By: Ted Dabrowski and John Klingner

Download a PDF copy of the report

Pensions get all the attention when it comes to Illinois’ collapsing finances. But there’s another government-worker benefit also wreaking fiscal havoc – free and heavily-subsidized retiree health insurance for state workers.

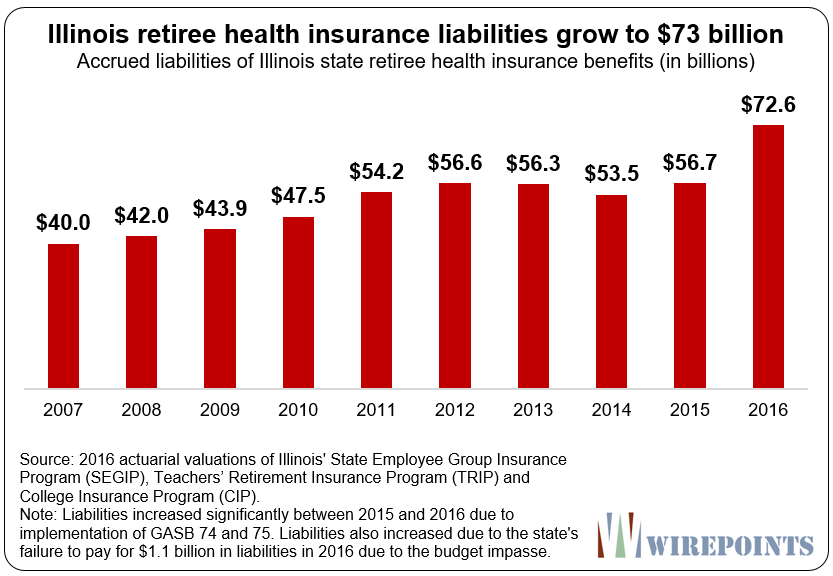

Illinois has promised $166 billion in retiree health insurance benefits to public-sector workers over the next 38 years. Actuaries say the state should have $73 billion invested today so it can safely make those payments in the future. The problem is, the state hasn’t set aside anything at all.

That $73 billion hole is yet another financial time-bomb – one that’s been totally ignored thus far by Illinois’ lawmakers, civic leaders and the media. Unfunded healthcare promises have grown 80 percent in the past decade and are now compounding Illinois’ state and local pension crises.

Illinois courts have ruled that public employee health obligations, like pension benefits, cannot be impaired. Unlike pensions, however, nothing is set aside and invested to cover that future expense. The liability is entirely unfunded, which is called a “pay-go” system. Instead of setting aside money for future costs, the state simply pays retiree healthcare costs as they are incurred. Growing future costs are left to future budgets.

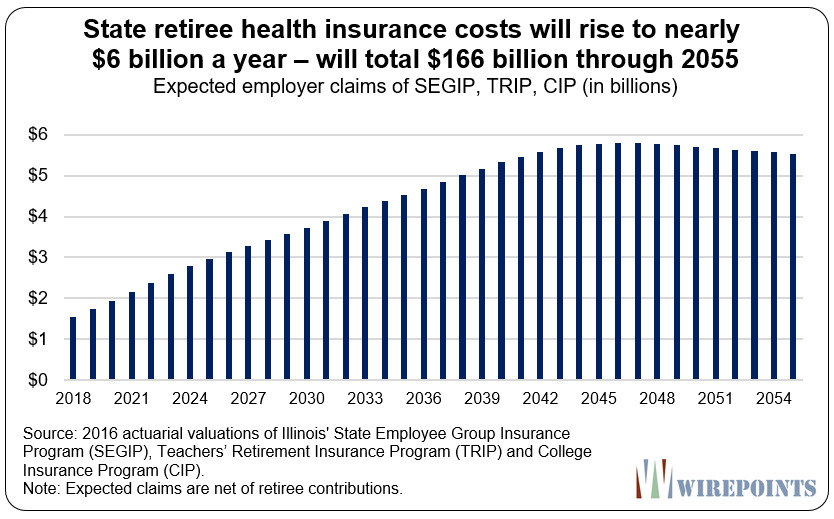

Expect those annual payments for retiree health benefits to further squeeze Illinois’ budgets as the bills come due. Payments by the state – meaning taxpayers – will rise from $1 billion today to nearly $6 billion in the future to meet the state’s yearly retiree health insurance obligations.

