By: Ted Dabrowski and John Klingner

Illinois’ nation-worst pension crisis is all but forgotten as COVID, crime and schools continue to take center stage. Not to mention Illinois’ nearly $200 billion in federal bailout funds have blunted the impact of retirement costs for a year or two.

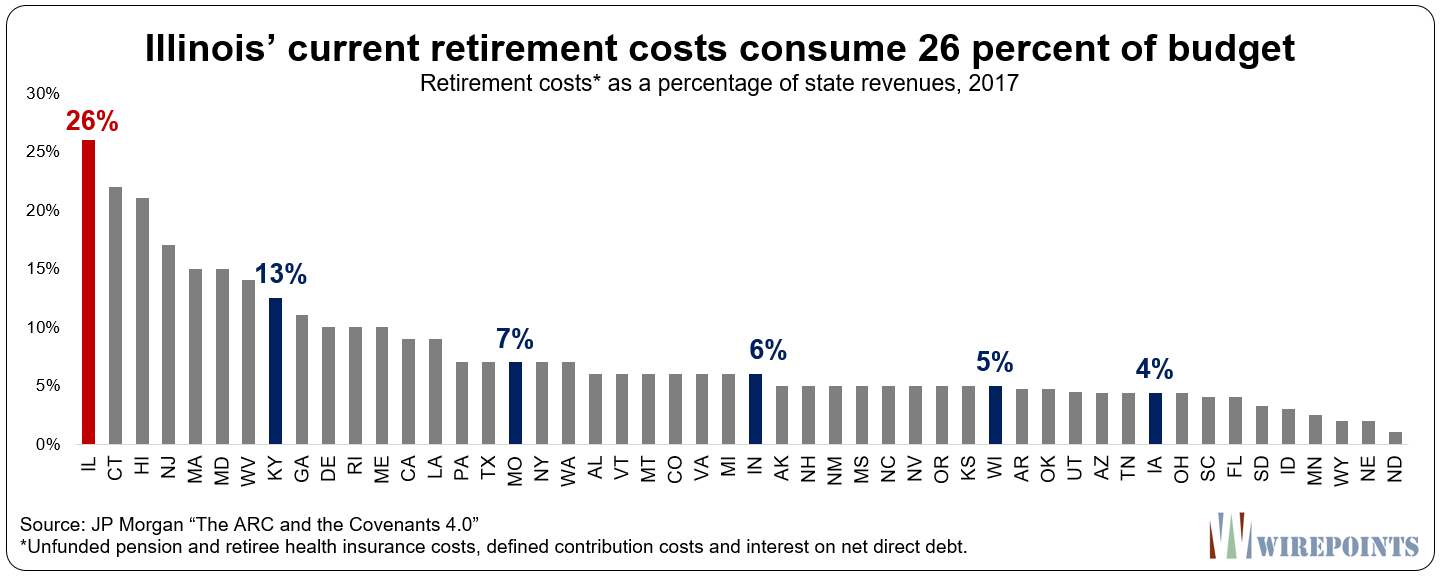

But that doesn’t mean that the state’s retirement problems have gone away or are any less severe. A recent legislative committee meeting served as a reminder that pensions are still set to consume nearly a quarter of Illinois’ budget, as they have in years past. A study by JP Morgan from a few years ago found Illinois pensions consume more of the budget than any other state in the nation. By comparison, all of Illinois’ neighbors but Kentucky spend less than 10 percent of their budgets on pension costs.

On Monday, Illinois’ five state-run pension systems submitted to the legislature their formal requests for state funding. A Senate appropriations subcommittee reviewed that request: $10.8 billion in costs Illinoisans will be on the hook for during fiscal year 2023.

Here’s some of the issues the Senate subcommittee covered in their meeting:

1. Pension costs alone are set to devour nearly 24 percent of Illinois’ $45.4 billion budget in 2023. That includes $9.6 billion in direct contributions to the pension funds, another $869 million in pension bond repayments, and a $295 million contribution to Chicago teacher pensions for their normal costs.

