Part 1: Illinois is the Nation's Extreme Outlier

Illinois’ General Assembly has refused to solve the state’s ever-growing retirement crisis for more than three decades. And for three decades, Illinois’ finances have steadily decayed. Debts have grown by billions year after year despite assurances by lawmakers that budgets were balanced and actions had been taken to bring the crisis under control. Illinois is now a national outlier, and in many cases, an extreme outlier – on almost every financial, economic and demographic metric that matters.

Pensions aren’t Illinois’ only problem, but because their costs dominate government budgets, their impact is felt everywhere. There’s no fixing Illinois without changing the current system and dramatically reducing the state’s retirement shortfalls.

The costs of retirement debts are overwhelming every constituency in Illinois. Retirement security for most government workers has collapsed in tandem with falling funded ratios. Spending on Illinois’ most vulnerable is being crowded out as retirement costs have grown to consume more than a quarter of the state’s budget; no other state spends nearly as much on retirements. And ordinary residents who pay for the costs of their public servants are being crushed by the country’s highest property taxes and one of the nation’s highest combined state and local tax burdens.

The evidence of the state’s decay can be captured in just two metrics: the state’s credit rating and domestic out-migration.

No state has ever been rated junk before, but today Illinois is rated just one notch above junk with a negative outlook. The rating embodies not just the state’s fiscal failures, but also the continued failed governance of the General Assembly. It’s not as if lawmakers weren’t warned of the consequences of their mismanagement. The big three rating agencies have downgraded Illinois 22 times since 2009.

Illinoisans have fled the state’s growing problems in record numbers. No other state lost more people over the last decade than Illinois. What was revered as the country’s destination state just 60 years ago is now a state with a shrinking population and the nation’s second largest rate of domestic out-migration.

This first part of Wirepoints’ four-part series lays out how Illinois is the nation’s extreme outlier and the negative impact that status has on people’s lives and livelihoods.

Illinois’ worst-in-nation crisis

Illinois is a national outlier when it comes to the financial well-being of the state and its residents.

Illinois has the nation’s largest pension shortfalls, both in amount and on a per capita basis. Total retirement debts consume more of Illinois’ budget than they do in any other state in the country, by far. And retirement costs have helped drive Illinois’ overall tax burden to one of the highest in the nation.

All of that has created a crisis of confidence in Illinois. The state has the nation’s lowest credit rating, sitting at just one notch above junk.

And since 2010, Illinois’ population has shrunk by more than any other state as residents have left in record numbers. That’s contributed to a fall in real property values and a vicious downward spiral for the state.

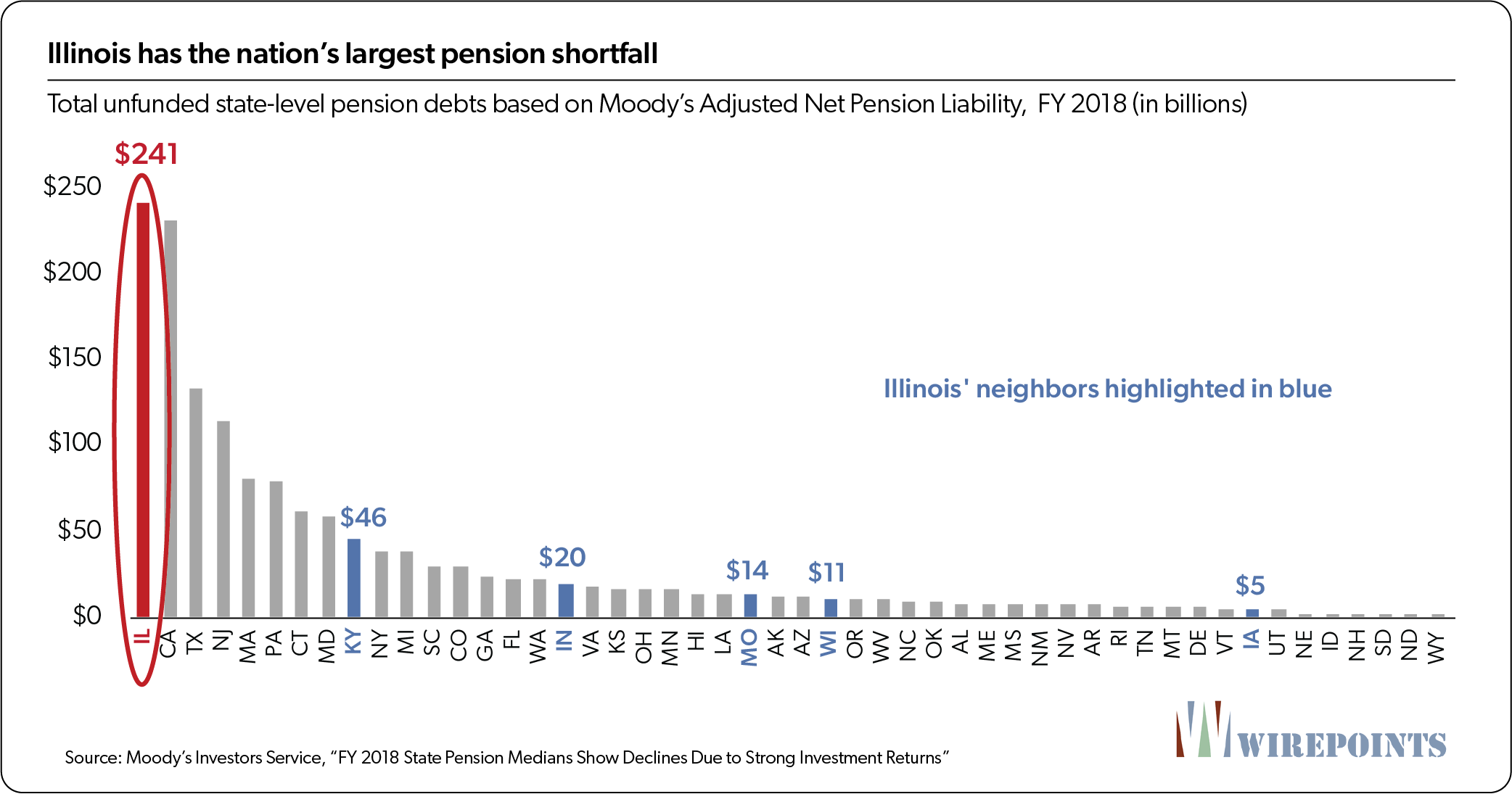

Moody’s Investors Service puts the pension shortfall for Illinois’ five state-run pension funds at $241 billion. Illinois’ debts dwarf those of its neighbors as well as those of the largest states in the country by population. Illinois is the extreme outlier nationally.

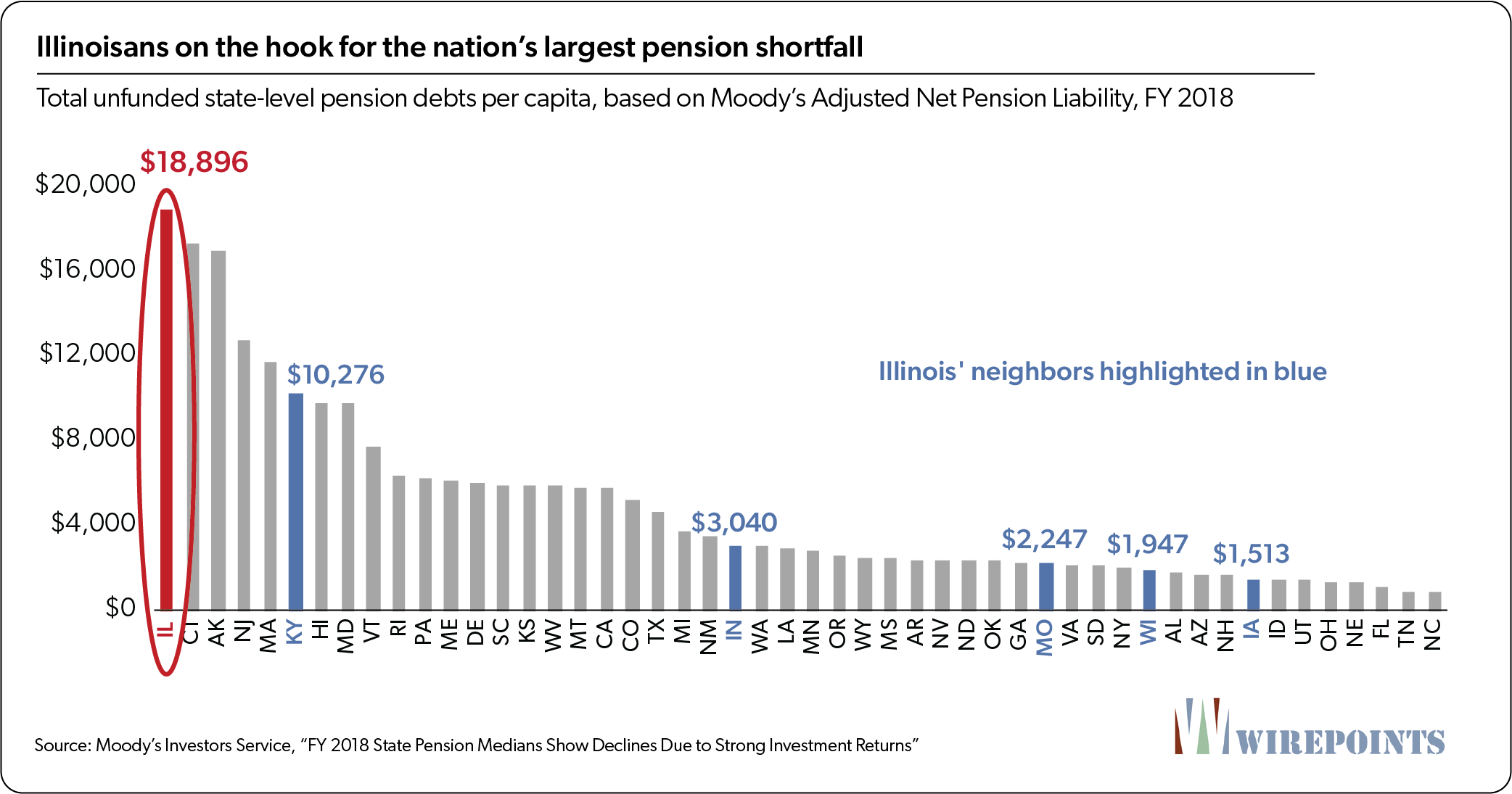

The same can be said when debts are measured on a per capita basis. At nearly $19,000 per person ($50,000 per household), Illinoisans’ pension debt burden is six times larger than the national average. Compared to residents in neighboring Wisconsin and Iowa, Illinoisans’ burden is 10-12 times larger.

