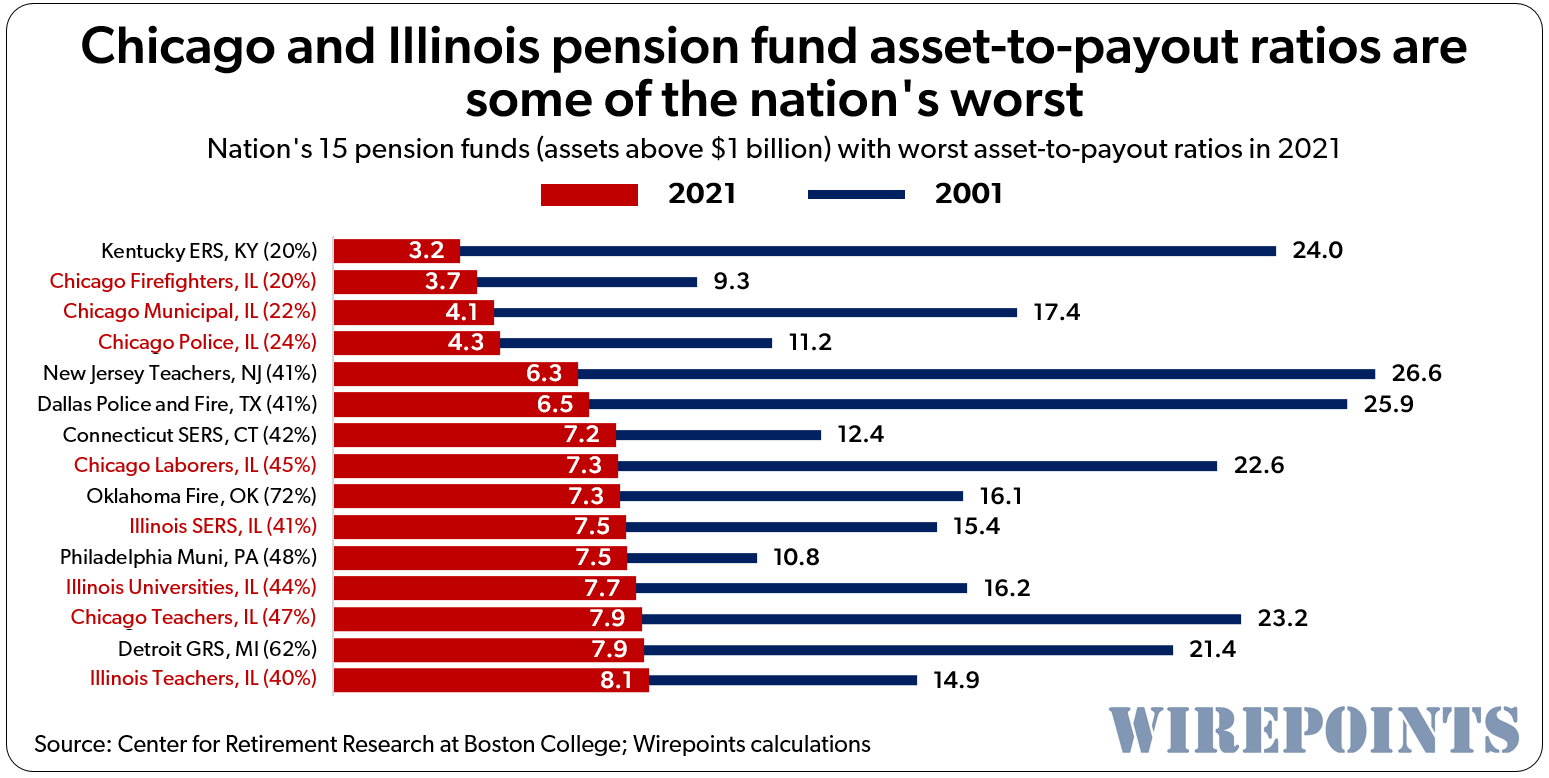

One way of looking at the health of a pension is how long its money will last. Most healthy U.S. pension funds, like Los Angeles’ police and fire fund, have enough assets in their investment accounts to pay their pensioners for the next 20 years or more without taking in any new money during that entire period. It’s a way of looking at how long a fund can last without new money. The longer a fund can make payouts without new money, the better it can survive market crashes and other unexpected crises. Moody’s and other agencies use the asset-to-payout ratio, as it’s called, as one of several key metrics for their credit ratings.

