Beyond Harvey: Many Illinois municipalities running out of options

By: Ted Dabrowski and John Klingner

Harvey, Illinois, was the first municipality to have its tax revenues garnished by the state comptroller for failing to fund its local pensions. North Chicago followed shortly after.

Many more Illinois cities could face garnishment as the result of the same law that was applied against both cities. A Wirepoints analysis of Department of Insurance data found that nearly 400 of Illinois’ 650 downstate public safety pension funds did not receive their fully required pension contributions in 2016, meaning more than 200 municipalities failed to meet their obligations.* A cascade of intercepts could bring even more chaos to Illinois’ dire fiscal situation.

But tax intercepts in Harvey are not the real story. The real story is what’s happening on the ground in many municipalities across the state.

In too many communities, pensioners’ retirement security is being wiped out. Homeowners’ equity is being destroyed. Businesses are being driven out by taxes. And cities are cutting back on services. Nobody is winning; everybody is losing. The negative impact of the broader downstate pension crisis can’t be overstated.

Wirepoints has performed an analysis of 180 Illinois cities with both a dedicated police and fire pension fund, examining their finances and their pensions. The findings, which will be released in a forthcoming paper, are alarming. Over the past 13 years – the time period for which individual pension fund data is available – finances have worsened dramatically in cities across Illinois.