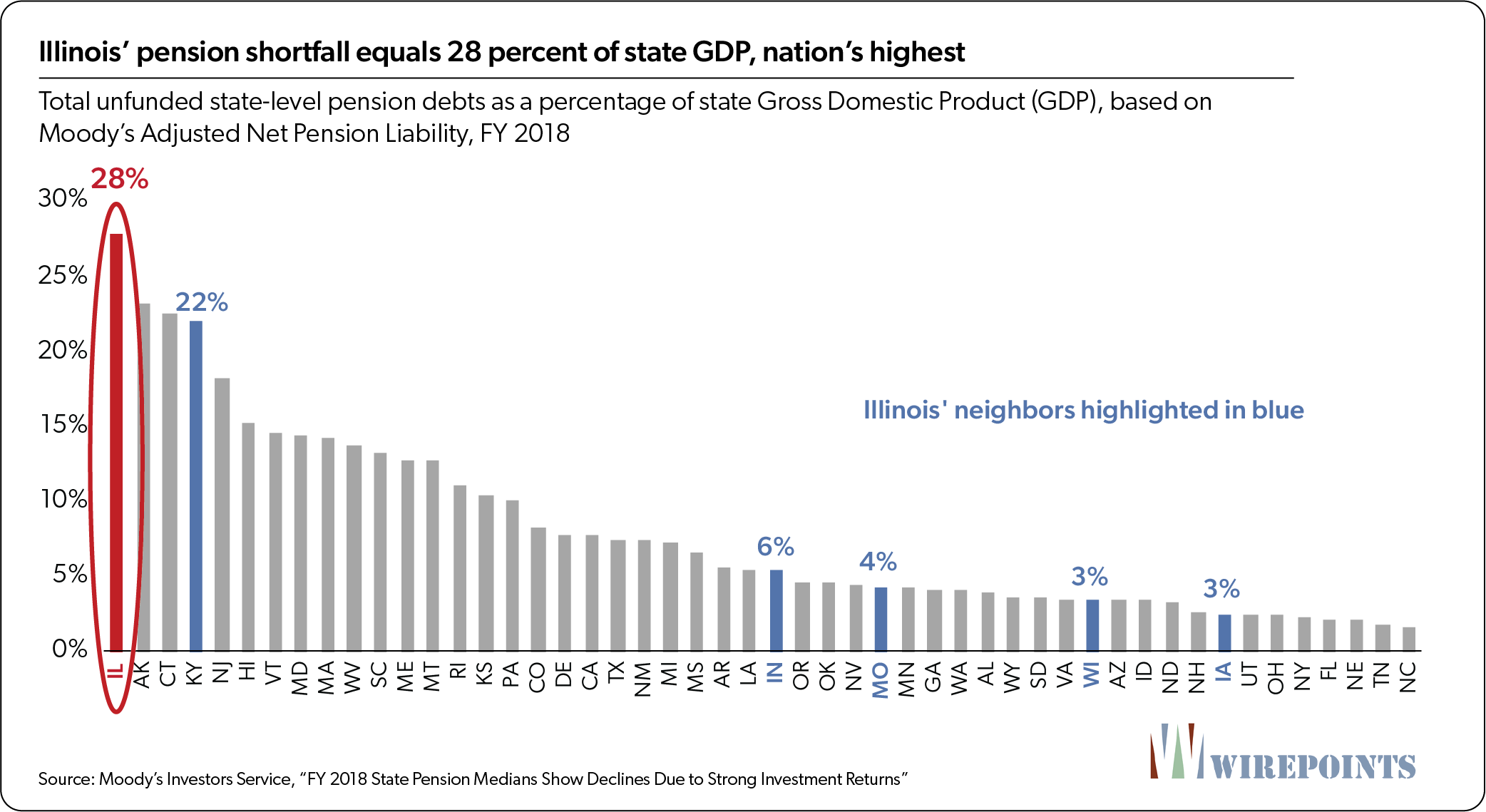

That burden is overwhelming the state’s economy, with state level-debts alone now equivalent to 28 percent of the state’s annual GDP. In most of Illinois’ neighboring states, the debt is just 3 to 6 percent of the economy.

State-level retiree health insurance liabilities add to Illinois’ debt load. According to Moody’s, as of 2018 each Illinois household was on the hook for more than $11,700 in official unfunded retiree health insurance benefits, the nation’s 6th-most. That amount is more than double the national average and six times what Kentuckians owe.

