By: Ted Dabrowski and John Klingner

Chicagoans are buried under so much pension debt it’s impossible to see how their city can avoid a fiscal collapse without major, structural reforms. The futility of paying down those debts becomes obvious when you try to figure out just who’s going to pay for it all.

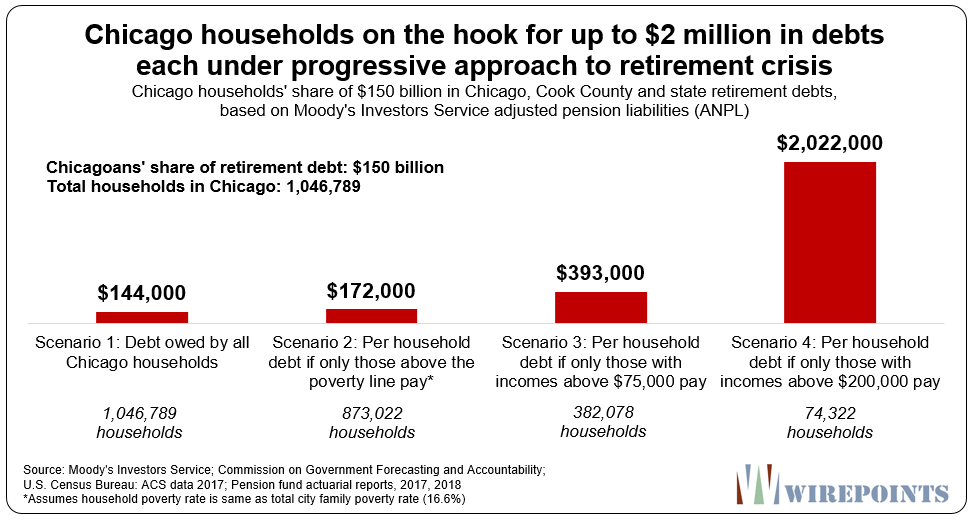

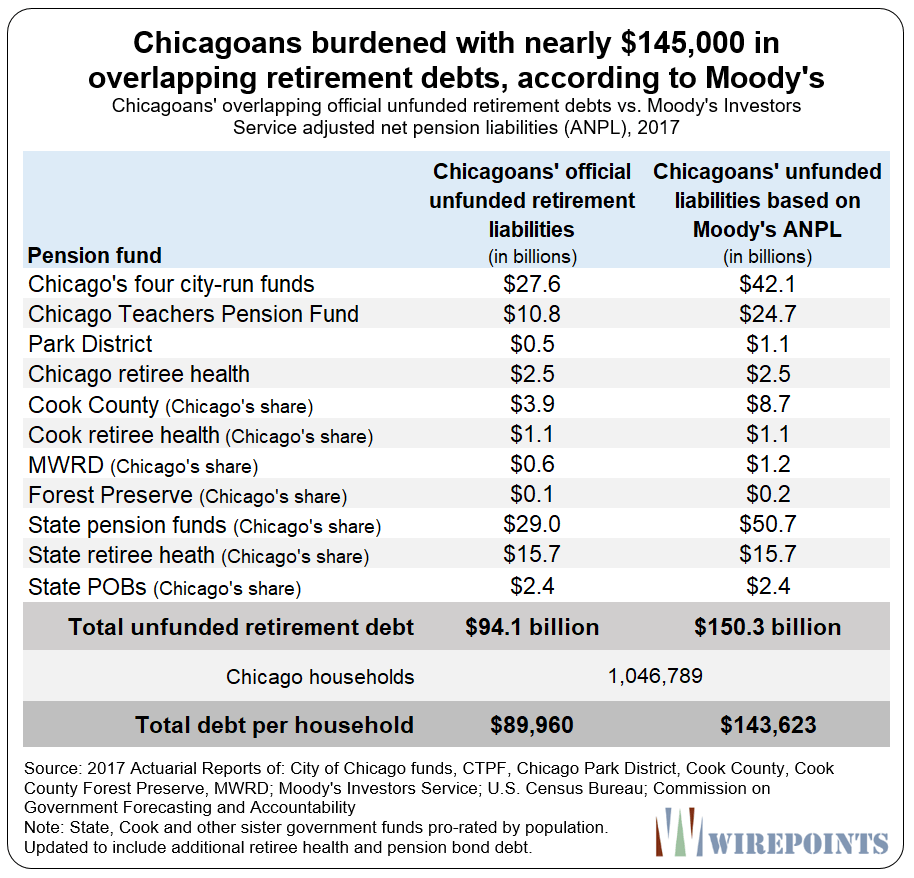

The total amount of city, county and state retirement debt Chicagoans are on the hook for is $150 billion, based on Moody’s most recent pension data. Split that evenly across the city’s one million-plus households and you arrive at nearly $145,000 per household.

