By: Ted Dabrowski and John Klingner

The nation’s weakest public pension funds may soon be among the casualties of COVID-19. Many were facing insolvency even before the virus hit and the stock market meltdown will only accelerate their decline.

Expect politicians in fiscally irresponsible states to ask for pension support as a part of any assistance they receive from the federal government. The country’s pension funds already faced a collective shortfall of more than $5 trillion in 2018, according to Stanford’s Pension Tracker. How the federal government doles out state aid, and what strings it attaches, will have long-term implications.

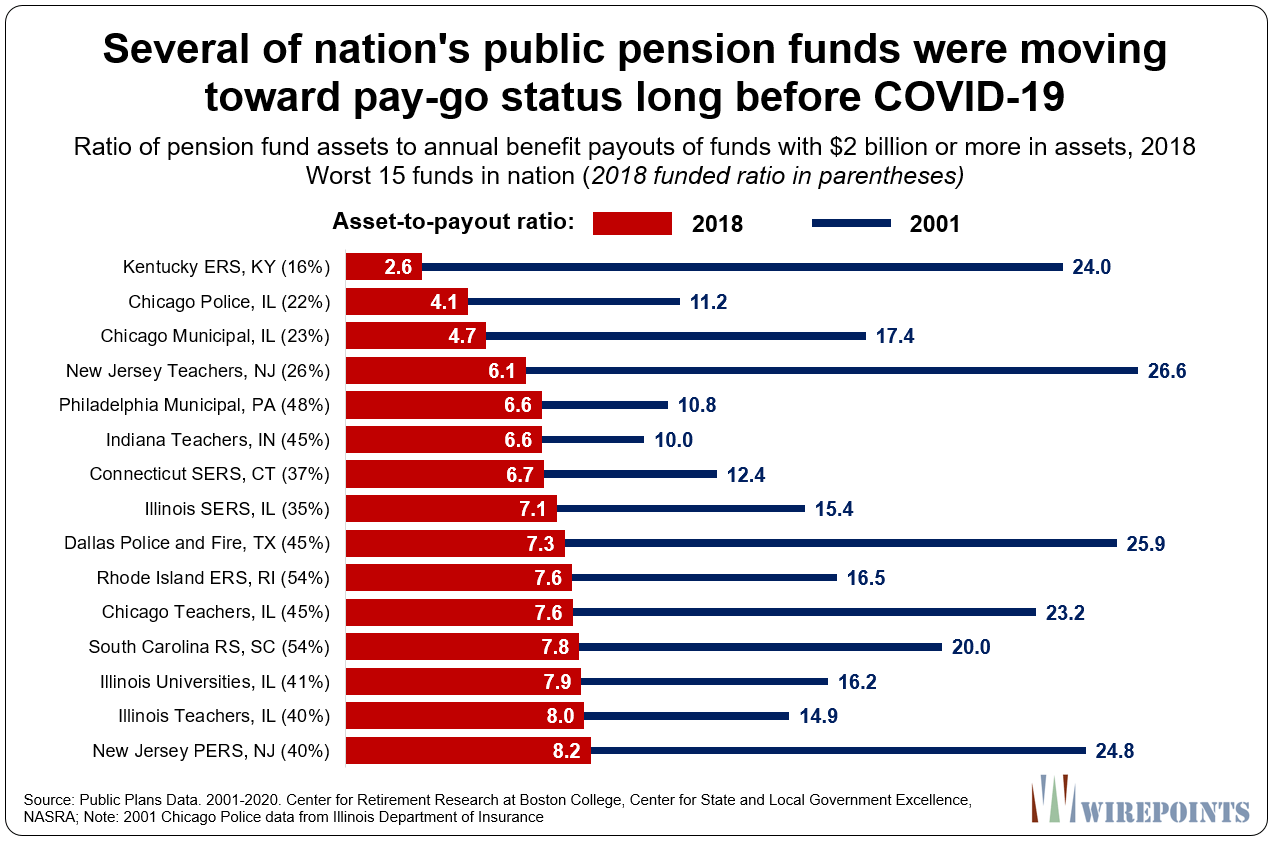

To see which funds were at greatest risk, Wirepoints analyzed the asset-to-payout ratios of 148 state and local pension funds across the nation with $2 billion or more in assets, using data collected by the Center for Retirement Research (CRR) at Boston College. The asset-to-payout ratio – one of the statistics Moody’s Investors Service uses to measure pension health – compares a fund’s total assets to how much it pays out in benefits each year. In other words, it measures how many years a pension plan can make benefit payouts before it runs out of money, assuming no new contributions or investment income.*

Worst-off are funds in the states most well known for their pension crises: Kentucky, Illinois, New Jersey and Connecticut. In 2018, the most recent year with comparable nationwide data, some of those funds had assets equal to just a few years’ worth of benefit payouts.

Kentucky’s Employee Retirement System had the worst asset-to-payout ratio in the CRR database. The fund had just 2.5 years’ worth of assets to make future payouts with.

For the full list of 148 pension funds, see Appendix 1.

Aaron Ammerman, Board Chairman of the Bluegrass Institute for Public Policy Solutions in Kentucky, says that the employees’ fund is at a level no public pension fund has ever recovered from and that the state’s other funds aren’t far behind.

Both Kentucky’s county-level and teacher funds also have less than ten years of payouts left. Unfortunately, even that fact isn’t enough to create change in the state. “Politically, it’s been really hard to get anything done in Kentucky when it comes to substantial reforms,” Ammerman says.

The New Jersey Teachers’ Fund had $26 billion in assets in 2018 – enough to cover only six years of payouts. The state’s public employee plan can cover just eight years of payouts.