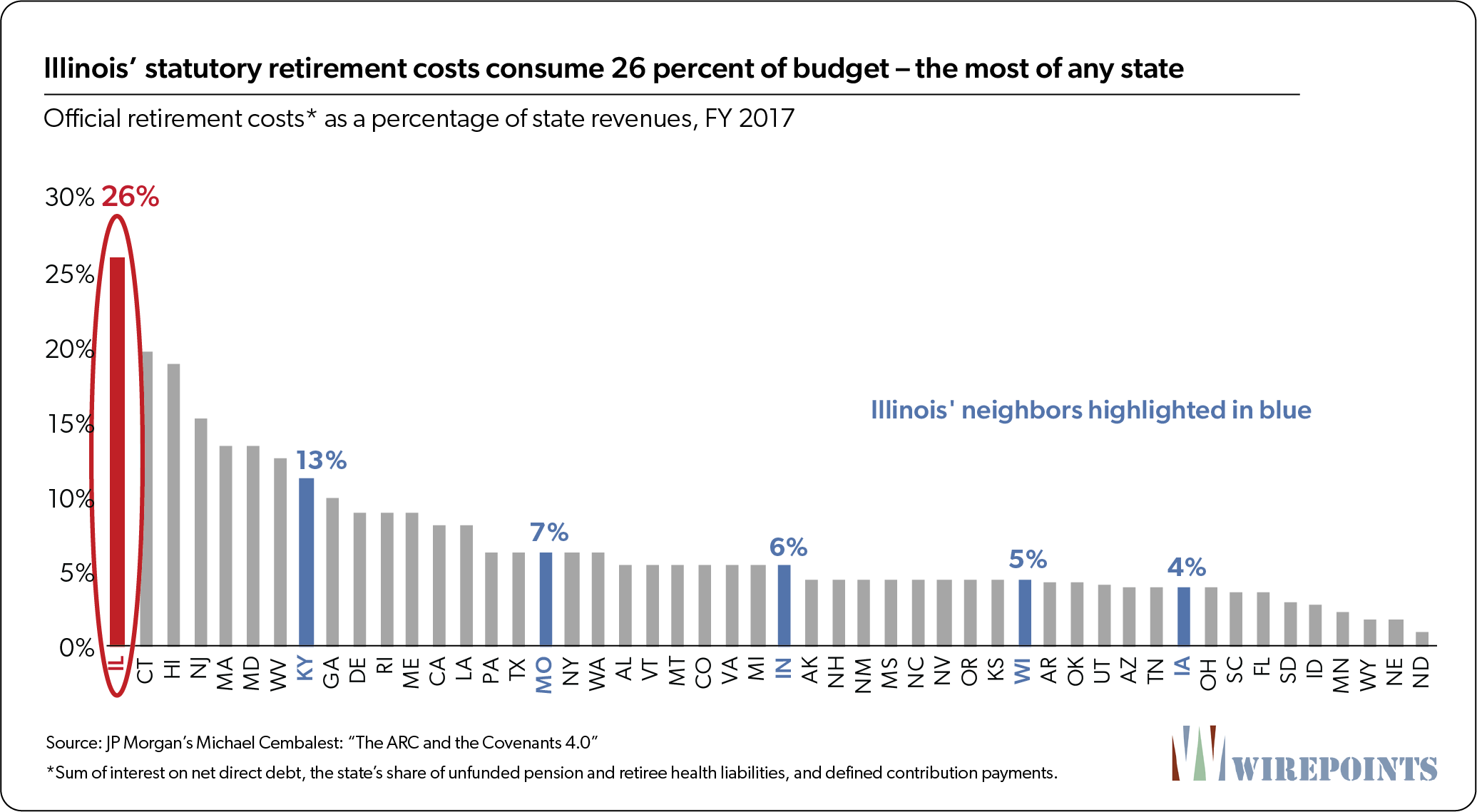

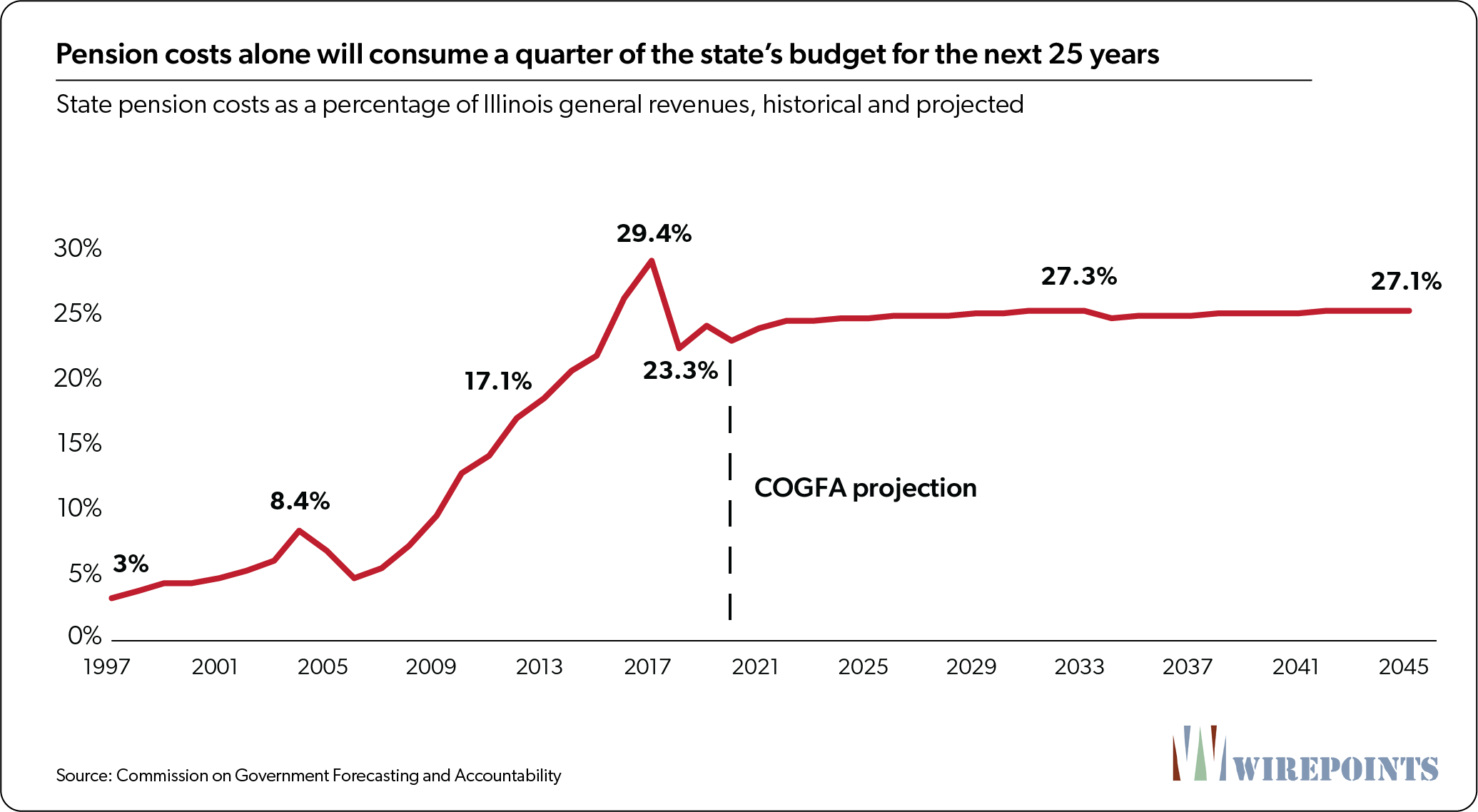

And it’s many times more than what households in states like Wisconsin and Indiana are burdened with. The combined cost of those retirement debts already consumes more than a quarter of Illinois’ state budget – the most of any state nationally.

That has crowded out new spending on other core priorities such as education. Billions of state appropriations for K-12 and higher education dollars are being spent on pension costs instead of students in the classroom.

And it’s still not enough. Illinois’ retirement crisis continues to grow because the state can’t afford to pay what it really should to get its retirement costs under control. J.P. Morgan’s Michael Cembalest calculates that more than half of the state’s budget is needed to make pensions and retiree health insurance actuarially sound.

That’s the largest share of any state budget, by far. Yet again, Illinois is the nation’s extreme outlier.

The problem of crowd out is not going to go away. The Commission on Government Forecasting and Accountability projects that the state’s statutory pension costs alone will consume a quarter or more of the budget for the next 25 years. And that’s the official, rosy estimate. Additional revisions to the pension funds’ assumed investment rates of return and other actuarial assumptions will likely cause official pension costs to consume even more of the budget over the next two decades.

Illinois simply can’t compete with its neighbors on services and tax levels when over a quarter of its budget is perpetually consumed by pensions. The extreme cost of Illinois’ retirement debts has also pushed residents’ overall tax burdens to punitive levels.

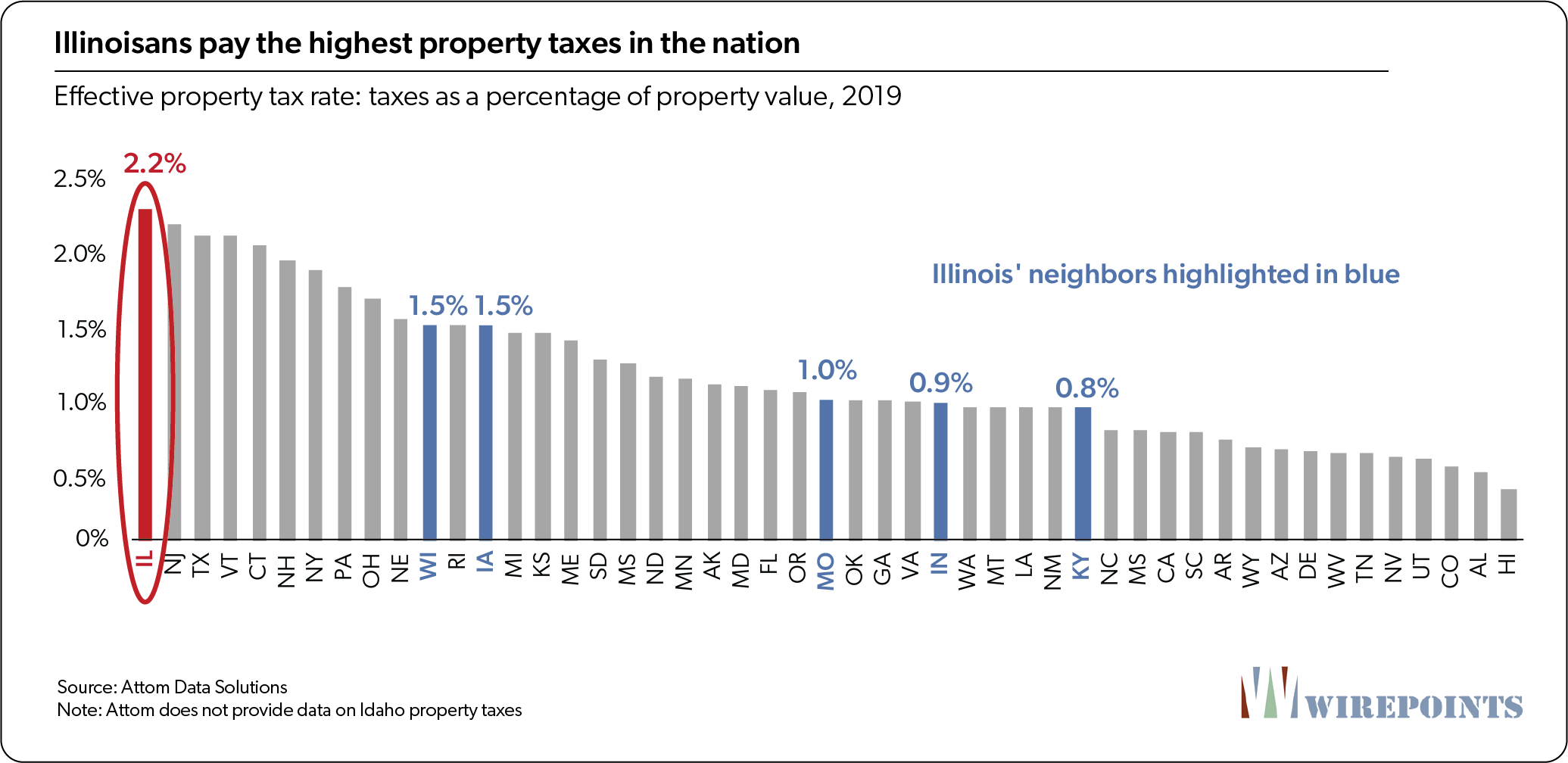

As pension costs have grown to consume nearly half of what the state appropriates on K-12 spending, local school districts have raised local property taxes to pay for Illinois’ bloated educational bureaucracy. Add to that the costs of Illinois’ local public safety pension crisis and that’s helped drive the state’s property tax rates to the highest in the nation – more than double what residents in Missouri, Indiana and Kentucky pay.

That statewide average doesn’t do justice to how destructive property taxes have become for some homeowners. In many Illinois communities, particularly in Chicago’s southland area, effective property tax rates have reached confiscatory levels of 5 percent or more.

According to Cook County Treasurer Maria Pappas, more than 57,000 Cook County property owners were delinquent on their taxes in 2019. Many are at risk of losing their homes.

But while property taxes impose the most public and painful burden in Illinois, they are only a part of the state’s overall tax structure. Illinois’ overall state-local tax burden is one of the nation’s highest. Kiplinger and Wallethub both rank Illinois’ tax burden as the highest/worst of any state, with Kiplinger calling Illinois the “Least Tax-Friendly State” in the nation. The Tax Foundation says Illinoisans are burdened by the 5th-highest taxes in the nation.

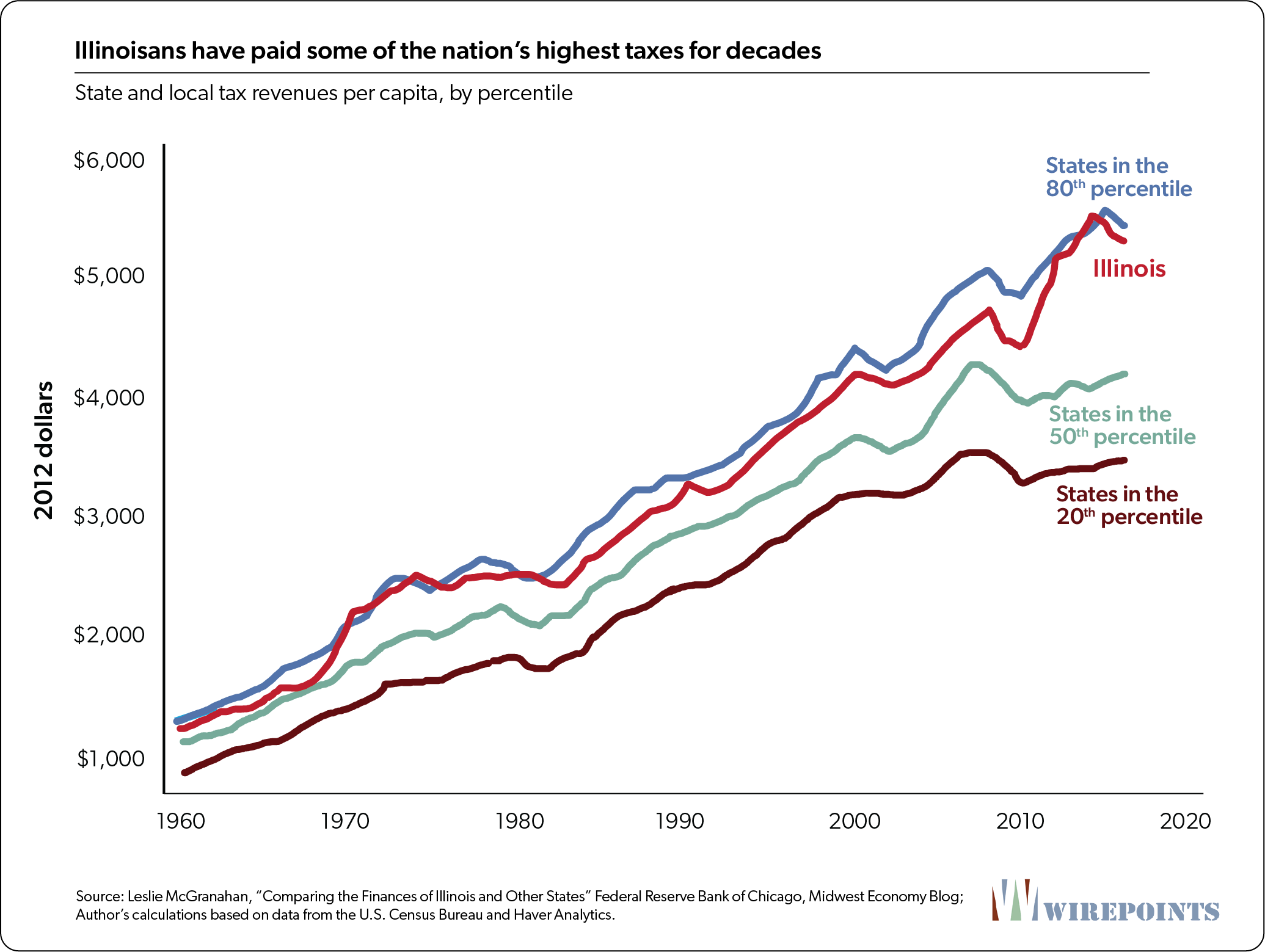

Federal Reserve Bank of Chicago economist Leslie McGranahan goes further, saying Illinois’ combined tax burden has been high for decades. McGranahan says Illinois has consistently ranked near the top of all states for state and local tax revenues per capita – tracking closely with the 80th percentile (the country’s top 10 states). Illinoisans have been paying more in total taxes than residents in most other states for the last 60 years.