Officially, retiree health and pension costs are already set to consume more than a quarter of the state budget over the next 30 years. But the state’s official numbers grossly underestimate Illinois’ true retirement costs. If the real cost of pensions and retiree health insurance were properly measured and paid for, they would consume an untenable 50 percent of the state’s annual budget.

That fact shows that without massive reforms, retirement costs are going to damage Illinois beyond repair. The state has no choice but to dramatically reduce its unfunded obligations.

Illinois’ “other” retirement debt

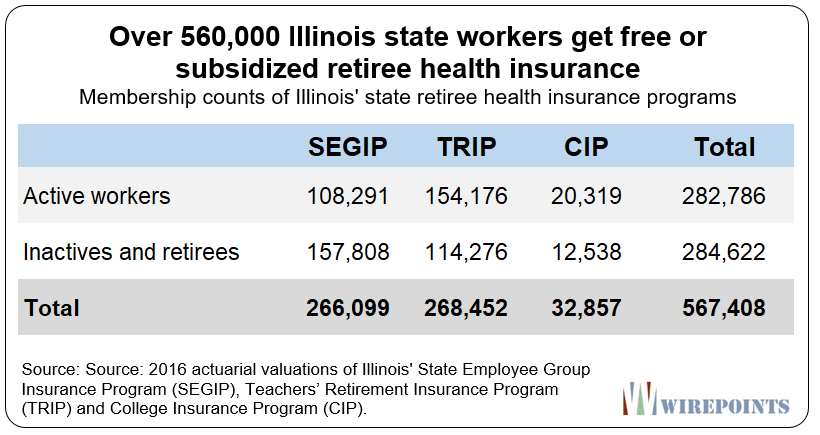

Illinois provides 567,000 public sector workers and retirees with subsidized retiree health insurance benefits. Beneficiaries include state employees and retirees (including state workers, public university employees, judges, and lawmakers), who participate in the State Employee Group Insurance Program (SEGIP); teachers in the Teachers’ Retirement Insurance Program (TRIP); and community college employees in the College Insurance Program (CIP).

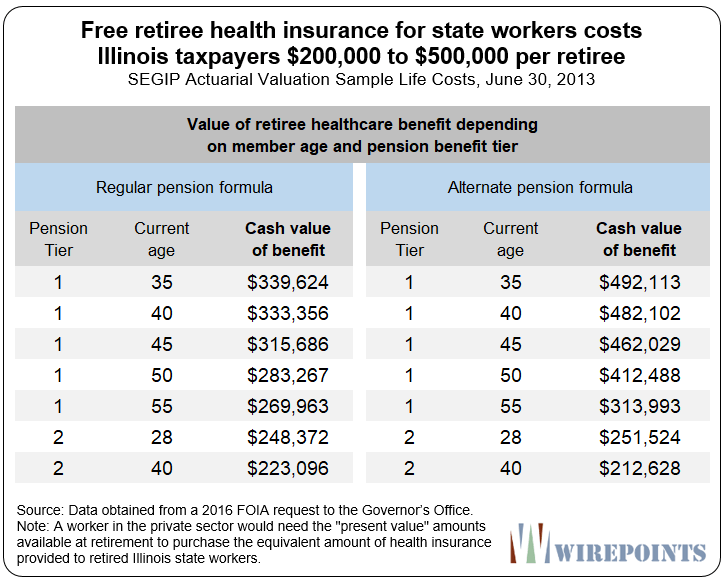

SEGIP provides the most lucrative health insurance benefits of the three systems. SEGIP members with 20-plus years of service receive free health insurance during retirement. (The system current provides state workers with a 5 percent discount on their retiree health insurance for every year of work, maxing out at 100 percent for 20 years of work. Retirees who retired before 1998 earned free health insurance after just 8 years of service – the minimum vesting requirement.)