But just look at Chicago’s firefighter pension fund. According to Chicago’s recently released 2022 ACFR, it can only pay out 3.4 years of pension payments before running out of money – again assuming that no new money comes in. That 3.4 asset-to-payout ratio is the second worst for a U.S. municipal pension fund with $1 billion or more in assets.

It’s a similar story for all of Chicago’s pension funds. The city’s police and municipal funds have asset-to-payout ratios of just 3.7 years. And the city’s “best” fund, for teachers, has assets for just 8 years of future pension payouts.

It’s also important to understand what mismanagement has done to the health of the funds over time. Twenty years ago, both Chicago and Illinois’ pension funds had enough assets to make 10 to 15 years of pension payouts. Not good at all, but certainly better than today.

It’s also important to understand what mismanagement has done to the health of the funds over time. Twenty years ago, both Chicago and Illinois’ pension funds had enough assets to make 10 to 15 years of pension payouts. Not good at all, but certainly better than today.

Now their ratios have collapsed and Illinois’ funds dominate the nation’s list of worst pension funds with $1 billion or more in assets. (The data below is based on 2021 numbers since not all 2022 numbers have been fully compiled).

Only Kentucky’s Employee Retirement System was worse off than Chicago’s firefighter, municipal and Chicago pension funds. The Kentucky fund’s asset-to-payout ratio was just 3.2 in 2021, but it used to be 24.0 back in 2001.

You can see how all of Chicago’s funds have collapsed. The Chicago teachers fund 20 years ago used to have assets worth 23 years of payouts and the laborer’s fund was similar, at 22.6.

That’s all history now and new pressures will keep today’s dismal ratios under pressure. Crime and murders, a shrinking population, the potential of a recession and the dangerous risks of a doom loop will stress the city’s finances and what’s left of the pension funds. Not to mention the many dangerous policies that have been communicated by Mayor Johnson before he took office.

That’s all history now and new pressures will keep today’s dismal ratios under pressure. Crime and murders, a shrinking population, the potential of a recession and the dangerous risks of a doom loop will stress the city’s finances and what’s left of the pension funds. Not to mention the many dangerous policies that have been communicated by Mayor Johnson before he took office.

A worsening asset-to-payout ratio isn’t just some technical budget issue. Instead, it represents a massive shortfall in the city’s pension funds that will eventually have to be paid off by taxpayers, assuming enough of them stick around.

Officially reported pension debts of the four city-run funds plus those of the teachers and the park district jumped $3.6 billion last year and now exceed $50 billion. That means each of the city’s one million households will, on average, have to fork over about $50,000 in future taxes to plug the hole for services that have already been rendered.

That $50,000 doesn’t include what Chicagoans owe for their share of Cook County government pension debts and state-level pensioner debts.

That $50,000 doesn’t include what Chicagoans owe for their share of Cook County government pension debts and state-level pensioner debts.

Add it all together and the future tax obligation for the “average” Chicago household starts to approach $100,000.*

Chicago’s pension crisis was on the backburner during covid, but it’s rearing its ugly head again – a fact that the managers of Chicago’s municipal fund themselves admit.

“Given the low funded ratio and the expected timing of employer contributions, the fund is still at risk of potential insolvency if an economic recession or investment market downturn were to occur in the near term,” the municipal fund’s actuarial report warns.”

Everyone in Chicago should be more than alarmed by these debts that go unreformed and grow by the year. The city’s public safety workers are likely to see their pension checks cut. City residents, rich and poor, will flee as this mayor and future ones try to squeeze more taxes out of them. And businesses and job creators won’t have any choice but to downsize or leave as they, too, become targets. It’s a downward spiral that should be stopped in its tracks, but not yet.

One day we’ll finally talk about reforms. But not yet.

*The number is much higher when based off of Moody’s calculations. We’ll update Chicagoans’ true debts when new Moody’s numbers are released.