A crisis of confidence

Illinois’ damaging budget crowd out and taxes – and the expectations for even more of both – have created a crisis of confidence in Illinois.

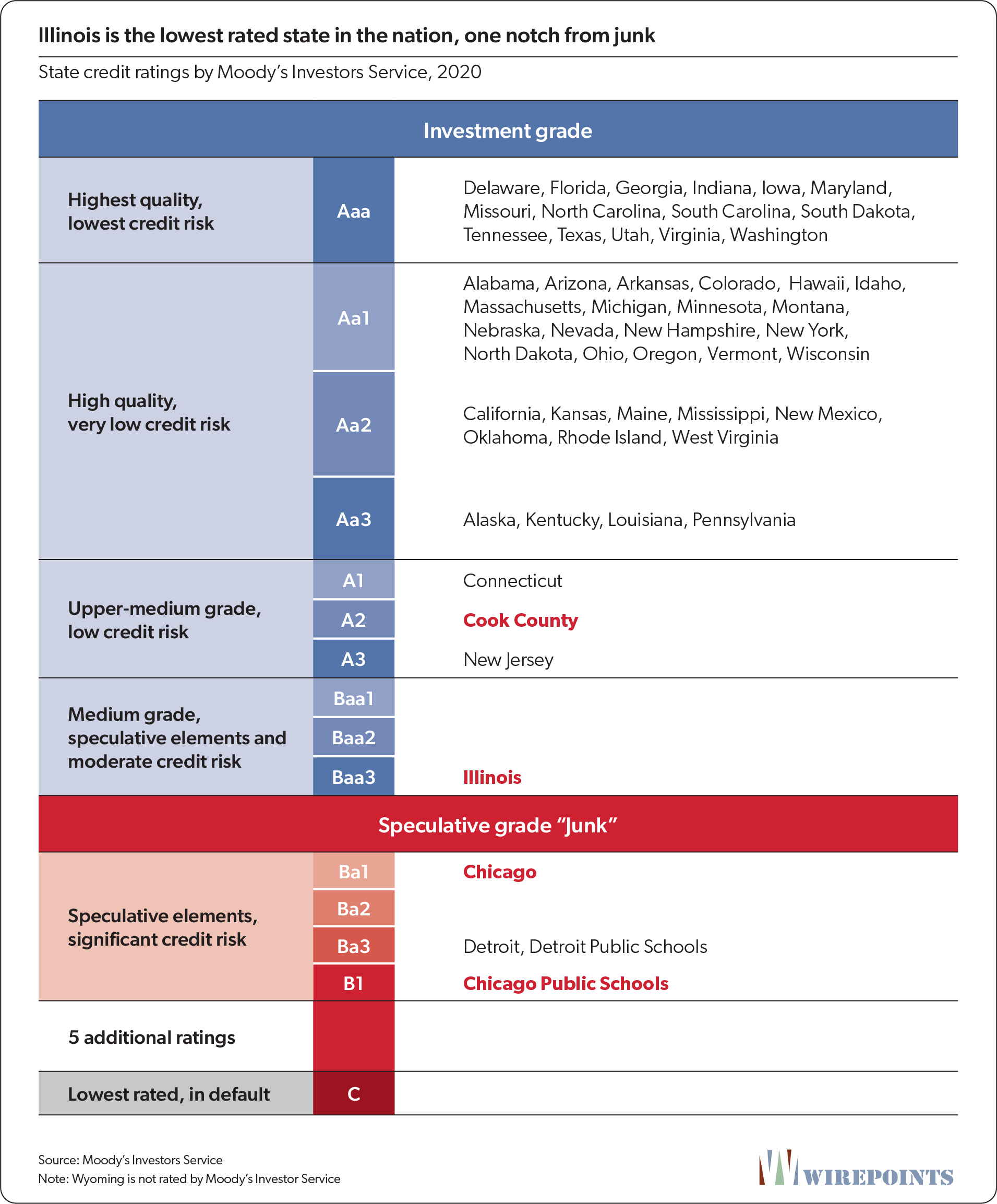

The state’s credit rating is arguably the most comprehensive indicator of Illinois’ financial health. It has collapsed after 22 downgrades from the nation’s three major ratings agencies over the past 11 years.

Moody’s Investors Service, S&P Global Ratings and Fitch Ratings have each downgraded Illinois to just one notch above junk, the lowest rating of any state. All three have also assigned a negative outlook to Illinois, warning of future downgrades. No state has ever been rated junk.

The City of Chicago is already rated one notch into junk by Moody’s, while Chicago Public Schools is four notches into junk. Cook County continues to be investment grade, with an A2 rating, but its rating is stuck between New Jersey and Connecticut, the nation’s two worst-rated states excluding Illinois.

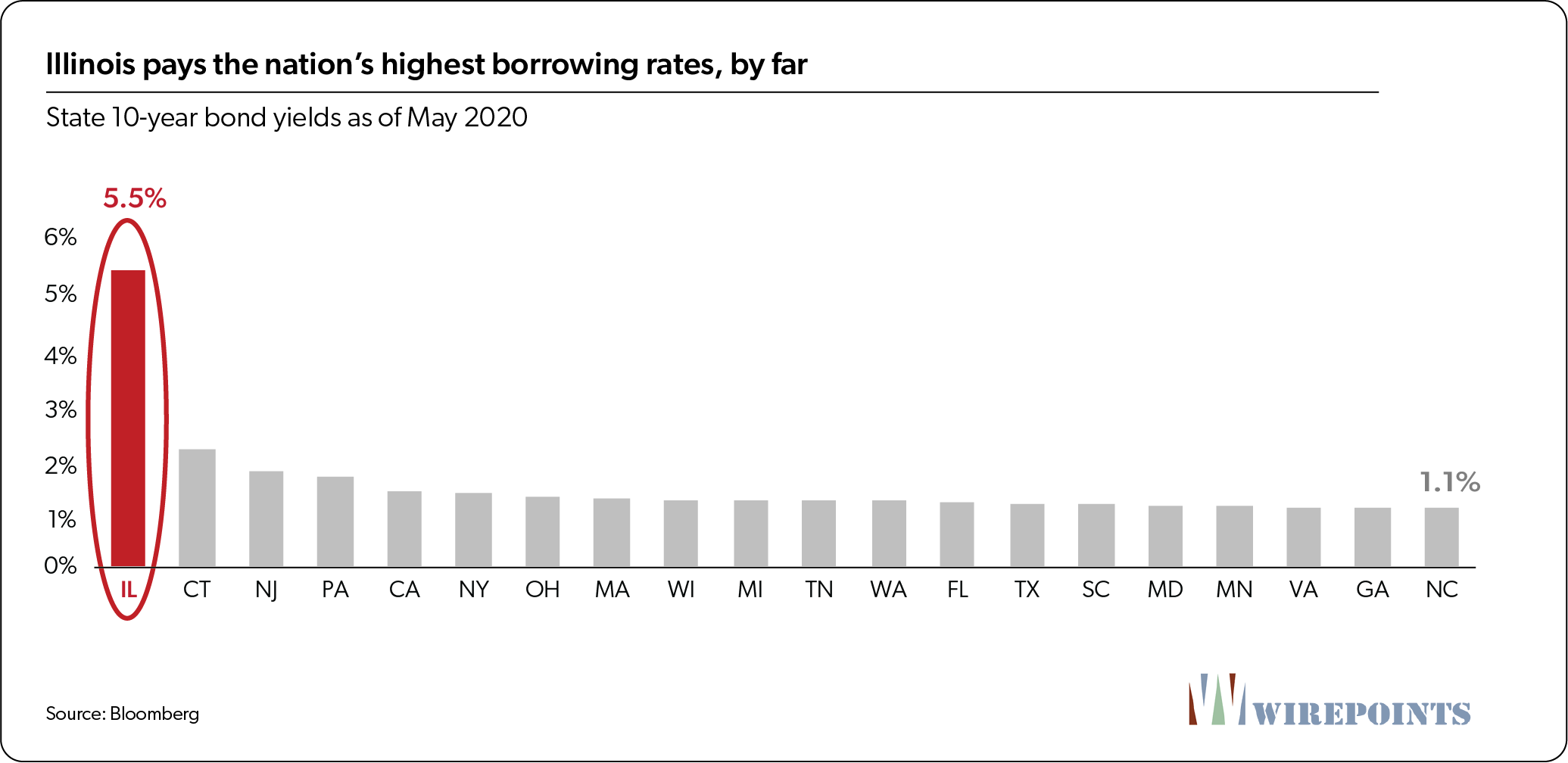

The state’s low rating has resulted in punitive borrowing costs. Illinois pays interest rates on its debts that are multiple times higher than other states. At over 5.5 percent as of May 2020, Illinois’ rate is now five times the 1.1 percent rate it costs AAA-rated states to borrow.

The lack of confidence is costing Illinois jobs and investments as businesses stay out of the state. For example, Warren Buffett says he wouldn’t relocate a business to a place like Illinois:

“In the public sector, you know, it’s a disaster…If I were relocating into some state that had a huge unfunded pension plan, I’m walking into liabilities…And those are big numbers, really big numbers…And when you see what they would have to do – I say to myself, ‘Why do I want to build a plant there that has to sit there for 30 or 40 years?’”