According to a 2011 study by Mercer on behalf of the Commission on Government Forecasting and Accountability (COGFA), most SEGIP members end up receiving free insurance: “Roughly three fourths of current retirees have at least twenty years of service and, therefore, do not have to pay contributions.”

Wirepoints also analyzed the 2018 state employee pension database and found that 73 percent of State Employee Retirement System (SERS) members have worked the requisite years to get free retiree health insurance.

The present value of that benefit for career workers is worth $200,000 to $500,000 per retiree, depending on the pension tier and age of the employee, according to a 2016 FOIA obtained from the Governor’s office.

(Retiree health insurance benefits contribute to the $110,000 average annual compensation packages received by state AFSCME workers. For details, see: Six facts Pritzker can’t ignore when negotiating AFSCME’s contract.)

Free retiree health insurance provided entirely at the employer’s expense is a benefit that’s rare in the public sector and almost unheard of in the private sector.

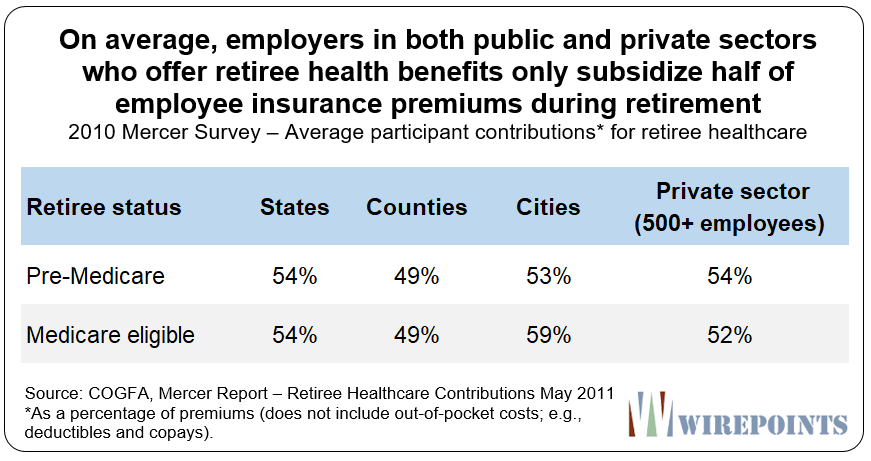

The Mercer study found that, on average, state county and city governments across the nation who offer retiree insurance benefits only pay about half of their employee’s premiums during retirement.

Mercer also found that most small- and medium-sized employers in the private sector do not offer retiree health benefits. And the 25 percent of large employers (500-plus employees) who do offer retiree health insurance benefits only pay half the cost of insurance, on average.

Members of TRIP and CIP get different, less generous benefit packages, but still receive insurance subsidies worth 50 to 75 percent of their premium costs – subsidies paid for by taxpayers.

