By: Ted Dabrowski and John Klingner

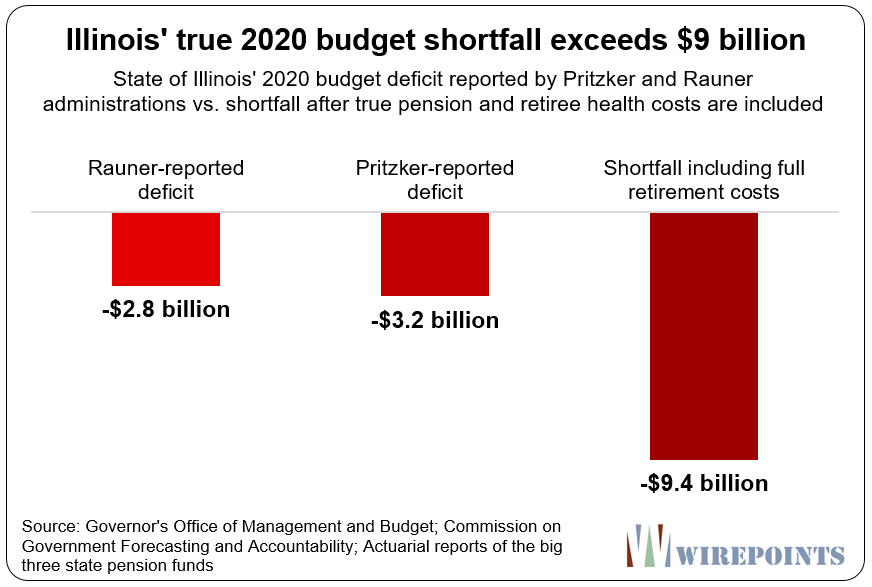

Gov. J.B. Pritzker’s administration has released a report that puts Illinois’ expected budget deficit for fiscal year 2020 at $3.2 billion. The report is critical of former Gov. Bruce Rauner for actions that Pritzker claims have made the budget hole even larger than previously projected. Rauner had reported the shortfall as $2.76 billion just three months ago.

But leaving politics aside – a new governor always blames his predecessor – Pritzker shouldn’t be given any credit for his more “honest” accounting of the state’s deficits. Nor should any previous governor. They’ve all understated the true shortfalls that are run up each year. Illinois’ official budgets never include the true cost of the state’s retirement benefits.

If Pritzker really wanted to break the cycle of fiscal dishonesty in Illinois, he’d tell the truth about how the big the hole is in 2020. The shortfall he’d report in his upcoming budget address would be at least $9.4 billion.*

That’s the actual shortfall if the state were to pay what it’s actuaries say it should – $3.2 billion for Pritzker’s original deficit projection, and $6.2 billion more to properly pay down the state’s retirement debts. That includes $3.2 billion for the state’s pension debts and nearly another $3 billion for retiree health insurance debts.

