Part 4: A Solution for Illinois' State Retirement Crisis

No material reform of any public pension in the State of Illinois is currently possible due to a strict interpretation of the pension protection clause in the state’s constitution. Yet those pensions are widely regarded as unsustainable in their current form and are the primary reason Illinois was approaching what the Wall Street Journal properly called an “inevitable financial collapse” – even before the current economic downturn.

In Part 3, Wirepoints discussed why the only readily apparent options to legally overcome the state constitutional obstacle to pension reform are federal bankruptcy or an amendment to the state’s constitutional pension protection clause.

Reformers and opponents alike regard bankruptcy as a last resort. But reform opponents, including the current administration, also categorically refuse to consider an amendment. They routinely claim that a state amendment followed by reforms would be voided under the Contract Clause of the United States Constitution, which prohibits contract impairment.

Part 3 showed why opposition to a state constitutional amendment is groundless. Reform opponents are wrong. Court decisions and expert legal opinions say they are wrong. The United States Supreme Court long ago laid out the standards for when contracts can be impaired. Those federal standards – the only ones that would apply after a state amendment – have been routinely applied to revise a variety of contracts. The vast majority of other states have either reduced benefits, raised employee contributions, or both, each of which Illinois refuses to consider. Recent experiences in Rhode Island and Arizona illustrate why the federal Contract Clause is not an obstacle.

To allow for reform, amendment wording must conclusively override the pension protection clause and all other state law issues. Suggested language was included.

Parts 1 and 2 showed why Illinois must reform its pensions if it is to restore fiscal stability and return the state to competitive levels of services and taxation. It includes details on the underlying causes of Illinois’ pension crisis, comparisons to other states that show the state’s extreme circumstances, and why pensions today are overpromised: benefit growth has far exceeded Illinois’ capacity to pay.

In this final part, Wirepoints presents various reform options that might be pursued after an amendment. It includes a baseline pension restructuring plan modeled on Illinois’ existing defined contribution plan run by the State University Retirement System. Our proposal has been scored by the state’s actuaries. The results are included herein.

Wirepoints’ baseline restructuring plan immediately freezes the state’s defined benefit plans. Stopping the growth in accrued pension promises and paying them off completely is the only way Illinois can guarantee an end to its public retirement crisis and assure retirees of what they will get.

Wirepoints’ proposal also includes changes to the state’s retiree health insurance benefits, an often ignored aspect of Illinois’ public retirement system. Going forward, state retirees would be required to pay for half of their health insurance costs – the national average for public workers – on a means-tested basis.

In addition, various other reform measures separate from Wirepoints baseline proposal were also scored by the state’s actuary. Those results are also included.

It should be noted that this series covers proposals only for the state’s pension and retiree health systems. However, most of the state’s 665 locally sponsored pensions also require changes. Local funds’ circumstances vary substantially, and may require different reform options than those presented here.

Illinoisans should not wait until Illinois becomes a failed state before finally demanding change. It is vital to reform the state now, while it still has assets and dynamism left, rather than delay until Illinois is a shadow of its former self.

he key goals of restructuring Illinois retirements

Wirepoints has made the case that pension reform is possible and necessary to restore Illinois’ finances. The questions that remain are: what should reform look like, and what should it achieve?

In the following sections, Wirepoints lays out a baseline restructuring for Illinois’ five state-run pension plans and the retiree health insurance plan for state workers, and provides a summary of the savings those plans provide. Savings of other potential reforms are also included. Illinois’ other retirement plans will each require separate proposals to match their unique circumstances.

Wirepoints’ core objectives in creating reforms are to:

- Reduce the state’s structural liabilities to help Illinois escape its downward spiral of growing debts and a shrinking population.

- Restore retirement security for state workers and retirees while protecting already-earned benefits to the extent possible.

- Help reestablish a competitive level of services, tax rates and economic growth for Illinois.

- Help ensure that Illinois’ most vulnerable citizens no longer suffer from a lack of core services and punitive tax increases.

- End the unfair Tier 2 system, where workers hired after 2010 are forced to subsidize the benefits of Tier 1 workers and retirees.