A growing budget problem

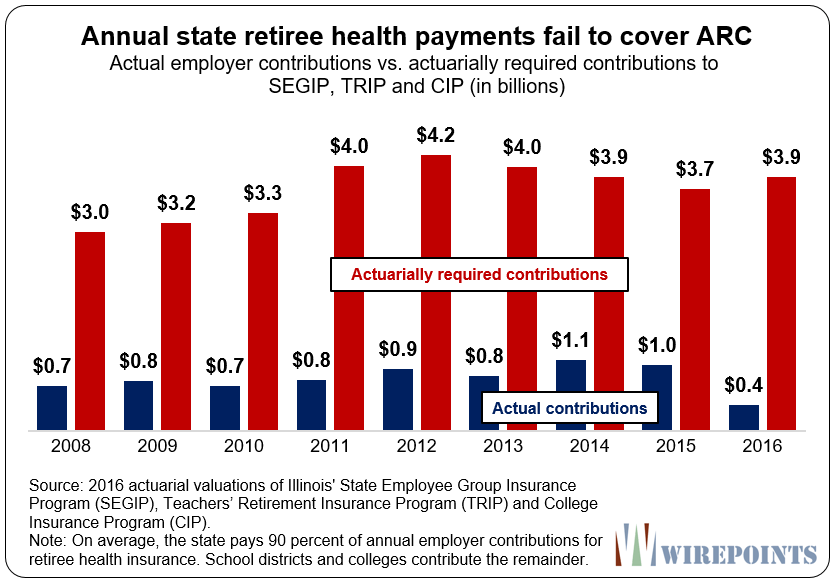

Illinois operates on a pay-go basis for retiree health insurance, meaning it falls far short of paying the actuarially required contribution, or ARC, for health benefits. The ARC is the amount actuaries say the state should pay to cover both current year costs and some of the unfunded liability.

For example, in 2008 the state funding shortfall already totaled $42 billion. But instead of paying the ARC of $3 billion, Illinois contributed just $700 million – the amount needed to pay only that year’s benefits.

That same underpayment has continued since then. The state has consistently underfunded its ARCs, leading to an average payment shortfall of about $3 billion a year.

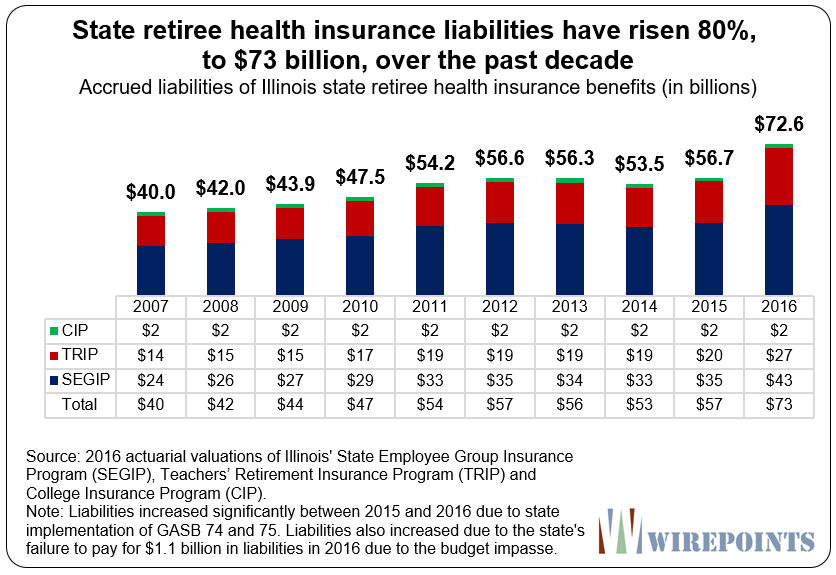

Those yearly shortfalls, along with recent changes in accounting, have pushed up Illinois’ retiree health insurance debt to $73 billion.

The rising shortfall matters since the annual pay-go cost of retiree healthcare is growing rapidly. By 2025, the pay-go amount will total $3 billion a year. By 2032 it will exceed $4 billion.

In total, the pay-go amounts will grow by 5 percent annually through 2045. The state has nothing set aside to take any of that additional pressure off of the budget.

Illinois is not alone in treating retiree healthcare as a pay-as-you-go cost. Fifteen states have absolutely nothing set aside to pay retiree healthcare. And over two dozen more have less than a quarter percent of the money they need set aside, according to data collected by the Pew Charitable Trusts.