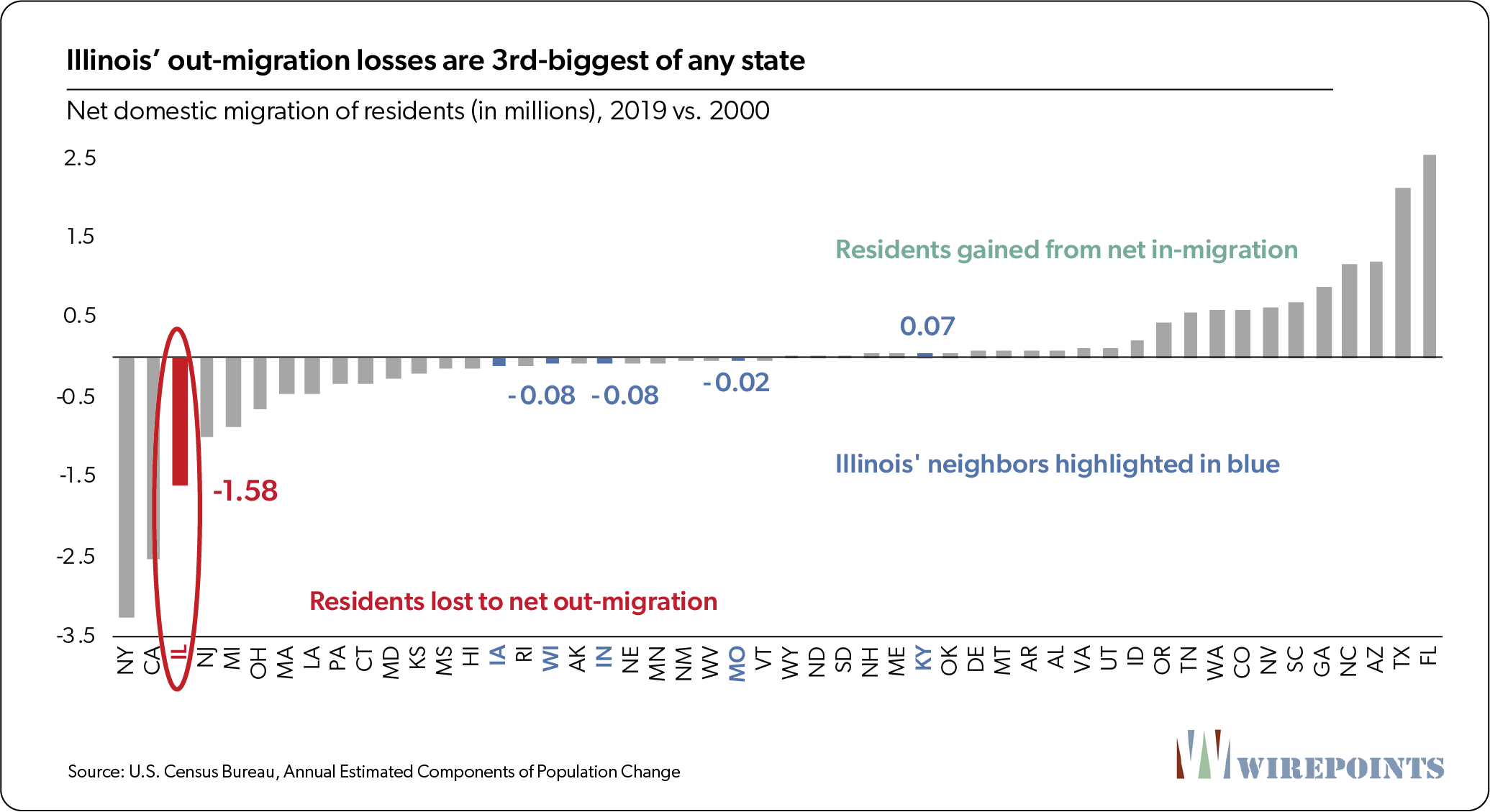

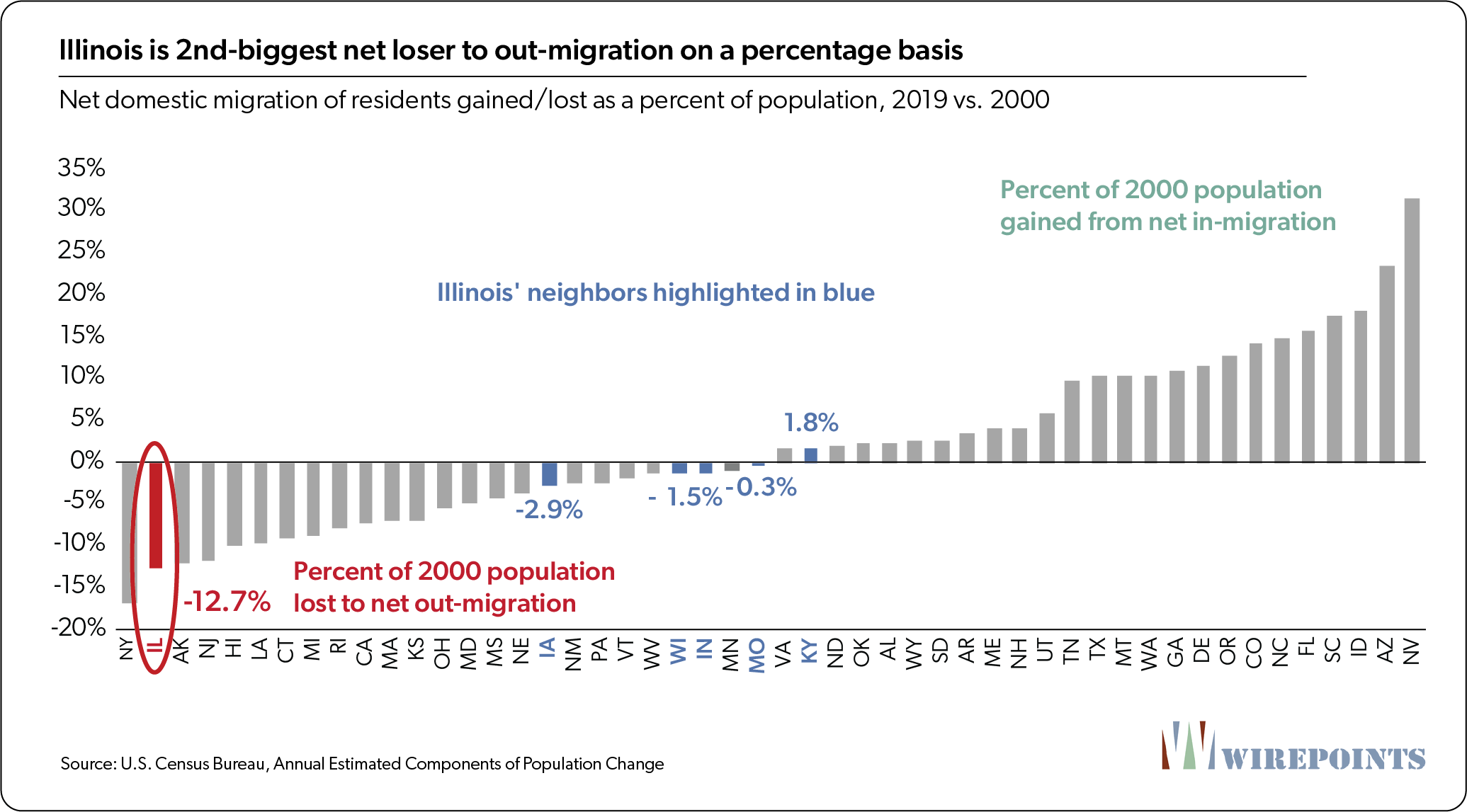

Illinoisans have expressed their own lack of confidence in Illinois by voting with their feet. U.S. Census data show that a net of 1.6 million Illinoisans have moved out of this state since 2000. Only New York and California lost more people. In all, domestic out-migration from Illinois resulted in a net loss of almost 13 percent of the state’s population as of 2000.

Those losses aren’t normal, even for a cold weather state in the Rust Belt. Neighboring states like Indiana, Wisconsin and Iowa have seen far smaller out-migration losses both in nominal and percentage terms.