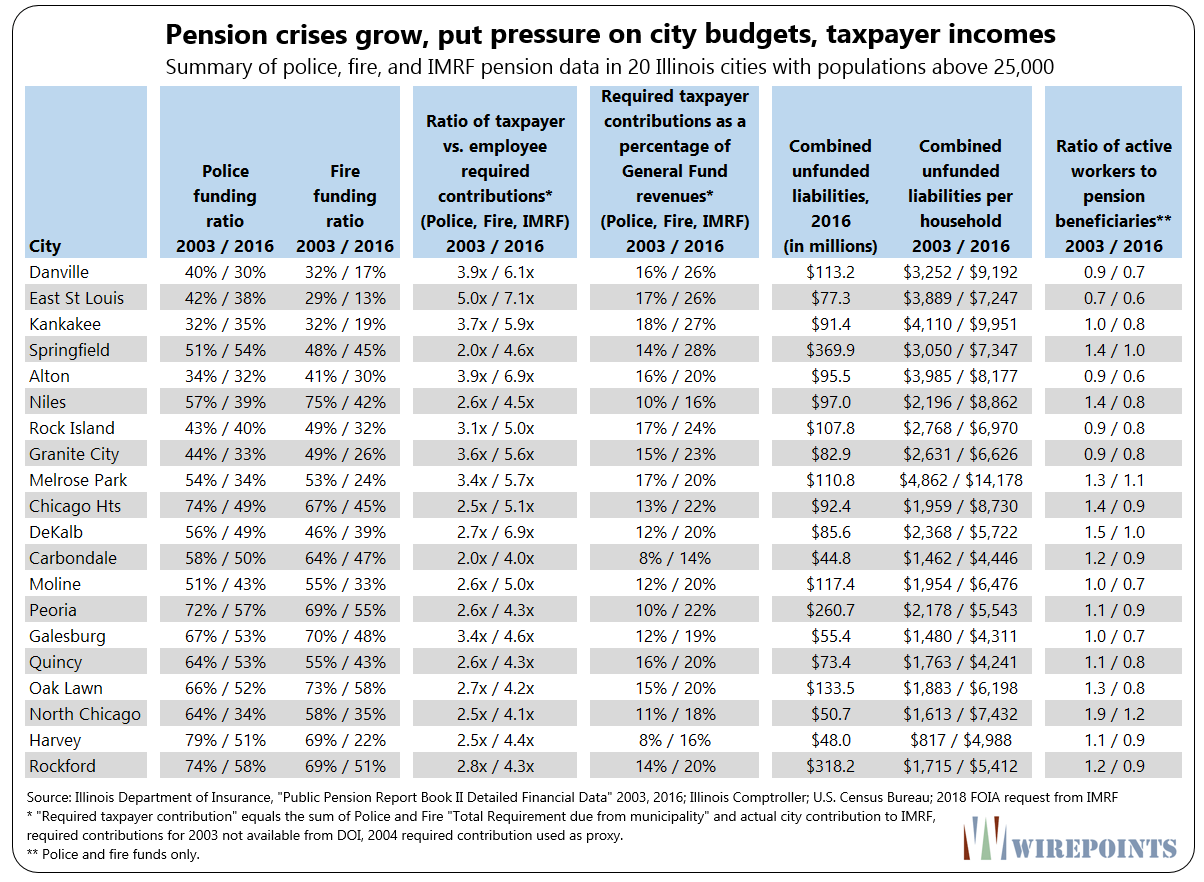

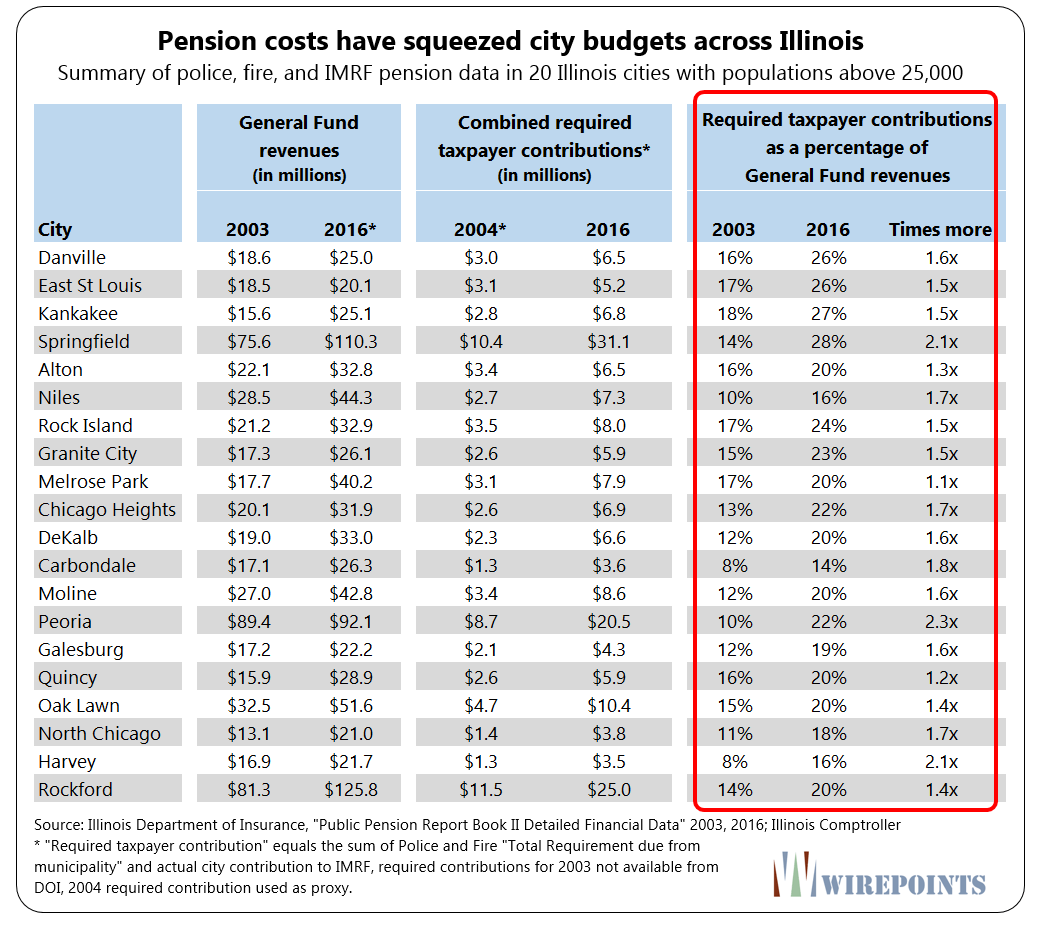

Listed below are a sample of 20 cities with populations above 25,000 where pensions are wreaking havoc and putting pressure on city budgets. Overall, their funding ratios have either collapsed or remained near-insolvent. Many cities will see 20 to 25 percent of their general budgets consumed by pension costs next year. And taxpayers are putting in far more toward pensions only to watch their systems’ funding ratios fall.

Little to nothing is being done to fix the crises. Local officials lack the power they need to make the effective changes that could help turn their communities around. And the state, which sets all the mandates that handcuff communities, refuses to hand over control to localities.

Illinois cities need major reforms immediately – from changes in retirement benefits to a roll back in collective bargaining mandates. A recent in-depth Wirepoints analysis of Danville captured much of what’s needed to turn Illinois communities around. But for those cities that are beyond reforms, like Harvey and East St. Louis, bankruptcy may be the only tool left that can protect retirees, residents and vital government services.

More than just Harvey

The dire situation of Illinois’ cities was made more real when the state comptroller intercepted Harvey and North Chicago revenues on behalf of their local pension funds. It demonstrated a simple fact that’s gone unacknowledged: Illinois cities are reaching a breaking point.

In most cases, the promises granted to workers have grown so much that cities have been forced to choose between funding pensions and funding basic operations. Or between funding pensions and paying for their workers. Or between funding pensions and taking care of their roads.

Harvey fired 40 public safety workers in response to the comptroller’s intercept. But plenty of other cities have had to make hard choices. Granite City has taken out loans to pay for pensions and has laid off four police officers and seven firefighters. Springfield previously laid off police and fire workers, closed public libraries and cut public works employees. Some communities have gone so far as to start selling assets to make their pension payments. Alton is selling its water treatment plant in order to afford its pension payment this year.

And in Danville, city officials have enacted a “public safety pension fee” that could amount to economic suicide. Simply hiking taxes without changing any of the systems that drive up the cost of pensions won’t fix the problem. It will only drive more people away.

To get a full picture of how dire the situation has become, Wirepoints looked at several different metrics related to both downstate pension funds and how they’re impacting municipal finances and residents. Wirepoints compared downstate public safety pension data from fiscal year 2016, the most recent data available from the Illinois Department of Insurance (DOI), to fiscal year 2003, the earliest year that individual pension fund data is provided by DOI. Illinois Municipal Retirement Fund data for 2003 and 2016 was provided via FOIA request from IMRF.

Harvey reached the end of the line first because it’s one of the state’s worst-off communities; its depressed economy and endemic corruption played a vital part in its downfall. But look at the numbers – at the collapsing funding ratios, broken budgets, and unsustainable tax burdens – and anyone can see that many cities aren’t far off from breaking points of their own.