- Improve budget certainty for governments and taxpayers by turning future retirement contributions into known, predictable, fixed costs.

- Ensure that retirements are controlled by workers themselves, not Illinois lawmakers. Workers must receive flexible, portable retirement plans they own and control.

- Ensure that reforms are “reasonable and necessary” to comply with the U.S. Constitution’s contracts clause.

Other key considerations:

1. The Commission on Government Forecasting and Accountability (COGFA) engaged Segal, the state’s actuary, to score Wirepoints’ reform plans via a legislative request. The high costs of running actuarial scenarios limited the number and scope of potential reforms Wirepoints could fully explore. For that reason, the scoring included in this paper was limited as follows:

-

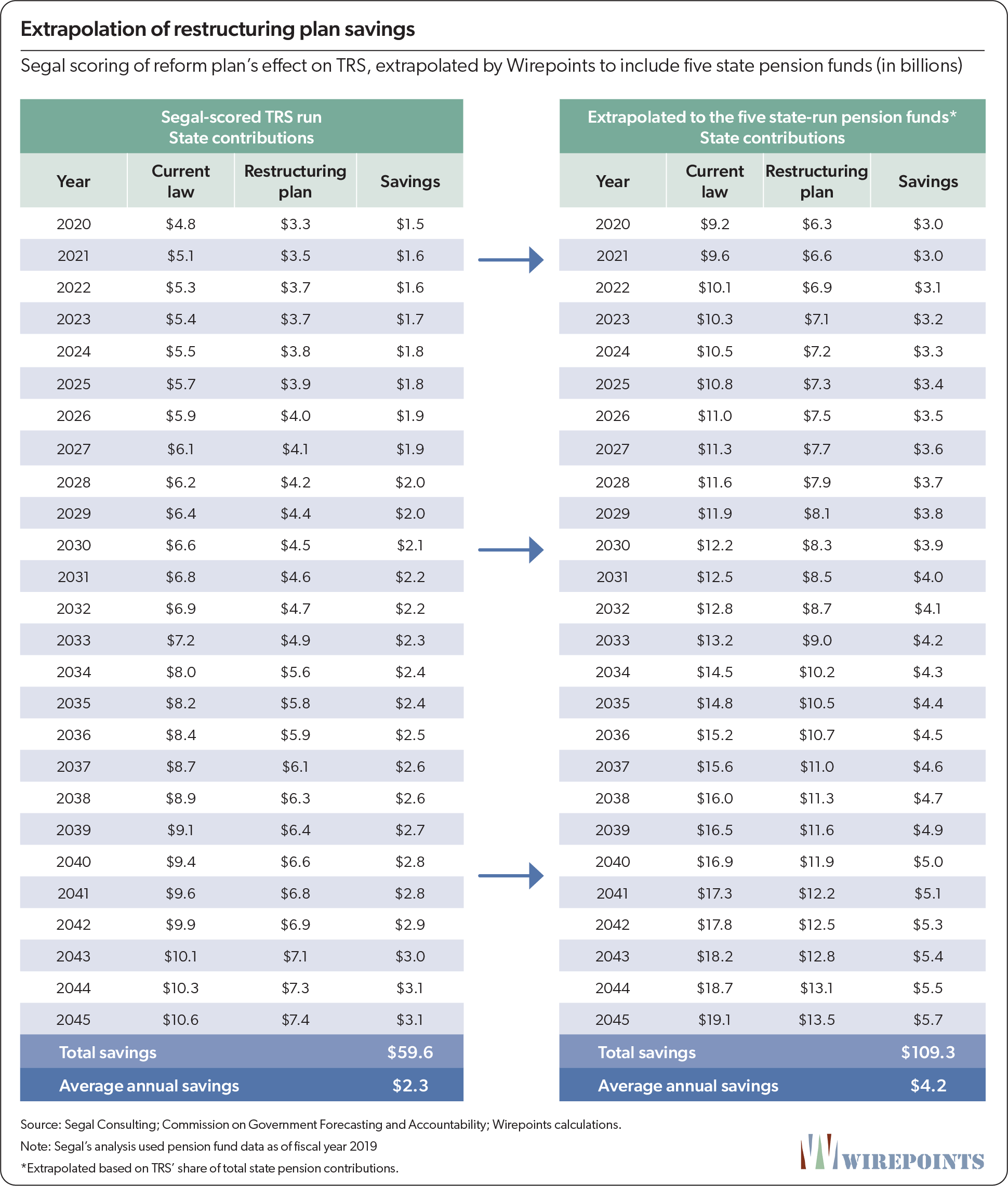

- Actuarial runs were performed only for the Teachers’ Retirement System. Wirepoints then extrapolated the TRS results to arrive at the savings for all five state-run pension funds.

- Wirepoints did not change the state’s current actuarial assumptions and statutory payment formulas. That allows for an apples-to-apples comparison of savings and debt reduction vs. current Illinois pension law.

2. Wirepoints’ baseline plan was scored before the COVID-19 crisis began. If the damage sustained by the pension funds is significant – if discount rates stay low and the stock market fails to recover – then additional and deeper reforms over and above the baseline plan may be needed.

3. Reforms that pair defined contribution plans with social security were not considered in this paper, except for those workers already enrolled in Social Security. Over 96 percent of all state employees today are in Social Security, while teachers, university workers, legislators and judges are not. The rationale for not pursuing Social Security for all workers is that contributions to the funds are costly, while the returns for beneficiaries are suboptimal.

A solution for pensions: Replicate SURS’ Self-Managed Plan (SMP) for all state funds