John Bury, a New Jersey actuary who writes on pension issues at Burypensions, warns that funds in his state could start bouncing checks to retirees. Plans like the teachers’ fund are stuck with alternative investments, private equity and other complex products and very little cash. He says that if the state stops making its full contribution and “this downturn lasts through this year, then New Jersey’s funds won’t have enough liquidity to issue checks.”

Collectively, Illinois is the worst state in the CRR database when looking at funds with $2 billion or more in assets. Of the 15 worst-off funds, six of them are in Illinois – three at the state level and three in Chicago. All of them have assets worth eight years or less in payouts.

Two extremes

It’s unclear just how long and how deep the current market decline will be. And it’s not known yet just how exposed these funds were to the market correction – pension funds only disclose their financials months after the fact. But all funds will undoubtedly take some sort of hit to their already depleted assets.

If those plans run dry, they’ll end up as pay-as-you-go systems, where pensioners are forced to rely directly on the operating budgets of their employers, and not pension fund assets, to get their retirement checks.

Some funds, like some in New Jersey, are already in deep trouble. Bury says that if New Jersey’s funds were using honest accounting, “the plans would likely be pay-go already.”

Collapsing to pay-go status is risky given that sponsoring governments would have to make even bigger contributions directly from their operating budgets. With no pension assets left, they’d be responsible for paying the full amount of pension benefits each year.

Some governments can’t afford that considering they’re at risk of going broke themselves. That’s the case for the city of Chicago, which was already junk-rated and struggling with severe budget deficits even before the COVID-19 crisis began. (See case study below.)

In contrast to those funds running out of cash, the nation’s healthiest pension funds are well positioned to weather the current crisis intact.

The best funds had assets equal to 20 years or more of benefit payments before COVID-19 came along. While their assets may take a hit from the downturn, none of them are in any danger of depleting their available funds.