Read more from Wirepoints:

- Chicago murders: Good news, bad news

- Chicago Weekly Crime Tracker

- Good, recent price news for Chicago area homeowners but gloom over longer term

- Chicago Public Schools doesn’t deserve another penny (Part 2)

- Chicago’s commercial ‘doom-loop’ could result in a property tax hike on homeowners as large as 22%

Appendix.

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

Just let it run out of money. Then let the lawyers and courts sort it out. That is what they are there for.

One bad economic downturn like the mortgage crisis a few years back and some of these pension funds are toast.

Already Happening:

Regarding the sale of LaSalle Plaza, in Minneapolis – “A source close to the deal said the building sold for $46 million, well below its current estimated market value of $87 million.

Hempel essentially bought the debt from Milwaukee-based Northwestern Mutual, which took possession from the previous owner, Teachers’ Retirement System of the State of Illinois. So the deal’s terms are not public.”

https://www.startribune.com/lasalle-plaza-downtown-minneapolis-sold-about-one-fifth-of-cost-to-build-it-pickleball-car-service/600285942/

What other loser investments are contained in the IL’s retirement fund portfolios?

Once we put pensions In the Illinois constitution all bets were off. Don’t remember how that happened. Enough people must have voted for it or it wouldn’t have passed. Same with the 3% compounded annual increase. Elections have so many consequences, especially in Illinois. Every Illinois politician collects a pension so it’s self serving. Don’t expect to ever see it on the ballot again. We had our chance and we blew it. We all know Illinois, why wouldn’t we expect it to get this bad?

It happened because our elected leaders thought it was unfair to tell people that after they had worked for 35 years that you were going to take away their retirement money. This was sponsored by republicans, received bipartisan support in the General Assembly and passed by the voters of the state. 1970 3% was added in 1989. It was supported by Republican Governor Jim Thompson. Now Thompson at least knew the state needed more tax revenue so he also raised taxes. He was right but Madigan didn’t let him get the full increase. This eventually led us to the Republican… Read more »

The inmates are running the asylum.

Wrong, not the publics elected officials, but Public Unions elected officials. They have gamed the system and destroyed it for everyone else.

Wrong. They were elected by all the voters.

Here is my best guess as to who exactly are the voters. Union members which comprise of at least 789,000 plus add spouses and voting eligible family members at you have at least close to 2,000,000 voters. Depending what’s on the ballot determines how many vote if it is their best interest. So turnout for recipients is a much larger percentage than the general public who may not benefit from the legislation. Here are some stats. This is a large organized voting block and is difficult to out vote them since most voters are clueless to the ramifications. Who fault… Read more »

The vote took place in 1970. Back then many people had pensions in the private sector as well. This was a matter of fairness as the idea that your pension could be stolen from you after working your whole life seemed horrible to most voters. Sure unions supported this measure as did Republicans and Democrats.

I had to pass a test on the new Illinois Constitution in 1970 to complete 4th grade. This was at one of the highest scoring elementary schools in the State. I was one of the rare poor students there, and not wanting to stand out, took the test seriously, although I have no recall if the pension provision was the subject of a question. In 1970, I agree that a pension provision of this type would not have attracted attention as most everyone would have viewed it as a question of fairness. The administration of pensions has been the problem… Read more »

The state pension fund for teachers have averaged over 9 percent for the last 40 years. They use a discount rate of 7 percent and they have shown they can out perform that number over the long term. These are obligations that are multi generation as you’ve noted. It doesn’t make sense to look at just a few years and when looking at long term, the assumed discount rate clearly isn’t the problem.

https://www.startribune.com/lasalle-plaza-downtown-minneapolis-sold-about-one-fifth-of-cost-to-build-it-pickleball-car-service/600285942/ LaSalle Plaza in downtown Minneapolis sold for $46 million Like other downtown buildings, the value of LaSalle Plaza has fallen since the start of the pandemic. In 2020 — payable in 2021 — the tower’s value peaked at a bit more than $103 million, according to Hennepin County property records. A source close to the deal said the building sold for $46 million, well below its current estimated market value of $87 million. Hempel essentially bought the debt from Milwaukee-based Northwestern Mutual, which took possession from the previous owner, Teachers’ Retirement System of the State of Illinois. So the… Read more »

Some investments make money while other lose. For the last 40 years TRS pension fund has been averaging 9.3%. Pointing out one loss here or there is pointless. You want to point to small snapshots in time and claim a larger trend. The facts don’t align to your thinking.