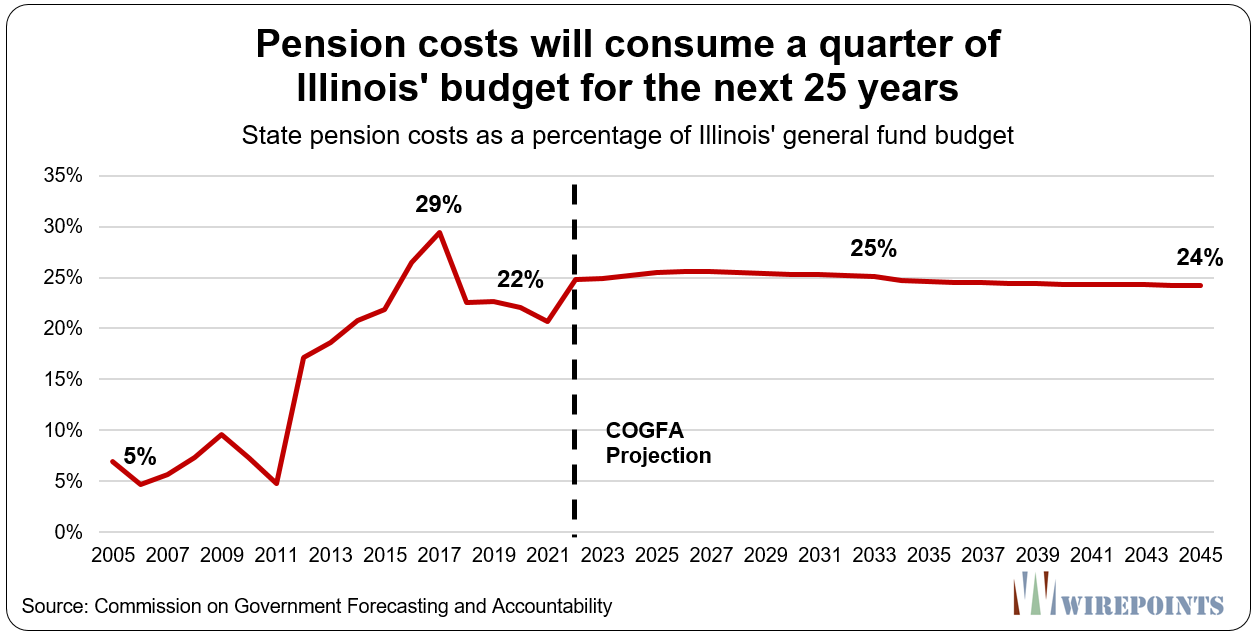

2. Pension costs have risen dramatically over the past several years, increasing from 5 percent in 2006 to more than 25 percent in recent years. According to the latest report from COGFA, pension costs will continue to consume about a quarter of the general budget for the next 25 years.

2. Pension costs have risen dramatically over the past several years, increasing from 5 percent in 2006 to more than 25 percent in recent years. According to the latest report from COGFA, pension costs will continue to consume about a quarter of the general budget for the next 25 years.

3. The state’s official pension debt totals more than $198 billion. That’s made up of $130 billion in pension debts, $9 billion in pension obligation and pension buyout bonds and $59 billion in retiree health debts.

3. The state’s official pension debt totals more than $198 billion. That’s made up of $130 billion in pension debts, $9 billion in pension obligation and pension buyout bonds and $59 billion in retiree health debts.

4. Moody’s puts Illinois’ state-level retirement debts at a much higher number: $376 billion. That’s more than $77,000 in debt for every household in Illinois. For a full count of retirement debts across the entire state, including local governments, see: Illinois pension shortfall surpasses $500 billion, average debt burden now $110,000 per household.

5. The state will contribute a total of $10.78 billion into the five pension funds in 2023 based on the state’s statutory funding ramp. That contribution will be made up of $9.63 billion in payments from the general budget and another $1.14 billion in other funds. That $10.78 billion is an increase of more than $200 million compared to last year and nearly double the $5.87 billion Illinois paid to pensions a decade ago.

6. Actuaries for the five state-run pension funds say Illinois’ statutory payment is too low. For example, the actuaries of the teachers fund calculate the state should contribute over $9.1 billion to TRS in 2023, $3.2 billion more than required by law, to properly fund the pension system. The higher contribution is based on more conservative actuarial assumptions.

7. The pension fund for lawmakers, the General Assembly Retirement System, continues to be the most insolvent of the five state pension funds. GARS is just 21 percent funded and has a shortfall of nearly $300 million. Illinoisans are forced to pay nearly $30 million every year to bail out the fund and keep it solvent – an amount equal to almost 300 percent of legislator payroll. In other words, Illinoisans pay nearly three times the amount for legislator pensions than they do for their lawmakers’ actual salaries.

8. The state will pay $295 million to the Chicago Teachers Pension Fund in 2023. The state has been paying the annual normal cost of the CTPF since 2019, one of the changes wrought by the 2017 “evidence-based” education funding bill.

********

The 2023 pension numbers show that Illinois’ pension crisis isn’t going away no matter how hard lawmakers try to ignore it. Not to mention the true state of Illinois’ crisis is far, far worse than the state’s official numbers show. You can read about the full retirement crisis in the Wirepoints pieces below:

- Illinois pension shortfall surpasses $500 billion, average debt burden now $110,000 per household

- Illinois pension debts dropped to $130 billion in 2021…and all it took was trillions in stimulus and a once-in-a-generation market rally

- Communities in crisis: More than half of Illinois cities get “F” grades for local pensions

- Illinois’ higher education crippled by skyrocketing pension costs

- Gov. Jim Edgar’s starring role in Illinois’ pension crisis: It’s bigger than just the “Edgar Ramp”

- Wirepoints’ Pension Solutions

Appendix

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

The container of last resort seems to be the Federal Bailout Bucket. It’s now shoring up multi-employer plans that were unsustainable ab initio. That includes NFL pension increases that pushed the funded percentages still lower. And the PBGC is essentially insolvent. Dollar denominated liabilities can always be paid with deflated dollars, although various COLAs will mean the systems are always chasing their tails. If anything is more essential than Teamster truckers, it is likely to be devoted public servants. Then we find veterans at the Federal level. And let’s not forget Social Security … where there is at least a… Read more »

So the vaunted Tier 2, ye ole savior of the pension system, will merely keep pension debt constant over the upcoming decades, even when virtually the entire workforce is Tier 2. Good times.

What’s the over/under when Tier 2 gets is first serious enhancement? 2030? What’ll it be? I’d wager the min retirement age requirement w/o penalty drops from 67 tom 62. It’ll be fun when most of the savings assumptions made since its creation never comes to fruition.

My friend has a son who is a youngish teacher on the North Shore. Bright kid who was not challenged in his education major at Normal. Not being the least inclined to economics, the kid has no idea of the lousy circumstance he is in as a Tier 2 recipient. He will pay taxes and other regressive charges like no tomorrow to pay for work long ago performed, yet be stuck with Tier 2 benefits. Sure, such benefits will likely be adjusted in his favor in the future but he has no realistic path to even modest prosperity. He left… Read more »