That’s an outrageous amount, but it would be a clean solution if each and every Chicago household could simply absorb $145,000 in government retirement debt. The problem is, most can’t.

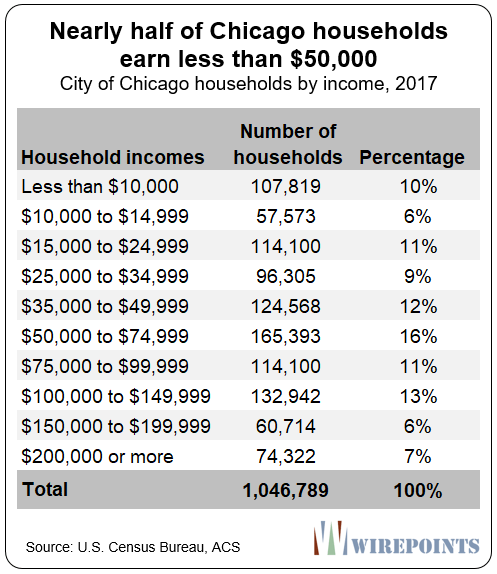

One-fifth of Chicagoans live in poverty and nearly half of all Chicago households make less than $50,000 a year. It wouldn’t just be wrong to try and squeeze those Chicagoans further, but pointless. They don’t have the money.

So if that won’t work, why not just put all the burden on Chicago’s “rich?” After all, Illinois lawmakers are pushing progressive tax schemes as the panacea for Illinois’ problems.

If households earning $200,000 or more are the target, they’ll be on the hook for more than $2 million each in government retirement debts. That’s an outrageous burden, too.

Saddling just a few households with all the debt will give those residents all the more reason to leave. And that will make the burden all the more unbearable for the Chicagoans who remain.

The process to target Chicago’s “rich” already started earlier this year. That’s when state lawmakers passed a progressive tax scheme which, if approved by voters in 2020, will hit Illinoisans earning more than $250,000 with tax increases as large as 60 percent. Chicago’s special interest groups want to hit the rich as well. They’re demanding a dedicated city income tax and a financial transaction tax that will impact the city’s wealthier residents.

Trying to find some middle ground on divvying up Chicagoans’ pension debts is also impossible. If all lower and middle income households earning up to $75,000 are protected, that leaves just 37 percent of Chicago households to pay the $150 billion bill. The burden on them would total $393,000 each. Still crazy.

Slice up Chicago’s debts anyway you like it, but the result is the same. There’s simply too much of it for Chicagoans to bear. Without structural pension reforms, expect the city to continue its path deeper into junk territory and an eventual insolvency. That will inflict enormous pain not just on taxpayers, but on the workers counting on the government for their retirement security.

Adding up the debt

For decades, official government reports have understated the true amount of pension debt Illinoisans are on the hook for. Government calculations have been criticized by the likes of Warren Buffet and Nobel Prize winners for using improper actuarial assumptions. For that reason, Wirepoints’ uses pension debts calculated by Moody’s Investors Service. The rating agency takes a more conservative approach to measuring debts than state officials do.

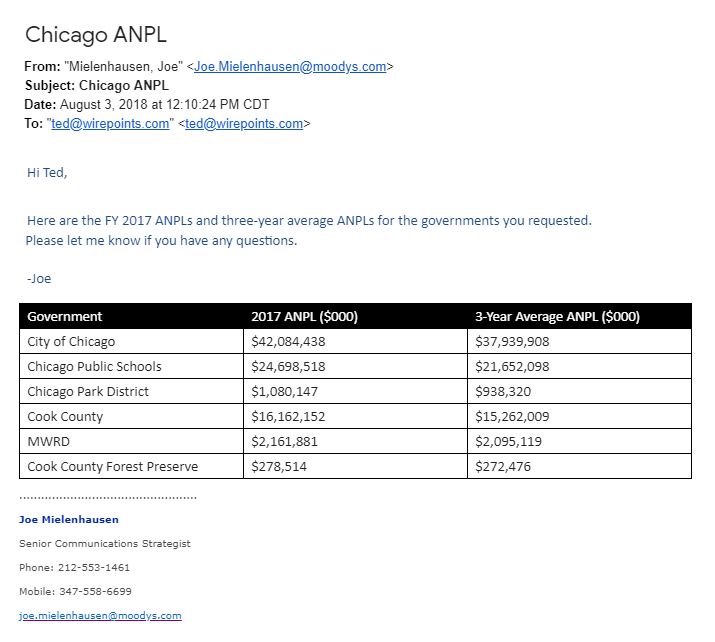

Chicago has four city-run pension funds that collectively face a $42 billion shortfall. The Chicago Public Schools’ pension fund is short another $24 billion. In all, there’s a $70 billion shortfall in the city-based funds alone.

