By: Ted Dabrowski and John Klingner

Borrowing to fix a debt problem does not work.

Just two weeks ago we warned East Moline residents of the dangers of letting their city officials borrow tens of millions of dollars to supposedly “fix” the city’s struggling public safety pensions. The city’s plan amounts to nothing more than “gambling on the stock market to get out of financial troubles,” we said of East Moline’s intentions to borrow $41 million by issuing what are called Pension Obligation Bonds, or POBs.

Now Moody’s Investors Services, the credit rating agency, has hit the city for its plans to borrow and expose its residents to potential investment losses. East Moline got a double-notch credit downgrade from Moody’s, leaving the city’s credit rating just two notches away from a junk rating. Think of it as getting your credit score dinged hard because you’re now riskier to lend to. Not only that, but you’re using up your borrowing capacity. If you ever need money in the future, you may not be able to get another loan.

The POB scheme is a bit complex, but it basically amounts to the city borrowing money and investing it in the financial markets, hoping the investment returns exceed the cost of borrowing when it’s time to pay back the debt years down the road. It’s a risky business called “interest arbitrage” and it’s a game that only brokerage houses, banks and qualified traders should play. The risk of losing money is real as evidenced by the trillions in losses experienced during the DotCom and Great Recession collapses of the last 20 years.

Not only that, but if the gamble in East Moline doesn’t work, it’s ordinary residents who’ll be on the hook for higher taxes to make up the losses. It’s definitely not something city officials should be involved in and one of the key reasons the Government Finance Officers Association says “state and local governments should not issue POBs.”

By the nature of its downgrades, Moody’s is also concerned about POBs. Here’s what the agency specifically said in its downgrade press release:

The downgrade to Baa2 reflects the city’s substantial leverage from debt, pensions and other post-employment benefits (OPEB) with high fixed costs. The city intends to limit the required increase in future pension contributions with the issuance of pension obligation bonds, though this strategy carries risk and heightens its exposure to potential investment losses.

High fixed costs have contributed to a series of operating shortfalls over the past several years. Management reduced expenses to stabilize operations in 2020 and maintains adequate reserves. Funding from American Rescue Plan Act (ARPA) is expected to improve fund balance in 2021. The general fund cash position is very narrow, though overall operating cash is sound. The rating also incorporates the city’s modest but growing tax base with relatively weak resident income.

POBs are a problem because they aren’t a real solution to cities’ pension crises. Borrowing more money doesn’t fix any underlying problems; it only hides them and lets them fester.

Blagojevich and Quinn’s POBs

East Moline residents only have to look at the state itself to see how POBs helped make Illinois’ pension crisis worse.

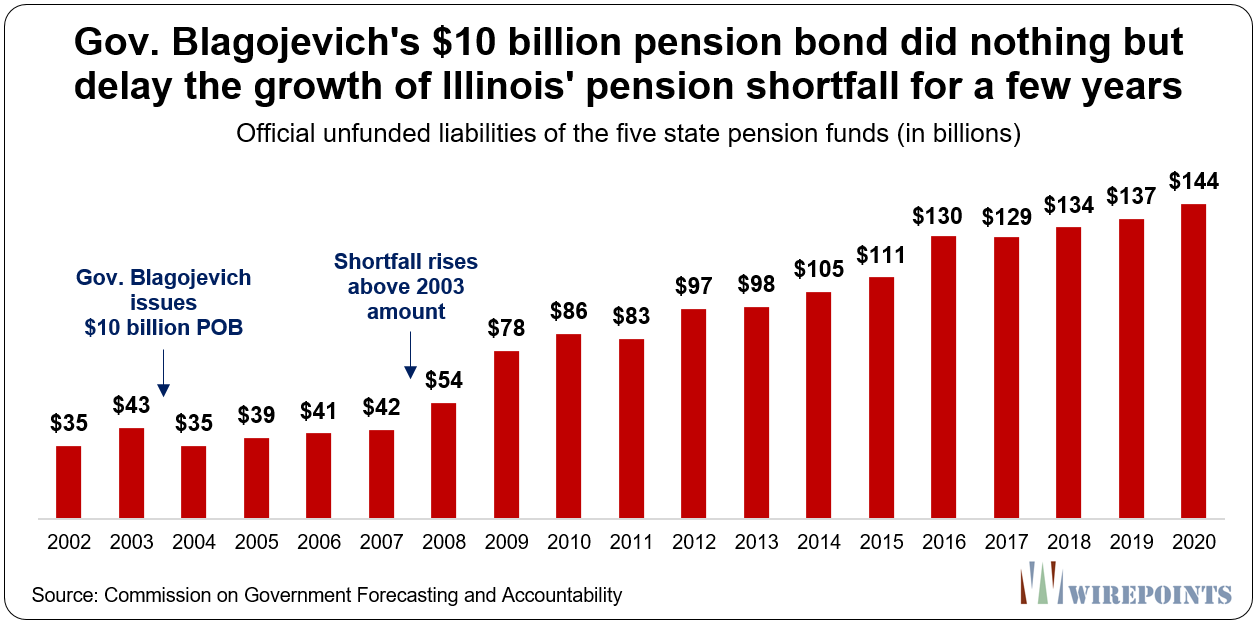

Gov. Rod Blagojevich issued $10 billion in POB’s in 2003 and poured the money into the pension plans. The additional cash in the plans initially dropped the state’s pension shortfalls by $8 billion to $35 billion, but it only took four years for the pension shortfall to end up higher than it was when Blagojevich issued the POB.