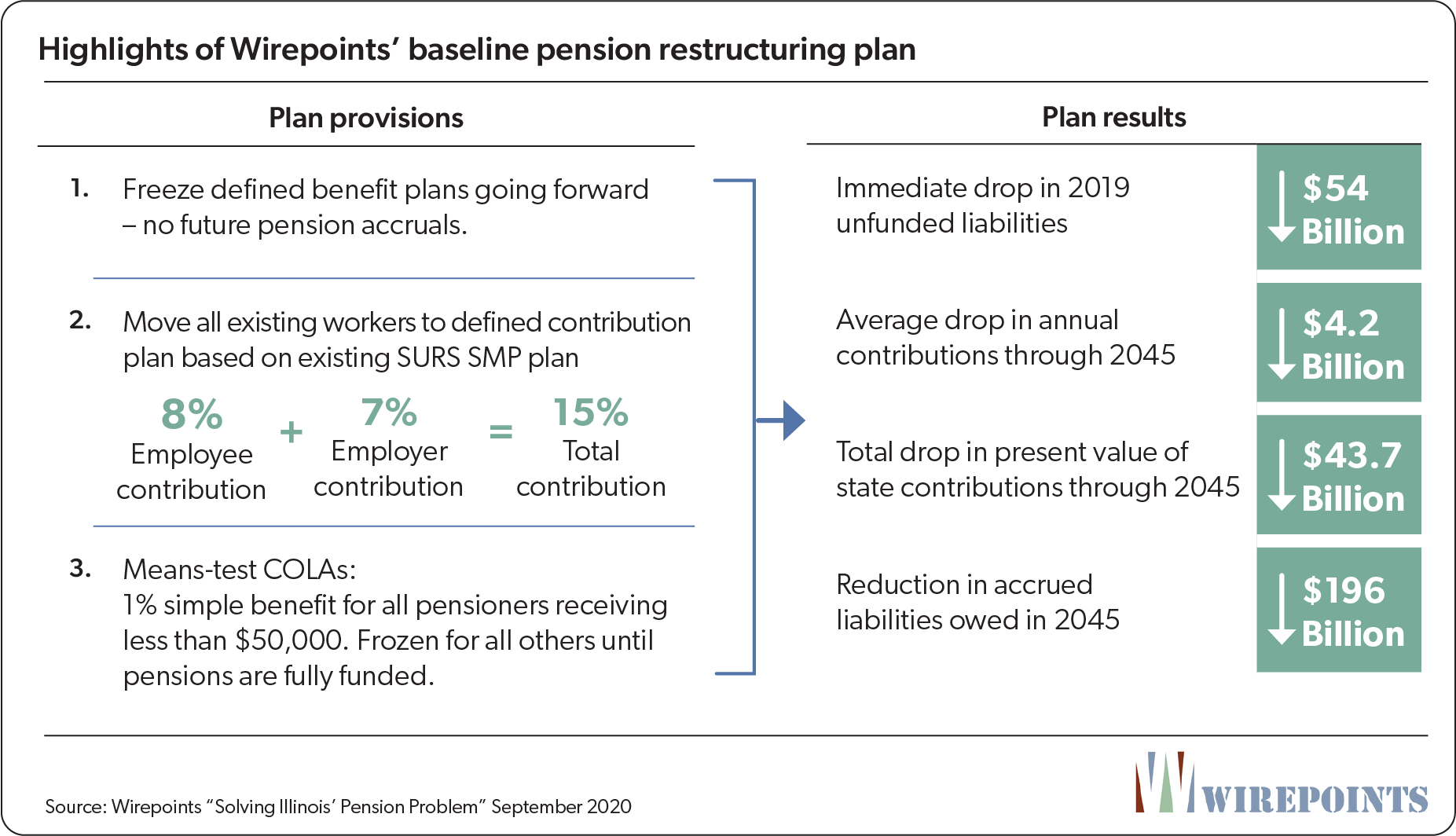

Wirepoints’ baseline restructuring plan for the five state-run pension systems does the following:

- Freezes the pension systems going forward, but protects benefits already earned. The five state-run defined-benefit plans are frozen immediately and defined benefits no longer accrue going forward. Pension benefits already earned by workers are still payable upon retirement. Retired members are not impacted by this part of the proposal.

- Transitions all current workers to a plan identical to Illinois’ existing defined contribution plan for university workers. All current workers in the five state-run systems are transferred to new plans that replicate the State University Retirement System’s (SURS) optional, defined contribution plan. Under the new plan, those workers not enrolled in Social Security contribute a mandatory 8 percent of every paycheck into a retirement account and the state contributes a matching 7 percent. In total, workers would have 15 percent of their salary set aside each pay period.Workers already enrolled in Social Security contribute a mandatory 3 percent of every paycheck into a retirement account. The state contributes a matching 3 percent. In total, state workers participating in Social Security have 6 percent of their salary set aside each pay period into the defined contribution plan. Retired members would not be impacted by this part of the proposal.