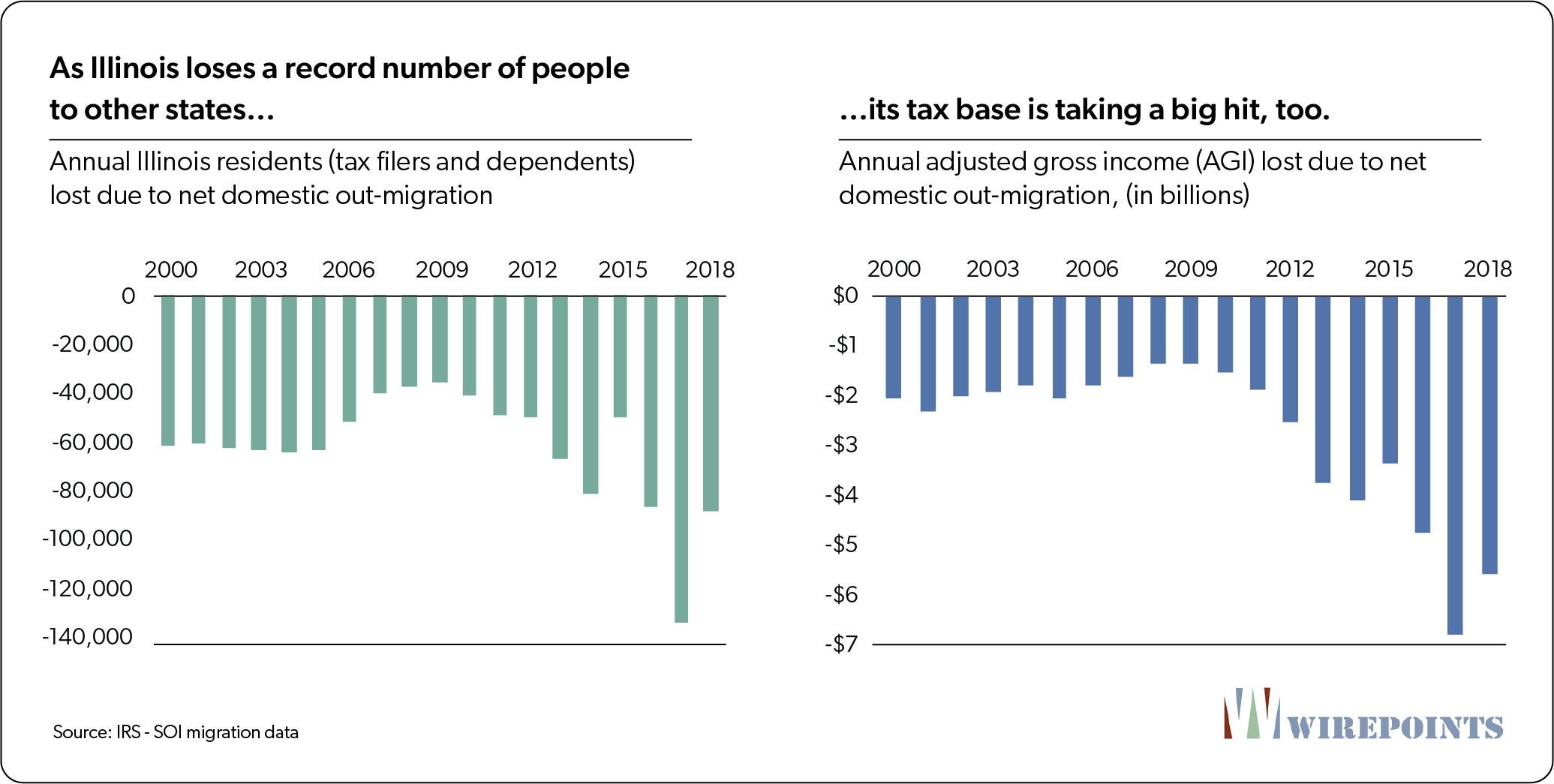

And as residents have left, they’ve hurt Illinois’ tax base. According to domestic migration data from the Internal Revenue Service, Illinois has lost an average of 62,000 tax filers and their dependents to other states every year since 2000. On average, Illinois lost $2.8 billion in adjusted gross income (AGI) due to out-migration annually.

Those numbers have ramped up in recent years as Illinois’ crisis has deepened. Net annual losses of residents have exceeded 80,000 while AGI losses have topped $5 billion.

The impact of losing those residents and their income is even bigger than it first appears. One year’s worth of losses don’t just affect the tax base the year they leave, but also all subsequent years. The losses build on each other, year after year. Add up the compounded losses since 2000 and Illinois’ cumulative AGI loss totals $410 billion.

The taxes lost as AGI has left have contributed to the state’s deepening fiscal woes. Illinois’ record losses to out-migration have been just one part of the state’s overall demographic collapse.

Net foreign immigration to Illinois has fallen by half since 2001. And the state’s net natural increase (births minus deaths) is down more than 50 percent.

All those demographic factors combine into a single fact: Illinois is shrinking. There are 170,000 fewer people in Illinois today than in 2010. No other state lost as many people and, in fact, only four states nationally lost population over that time period.

A falling population has perpetuated Illinois’ downward spiral. Lower demand for homes, in tandem with growing debts and rising taxes, has pushed real home values down. U.S. Census Bureau data show Illinois median home values have grown just 11 percent since 2005, the 6th-worst growth nationally. That’s far short of inflation, which was up 30 percent over the same period.

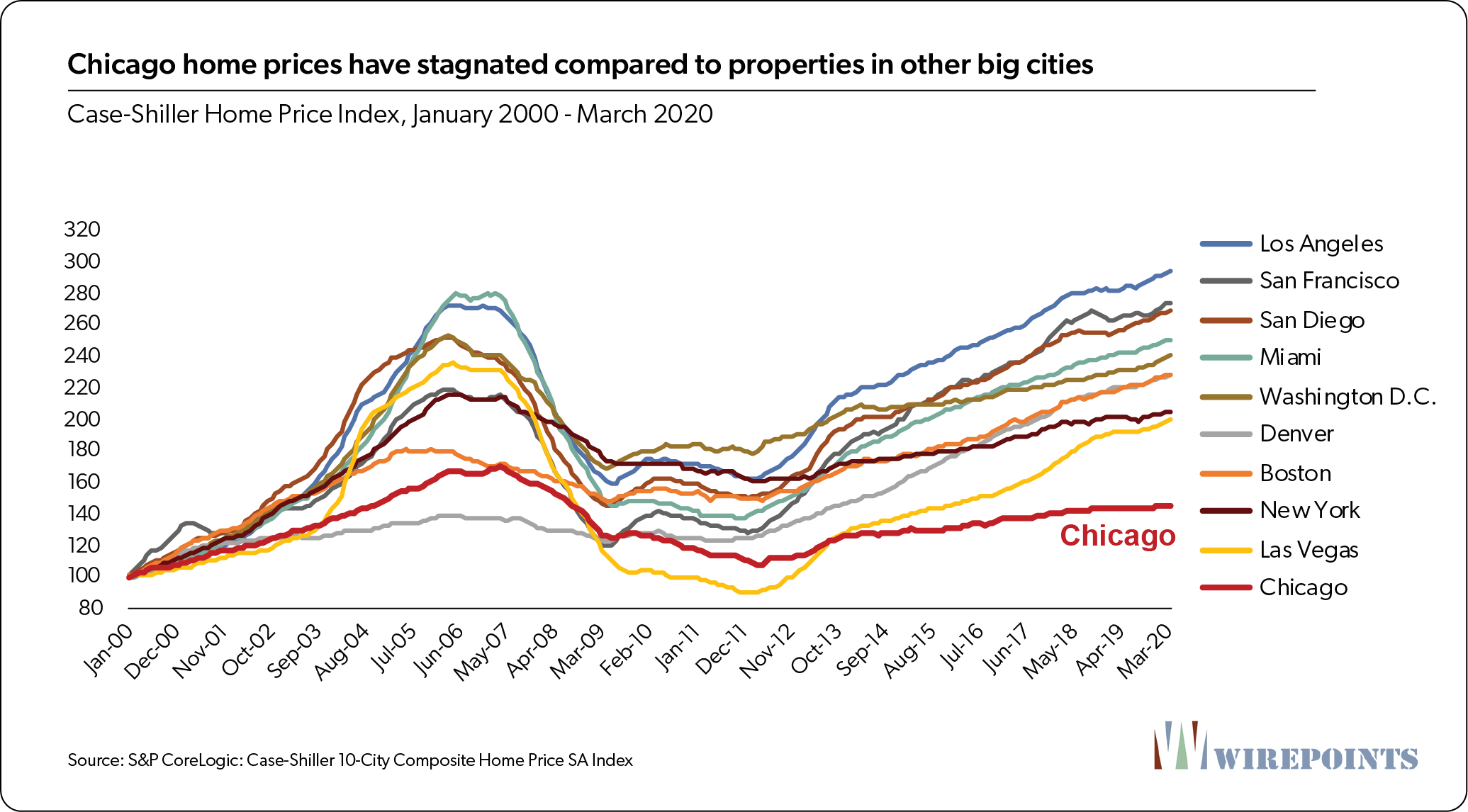

Chicagoans, in particular, have been hit hard since 2000 when it comes to their home values. Windy City residents would have been far better off today if they’d owned property in any of the other nine cities that make up the Case-Shiller 10-City Composite Home Price Index.

Chicago home prices have grown just 44 percent since 2000. By comparison, inflation was up 46 percent over the same time period. Meanwhile, home prices in Los Angeles grew four times those in Chicago, or 181 percent. Prices in Miami, up 143 percent, and Washington D.C., up 130 percent, have grown three times more than those in Chicago.

All these facts reflect Illinois’ outlier status before the COVID-19 crisis. The damage inflicted by the virus and the economic shutdown will inevitably make those numbers even worse.

Illinois’ per capita debts are overwhelming

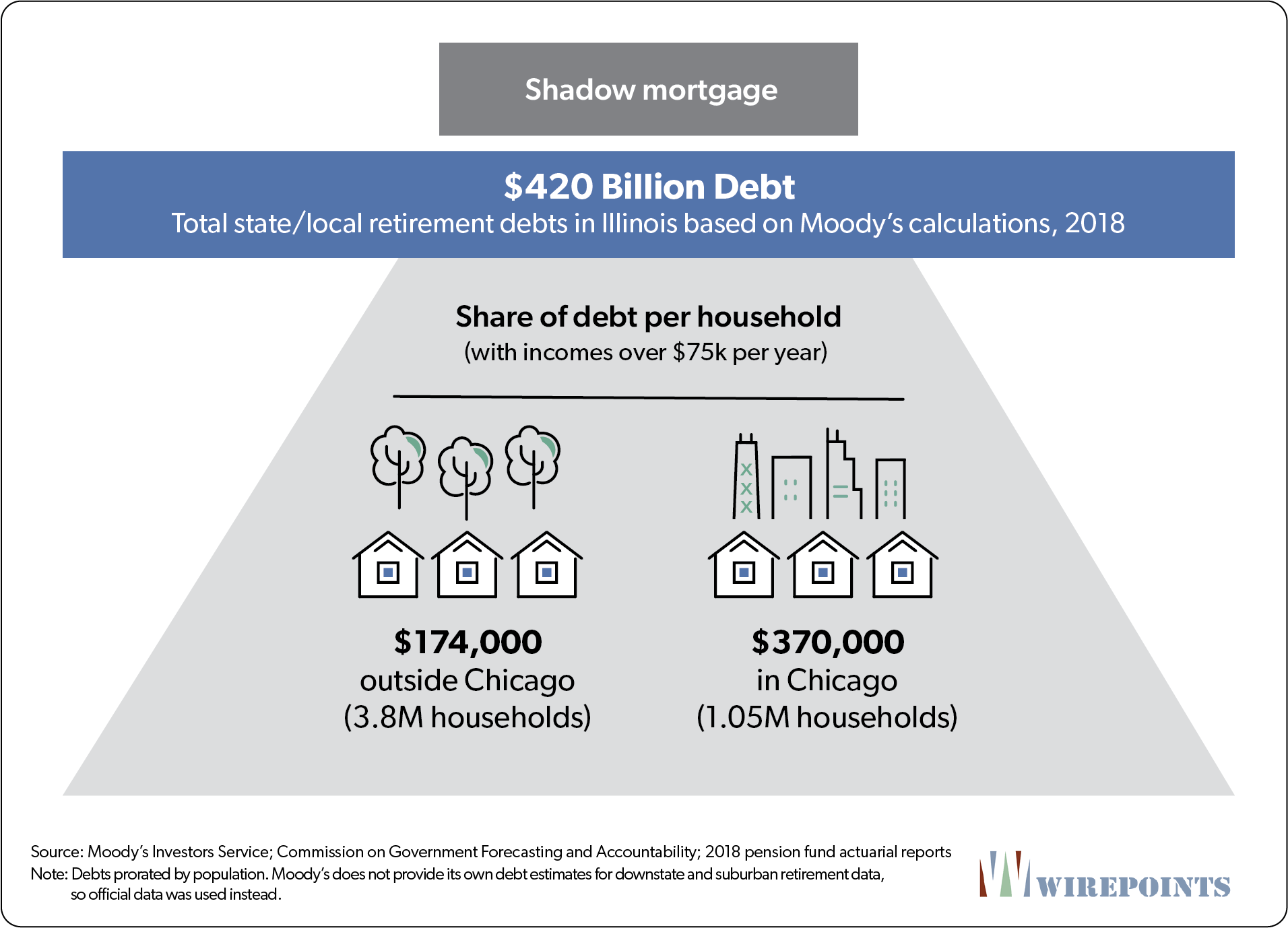

Another way to understand the depth of the retirement crisis is to look at Illinois’ $420 billion in Moody’s calculated retirement debts on a per household basis. (See the Appendix for a full breakdown of the $420 billion.)

