By: Ted Dabrowski

State politicians are ready to go on another borrowing binge.

According to a recent S&P presentation given to bankers and other government officials, Gov. J.B. Pritzker wants to borrow another $6 billion from the bond market over the next year. It’s part of his plan to hike taxes, borrow and extend debt repayments to plug the state’s budget holes. As a banker present at the meeting told me, even the financiers were caught off guard by the amount and the timing of the debt.

The question is, “when will too much debt finally be too much?” As the Wall Street Journal recently reported, Illinois already contributes more than 25% of state revenues toward pensions and other debt, and it would jump to over 50% if Illinois paid the proper amounts. Illinois is the nation’s extreme outlier when it comes to too much debt and you have to wonder how far the state can push it before the game ends.

The new borrowings, which still need legislative approval, represent a nearly 20 percent increase over the existing $30 billion the state already owes in general obligation bonded debt.

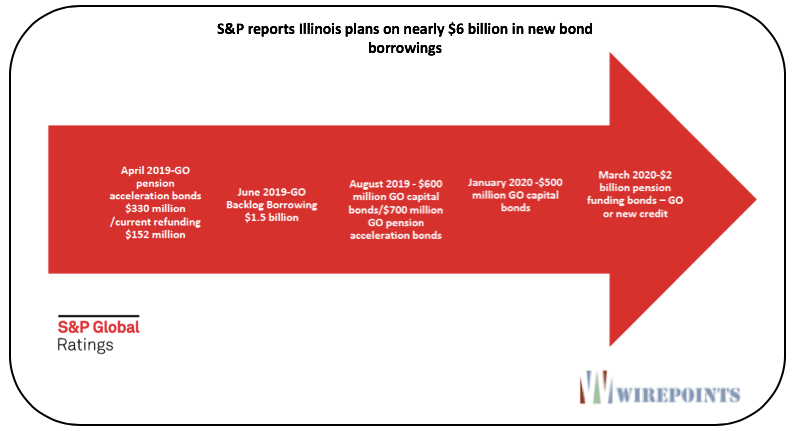

What’s on tap, according to S&P?

- $1.5 billion more to pay down the state’s unpaid bills

- $2 billion in pension obligation bonds (a gamble with taxpayer funds)

- Another $1 billion to pre-fund pensions (virtually same as above)

- $1.1 billion in general obligation bonds for capital

- $150 million to refinance debt

Look for the status-quo pundits to say that all this new borrowing is good. That it refinances more expensive debt, like unpaid bills, and that it helps replace some of the pension debt outstanding.

But anybody who’s been following Illinois knows that more debt simply begets more spending and more debt. It’s how Illinois has ended up with the nation’s worst pension crisis and $234 billion in unfunded liabilities, according to Moody’s. It’s how the state racked up another $73 billion in retiree health insurance obligations, all of it unfunded. And Illinois’ bonded debt burden is already one of the nation’s highest, according to the S&P presentation.

Borrowing more to “fix” the state’s debt problems is precisely what’s gotten Illinois into this mess and Pritzker seems set to continue the trend that was started by former Gov. Jim Edgar’s pension ramp and perpetuated by Govs. Rod Blagojevich and Pat Quinn’s pension obligation bonds.

Nevertheless, it’s clear Illinois hasn’t reached an inflection point yet. A demand for municipal debt nationally, a goldilocks U.S. economy and low rates globally mean investors are still looking for high interest rates anywhere they can get them. Illinois and the premium interest rates it must pay gives them just that.

But the good markets can’t be expected to last forever. Expect more eyebrows to be raised as the debt load gets bigger and the markets get dicier.

For details on how Illinois has racked up so much debt, read Wirepoints’ research reports and commentary here:

Every Illinoisan Must See These Two Charts In The Wall Street Journal – For the state, about 25% of revenue now goes towards pensions and other debt, but that would jump to over 50% if proper amounts were being paid.

Moody’s vs. Illinois politicians: $100 billion difference in pension debts – Moody’s recently released what fiscal realists would say is the true estimate of Illinois’ unfunded state pension liability – $234 billion.

Illinois’ other debt disaster: $73 billion in unfunded state retiree health insurance benefits – Illinois owes another $73 billion in retiree healthcare debt and doesn’t have a single dime set aside to pay it.

Gov. Jim Edgar’s starring role in Illinois’ pension crisis: It’s bigger than just the “Edgar Ramp” – The bipartisan compromises Edgar championed are responsible for turning the state’s pension problem into a full-blown crisis.

Special Report: Illinois state pensions: Overpromised, not underfunded – Illinois’ pension crisis is the result of overpromised benefits, not underfunding by taxpayers.

Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

TruthinAccounting had a piece on the use of “deferred assets” on balance sheets. I thought these went out with Enron, but apparently Illinois and a few other public entities are using them to cover up pension debt. The Philly School District in Pa. has assets of $2 billion, deferred assets of $700 million, and debts of $8 billion. I hope that GASB looks into this kind of book-cooking.

https://www.truthinaccounting.org/news/detail/how-big-is-illinois-balance-sheet

They borrow because they can, the friendly rating agencies, the great collateral offered to the bond market in both a constitutional clause and hard collateral putting bondholders first in line for repayment. A thirsty market for yields. And leaders willing to raise taxes. And the elimination of bondholders risk in bankruptcy. All forces are enableing more borrowing not less. The only possible end to Illinois borrowing madness is when the rating agencies declare junk and force the big players out. But that won’t happen anytime soon, the market and raters have us right where they want us, by the short… Read more »

Spot on

You can’t fix a debt problem with more debt.

When will these knot-heads ever learn?

You can if you are doing refinancings at lower interest rates however we know they are doing refinancings at ever higher interest rates given their credit rating. So, yes they are knuckleheads. But, they keep winning elections

And it’s not just that. They borrow more (longer maturities, or more backloaded repayments) to free up space to borrow more. Smart.

When the entire state is utterly destroyed and looks like Harvey.