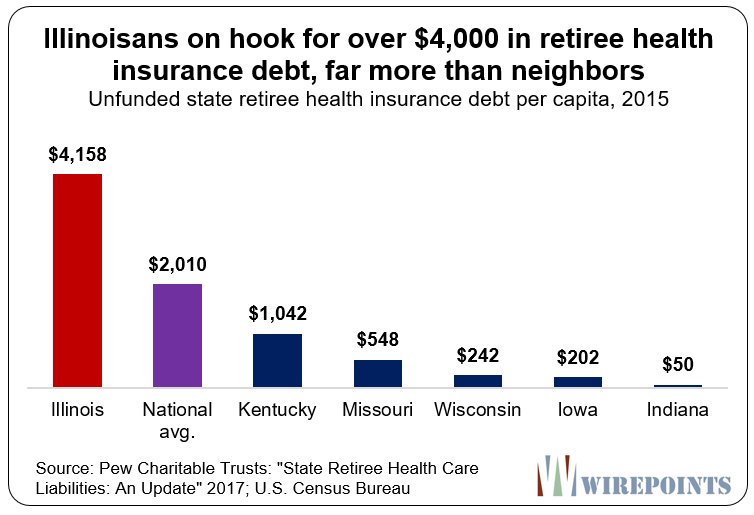

But the extent of underfunding is extreme in Illinois. That’s particularly true when comparing the unfunded retiree health care debt per capita in Illinois versus our neighboring states.

As of 2015, each Illinoisan was on the hook for more than $4,100 in unfunded retiree health benefits, the 6th-most in the nation. That amount is double the national average and quadruple what Kentuckians owe. And it’s many, many times more than what residents in states like Wisconsin and Indiana are burdened with. It’s another debt that makes Illinois noncompetitive vis-a-vis its neighbors.

But that’s based on older numbers. As of 2016, Illinoisans are burdened with $5,700 each in state retiree health insurance debts. That’s more than $15,000 for every household in the state. (Liabilities increased significantly between 2015 and 2016 due to state implementation of GASB 74 and 75. Liabilities also increased due to the state’s failure to pay for $1.1 billion in liabilities in 2016 due to the budget impasse.)

The total cost of state retirements

When you add up what Illinois owes in pension and retiree health debt – valued under more realistic assumptions – it becomes crystal clear that Illinois’ situation is far more dire than currently reported by the state, the media or rating agencies.

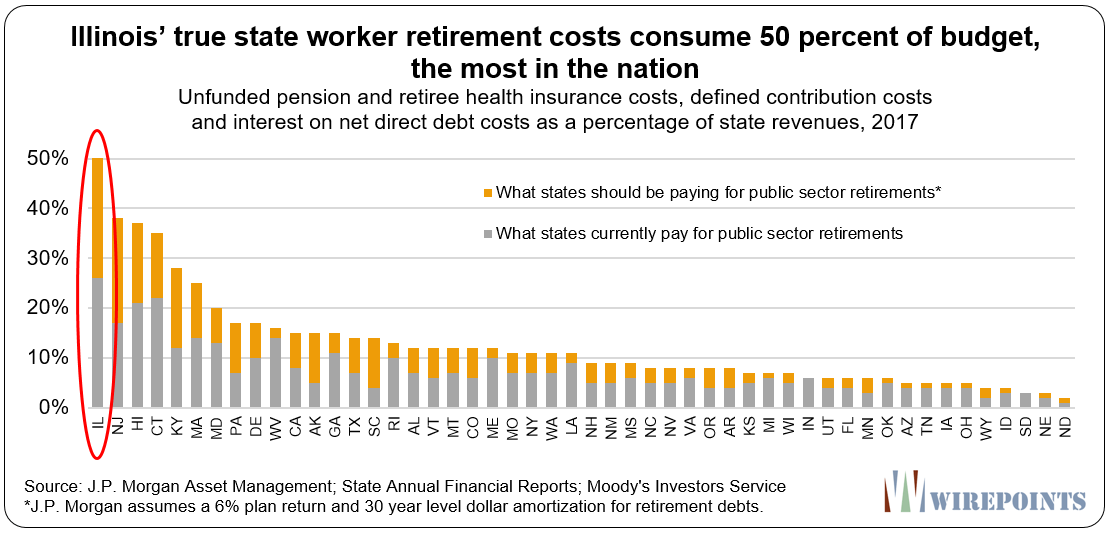

J.P. Morgan recently looked at the amount states should be paying toward pensions and retiree health care to be actuarially sound – as opposed to what states currently pay. They found Illinois to be the outlier nationally, with more than 50 percent of its budget needed to reach an actuarially sound position.

