By: Ted Dabrowski

If you’re worried about your job, pay and Illinois’ overall economy, you may want to pay attention to the latest proposal from Moody’s Investors Services.

Moody’s – the rating agency that calculates the “credit score” of cities and states across the country – wants to update its rating methodology for states and territories. It wants to increase the influence that debt and pensions have on the overall ratings of those governments.

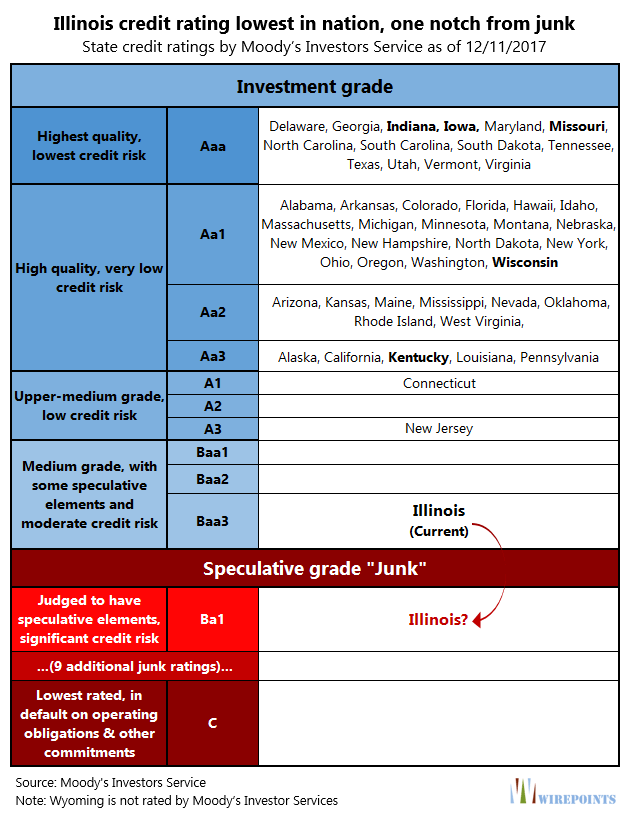

That’s bad news for Illinoisans and the state’s economy. Moody’s already rates Illinois’ credit just one notch above junk – the worst in the nation for any state. Any additional focus on pensions and debt could throw the state into a junk rating territory quickly.

Specifically, Moody’s proposes the following changes:

“Proposed changes include reducing the weight of the governance factor to 20% from 30% and increasing the weight of the economy factor and the debt and pensions factor to 25% each from 20% each, to reflect the relative influence of the state or territory economy and the effect of long-term liabilities on credit assessments.”

Illinois already has the nation’s worst pension crisis and its pension shortfalls have failed to improve despite one of the longest bull markets in history. If and when the inevitable recession comes, expect the negative impact of pensions to increase.

In the absence of major reforms, a junk rating is the logical next step for Moody’s.

A junk rating means higher borrowing costs for the state, just like a bad credit score means higher interest rates on a mortgage or a car loan. A junk rating also means less money for all kinds of services the state provides, whether it’s student loans for low-income students, health care for the disabled or public safety on our streets.

But that’s just part of the cost. A junk bond rating would also scare away investors and entrepreneurs. Fewer companies would want to invest in Illinois and those already here would choose to take their future spending elsewhere. And would Amazon really want to bet its future and a second headquarters on a junk-rated state?

More people would also leave as the economy worsens. We’ve already seen the impact of dysfunction and too-high taxes over the past few decades.

Recently released IRS data shows that outmigration from Illinois continued in 2015/2016, even though the national economy had stabilized and stock markets had recovered to new highs. That year, the state lost of a net of 86,000 people. And both Illinois and Chicago have lost people three consecutive years.

The bottom line is it’s impossible to grow the tax base and an economy when the state’s population is fleeing and pension debt swallows everything in its way.

Moody’s says that for now, “If the proposed methodology is adopted, no ratings will be placed on review for a possible rating change.”

But don’t expect them to be too patient with Illinois. The state’s $250 billion debt – that’s the figure Moody’s calculates – is strangling the state. And Illinois is going into next year’s budget with a beginning deficit of up to $3 billion dollars.

Moody’ new methodology should be a wakeup call for state legislators. Getting that debt down will mean implementing 401(k)s for all new workers at all levels of state government, reforming the Constitution’s pension-protection clause, and negotiating a bankruptcy clause with the Federal government.

If legislators don’t act quickly, expect real pain for all Illinoisans.

Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.