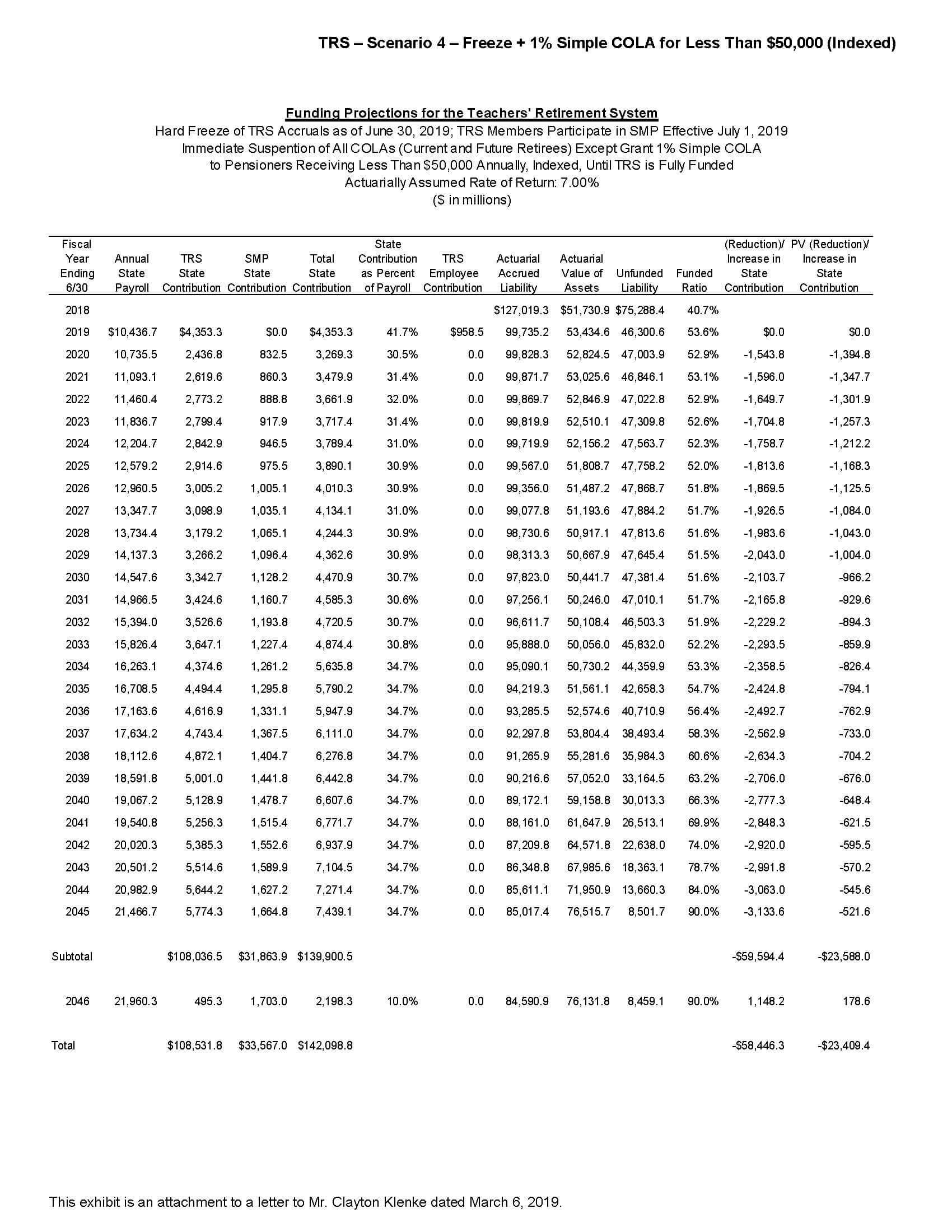

- Means-tests COLAs until pensions are fully funded. To ensure all workers, including those far into the future, receive their already-earned pension benefits, COLAs are means-tested and limited to members with annual benefits under $50,000 (adjusted for inflation going forward). Those members will receive a 1 percent simple COLA benefit. COLA benefits will be frozen for all other current and future retirees until the pension systems are fully-funded.(Wirepoints recognizes that there are many potential ways to restructure COLAs, i.e., on an “ad hoc” basis, only on the first $20,000 of benefits, etc. However, actuarial costs limited the number of potential scenarios Wirepoints could run.)

How the SURS Self-Managed Plan works

In 1998, the Illinois state legislature created a new retirement plan that offers state university workers an alternative to the traditional pension plan. Called the Self-Managed Plan, or SMP, these 401(k)-style accounts offer workers more flexibility, portability and individual control than pension plans do. More than 20,000 Illinois state university workers have opted into the SMP plan since its inception.

Under the SMP, an employee contributes 8 percent of each paycheck toward a 401(k)-style account, and the state matches that contribution with another 7 percent. Like the traditional pension plan, university workers with SMPs don’t contribute to or participate in Social Security.

Since 2012, 15 to nearly 20 percent of new university workers have chosen to enroll in the plan annually. That’s a high level of participation considering the pension plan, and not the 401(k)-style plan, is the automatic default plan offered by Illinois’ public universities and colleges.

University workers who opt in to the SMP are required by law to contribute to their 401(k)-style accounts. They can’t skip contributions or borrow funds from their accounts like many in the private sector can. SURS offers two investment providers to choose from, TIAA and Fidelity Investments, both of which sponsor funds with different levels of investment risk and potential returns. The state is also legally required to contribute funds into the worker’s account every pay period. It can’t offer IOUs like it does for pension funds.

Also important is that the SURS plan lets retirees convert their savings into Social Security-like benefits. The plan offers different payout options at retirement, including a lifetime annuity payout which retirees cannot outlive.