Gov. Pat Quinn used the same playbook to borrow $3.7 billion and $3.4 billion in 2009 and 2010, respectively. And just as with Blagojevich, the shortfall continued to rise and now totals more than $144 billion.

Gov. Pat Quinn used the same playbook to borrow $3.7 billion and $3.4 billion in 2009 and 2010, respectively. And just as with Blagojevich, the shortfall continued to rise and now totals more than $144 billion.

Borrowing by both governors gave the illusion that something was being done about pensions, but the reality is they did nothing to slow the rapid growth in pension promises.

To add insult to injury, Illinoisans are still paying back Blagojevich’s 2003 POB. They’ll be paying back principal and interest on the bond – a total of $11 billion – through 2033.

East Moline residents face the same problem. They’ll be forced to slowly pay down their own POB over the next two decades. And without real pension reform, they can expect their pension shortfalls to increase at the same time.

Read more about POBs:

- Wirepoints’ report on Illinois’ largest 175 cities.

- Politicians’ next pension “fix”: Gambling with your money

- Pension obligation bonds: Some Illinois city leaders want to gamble with taxpayer funds

- Chicago’s pension bond scheme: What an honest press conference with Rahm Emanuel might look like

- Pension Obligation Bonds Are Like Big, Fat, Dangerous Margin Loans For Stock

- Communities in Crisis: More than half of Illinois cities get “F” grades for local pensions

Expect no retraction or apology. This what they do.

Expect no retraction or apology. This what they do. The state’s existing buyout program for its own pensions is the precedent for Chicago, which should be a warning: Look out for similar exaggerated claims and shoddy analysis.

The state’s existing buyout program for its own pensions is the precedent for Chicago, which should be a warning: Look out for similar exaggerated claims and shoddy analysis.

Have to immediately ditch these lavish public sector defined benefit plans. Such plans have been tossed years ago by almost all companies cause they are expensive and risky. Immediate, effective action on public sector pensions in Ill is a must-have, now. Otherwise, a slow painful ride, with no money for almost anything except the vaunted public sector class. (ps firemen too!—almost no fires these days–old days wood buildings and no water extinguisher systems in buildings).

Gee, why hasn’t anybody else ever thought about that?

The lower rating means better rates for the vultures (investors, market makers, brokers, etc.) The only real guarantee they need is that government, in the future and forever, is willing to tax, tax, tax the public. That is the only real collateral. And they know they will get that guarantee as people don’t want to lose a house. The downgrade and nasty letter from Moodys is all just a part of the game you see. Thats the part that makes Moodys look credible and free from prosecution. Because in reality Moodys is the first market maker, they make the market… Read more »

Most people pay attention to unpaid bills. Many are aware of pension debt. Very few are aware of the general debt floating around any level of government.

Part of the con is that there is a team of private sector consultants (i.e., those with selfish interest in selling bonds) who participated in convincing gullible and short-term thinking officials that they have their interest in mind. This is the never ending path for greed and shallow solutions. Those complicit in the debt game knew what the rating agencies would say but don’t give a damn because they need clients and sales. Did the city hire an independent (truly independent) financial advisor? If yes, we need to read their report. If not, well, then they bought into someone’s selfish… Read more »

There are NO Democrats at local, state or federal who believe in stewardship. It’s all about the expediant -just a big financial con game, with taxpayers the only ones held accountable. ‘Crack-up Boom’ will happen.

You can’t borrow your way out of debt.

Now East Moline has gotten a double-notch credit downgrade from Moody’s, leaving the city’s credit rating just two notches away from a junk .The rating on the Build Illinois bonds reflects Fitch’s view and enacting plans for early retirement of federal pandemic loans.

Those two sentences, written like that, first a sentence about a Moodys rating, and then a sentence about a Fitch Ratings, needs more clarification to have any meaning.

What Build Illinois bonds?

East Moline, il Build Illinois bonds?

When was that rating issued?

What is the URL to the referenced Fitch Ratings in the second sentence?

Do you believe the Moody’s rating is incomplete, missing some of the items in the second sentence?

Pension Bonds for Dummies, Chapter 1 (repeat). The Debt Shuffle. Exchanging one form of debt (unfunded pensions) for another form of debt (pension obligation bonds) does not address the root problem (debt). https://wirepoints.org/a-warning-to-illinois-taxpayers-pension-obligation-bonds-let-politicians-gamble-with-your-money-wirepoints/#comment-240521 Pension Bonds for Dummies, Chapter 2 (new learning) Risk is shifted from enrolled members in the pension fund (afraid of a potential future reduction in benefits) to both pension obligation bondholders (risk of municipal default on payments to bondholders) and municipal taxpayers (risk of tax hikes if pension fund investments underperform). Did anyone explain Chapters 1 and 2 to the taxpayers in plain English with easy to… Read more »