Tennessee’s Political Subdivision fund for local governments, for example, was 98 percent funded in 2018 with an asset-to-payout ratio of nearly 24. Missouri’s local fund also had 24 years of payouts. And South Dakota’s state fund was 100 percent funded with a ratio of 22.6 years.**

Illinois Case Study

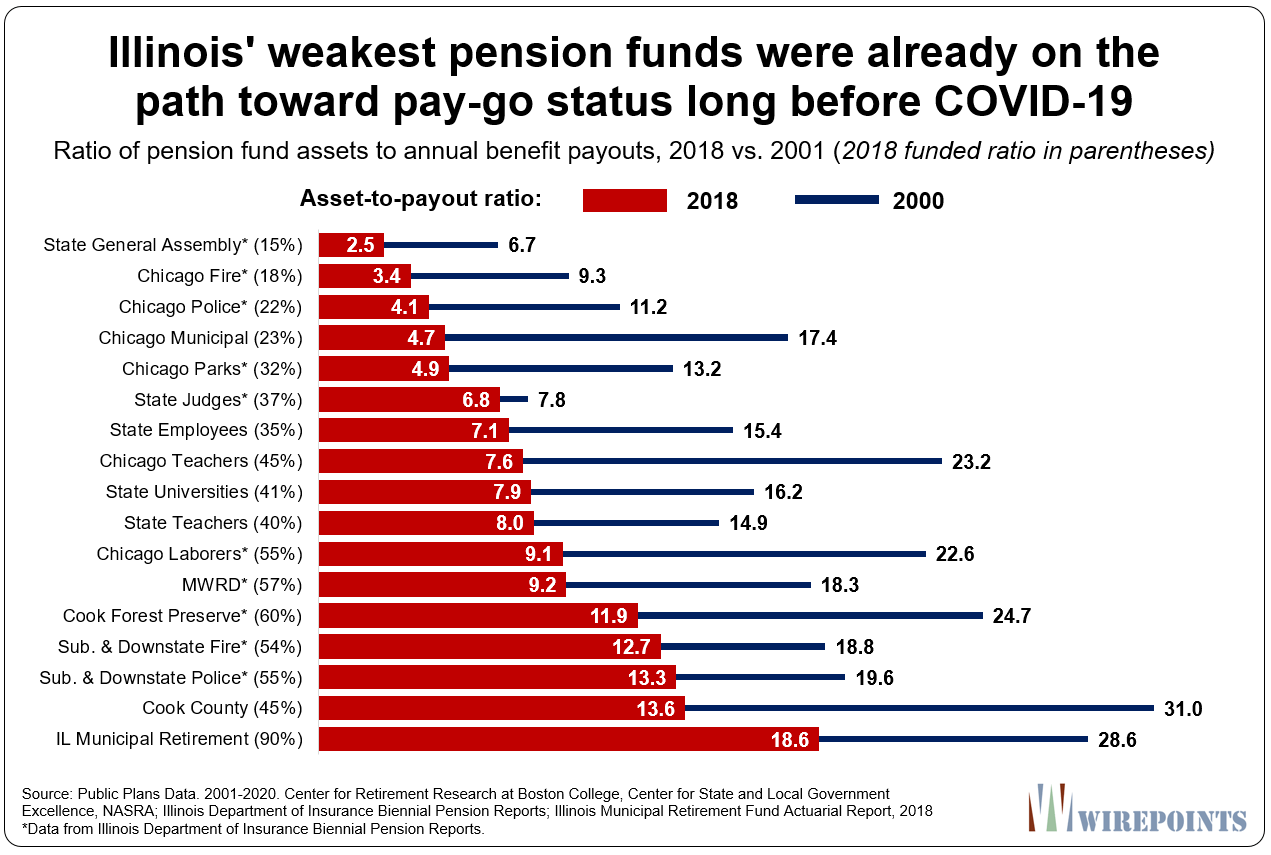

Illinois pension funds are some of the most at-risk in the nation for going pay-go. Wirepoints calculated the asset-to-payout ratios of the pension funds in Illinois and found several had just two to five years’ worth of payouts left in 2018.