It’s important to remember that taxpayers are burdened with far more than just their own city’s pension debts. Those same taxpayers are also stuck with the state’s own $130 billion pension crisis and $56 billion in retiree healthcare debts. School districts impose another $21 billion in debts of their own. And residents of Cook County are burdened with another $7 billion in pension debts on top of all that.

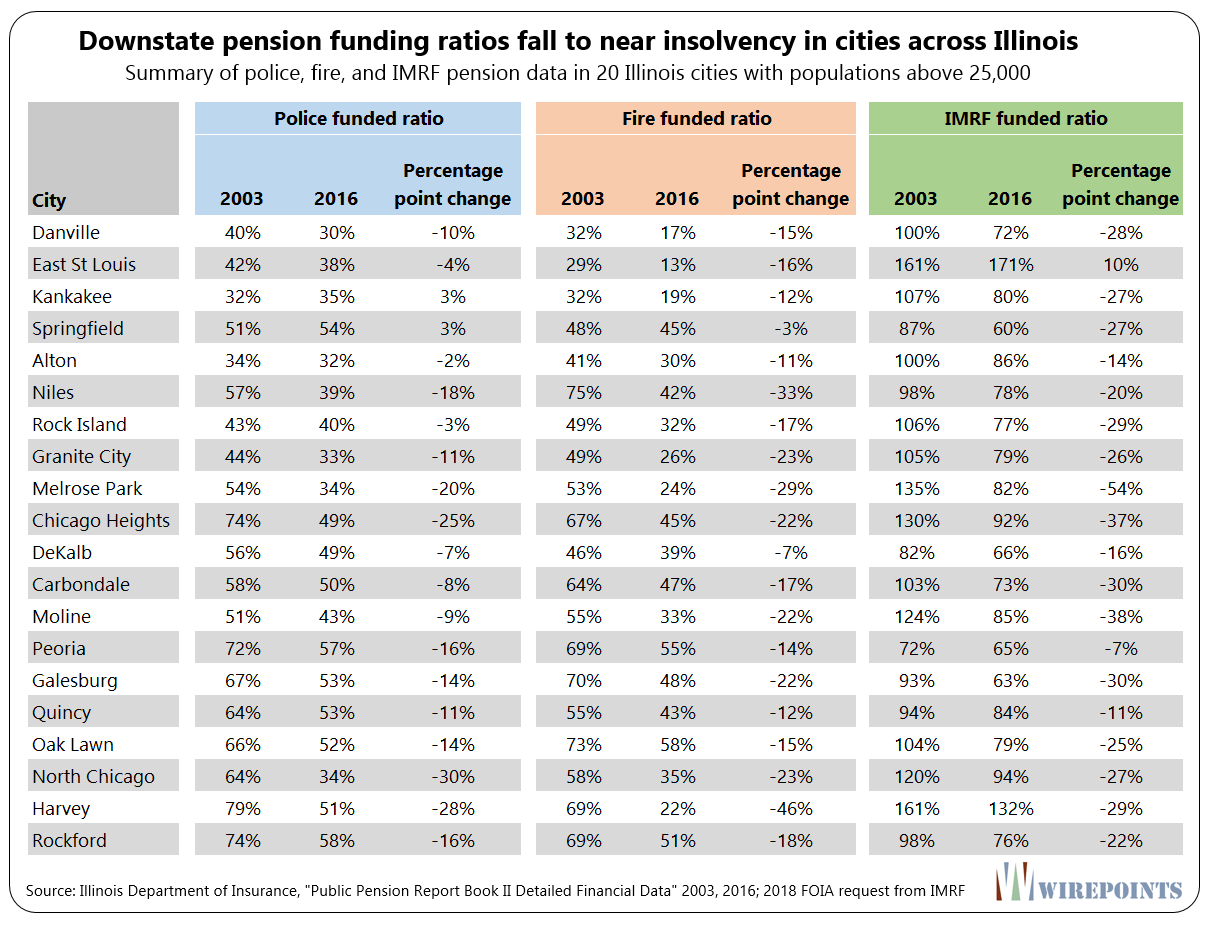

Funding ratios fall toward insolvency

The funded ratio of a pension plan is one measure of how healthy a pension fund is. The ratio simply looks at how much assets the fund has on hand today compared to the present value of the total benefits it has to pay out in the future.

Collectively, downstate police and fire pension funds owe $23.4 billion in benefits but have only $13.4 billion on hand to pay for them. In other words, public safety pensions are just 58 percent funded and have a $10 billion shortfall.

The U.S. Federal Employee Retirement Security Act (ERISA) requires pension systems in the private sector to be 100 percent funded. The rule for the public sector should be no different. The further a pension falls from 100 percent funding, the harder it is to get back to it.

Unfortunately, a vast majority of downstate police and fire pensions are badly funded. Nearly 30 percent of downstate public safety pension funds have less than half the money they need on hand today to pay out future benefits. More than half are less than 60 percent funded. If any of these funds were operated in the private sector, they would have already been declared insolvent many times over by now.

Worse, many cities’ police and fire funding ratios continue to stagnate or even fall despite the recent period of stellar stock market returns.

Chicago Heights’ police fund went from 74 percent funded in 2003 to less than half funded in 2016. Harvey’s fire fund collapsed nearly 50 percentage points over the same period. And Danville’s fire fund fell 15 points, to near total insolvency. It has only 17 cents on hand for every dollar it needs to pay out future benefits.