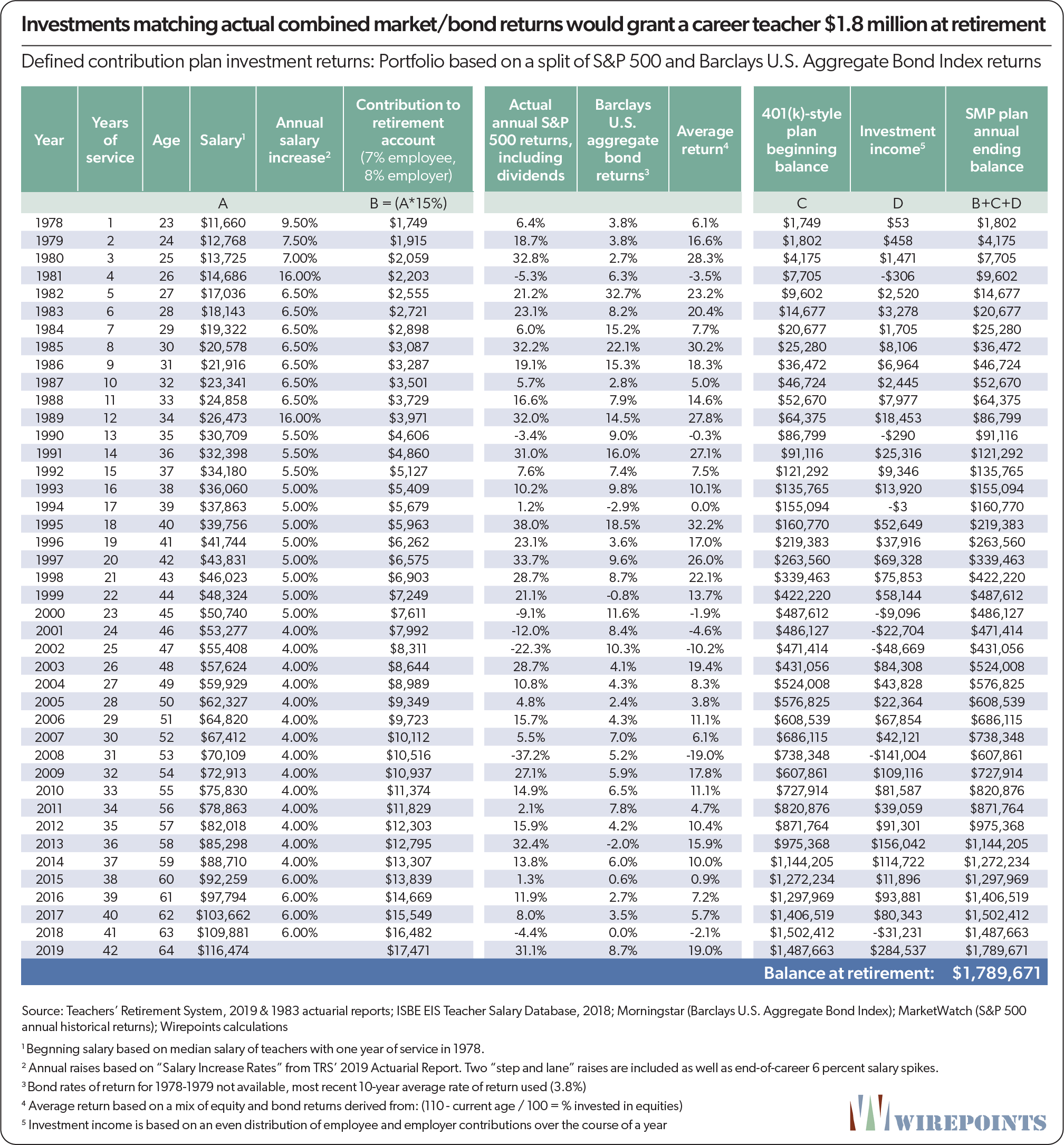

The 401(k)-style plans, as structured in the SURS plan, can provide for comparable retirement funds to what a pension can provide. For example, if a newly hired teacher had been offered her own SMP account in 1978, historical returns show she could retire today with $1.8 million in retirement funds. (See Appendix A for more information.)