If the discount rate was at 4 percent, people might behave differently. This isn’t my idea – lots of actuaries stand behind it. You and I agree politicians have not funded the plans at anywhere near the required rate. It strikes me you would want to incentivize good behavior. Please don’t make the common finance mistake of citing an average rate of return. One or two bad years really sets a fund back, meaning performance has to be very good to get back to what was once even. Investors in the current economy know this all too well. I appreciate… Read more »

I’ve made no such mistake. I’m not quoting one or two years. TRS has averaged 9.3% growth from 1982 to 2022. That’s 40 years. The investment rate of return is not the problem.

If voters want 4%, I’m all for it as long as they vote for the tax increases to cover the larger perceived debt.

The 1970 Constitution was passed in Dec with a low voter turnout. How many people in the general public knew about the ramifications if they voted for it? Those in the “Know” had most if not all the details but the average person only knew what was in the papers. Remember-No internet/no computers/no social media to discuss the details. Even just recently when Madigan was speaker bills were put into the trash pile/new budget put in hours before they can vote and many lawmakers did not know what is in the new budget. Business as usual in Illinois. Transparency is… Read more »

It is also worth noting that the 1970 constitution was the product of a convention loaded with Democratic Party hacks and shills for special interest groups. Remember it is where Richard M Daley began his political career. This mess is the product of the baby boom generation.

Yet the pension amendment was proposed by a Republican from Hinsdale.

I was two years old in 1970 but over my life, I watched Illinois only continue to spiral faster and faster towards a financial calamity. All orchestrated by Michael Madigan…Madigan who represents a tiny little fraction of voters, has single-handedly created increasing momentum year after year, to send Illinois into the abyss

This is why me and my family high tailed it out of Illinois over 10 years ago.

Toss in another 500,000 short-haired suburban Harpies (of all races) and their soy-boy husbands, and there’s JB’s 2,500,000 million guaranteed votes every election. And 18% of those were mail-in ballots, roughly 450,000, assuming every mail in ballot is for JB (and you know they are!)

https://www.illinoispolicy.org/record-number-of-illinois-voters-cast-ballot-by-mail-in-2022-midterms/

Did public union retirees also vote for these leaders? Of course they did. It’s fair for some voters to pay for the sin of electing bad leaders, but not other voters who are now public pensioners. Can’t possibly ask them to share in the consequences of “the voters” sins.

It’s easy to commit sins after you are certain you have insulated yourselves from the consequences.

“It’s fair for some voters to pay for the sin of electing bad leaders, but not other voters who are now public pensioners.” If public pensioners live in Illinois they also pay taxes. They will pay their share just like every other Illinois taxpayer. If they no longer live in Illinois they won’t pay just like every other ex-resident of Illinois. The same consequences exists for both. The debt is owed by all and as such all Illinois taxpayers will pay. In all fairness and justice! The United States Supreme Court has made clear that the United States Constitution “bar[s] Government… Read more »

Pensions are not subject to income tax in IL, so I guess they won’t be paying their fair share after all. Yes, I’m aware that they pay other taxes. The non-pensioners pay those taxes too, in addition to their income tax. Some voters are just more responsible for their bad choices than other voters, I guess.

Social Security, IRA, and 401k withdrawals are also not taxed on income either. They are treated exactly the same. If you want pensioners to pay income taxes then so will the other private sector retirees. I’m good with that. Are you?

Yes. Putting the burden on young people, and acting as if this is somehow moral and just (all should bear the burden equally!) is wrong. But we both know that the pensioners will be outraged if the suggestion is made that they should be taxed. And the politicians will most likely cower in terror. They all know which demographic produces a high voter turnout.

I agree that the retired class won’t allow it without massive blowback. Both public and private retirees. Doesn’t mean they shouldn’t tax retiree income the same.