Even funding of Illinois Municipal Retirement Fund (IMRF) pensions have declined. Pension contributions to IMRF are prioritized by law, yet funding has fallen far below 100 percent in many localities. Of the cities below, 11 have seen their IMRF funding fall below 80 percent.

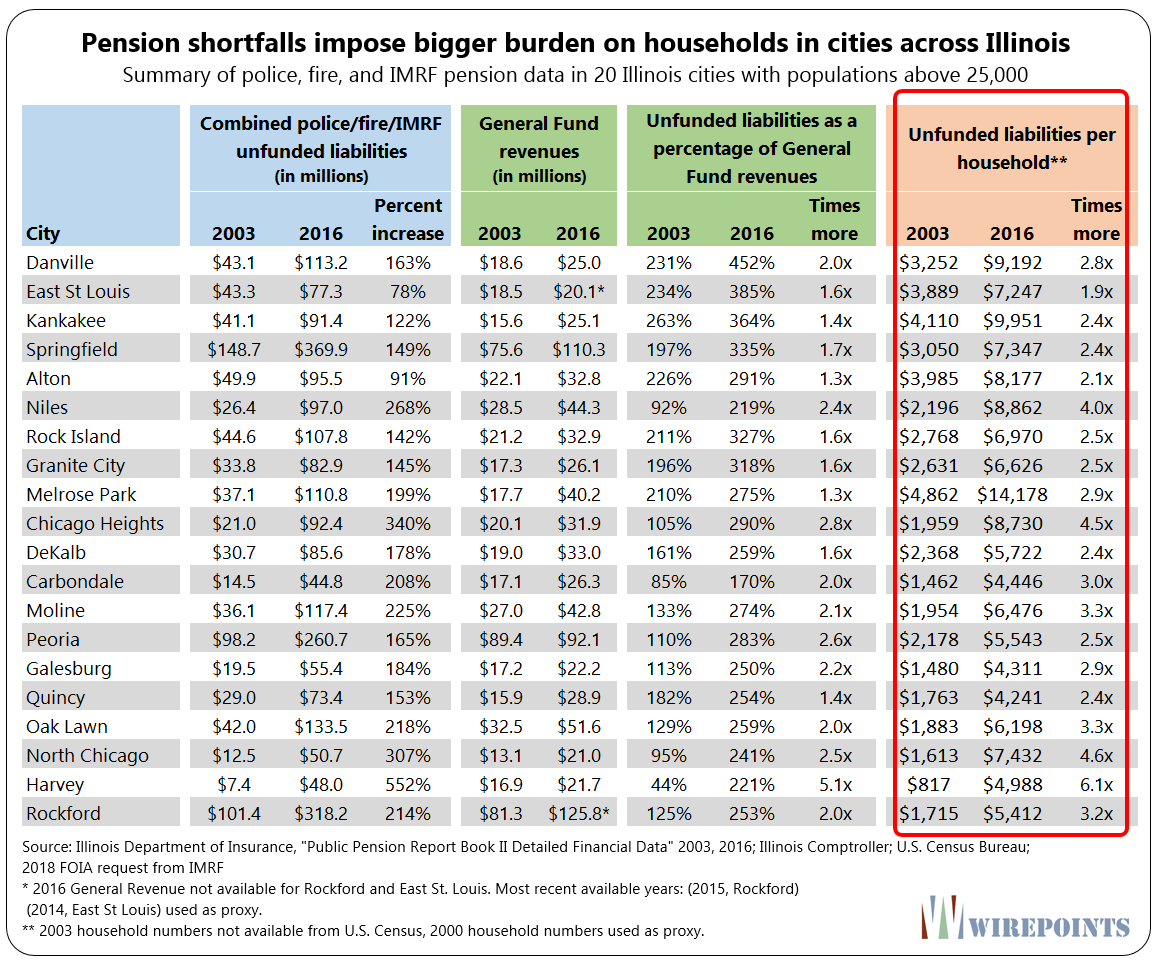

Pension shortfalls per household jump.

Wirepoints also looked as how much pension debt each city has amassed per household as a way to measure the growing burden on residents.

The burden of cities’ unfunded liabilities won’t fall on active employees as their contributions are fixed by law. And the debts are unlikely to be paid off by investment returns.

So taxpayers on the hook. And the debt they’re on the hook for has grown considerably over the past 13 years. In Danville, pension debts per household tripled between 2003 and 2016, to more $9,000. Harvey households are on the hook for nearly $5,000 in unfunded liabilities, six times more compared to 2003.

And households in Melrose Park saw their debt burdens triple, to a massive $14,000 in 2016.