By comparison, 37 states need only 15 percent or less of their budgets to be considered sound.

Conclusion

J.P. Morgan’s assessment is another profound indicator of just how bankrupt Illinois has become. It’s untenable.

And that analysis doesn’t even include Chicago’s $71 billion in pension shortfalls (Moody’s estimates), as well as tens of billions more in other local government retirement debts.

This mess is the result of handing out unaffordable benefits at all levels of government for decades. The state alone has allowed total pension benefits to grow over 1,000 percent over the last 30 years – a pace far faster than taxpayers could ever afford.

Layer on top of that free and heavily subsidized health insurance benefits and it’s no wonder Illinois faces one of the most extreme crises of any state in the nation.

Barring massive reforms that reduce those liabilities, expect everyone in Illinois to lose.

Download a PDF copy of the report

Read more about Illinois’ state and local public retirement crisis:

- Illinois state pensions: Overpromised, not underfunded

- Overpromising has crippled public pensions: A 50-state survey

- Beyond Harvey: Many Illinois municipalities running out of options

- $125,000: The pension debt each Chicago household is really on the hook for

Read all of Wirepoints’ major work on pensions here.

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

Question: Noticed this clause in the D211 contract regarding post-retirement healthcare coverage. Is this tracked as a liability on the school district books? Also, how does this play into your OPEB calculations?

“A certificated unit member will receive a yearly contribution of three thousand dollars ($3,000) toward the cost of health insurance until eligible for Medicare. Payment will be made in lump sum payments each year until eligible for Medicare. Except as allowed in paragraph E, retired certificated unit members are not eligible for health insurance benefits through District 211.”

Two questions: 1) Do the annual cost figures referenced in one of the charts above, that start out at around $1.5 billion in 2018 and peak at around $5.5 billion in 2045, apply only to retired employees, or do they include active employees as well? If it is the latter then these figures are misleading, because virtually all large firms in the private sector also provide health insurance to their active employees. In other words, even if the state completely eliminated retiree health insurance, the majority of these costs would still be incurred to provide health insurance for active employees.… Read more »

1. The above numbers only apply to retiree health insurance benefits. The state’s payment of healthcare costs for active workers is a separate expense that’s also generous. Active state workers receive Cadillac health care benefits – the state pays subsidies equal to about $15,000 per worker a year. To read more about the healthcare subsidies provided to active state workers, see: https://wirepoints.org/six-facts-pritzker-cant-ignore-when-negotiating-afscme-contract/ 2. Yes, the actuaries take all sorts of assumptions into account to calculate future payments and the AL, including the future “on-Medicare” membership. And don’t forget that new workers join every year at the same time as retirees… Read more »

If those figures are just for retiree health insurance, then I agree with you that it is a lot of money for the state to pay. One mitigating factor, though, is that employees who are encouraged to retire at 55 or 60 knowing they have a bridge to Medicare will probably do so with lower pensions than if they worked the additional years to age 65. So if, despite the Kanerva ISC ruling, you could cut or eliminate retiree health insurance, you would effectively force many older workers to stick it out through age 65 and this would have other… Read more »

Andrew – Your assumption that retiring earlier with a lower pension saves money is incorrect, especially if those retiring early have reached full vesting, which is usually the main driver to begin retirement. Although a person retiring at 55-60 will indeed have a smaller yearly pension than the person retiring at 65 (assuming consistent salary increases year-over-year), the 60 year old retiree will withdraw more from the pension system over a lifetime. There are a number of variables in play (retirement age, lifespan, raises, etc), but typically you’d need very large yearly raises and a very long lifespan (well into… Read more »

Option 1: Leave Illinois and improve your family’s well being and quality of life

Option 2: Stay in Illinois and enduring great pain/suffering and have your family’s lives ruined.

The choice is clear and simple.

Illinois is one big GameStop, that just lost $500 million in the last quarter. GameStop’s model is to pay $8 or less for used video games, or $12 in store credit. Illinois has a simpler cash flow gimmick–kick the can and make promises to workers that will never be kept.