There are a couple of problems with taxing 1099R pension income earned in Illinois. First and foremost it was taxed by the State as it was earned. Do you subject the deposits to double taxation or tax only the gain? If only the gain, they aren’t ordinary income so are they interest? Dividends? Capital gains? Each category has a different rate for long and short term. Then, there is the question of losses in down years. Can they be deducted? By far though the biggest hurdle to taxing pensions is every politician who sits in Springfield has one or two… Read more »

“First and foremost it was taxed by the State as it was earned.” Are you claiming that pension contributions were funded with after tax money? Contributions from the employer been taxed? From my understanding not one dime of pension income has yet been taxed and most states tax when payments are received. Why do other states have no issues with taxing pensions? Move to one of those states and you will find that it’s not that difficult at all. How does one have losses to pension income? Did they pay the pension fund instead of getting paid. The pension fund… Read more »

I believe if you check the paystub you’ll find contributions to pensions,401, 403 and 457 deferred plans are all made after State income tax has been paid on the taxable gross amount. Federal tax is deferred not state tax.

Arizona, Arkansas and others who tax pensions have other state tax laws that differ from Illinois. Retirees from Illinois who move to another state may indeed find their Illinois pensions taxed again in their new location. Something to consider before a move.

Any pre-tax contributions to retirement accounts that aren’t counted towards your federal AGI are carried over to your state return. Your state tax return then requires you to add certain income using schedule M. This form also outlines what income can be subtracted/added to your state AGI. Your retirement contributions are not added to your Illinois AGI.

Looking at your paystub won’t tell you anything. Your paystub would only show state tax withheld not actually what you owe. My guess is your withholding is including income for retirement contributions but that’s not the same as taxes owed.

I don’t even count Edgar and Big Jim as Republicans anymore. Now that we have the 40,000 foot view you can see that they worked to serve their own interests and of course that means working with Madigan, DeLeo, and every other RINO who was working or is still working in government. There has been no opposition party and the state is solid blue by a longshot. The state has been so carelessly financially mismanaged with many corrupt players enriching themselves with tax dollars and largesse. No opposition party, no understanding of a balance sheet, and absolutely stealing for so… Read more »

Do not do anything till the funds run out. Then let the courts sort it out.

Law school 101: when the facts don’t support you, argue the law. When the law doesn’t support you, argue the facts. Public employees and retirees argue the law, based on an Illinois court decision that is at variance with other states. The decision was rendered by elected judges who are in thrall to the unions which provide campaign contributions and votes, plus the fact that those judges are also setting precedents for their own government pensions. Facts include declining ratios of actives:retired, retirements at younger ages with increased life expectancy, investment losses, eroding tax base and “robbing” other public sector… Read more »

One more thing about ‘Law 101’, when challenged repeat the same answer but much louder.

What is rarely addressed in the conversation is politicians’ failure to adequately fund pensions.

Illinois pols have spent decades “kicking the can down the road,” with only their next election in mind.

Political cycle after political cycle voters keep electing the same pols who promise the moon and the stars and deliver nothing.

Stupid chickens.

The Actuarial Science deniers on CF scoff at charts, graphs, and projections. Their union thugs and the CTU have told them that everything is copacetic and that’s all they need to know – financial analysis is for suckers.

The thing Illinois residents need to ask themselves is, “What’s more likely, pension benefits being cut when the reserves are drained, or a new tax, very possibly on retirement income?

I myself found it too risky to stick around in Illinois and wait for the answer.

Per the State Constitution those benefits can not be cut so it will be new taxes.

(I should add each and every day I see new spending initiatives so the possibility of cutting spending ain’t gonna happen.)

City pension debt will also have to add untold $billions$ in additional debt depending on what state legislature decides to change for TIER II pensions to meet minimum “safe harbor” requirement or additional changes. Per Suntimes article from yesterday there are 2 bills in the works that Brandon asked to be held off on til fall for Chicago Fire alone (https://chicago.suntimes.com/city-hall/2023/7/5/23784857/chicagos-pension-crisis-investment-income-stock-market-police-fire-annual-audit-deloitte). One would assume if these bills pass then there will be further TIER II pension change bills for cops, teachers, etc(Catanzara and Gates talk about it on media all the time). These pension changes, just like the 3% COLA… Read more »

WM, WP is well aware of the magnitude of the health benefits debt, but I agree this debt should routinely be noted by WP and anyone else whenever pension debt is estimated. To estimate total IL debt from the two sources, add a staggering 40 percent to the pension debt. I’m not sure of the add-on percentage for Chicago alone.