Residents tapped out

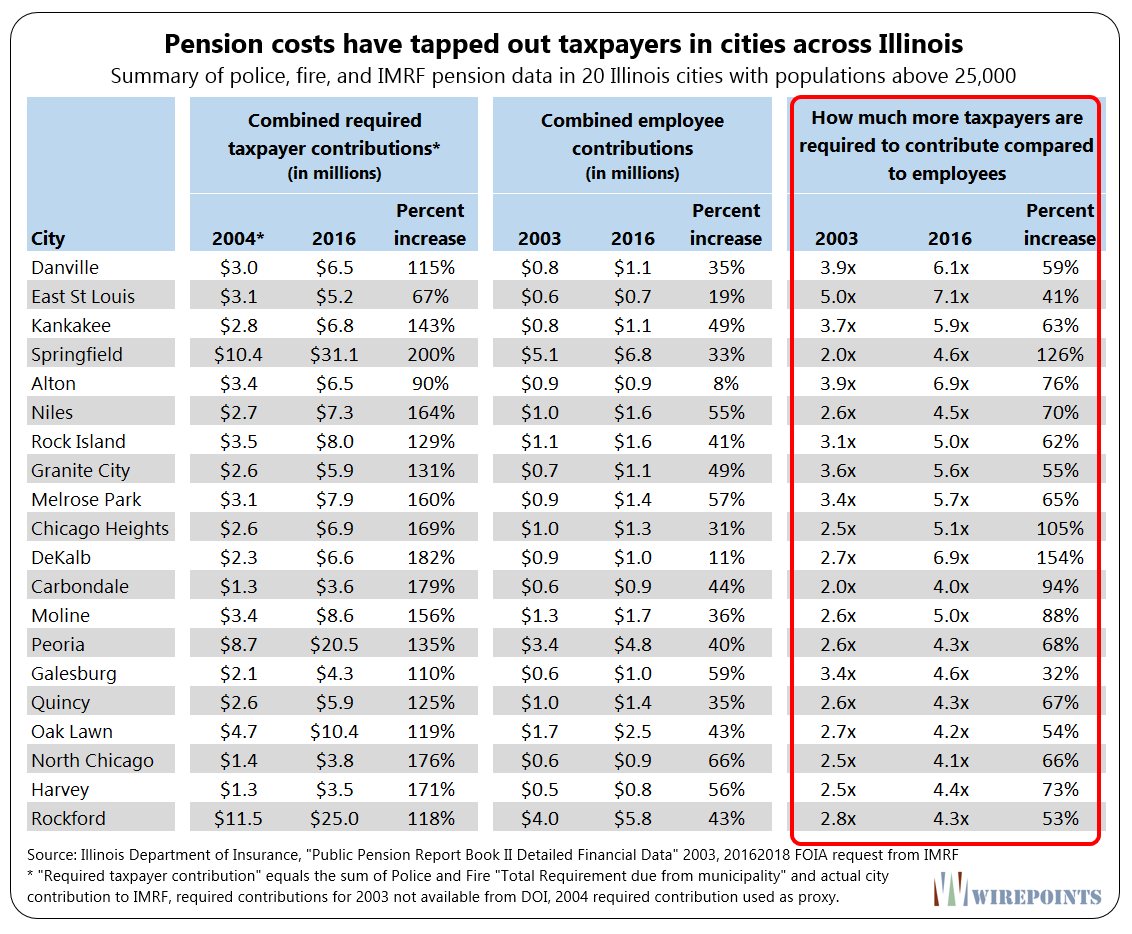

Taxpayers in many cities are tapped out. Illinoisans already pay the highest property taxes in the nation. Yet pension costs continue to rise every year, regardless of whether or not residents can afford it.

Wirepoints measured how tapped out residents are by looking at how much they are required to contribute to pensions compared to the contributions of active city employees.

In 2003, taxpayers were already contributing twice as much to local pensions as employees in cities like Carbondale and Springfield. Now taxpayers are contributing 4 times and 4.6 times more, respectively.

DeKalb taxpayers have it the worst. Taxpayer contributions have grown more than 180 percent since 2003. Residents now contribute 6.9 times more to the city’s pension funds than employees do.

Budgets getting squeezed.

Pension costs are draining local finances. As city spending on pensions increases, the portion spent on everything else – from public safety to social services to roadwork – falls.

Wirepoints measured the impact of that crowd-out by looking at each city’s required pension contributions as a percentage of General Fund revenues.

Many cities are spending the equivalent of a quarter or more of their general revenues on pension contributions. In Kankakee, pension contributions take up 27 percent of general revenues. And in Peoria, pension costs consume 22 percent of the city’s budget, more than double what they consumed in 2003.