True shortfalls

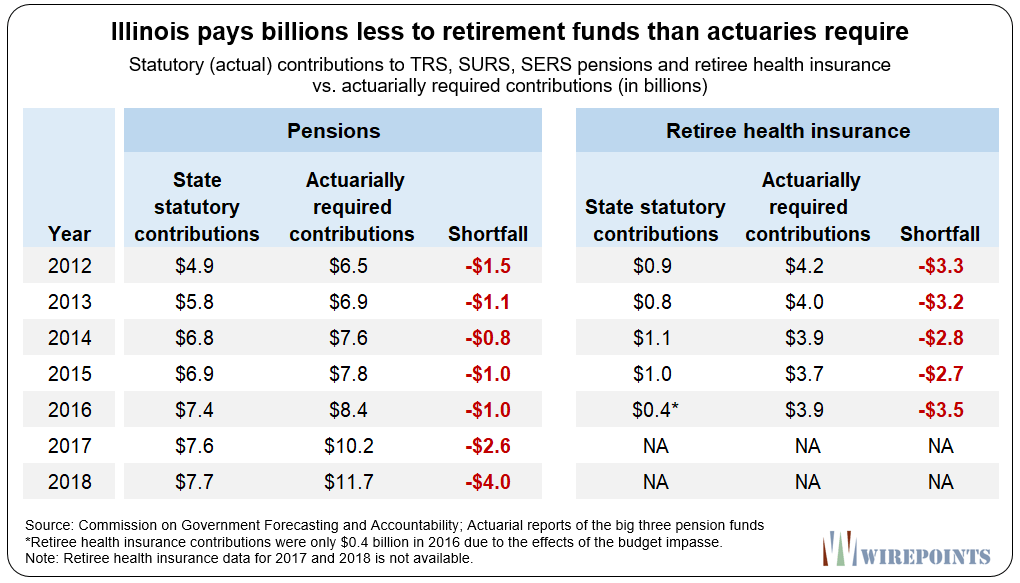

Every year, the state’s actuaries determine what amounts Illinois should contribute into state worker retirement benefits. And every year, lawmakers underpay those amounts. Statutory contributions set by Illinois lawmakers are always far lower than what’s actuarially required.

That makes the budgets look far better than they really are.

Wirepoints compared the actuarially required contributions (ARC) vs. the actual contributions to the state’s pension and retiree health insurance funds over the past several years. The state has consistently shorted the funds by billions as a matter of practice.

Those additional costs, if they had been reported properly, would have significantly impacted Illinois’ official budgets.