Take Chicago’s fire pension fund. In 2018, its total assets were $1.1 billion and its pension payout for that year was $330 million. That means it had about 3 years’ worth of payouts on hand – an asset-to-payout ratio of 3.4. There are just a handful of funds in the nation with lower ratios than that. By comparison, the plan had a ratio of 9.3 at the turn of the century.

The market sell-off and lower interest rates as a result of COVID-19 means the asset-to-payout ratio, barring any bailout, will continue its path toward zero.

It’s a similar story for Illinois’ other funds. Chicago’s police, municipal and park funds had ratios of less than five. The state’s employees, universities and teachers’ funds had assets worth just seven to eight years’ worth of payouts. All those funds are in the bottom 10 percent nationally.

Illinois’ dire asset situation is compounded by the fact that both Gov. J.B. Pritzker and Chicago Mayor Lori Lightfoot continue to categorically reject calls for a constitutional amendment that would allow pensions to be reformed.

Illinois’ pension crisis stems from a long history of overpromised pension benefits. But both the governor and mayor are unwilling to cross the public sector unions, even as the city and the state continue their downward spiral.

The coming bailout push

With so many cities and states suffering significant budgetary shortfalls due to COVID-19, it was inevitable that some of the nation’s worst-off governments would push for a bailout of their pension funds.

Illinois was the first state to ask. The state’s Senate Democratic caucus is seeking $20 billion in direct assistance for pensions as part of a $42 billion bailout request.

John Bury thinks that bailouts are likely given that so many funds are running out of assets. There will be a lot of financially responsible states that reject the idea of a pension bailout, he says. But if the federal government does get involved, it “should have some pension-reform strings attached.”

Most states with failed pension plans will complain about having to reform. But they are running out of options. New Jersey and others “still have enough money to keep going for two to three years,” Bury says. “But after that, who knows?”

The unwillingness of such states to make hard choices on their own is precisely why the federal government shouldn’t step in. But if it does dole out funds, any help must come with preconditions.

Defined contribution plans, cost of living reforms and increased retirement ages are all part of the reform suite the federal government should require. And for states that have constitutional protections, state lawmakers must commit to removing them or lose out on the aid.

Whether the federal government eventually provides direct aid to state and local governments remains to be seen. However, it’s imperative that any such support not be used to bail out pensions or enable irresponsible states to further ignore their retirement crises.

*A fund’s asset-to-payout ratio serves as a snapshot of a fund’s health. A shrinking ratio over time indicates a falling level of assets relative to a fund’s payment obligations. The ratio, however, does not predict when a fund will run out of money. The fund’s decline can be expected to take longer than the ratio indicates given it will still receive contributions from its sponsor and employees, as well as generate investment income.

**The state of Washington has a sprawling, complex set of segmented pension plans based on different tiers, which create outliers in the database. As such, Wirepoints does not highlight them in the text.

Appendicies

Appendix 1. Comparison of state and local pension fund asset-to-payout ratios, 2018

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

Illinois is going to be insolvent shortly. That will solve all the problems. All checks will bounce and everyone will have to fend for themselves. The courts can order payments, but the can not make money appear that is not there. Let them issue IOU’s to all pensions.

The asset to payout ratio is a very misleading measure of pension plan solvency because it ignores annual contributions that employers and employees are already making, and these are typically required by law so they must continue. Take Illinois Universities (SURS) as an example. Yes, the assets were 19.35 billion and the annual benefit payout 2.45 billion in 2018, but the statutory state contribution is currently 1.9 billion each year. So provided that the contributions and benefits grow at similar rates, even if the plan earns zero investment returns on average, the assets only decrease roughly 0.5-0.6 billion each year… Read more »

Andrew, this ratio is just one of many ratios that anybody analyzing a fund should look at. But used properly, it’s a very powerful one. It can give you some hints very quickly that something is wrong. Take Chicago’s municipal fund. In 2000, it had assets worth more than 17 years of payouts. By 2018, it was just over 4.7. Warning signals should have gone off long ago. That collapse is alarming. Add to that the current stock market meltdown and 10-year yields below 1 percent. Compound it with a sponsor city that’s junk rated and seeing its revenues cut… Read more »

The federal government should bail out all the honest hard working taxpayers 401K’s. They really deserve it. Cops, Teachers and Firemen are nothing but overpaid lazy do nothings.