Residents in the City of Chicago are burdened with $141 billion of those retirement debts. That’s the total overlapping city, county and state debt, based on Moody’s calculations, each Chicago household is saddled with. Divide that shortfall between the city’s one-million-plus households and the burden works out to $135,000 each. Call it a “shadow mortgage.”

Take the remaining $279 billion in debt and divvy it up among the 3.8 million households outside of Chicago, and their burden amounts to $74,000 each.

The true household burden is far larger

The reality is many Illinois families don’t have the means to contribute toward Illinois’ retirement shortfalls. Nearly 15 percent of all Illinoisans are in poverty and just 44 percent of Illinois households make more than $75,000 – a proxy for which households are more capable of taking on a shadow mortgage.

When the burden of that $420 billion debt is placed solely on those households earning $75,000 or more, Chicagoans are saddled with $370,000 each. And non-Chicago households are on the hook for $174,000 each.

The amounts are overwhelming and will only get worse as Illinoisans continue to escape that shadow mortgage. As more Illinoisans leave, the debt on those that remain will grow even larger.

Conclusion

Illinois’ outlier status isn’t just a grim anecdote. Illinois’ reputation as financially irresponsible has serious consequences, encapsulated in its near-junk status and its record flight of residents.

The state has reached the point where gimmicks used to avoid real reform – the same ones that landed Illinois its rating – are no longer available. The impact of COVID-19 has only further restricted the state’s options. Borrowing any meaningful amount, without additional federal backing, will be extremely difficult. Tax hikes will inflict additional harm on residents and businesses that have been crippled by the economic shutdown. Shorting the pension funds will trigger even more punishment from rating agencies. And reamortizing pension debts further into the future won’t be accepted by the agencies either.

The state’s retirement debt is insurmountable without significant changes to Illinois pension systems. But before a solution can be adopted, a proper diagnosis of the problem must be performed.

The second part of Wirepoints’ four-part series will cover how overpromised benefits, and not underfunding, has been the main cause of the state’s retirement crisis. And it will show how overly generous pension and retiree health insurance benefits have driven those unaffordable promises.

Appendix: The Numbers

Summary of Illinois’ state and local retirement shortfalls

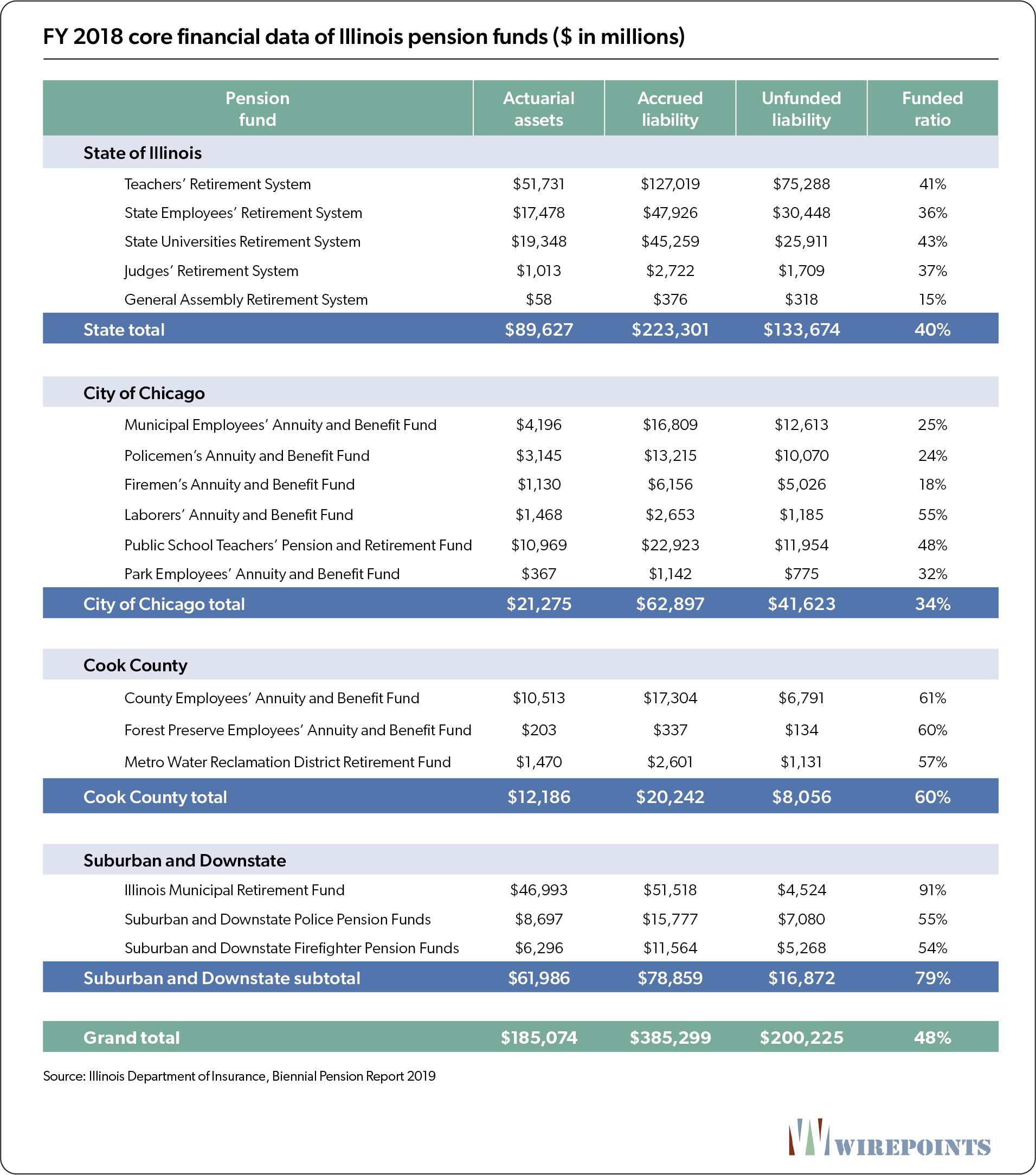

Illinois had $288 billion in official state and local public sector retirement shortfalls in 2018. That was made up of $134 billion in unfunded pension debt for its five state-run pension funds.

Additionally, Illinois has a $56 billion retiree health insurance shortfall and $11 billion in pension obligation bonds. Local government retirements were short another $87 billion. As large as those amounts are, the official numbers vastly understate the true size of Illinois’ debts.

Official government numbers use rates near 7 percent to discount future obligations, while true market rates are far lower.

Financial experts – from Nobel prize winners like Stanford’s Prof. William F. Sharpe and University of Chicago’s Prof. Eugene Fama to other academics including Hoover Fellow Joshua Rauh and Jeremy Gold – criticize the use of inflated discount rates.

Moody’s Investors Service uses more appropriate discount rates based on AA-rated corporate bonds, resulting in pension shortfalls that are far higher than official estimates. The discount rate used by Moody’s for its 2018 calculations was 4.14 percent.

When Illinois’ debts are added up based on Moody’s analysis, Illinoisans are subject to $420 billion in state and local retirement shortfalls. That’s a 46 percent increase in the debt Illinoisans are on the hook for when compared to official numbers.