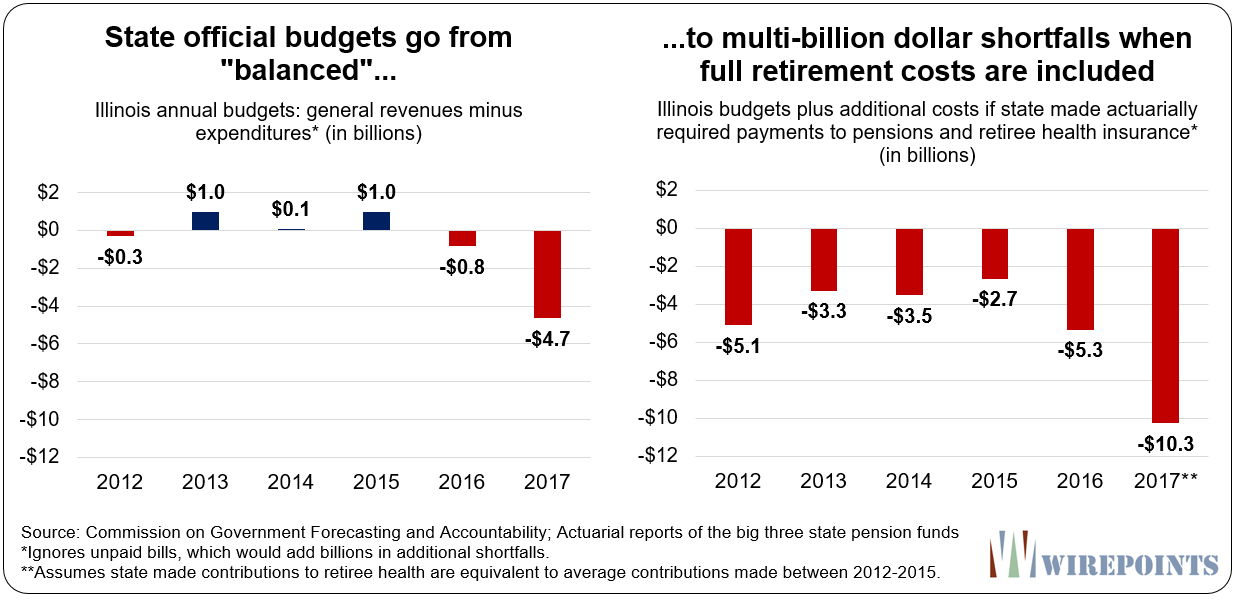

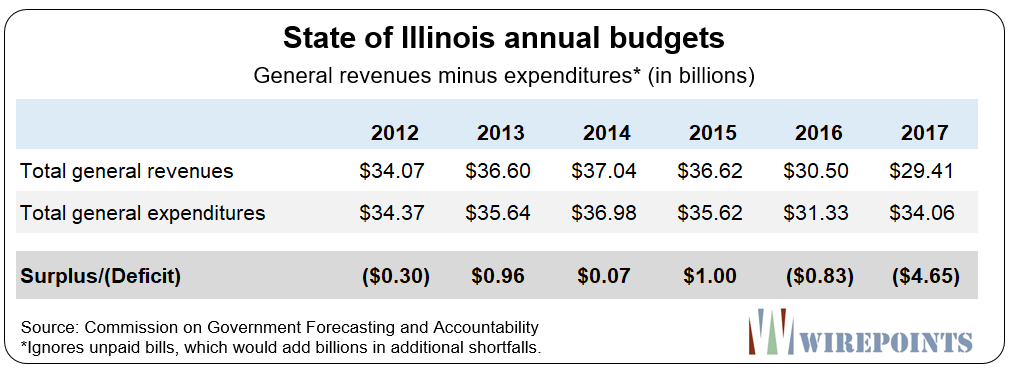

Take, for example, the budgets of the past five years (see appendix below). Their official surplus/shortfalls, as reported by COGFA, hovered around zero. (The exception is 2017, which was impacted by the budget impasse.)

But when actuarially-required pension and retiree health insurance costs are properly accounted for, the budget balances reveal a far worse picture. “Balanced” budgets become grossly unbalanced by the billions.

Hiding those true costs has helped Illinois rackup official pension debts of $134 billion and retiree health insurance debts of $73 billion, despite “balancing” the budget each year. (And all this ignores the billions in unpaid bills the state has run up since 2001.)

It’s also why Illinois ended up with a credit rating that’s just one notch above junk.

$9 billion shortfall

The contribution shortfall over the last couple of years averages about $6.2 billion annually – $3.2 billion for the pension funds and nearly $3 billion for retiree health. Apply that to Pritzker’s $3.2 billion deficit and the true shortfall for 2020 jumps to $9.4 billion.**

The problem in Illinois is that its politicians have never been honest with its residents about the true costs of the retirement benefits they’ve promised, nor about the true scale of Illinois’ debts.

Their constant distortions make it impossible to properly diagnose what’s really wrong with Illinois. And as long as that’s the case, politicians will get away with promoting pension bonds, asset transfers, tax hikes and securitizations as the “solutions” to Illinois problems.

That’s exactly what’s being promoted now by Pritzker’s administration, as our companion piece describes.

Read more from Wirepoints about Illinois’ budget crisis:

- Illinois’ crisis: 20 facts Pritzker doesn’t want ordinary Illinoisans to know

- ‘Asset Transfers’ To Pensions: Be Afraid

- Moody’s vs. Illinois politicians: $100 billion difference in pension debts

- Illinois’ other debt disaster: $73 billion in unfunded state retiree health benefits

- Overpromising has crippled public pensions: A 50-state survey

*And that’s still not the full true shortfall. The actuaries’ required contributions are still based on the state’s rosy assumptions, i.e., high interest rate assumptions. More realistic assumptions like those of Moody’s or JP Morgan mean Illinois’ true shortfall are higher still.

**Pensions: Wirepoints uses the average pension contribution shortfall in 2017 and 2018, approximately $3.2 billion, as a proxy for the 2020 shortfall. Those years more properly reflect any future shortfall because the state tightened its actuarial requirements in 2017. Retiree health: Actual retiree health contribution shortfalls for 2016, 2017 and 2018 are not yet available. Wirepoints uses the average shortfall of the 2009-2015 period as a proxy for the shortfall in 2020.

Appendix

Audio and summary

Audio and summary  If this bill passes, say goodbye to local control over all Illinois parks and expect to see open drug and alcohol use, needles, no sanitation and fire hazards, but no ordinary park users.

If this bill passes, say goodbye to local control over all Illinois parks and expect to see open drug and alcohol use, needles, no sanitation and fire hazards, but no ordinary park users.

Wirepoints State of the State.