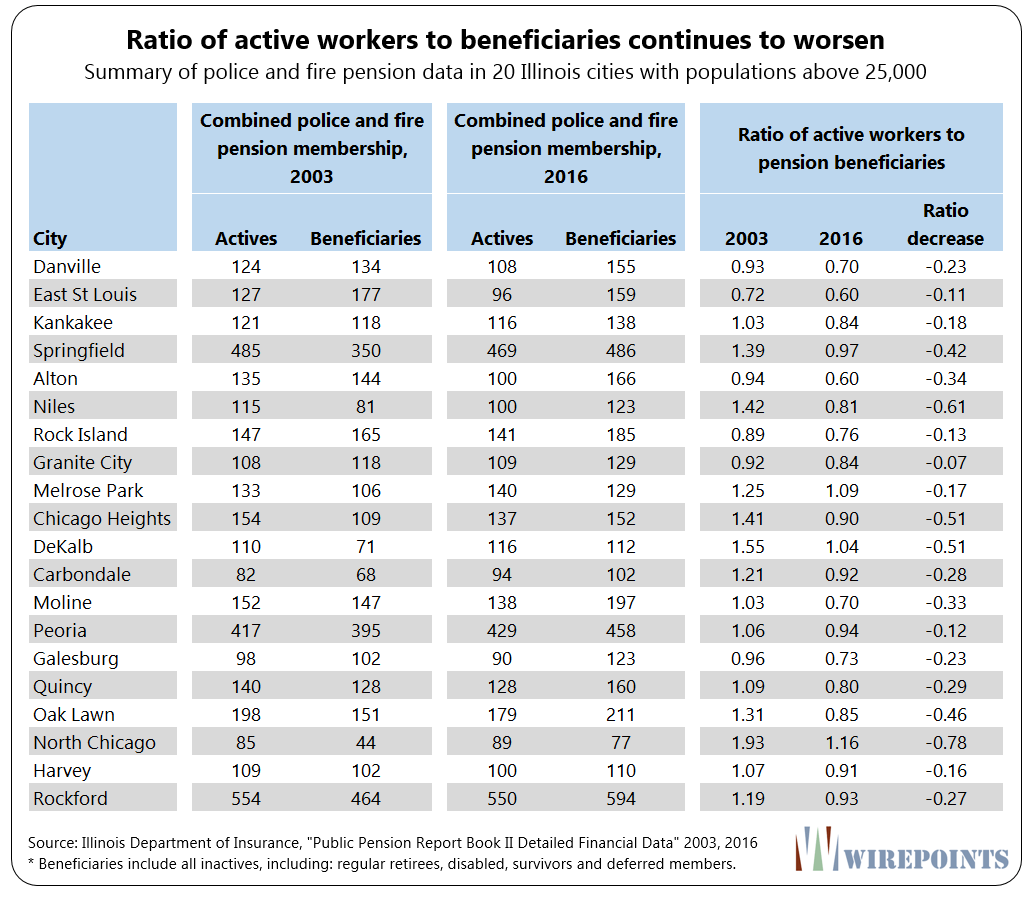

Less active workers, more beneficiaries

Looking at the number of active participants compared to beneficiaries is another measure of pension health.

Unfortunately, under that measure too many public safety pension funds are sick. Many Illinois cities now have more beneficiaries drawing pension benefits than active workers contributing to the pension funds. In fact, of the 20 cities below, only three still maintain a positive active-to-beneficiary balance.

In Niles, the active/beneficiary ratio fell 61 percent between 2003 and 2016. In 2003, there were 1.4 active workers for every beneficiary in Niles. By 2016, the ratio had fallen to just 0.81.

Of the 20 cities, Alton is worst off. Its ratio fell to 0.6 in 2016 from 0.94 in 2003. That means the city has just 6 active workers for every 10 beneficiaries today.

Overpromised, not underfunded

Most critics of the pension crisis will be sure to blame local politicians – and by extension city residents – for underfunding municipal pensions.

But the reality is that the growth in pension promises have been so extreme that local politicians were put in a no-win situation.

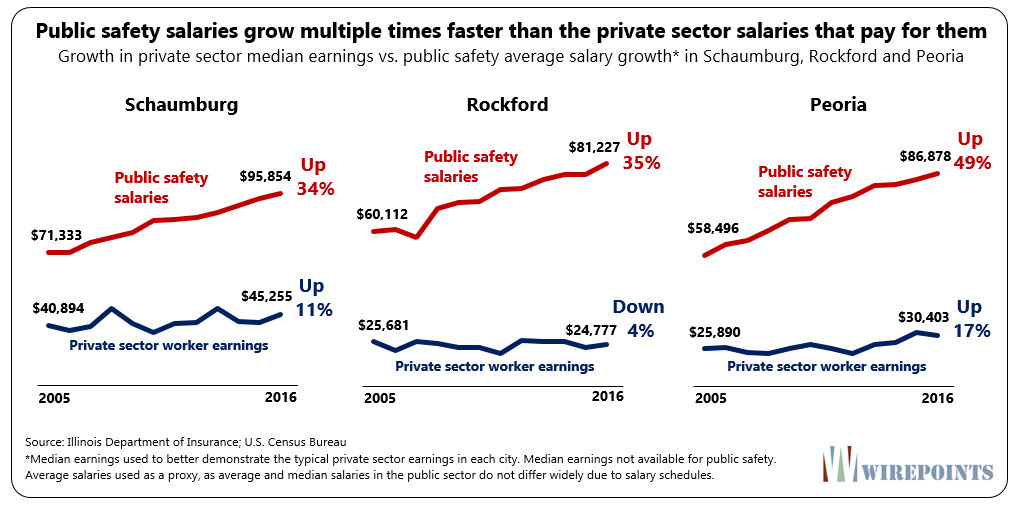

For three decades they’ve been forced to choose between funding out-of-control pension promises vs. local operations and salaries. Since pension funds were largely out of sight, salaries were prioritized. In many cases, they’ve grown far faster than the earnings of the city residents that pay for them.

And those salary increases, in turn, made pension promises even more costly. The last decade – when the downstate pension crisis was already in full swing – bears that out. Public safety salaries in most cities have far outpaced that of the earnings growth of the residents that pay for them.