The upcoming recession will accelerate the fall off the pension fiscal cliff to a point at which a national solution will be implemented – a Federal bailout – particularly if we get another Democrat-run oval office and legislature. Those in states that have exhibited prudent fiscal management will pay for the sins of those states which were negligent. Appalling and unconscionable, but without pension reform on a massive scale, the easier fix is to raise everyone’s taxes. And with the weight of union influence on Democrats, they’ll take their marching orders. Here’s a better idea than burdening non-Illinois citizens with… Read more »

“One day we’ll finally talk about reforms. But not yet.”

Meanwhile the spending continues on like the partiers on the Titanic till it happens.

Boom!

Well, this problem isn’t going to go away for BJ without some sort of fix. Which will likely take the form of another epic pension stall, justified and excused with monumental obfuscations and mendacities. It’s either that, or higher taxes for pensions, and lots more of them. Meanwhile, Johnson still can’t explain where the taxes are going to come from to fund all the ‘social worker on every corner & chicken in every pot’ stuff he actually campaigned on. Johnson and all these unions & progressive/woke agencies-n-etc – they’ve been rabble rousing for years, claiming to have figured out better… Read more »

When union pensioners get IOU’s from the city and state, maybe then reform of the corrupt and broken system will start. But certainly not before then.

I’m sure there’s no political will to do this but I think if you collect a pension and then take another job then that pension should be considered taxable income because you’re really not retired. Wouldn’t want this to apply to the person collecting a $30K pension and working a job that only pays him $40K but for the big double dippers it should apply.

We don’t have what you want in IL, but with only a few exceptions, perhaps, any new income not considered 1099-R income will be taxable by the state. That in itself embodies at least some of the general idea of your position.

I believe in Wisconsin when then Gov Walker changed the policy of a person who retires and goes back to work many times in the same job they must suspend their pension. Of course many were grandfathered in. This took place a number of years ago so new retirees cannot double dip. I’m sure there are income limits and if they start a business or work for someone else not in public service may be allowed. This is still legal in Illinois. Rockford’s park district super retired with a nice pension and tried to get rehired for the park district… Read more »

Retired teachers often still do work for school systems, sometimes their own, If it can be done with pension contributions not going to TRS but maybe ILMRF that’s permissible without any pension reduction by TRS, and if that employee meets a minimum allowable years of employment (5 years?) he may receive a pension from TRS. But, with only minimal years of service credit it’s going to be a very small pension. I do know of one case where the employee had a valued “skill set” beyond teaching, then started a higher paying job under ILMRF presumably while still drawing his… Read more »

That should have read “(5 years?) he may receive a pension from ILMRF.”

A small pension does not mean an inexpensive lifetime health plan, does it?

I don’t know. My guesstimate is that the size of the pension and/or years of service are not connected at all to the medical insurance plan’s benefits or benefit levels. In percentage terms, though, such 2nd-career public employee retirees surely are so rare its a blip in the overall cost to the state. Maybe there’s a prohibition to granting such people more insurance coverage if they already have it through another state employee retirement system. Naw, that would make too much sense! Legislators rarely give all that much thought to the cost of bills they pass into law most people… Read more »

We’d have to amend the constitution and as I said there’s no political will to do that and I don’t expect it to happen in my lifetime. In a few years when I retire I’ll be out of IL, if I lose my job I’ll be out sooner. If I saw that they were trying to make things better for taxpayers I’d stay but all they’re trying to do is buy votes by making things better for public sector unions at the expense of taxpayers.

Good luck getting something like that passed

Just sayin…

BLM BJ won’t care about this. He only cares about the teachers union, and that fund will be fine until his destruction of the city is complete, which will be less than the 8 years. If the cops fund goes under, better for BLM BJ’s primary constituents, the criminals.

Johnson will need to take a Tylenol the size of the John Hancock building for his headache to tackle the pension problem.