Chicagoans are also burdened with an additional $11 billion in debt – their share of debts owed by various Cook County governments.

Chicagoans are also burdened with an additional $11 billion in debt – their share of debts owed by various Cook County governments.

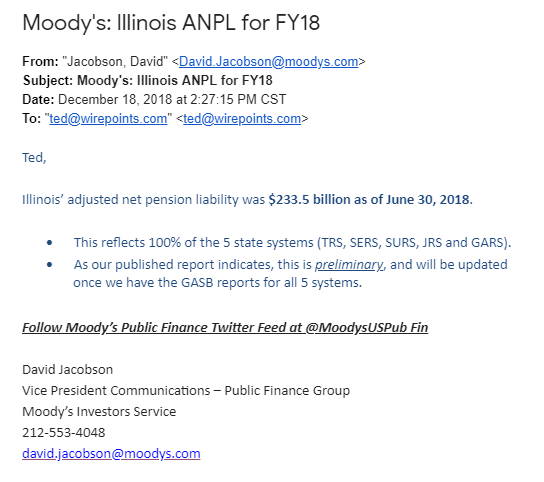

And Chicagoans’ share of state retirement debts for pensions, retiree health and pension bonds adds another $69 billion.

In total, Chicago households are on the hook for $150 billion in combined retirement debts.

Chicago the outlier

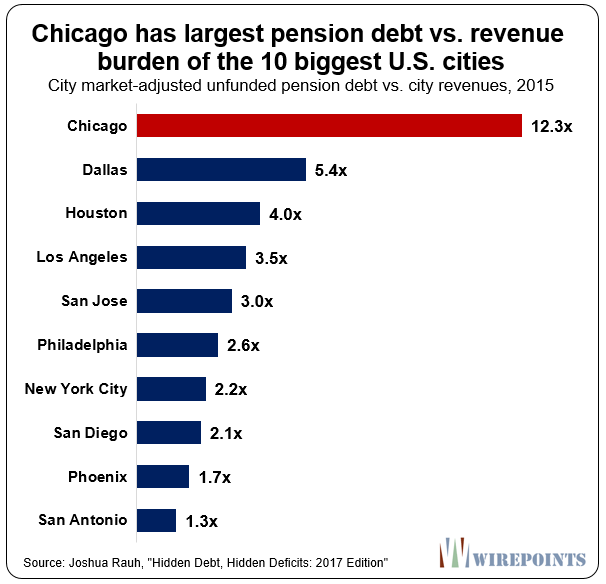

Not only are those debts overly burdensome to Chicagoans, but the city’s debts alone make Chicago a major outlier nationally when it comes to retirement debt.

According to Joshua Rauh of the Hoover Institution, the city of Chicago’s pension debts are now 12 times the size of its annual revenues. No other major city faces such a burden.

In fact, according to JP Morgan, over 63 percent of the city’s budget should be going towards retirement payments. That’s the worst of any major city in the nation, by far.