Your last sentence suggests you must have some Ph. D. dissertation on that topic. Otherwise, you must have gotten that generalizaton straight outta the other brain that resides in your ass!

The term “ass clown” is an apt title.

Pay your taxes slacker! I need more cash to burn on lottery tickets. Casino is closed, lottery tix are the best. My favorite is the $25 crossword game. I usually buy 6 at a time. PAY ME

What about funding everyone’s 401k too? That decline was truly 100% caused by this act of God affecting a totally honest investment. The decline of public pensions was caused because those were Ponzi schemes, a pretend investment, that hit the wall of an operational tax skim. So the fed will get into the Ponzi game now while everyone with a 401k pounds sand? I’m not going to solution this here, but any semblance of a fed bail needs to be accompanied by great pain, great restructuring, great contract rewrites, great haircuts on the bond vultures, and a great many class… Read more »

Agree 100%. Boost up our 401ks and also, no bailout money at all until AFTER legislation is enacted and pensions are completely restructured or turned into 401k plans. No public employee who is making a six figure salary should be able to retire after 25 years (age ~50) and rake in millions of dollars for the next 25 to 30+ years off of taxpayers.

If there is to be a bailout it should not be in the form of an upfront lump sum. That’s too much like selling pension bonds and moving money beyond the reach of anyone but pensioners. Further, without conditions the sudden improvement will simply provide the unions with additional ammunition to seek pay and benefit increases. Instead, money should be trickled in as a reward for reforms appropriate to the state involved. Perhaps a federal insurance program should be enacted along with the bankruptcy option. Make the bankruptcy provision effective in a year or two and allow individual employees and… Read more »

I don’t believe anything should be considered by the Federal government on a taxpayer bailout for Illinois until Illinois can demonstrate it’s done all it can do to fix it’s past mismanagement. Illinois must be put to the test first.

Federal taxpayers are currently picking up the cost for Wuhan virus expenses because this is a ‘National Emergency’. When Hurricanes, Tornado’s, Earthquakes, Wild Fires, and other ‘force majeure’ events hit, I do not believe FEMA or the Federal Government starts to cover secondary costs (lost wages, lost sales tax) or unrelated costs (decades of mismanagement). So to say there will be a ‘bailout’ is very premature – it would be a new precedent. Also, many have argued bailouts are unconstitutional (I know, Democrats see the Constitution as legality to be undermined). I don’t think bailouts will happen – Even though… Read more »

John & Ted: GREAT article and data! Depending on the average weighted age of current retirees (weighted by amount of bft pymts) and depending on COLA, a fraction of probably between 12-18 is necessary for the assets to cover the liabilities of just the current Retirees. If the assets are less than that, it means not even Retirees are covered, so there are ZERO assets for Actively-Employed participants, unless Retiree bft pymts are drastically cut.

I am concerned mitch McConnell will cave (as you can see Kentucky is in some trouble too with pensions). There is also the emergence of modern monetary theory gaining traction, where it is believed the federal government can print all the money it wishes without fear of inflation until full employment. The proponents of mmt say that inflation in Zimbabwe wasn’t caused by printing, but by decrease in production with printing (they also cite the weimar republic as an example of hyperinflation from printing/declines in production). I’m a libertarian, so I’m against printing money, and if that’s the case, shouldn’t… Read more »

MMT is truly one of the dumbest concepts I’ve ever encountered.

Not at all known if they’ll be rewarded, and if it’s 20B, it will be sprinkled around and not make much difference.