Vouchers d

For insurance and care for health care in place of their insurance. They keep what they don’t spend

Time to cut all pensions down to equivalent of Social Security, including teachers. Insane to have teachers retiring with a $90,000 plus pension and administrators leaving with pensions in hundreds of thousands dollars. End pensions for new hires now.

There is a further “layer” here. Long-service employees are older and more prone to health problems. Many of them are already retirement eligible.School and university employees have tenure and are hard to off-load. My experience representing this type of employer has established that the situation calls out for “early retirement windows.” Health care costs move from school budget to pension system budget. School budget gets hit by offer of either cash or deferred early retirement incentive. But school gets to offload a high-paid burnout in exchange for two young enthusiastic replacements. Short-sighted because sometimes they need to hire the teacher… Read more »

This kind of problem is even worse than the pension problem. Because this one involves maintaining an actual cash flow to the insurance providers. Unlike cutting monthly pension checks from a dwindling pension fund. The providers are sending real bills to be paid, now. There is no actuarial deficient “fund” sittting there.waiting to run out, only cash flow. To real bills.

Worse yet: Most health “insurance” programs are largely self-insured by the employer or the pension system, with the nominal insurer acting as a clearing house for claims. Not only does the public fail to understand that payoffs from insurance companies are not really “found money” but many others do not understand that it’s likely to be a self-insured program in which premiums are simply a way to pay insurers to administer the benefits and (sometimes) actually reach into their own pockets in a stop-loss situation.

My dental insurance payoffs feel like found money because I don’t pay a lot for dental insurance. However, those payoffs are limited to $1500 a year. ( ! )

… and all this debt is growing during a time of low unemployment and a strong stock market. This is when Illinois should be drastically reducing debt. You don’t need to be genius to figure out what happens to Illinois when the next recession hits.

The unfunded liability grew $15.9B in a single year between 2015 and 2016. What do you suppose it is today?

If the state picks up most, if not all, of the insurance costs the recipients have no incentive to use the benefit wisely. This, along with ever increasing medical costs well above the rate of inflation, will cause this liability to explode.

They used a 2.85% discount rate in 2016. The Unfunded Liability will be a little lower in 2017 because rates went up to over 3 percent. So it will be down a couple of billion. But is am assuming they don’t make major changes in health care cost assumptions. If those change, that, too, will affect the liability.

Thanks Ted. Great article BTW. Please consider putting a warning label on these as they tend to cause extreme irritability and general distress.

Which begs the question: Why use different discount rates for pensions and healthcare if the investment mixes are similar?

Which begs a bigger question: Why use discount rates if there is no money invested at all?

The media does a poor job when it comes to covering public finance in Chicago and Illinois. I think some of it is due to bias as by and large reporters share the same world view as those who want to maintain the status quo. But I think the biggest culprit is the education system, which produces innumerate graduates with regard for emotions and narratives but not much concern or facilty with math. This having been said, I don’t think Wirepoints’ work is unnoticed, as it gives fabric to what so many are observing in Illinois. There a remains a… Read more »

Public employees should be transferred to the ACA not the Cadillac plans offered to them at taxpayers expense. It is easy to offer someone anything as long as someone else pays for it. No one knows future healthcare cost due to unknown variables such as life expectancy and prescription drug costs which are going thru the roof so $73 Billion may be conservative. But I guess taxpayers have unlimited resources?

watch the you-tube vid “cities in financial straits weigh bankruptcy, PBS”. That former cop in Vallejo kept his pension but lost his heath insurance which he now has to pay $700 a month for. If it sounds too good to be true, (like lifetime free healthcare) — well, you know the rest.

This can be fixed easily. Simply issue a healthcare obligation bond (HOB) today for $30B or so, re-amortize the insurance costs to smooth out the payments over time, make the full ARC payments every year, and voila…fully funded retiree health care. Oh wait…

Look at the tiny debt Indiana taxpayers have.

Another reason we are glad to live here in America’s fiscal responsibility capital.