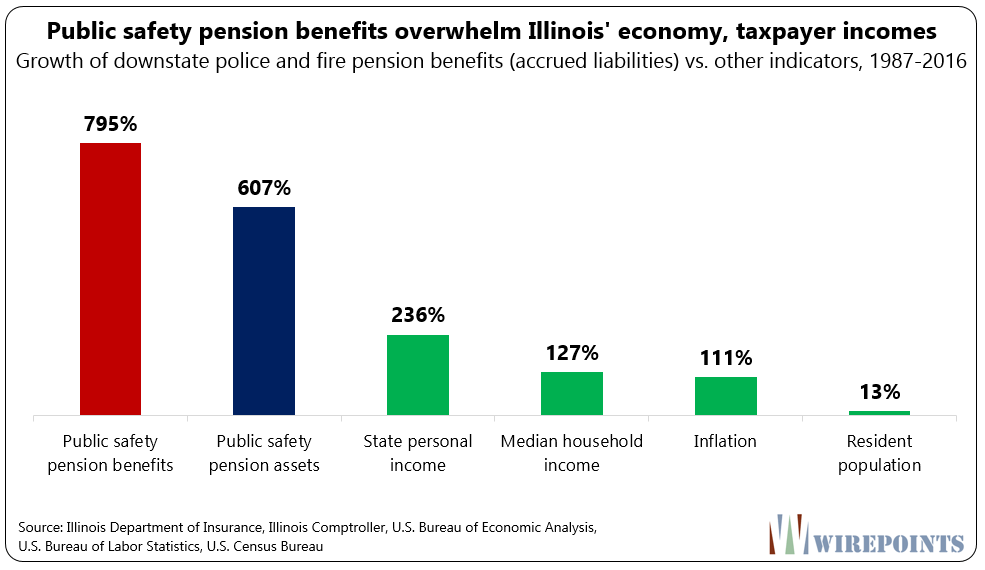

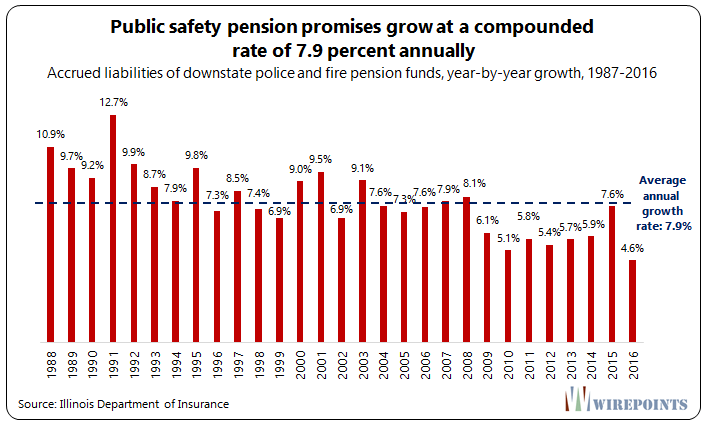

A look at the growth in total owed benefits across the state shows just how much those promises have skyrocketed over the past three decades.

In 1987, municipalities owed a total of $2.6 billion in benefits to public safety workers and retirees across the state. Today, that number has jumped to $23.4 billion. That’s nearly an 800 percent increase.

Those total owed pension promises have grown at a pace that’s swamped local economies, inflation and household incomes. Inflation has risen by just 111 percent and household incomes by 127 percent over the past 30 years.

Pension promises have been growing at an extreme pace year in and year out for more than 30 years. On average, benefits have grown 7.9 percent a year.

Growth has slowed slightly over the past decade – to an average of 6.2 percent a year, still more than three times the rate of inflation – but the damage has already been done. Cities and taxpayers could never afford to pay for promises that have compounded like that.

But it’s not as if local communities didn’t try to keep up. Public safety pension assets managed to grow more than 600 percent over the period, way faster than any other indicator as well. No matter how fast assets grew, however, they weren’t enough to both make up for previous underfunding and the increase in promised benefits.

The rapid growth in pension promises has finally caught up with cities. Each city’s situation is different, obviously. Some communities have had better investment returns, more realistic actuarial assumptions, have contributed more and maintained better funded ratios than others. But in the end, most have been unable to keep up with their pension promises. Cities have started to run out of options.

Worse yet, cities like Harvey, North Chicago and East St Louis have hit a point of no return. Their costs have gotten so out of control that they’ve been using their pension assets to pay out annual benefits.

Harvey is effectively bankrupt

Harvey is out of options. It has no more assets to sell. It can’t raise any more money. Its tax base is tapped out and more than 4,000 property tax bills have gone unpaid – the most for any city in Illinois. Effective property tax rates are already at nearly 6 percent of home values, and that’s being generous. Most homes aren’t worth what the assessments say they are worth.

In virtually every way, Harvey is already operating as if it were in bankruptcy – only it’s choosing the terms.

To get around its fiscal shortfalls, Harvey is already defaulting on its bond payments. The city has not made its required pension contributions for a decade. Now it’s laying off police and fire employees, cutting public safety services at precisely the time it will need even more of them.

The problem is, this type of self-imposed bankruptcy is disorderly, unfair and chaotic – especially for small communities that don’t have influence in Springfield.

The roots of Harvey’s problems are the same ones driving cities and towns all across Illinois into crisis. Harvey just managed to get to the end of the path first because of its particularly deep economic plight and criminal mismanagement. But many others are all stuck on the same path, dealing with the same impossible pension math.

If Illinois cities are to get out of their impossible situation, that has to change.

That means giving municipalities the power to bring city retirement benefits in line with what their residents can afford. It means empowering local leaders to alter collective bargaining agreements to bring labor costs in line and make labor rules more fair. It means ending state-level mandates like prevailing wage rules and reforming expensive systems like workers comp.