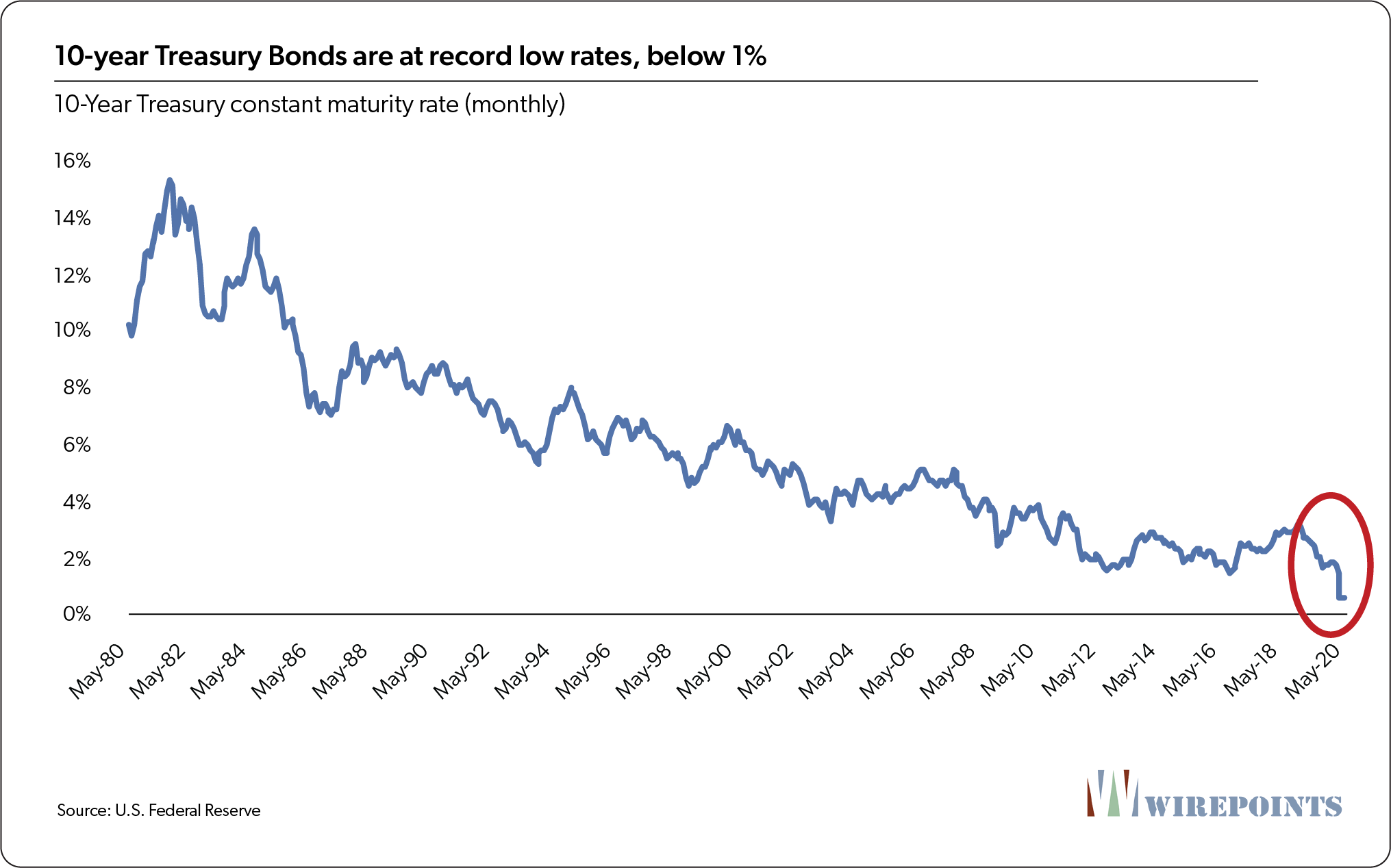

Illinois’ total debts will get far larger, however, as Moody’s updates its calculations with even lower discount rates. As of April 30, 2020, that rate had fallen to 2.8 percent, a reflection of the continued collapse in long-term yields. Structurally, those rates have fallen in tandem with the 10- year U.S. Treasury rate, which is now below 1 percent.

Summary of Illinois’ pension fund finances

Summary of Illinois’ pension fund beneficiaries and benefits

Summary of Illinois’ state retiree health insurance funds

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

Politicians caused the pension problems by putting young workers on the pension to reduce their work force. It was an outrage then and now.

Touché! Wirepoints’ Ted, John and Mark are telling the truth! I’d say a good, actual discount interest rate is close to halfway between 7.0% and 4.1%, which is 5.5%. It’s the “slightly on the conservative side” of the net (after all expenses paid from the trust funds) return on assets, given a trust fund invested prudently. Sure the net return MIGHT be 6 or 7%, but it’s safer and more prudent to assume 5.5%. That’s what I assume when doing projections for how much can be spent for MY own retirement assumptions, and the basis for my book to dispel… Read more »

The proponents of the progressive income tax are like the owner of a boat with a hole in it. Instead of closing the hole, he demands bigger buckets to bail with. If given the tax, they’d just blow it like they’ve blown all the other increases.

Since I get a pension from the Illinois Municipal Retirement Fund, I eagerly read your article. My pension fund is 91% funded! I paid larger amounts for my salary into my fund as did the public libraries I worked for. I do NOT get any kind of insurance benefit. I deserve and have earned my pension. To lump a well managed and well funded fund in with some of these others is irresponsible and just plain WRONG. I don’t want MY well run fund looted by you or anyone else trying to take it away. What do you want small… Read more »

Don’t forget, too, the IMRF is funded by the municipalities that participate, not the State of Illinois

No one here is proposing, and have never heard of a proposal, to loot the IMRF or any pension fund (take money out of the fund and divert it to another purpose). IMRF is in the article simply because it is one of the public sector pension funds in Illinois. There are many possible scenarios that can occur which would cause one to receive less than 100% of a public sector pension payout in the future though, even without the government “looting” the fund. Many of events are outside any politician’s direct control, such as a prolonged recession, depression, stock… Read more »

“Many of events are outside any politician’s direct control, such as a prolonged recession, depression, stock market crash, bond market crash, mass exodus out of Illinois, investment returns less than projected, etc.” You are making the common mistake believing that the level of pension funding has anything to do with pensioners receiving their checks. The way it is currently set up the funds can run completely dry and the state is on the hook for making the pension payments. If the funds run dry bondholders and pensioners are first in line to collect payment before other “necessary” expenditures. There is… Read more »

Also, someone (you?) mentioned a week or two ago that the general assumption most here make is that only public employee and pensioners would be hurt in a state bankruptcy if it were allowed. That’s only an assumption and not likely the case. It would also put in jeopardy the secuirty of those receiving income from IL bonds and those of its lower-level units. It might well also cause a reduction in any other contractual situation the state has created with any business whatsoever, and there are lots of those that would negatively affect the public at large one way… Read more »

I made no such “common mistake” assumption.

The point was there is no guarantee the State of Illinois will honor the “state guarantee” in the state constitution, due to many possible scenarios.

No one can predict the future with 100% certainty.

Your common mistake was conflating actuarial assumptions with the states requirement to pay. You referenced a depression, stock market decline, bond market decline, investment returns less than expected, etc… This comment makes it appear that if the funding of her pension goes down because of the things you mentioned then she may get less than 100% of her pension. That is not the case. Until the state can no longer increase their total tax revenue, Joy will continue to get her pension at 100%. The moment the state loses so many taxpayers that they can’t collect more revenue to cover… Read more »

I already stated the State has no plans to loot any pension fund.

So you are making the point that if the fund depletes its assets, the state will convert to pay as you go, as long as it is able to do so?

If so there is that clarification.

Obviously if it gets to that point its because actuarial assumptions were not met.

I don’t think your opinion is far off the mark at all but might have thought so a couple of years ago in tamer times. But, we live in strange time now and probably to the detriment of many such things formerly considered absolutely assured. No one can predict the future with nearly any certainty at the present time. All it takes is a few “slick willy” lawyers to read and promote laws in a new, unique way and what’s “promised” disappears overnight. That’s how it is in the current era of Pres. Trump and AG Barr apparently at the… Read more »

How many years did the state fail to pay its share of pension costs? How much did the state borrow from TRS and not pay back? Reform is needed but there is a lot of background not covered by charts and graphs. Where were the fiscal people when the state said they would pay the local district share of pension money and salaries started climbing?

That comes next week. You’ll find out then that Illinois’ problem has never really been about Illinois failing to pay, its been about politicians’ overpromising.

It’s nice to see Wirepoints getting back to it’s primary message and away from the current covid distraction. Wirepoints in a followup will undoubtedly explain how Illinois can fix the mess. Whatever the fix is, it doesn’t matter, because liberal/democrat voters prefer to be ignorant and will never support anyone presenting reality. For those of you still on the fence about leaving Illinois, consider all 50 states as competing businesses. There will be winners and losers. That’s the nature of competition. The stock price of Illinois is in a free fall while states like Texas are seeing their stock price… Read more »

While this focuses on what discount rate the pension systems should use, what about our pension systems using an investment rate of return that is equal to the discount rate? I thought the target funding percentage was dependent on those two rates and, if equal, 100% should be the target funding level. Our pension systems target funding is 90%. There are others who are pushing 70% or 80%. But none of those targets jive with our discount and investment rates.

I thought that’s how pension accounting works. Maybe some pension experts here can chime in.

be nice if this was sharable

keep informing all the people, great job!!!!!!

Well done Wirepoints! This is extremely thorough, and thoroughly depressing…maybe it will open some eyes.

President Trump and Senator Micth McConnell should draft legislation for States to file federal bankruptcy. This would be a States’ choice, and not a mandate.

I know more is coming, but perhaps adding in a proforma on Pritzker and Madigan’s tax hike(s) could crystalize things a little better. I give the tax hike at least a 50/50 chance – many people who would vote ‘NO’ have left the state.

Does the debt per household take into account the percentage of state and local retirement debt allocated to commercial, industrial, railroad etc properties?

The debt isn’t really allocated to those properties. They are just part of the tax base.

Well the point I was getting at wais absent a disclaimer the retirement debt debt per household metric then leaves the average person with the wrong impression since corporations etc. also pay taxes.

Ah, I see. But it is important to remember that businesses ultimately pay no taxes. People end up bearing them — business owners, employees, suppliers and customers. Yes, some of that gets exported out of the city, but some gets imported, too, so we think the fair way to picture it is per household.

So the the IDOR Business Income Tax Rate, policies, and state laws result in the State receiving revenue from business.

Some of that business income tax revenue will be used to reduce retirement debt which will reduce the amount of debt per household.

Yet the businesses ultimately pay no taxes.

https://www2.illinois.gov/rev/research/taxrates/Pages/income.aspx

The per household metric implicitly highlights a key fact. Only a small portion of taxpayers – perhaps those at 200k a year and over – are capable of paying any additional taxes in amounts that could even put a small dent in the debt. And while I agree that we should not ignore taxes businesses and corporations pay, in the face of rising taxes, corporations will always find a way to defer or avoid taxes, with levers to pull that average wage earners cannot utilize (this from the ate Martin Ginsburg, my tax professor and spouse of our current Supreme… Read more »

The point was to make it clear that business are not included in the per household metric.

If the people are getting taxed to death and the business and corporations are largely spared as evident through net income or whatever measure(s), one would think sooner or later people will get so angry that there will be some sort of revolt, regardless of how many lobbyists the corporations employ.

Perhaps this is one reason the left is becoming more radical.

After all, it’s people that end up paying all taxes.

I know this piece is setting the background for further articles , but reading it one is immediately taken with what is to be done ? There are but two answers : hope for a Biden administration and D Congress to federalize the mess or some form of ‘bankruptcy’. There are no other alternatives : State led reform is never going to happen there are too many oxen to be gored in any state level reform. So the answer will have to come from elsewhere. BTW as bad as the economic fallout from the shutdown is/was, it does not seem… Read more »

The problem appears to be too large to be corrected by a federal bailout, assuming that Illinois would only receive a population-adjusted proportion of federal funds set aside for a state pension bailout.

“Biden administration and D Congress to federalize the mess or some form of ‘bankruptcy’. There are no other alternatives : State led reform is never going to happen”

Even if the federal government allowed some form of bankruptcy it would require the state of Illinois to initiate that bankruptcy. No such federal power is available to force a state into bankruptcy. If the states not on board then reform will never happen. You will need to win the hearts and minds of the voters of Illinois to change how business is done in this state.

I think Federal bailouts are a dead issue for Illinois given that Pritzker and Madigan have not shown any concern to fix the fiscal mess they created. Other states cut back on spending immediately – Pritzker increased spending!. Pritzker also owns the statewide lockdown – it was unwarranted and illegal. No, the rest of America doesn’t owe Illinois a thin dime.