The Civic Fed wrote recently that Illinois could raise $1.8 billion annually by taxing retirement benefits. Does Wirepoints think a future tax on retirement benefits is likely? The Civic Fed writes: “Of the 41 states that impose an income tax, Illinois is one of the few that does not tax retirement income. It is one of three states that exclude all pension income and one of 27 states that exclude all federally taxable Social Security income. The Illinois Comptroller reports that the exclusion of federally taxable retirement income resulted in Illinois losing out on nearly $2.9 billion in individual income… Read more »

That would not come anywhere close to solving the problem and you’d soon see the 100K adjusted downward until it’s 20K since those that could leave would. (Although a lot already have.)

My thoughts exactly. Give em one more reason to leave….

The article doesn’t come up. But I wonder how many retirees are actually staying in this pit of a state. We know that the wealthiest retirees, the retired municipal workers, get out of here pronto so that the only thing they still have of Illinois is their monthly pension check.

The last report I viewed shows that 82% of pensioners remain in the state. Most people stay despite your made up “facts”. Typical Proud and Ignorant MAGA.

Would need context for that number. If it was 82% in 2022, 82% in 2021, 82% in 2020 then there’s no trend, if it was 82% in 2022 83% in 2021 84% in 2020 then it would show a trend. I’m assuming it’s the latter but I’d also assume it’s the later with the entire retirement population in IL.

You’re doing a lot of assuming. The report was from 2019. Either way, most of the pension money stays right in Illinois despite all the assumptions.

The assumption I made is that pensioners leave at the same rate as non pensioners, I could be way off on that. More people leaving than coming is not an assumption.

Yes, 82% of pensioners, but what % of pension money leaves Illinois? I’ve read that the university system – with some of the highest paid grifters – has far more people leaving than any other system. It would make sense that the local guy with the smallish pension stays closer to home but the higher paid doctors, judges, professors, educators, former politicans, they all leave the state.

“They all leave”.

Show your work. I doubt you read any article that shows they all left. What percentage? What income? Most of the money stays right here. Regardless, who cares? It’s their money. No different than a private sector worker, they are free to move and spend their money anywhere they like.

I found the article. It’s almost 83% of the pension money that stays in Illinois. In 2019, $2.4 billion of the $13.9 billion leaves the state.

So, it’s the smaller pensions that leave. Interesting.

LOL

Nationally, 90% remain in-state.

I have a number of municipal and state pensioners in my neighborhood. You would be hard pressed to find a more slothful, yet arrogant kind of Democrat as these folks. So most are still here in the ‘utopia’ they and their union bosses helped Democrats create.

They should tax out of state residents on their IL state pensions.

The state of residence can do that. The state where it’s paid cannot.

And now California has an exit fee, trying to keep folks from moving out.

This is what will happen.

A bill to tax retirement income will be rammed through.

Then the Democrats will carve out an exemption for public sector retirees, leaving private sector retirees like me holding the bag.

Then more private sector retirees will attempt to leave the State.

Then the crooked Democrats will ram through an exit tax.

Simple.

ABSOLUTELY, if you collect a state pension and live out of state there should be a distribution cost of 10%. This will collect from the benefits you are receiving and no longer contribute back into the state.

How about a 10% fee on IRA and 401k accounts for people leaving the state. I mean they made that money in state and now they no longer contribute.

I don’t think you really intended this idea to apply only to retirees, but it would seem that way in that the postings here at the moment deal with IL public employee retirees. I doubt it would be legal if applied solely to that group. Again, I’m guessing that’s not your intent.

I was merely pointing out the absurdity of the idea. Would the same people that support taxing out of state pension retirees also want to tax out of state 401k and IRAs from individuals that moved? I’m guessing no. Completely illegal either way.

👌

Tax everyone’s retirement income. Period.

At source, like they do in Europe.

Then all those who have left the state having earned their pension here have to pay Illinois tax.

Because Government pensions are so much more than mine let these rich folks pay their fair share LOL!

Fair enough?

Sure, “fair” is always sticking it to someone else, isn’t it?

Again, most residents IRA s and 401K s weren’t funded with taxpayers money. You keep conveniently omitting that fact.