But for many cities, the time for structural reforms have probably passed. For those communities, bankruptcy, if their particular circumstances are right and if it’s not already too late, is the only option that can protect retirees, restore financial stability and assure basic services.

*Unlike cities and their dedicated public safety departments, the 100 firefighter pension funds operating under Fire Protection Districts will have a much harder time benefitting from the intercept law.

Read more about the crisis here:

Chicago Fed’s Answer For Illinois Pension Crisis Is A Statewide Property Tax!

Why a bankruptcy option for municipalities is essential

Second domino falls in Illinois: North Chicago revenues garnished for pensions

Harvey, the first domino in Illinois: Data shows 400 other pension funds could trigger garnishment

Audio and summary

Audio and summary  If this bill passes, say goodbye to local control over all Illinois parks and expect to see open drug and alcohol use, needles, no sanitation and fire hazards, but no ordinary park users.

If this bill passes, say goodbye to local control over all Illinois parks and expect to see open drug and alcohol use, needles, no sanitation and fire hazards, but no ordinary park users.

Legalize Weed. Take the money and fix pot-holes. Call it operation pothole. Then tax the UFO’s. Who do they think they are!!! Zooming around our beautiful state not paying a dime I might add. For thousands of years UFOS have been abducting Illinois citizens and the UFO’s never paid into the tax system. BS just because the flying saucer don’t touch the ground the aliens have NEVER paid property taxes!! Think about it. That’s who to blame aliens!!! Aliens caused the short fall. I want to see lincense plates and city stickers on ALL ufo’s operating in the state. Then… Read more »

Bruce Rauner and his Republican fiends like Corey Lewandowski, David Bossie, and Dan Bongino are destroying the state of illinois for their own political gain.

As Danielle DiMartino Booth points out in her book,Fed Up: An Insider’s Take on Why the Federal Reserve is Bad for America, the Fed is controlled by a cabal of over 1,100 Ph.D economist academics who live in a theoretical hall of mirrors echo chamber,and who disregard those that lack such academic credentials from a handful of universities. These people live in a theoretical world of thought experiments. Weimar Ben Bernanke admits in his memoir, he was a naive patsy for Wall Street banksters. EXCERPT from Ben S. Bernanke’s The Courage to Act:A Memoir of a Crisis and Its Aftermath… Read more »

How about reporting on YEARLY payouts and income for the pension funds. No one has 100 percent of their food budget saved up for example. Oh, don’t forget the rolling economic depressions since 2001.

It’s an increasingly delicate problem because we need public safety offices to preserve order as the system crashes. The price for maintaining public order in the face of imminent disorder is like the price of plywood when the hurricane is close by. Cutbacks in cops will bring forth more thieves and thugs. Many have seen this coming. It’s long been an implicit threat when public safety unions go to the bargaining table. Few politicians dared risk the consequences of saying no. Can kicked; problem postponed. Now what?

Hire private cops like in the movie “Robocop”. Didn’t Camden, NJ do that?

Ronald Regan had a GREAT respond when similarly threatened by the Air Traffic Controllers. He FIRED all of them.

Were must NOT give in to the financial extortion from Police Unions/workers, and if the Police strike (formally or through job actions) they should be fired. In an emergency, the National Guard could be called in to maintain order while new Officers are trained

Well, T.L.’s suggestion is worth a try if the negotiator for the city has enough testosterone patches. The city would probably have to wait until the current collective bargaining agreement expires and then deal with numerous legal distractions while the various mandatory arbitrations and injunctions and court appeals were ongoing. In my home town the usual response to any hint of backbone was to pack the city council chamber with blue uniforms shuffling their feet and glaring at the citizens’ elected representatives. Same result if the matter went to court — a couple sheriff’s deputies trying to preserve decorum while… Read more »

Governor Bruce Rauner has really let the people of Illinois down.

Thank you Bruce Whiner for raising our taxes.

The Trump Tax Cuts are ruining Illinois.

Thank your democrats in office.spend,spend.Remeber this at the voting booth.

Greed HAS consequences.

The ludicrously excessive pension (AND benefit) promises need to be reduced by 50% to 75%………. including those already retired.

Or, you (yes YOU, Public Sector workers) can just watch as your Plan’s assets run down to ZERO.

And at the same time cities like Aurora are awash in taxpayer subsidized building sprees. From the fox valley park district expansion, to yet another renovation of the water street mall, to a rehab of the old Copley….all on the taxpayer. crony capitalism at its best. Formula: step 1 developers elect theri boy to office step 2 import poverty and crime step 3 declare areas of you city impoverished and blighted step 4 collect state, federal, county dollars to fund rehabilitation of blighted areas step 5 redistribute tax dollars to the private sector developers who put you in office step… Read more »

Cities should look to Eddie Lambert of Sears for an example of an orderly retreat. He is closing stores and selling brands and investing some money to possibly save a few stores. But there’s this idea that cities are not a business. This you-tube interview with a CalPERS spokesman doesn’t inspire confidence. Brad Pacheco comes off as a little bit of a jerk. Loyalton managers probably had no idea that CalPERS keeps two sets of books, one with the real numbers and one with the fake numbers.

https://www.youtube.com/watch?v=F2T9WVyWMMQ