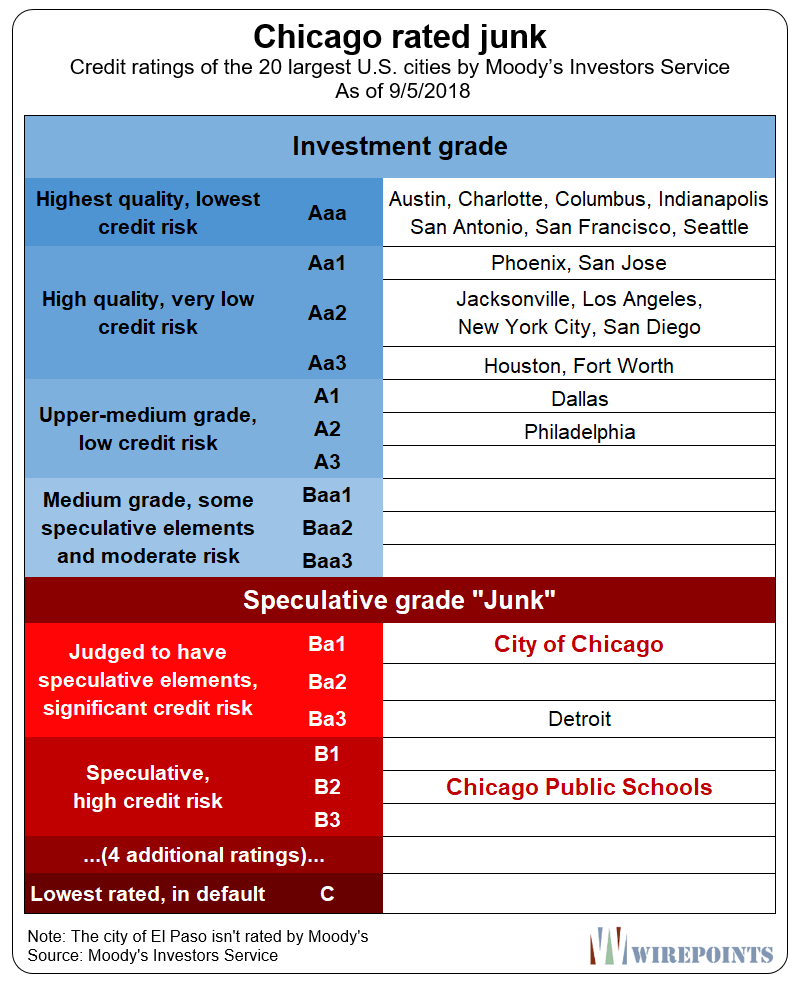

Too much debt is the key reason Chicago’s credit ratings have collapsed. Moody’s already rates Chicago one notch into junk and the Chicago Public Schools five notches into junk. Detroit is the only major U.S. city rated worse than Chicago (See Appendix 2).

Impossible without reforms

The above numbers show the impossibility of stopping Chicago’s fiscal decline without serious, structural pension reforms.

Some pension proponents will find offense with our use of Moody’s debt numbers – they’ll say Moody’s assumptions are too pessimistic and overstate the problem.

But the debt burdens are still unworkable even if official government numbers are used. The average Chicago household is still on the hook for $90,000 in debt under the official numbers, while households making $200,000 or more would still face a burden of more than $1.2 million each.

Without structural changes, those numbers will only get worse.

For starters, lower discount rates and more conservative actuarial assumptions continue to show that pension debts are much larger than politicians say they are.

Second, as in-migration into Chicago slows and out-migration increases – a fair assumption given that Chicago has shrunk four years in a row – the debt burden on those who remain will rise.

And third, the risk of a recession is growing now that the nation’s economic expansion has lasted an unprecedented ten years. Any significant pull-back in the stock market would deal a major blow to Chicago’s deeply underfunded pension plans.

Tax hikes won’t solve Chicago’s massive debt problem.

Only structural reforms, including changes to cost-of-living adjustments – will make the city affordable again for the ordinary Chicagoan. And that requires an amendment to the state’s constitutional protections.

Read more about Chicago and the state’s pension crises:

- Why Warren Buffett is right to warn about Illinois: The state’s true retirement costs now total 50% of annual budget.

- If a decline in births is a problem nationally, it’s a full-on crisis in Illinois

- Chicago’s pension funds looking more like a collapsing Ponzi scheme

- Illinois state pensions: Overpromised, not underfunded

Appendix 1

Below are emails from Moody’s outlining the pension debts of various Illinois governments. Moody’s Moody’s term for pension shortfalls based on their calculations the Adjusted Net Pension Liability, or ANPL.

Appendix 2

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

Unions and their leftist pols have created a ponzi scheme. Get out now…

If you’re wealthy and you still live in Chicago (and in Illinois), you deserve to have this happen to you.

help let the american people know

for the past nearly 30 years , all across america,

trillions of dollars of taxpayer money has been stolen through racketeering fraud, ,

and nobody will listen .

https://www.youtube.com/watch?v=DB_c5FVjdx8

Loved this video!!!!!!

What about the approx $547 billion in endowments the large colleges have? This should have been used to reduce student debt all along to a greater extent than it is now.

The solution is to tax the politicians who created this mess. If they had put the required funds into the pensions like they were supposed to instead of kicking the can down the road, so they could fund pet projects to get them reelected, we would not be in the situation. The people of Illinois did not create this mess, the politicians did and the people should not have to pay for their incompetence and greed-let them pay!!