Somehow I’m failing to see the distinction. Whether you are a private or public employee 401k and IRA accounts are funded by pre-tax dollars unless you chose a Roth acct. Whether the earlier source of those funds is funded by someone in a private or company purchase or it’s funded by the taxpayers it’s all funded in general terms by people in the same society-at-large. The source is irrelevant, isn’t? In both cases it’s pre-tax money funding the account. Please “set me straight” so I might agree with you. Polite responses are appreciated!

The fact that a massive shortfall in the budget is looking to be corrected by taxing people that funded their retirement with their money just the same as those with pensions much more lucrative than those in the private sector, yet funded by that sector is rather irksome. Add in the fact that more than a few drawing the taxpayer funded pensions have been proven to be lax in their duties and committed criminal acts while supposedly serving the public as elected to is the capper.

Okay, at least I understand your viewpoint now. I thought you were attacking public employee pensions from a strictly economic basis. There’s a hint of that in your response, but it’s got a stronger suggestion of such people being unworthy of the general public’s forced personal sacrifice. That’s probably so in a few cases as you’ve cited, maybe so in some others and maybe clearly not so in yet others. Morality and work ethics vary among the general public, too. There are way too few monks in our society forever seeking forgiveness for their sins while slaving away for room… Read more »

I completely disagree. How is this any different than an exit tax or an onerous real estate transfer tax? Why should anyone have to pay for their freedom to escape the fiscal hellholes of Illinois, New York, New Jersey and Connecticut? By no means am I a progressive ideologue. Rather, we should be taxed LESS not MORE.

If you move to a state that doesn’t have high (or no) income taxes, it really is not a huge incentive anyhow. I agree with Paul however they should have a (tax) distribution fee of any state retirement income going to a non-resident.

Even though Illinois is one of the few states that doesn’t tax retirement income, it doesn’t seem to draw retirees from other states that do. So it’s not exactly a tax policy that’s drawing retirees to the state. While it might keep some residents here, I’d wager there are more important factors keeping those retirees in state (ie family). Taxing retirement income might be the last straw for those folks. The sad fact is that retirees are the fastest growing segment of the state’s population and generally hold a lot of wealth. Not taxing them seems foolish. At the very… Read more »

You are completely correct Nixit. They should be taxed just like everyone else. Some may leave but most will stay and the state will collect around $2 billion more per year. A more fair taxing system coupled with much needed revenue.

More fair taxing system. Much needed revenue. Yeah, they’re spending it so wisely, aren’t they? Let’s not demand less spending. Let’s give them more.

I would love less spending. Unfortunately the majority of the voters don’t agree with me. So instead we need more revenue.

If it were done as you propose it would surely be illegal since your intent clearly aims at exclusively punishing public employee retirees simply by stating SS is exempt. But, if you did it a bit more cleverly by exempting, say, $60k of retirement income for an individual tax return and twice that for a married joint tax return you’d accomplish the same thought without referring to SS at all.

Oof, you don’t understands wages.

We already pay taxes on our social security contributions as that 6.2% is deducted from our gross wages BEFORE any deductions for retirement (pension or 401k) contributions. Pension and 401k contributions are both pre-tax deductions, meaning you have not paid income taxes on those contributions, hence they should be taxed now in retirement when they are withdrawn. Get it? Treating SS income like tax-deferred retirement income is inherently inequitable. They are entirely two different things.

Furthermore, many state workers and IMRF participants are on a pension/SS hybrid system, so there is no punishment.

Well, yes, you do raise a good point. But, still, I’m not sure that mentioning SS income as a deduction against state retirement income taxes would fly politically. That alone is likely to create reasons for dismissing any such retirement income tax. It’s hard enough to think about any such tax successfully being enacted in IL, and your SS language in it could be yet another barrier to getting it done.

Ken, my guess would be that’s less likely than an attempt expand the sales tax base to services or simply raise the income tax rate.

Good luck on getting a pension tax in Illinois. I just don’t see it happening

I’m not sure of the outcome, but if IL decides to tax pensions, I think a large number of pensioners will bite the hand that fed them and scoot.

Due to not considering a mass out-migration of retirees, IL may over-estimate a little the additional revenue it’ll receive from taxing retirement income, and water’s a little wet.

Revenue projections that result from new taxes or even tax changes always are subject to both known and unknown consequences. There is nothing new under ths sun as an old saying would remind us.