Disagree somewhat. The people of Illinois did create this mess by voting Democratic. Did you?

Yes, and the democrats showed up by the hundreds of thousands to vote for JB. He had 2.5 million votes! Because they hate Trump.

Then they deserve what they get for voting for dems.

Brilliant analysis! But what if it’s already too late?

It is not too late if you leave now. It will get worse!

Brilliant analysis! But what if it’s already too late?

It was too late 20 years ago…

Elizabeth Warren is already talking about a wealth tax, albeit kicking in a high levels and taxing accumulated wealth rather than income. This article seems to be talking about an income tax. Either type holds the potential of appealing to the majority of voters who will assume it’s their chance to do a bit of leveling without cost to the yes voters. Beginning with tomorrow’s debates, I anticipate that a lot of Democrat(ic) candidates will try to outdo one another supporting the concept. A similar concept, quite easy to enforce, would be to tax “excess” pension wealth including 401(k) accumulations… Read more »

Reminds me of the progressive tax. Only affects those over $250,000 a year. And in two years when that’s not enough, it will be $200,000 a year, and then three years from now, it’s any household with a six figure income – because six figures is RICH in this state compared to the residents of Englewood. And then it will be anyone that has a job will be taxed at progressively higher rates, all to pay the pensions of teachers and former state workers. Think of the children, think of the children!

I had that exact same thought. When it’s the pols who get to write the definition of “wealthy”, one must wonder how broad that definition will eventually become.

Only affects “households” over $250,000 a year. Since there are no married tax brackets, 2 working spouses would start to pay more at $125,000.

I took a healthy dose of tax law at one point in my life, and had a college roommate who is now the head tax guy at Brookings. The tax experts I have talked to tell me that somewhere between 250-600k on income a year is where the money is for the Government to grab. That is it – not enough truly wealthy people around and people making 125k or less are already tapped out. Wealth taxes historically have completely failed, because the truly wealthy move or engage in tax avoidance tactics available to them, and the revenue actually obtained… Read more »

Here’s the thing about the “401(k) thing.” Actually more than one: A) If we seek to trim the public DB pensions above $X per year [as the PBGC guarantee program does in the private system], there’s a sort of mutuality in eliminating the tax deferral for 401(k) balances above a certain point. B) “Middle class folks” don’t generally accumulate giant balances while the very-well compensated are able to use 401(k) as an easy way to shelter millions. (Of course at 70-1/2 they have to start paying income tax but the rollover an inherited IRA provision likely signal that large accumulations… Read more »

Further to my earlier comments that appear below: It appears we are going to have to blend or choose among various unpleasant alternatives. Bailouts involve either taxes or devaluing the currency. Pension reductions (or taxing parts of 401(k) accumulations) are disrupting expectations and resemble simple confiscation. Plus taking money out of circulation in the economy. Social security, military pensions, medicare etc. are not prefunded to any extent either so the devaluation or confiscation will be required there also. The political process will likely result in a combination of unthinkables. Most of the solutions will result in value loss in real… Read more »

My household approaches and sometimes exceeds the $250,000 mark. I’m self-employed so I can control how much I want to work. And believe me, I only work as much as I need to. I could make twice as much money if I just put a little more effort in but the problem is that means paying MORE than twice as much tax with progressive tax rates. My free time is worth far more than a little more money, of which nearly half of every additional dollar earned goes to taxes. The country wonders why there is such wealth gap between… Read more »

So I have a lot of accumulated wealth but not a lot of income, where do I get the money to pay the tax? Sooner or later that accumulated wealth will get redistributed to my heirs or charity. I’d rather not have the government squander it. Although $2.5M sounds like a lot of money in a 401K at 3.5% it only generates an annual return of $87,500.

Perhaps this is just me being optimistic, but I don’t see outright asset/wealth confiscation ever happening in the USA. It’s not in our DNA (yes yes lots of other crappy policies in place aren’t in our DNA, I get it). But this is a step too far. I view it like free news/websites, they are used frequently but the second you add a paywall (even if it’s $1/year) people say to hell with it and not want anything to do with it. So yes all these liberal policies are blossoming but this is so far over the line (not to… Read more »

The fact of the matter is that most news organizations can’t sell their own product – i.e. the fake news. Because it has zero value. I cancelled my long standing Trib subscription in 2016 after it went full on Trump Derangement Syndrome. I don’t miss a thing.

The only product newspapers can sell are the eyeballs of the readers to advertisers.