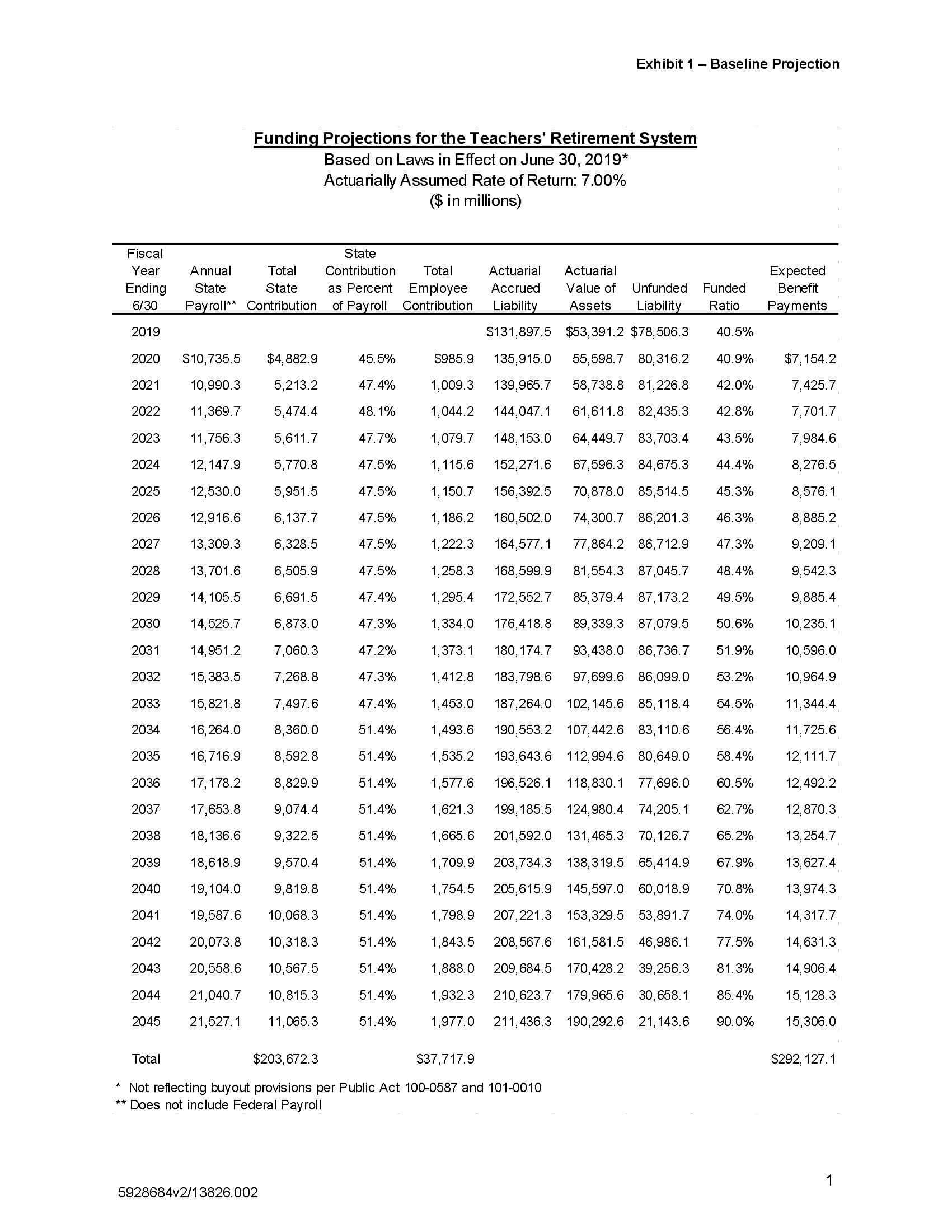

Baseline pension restructuring savings

The restructuring plan would impact pension fund finances in the following ways:

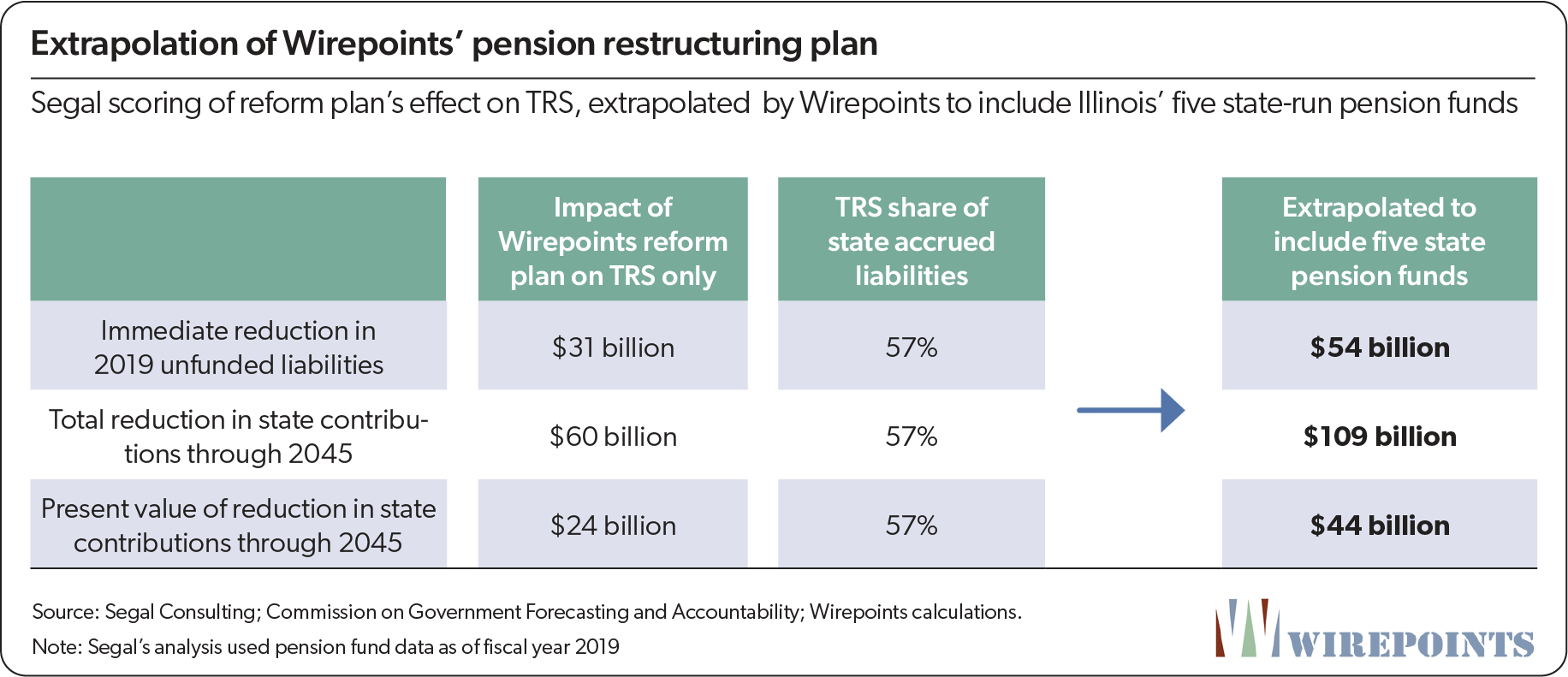

- $54 billion immediate drop in unfunded liabilities.

The state’s $137 billion unfunded liability falls to $83 billion, a 40 percent reduction. - $4.2 billion reduction in average annual contributions through 2045.

First year savings under the plan would total $3 billion. - $43.7 billion present value reduction in contributions through 2045.

In all, the state would contribute $109 billion less to pensions through 2045. - $196 billion reduction in accrued liabilities by 2045.

The state would be burdened with $135 billion in liabilities in 2045 instead of the $331 billion projected today.

Importantly, the state plans would no longer accrue new defined benefit liabilities going forward. That’s key to allowing the state to focus on repaying its post-reform pension debts without the constant addition of new defined-benefit liabilities.

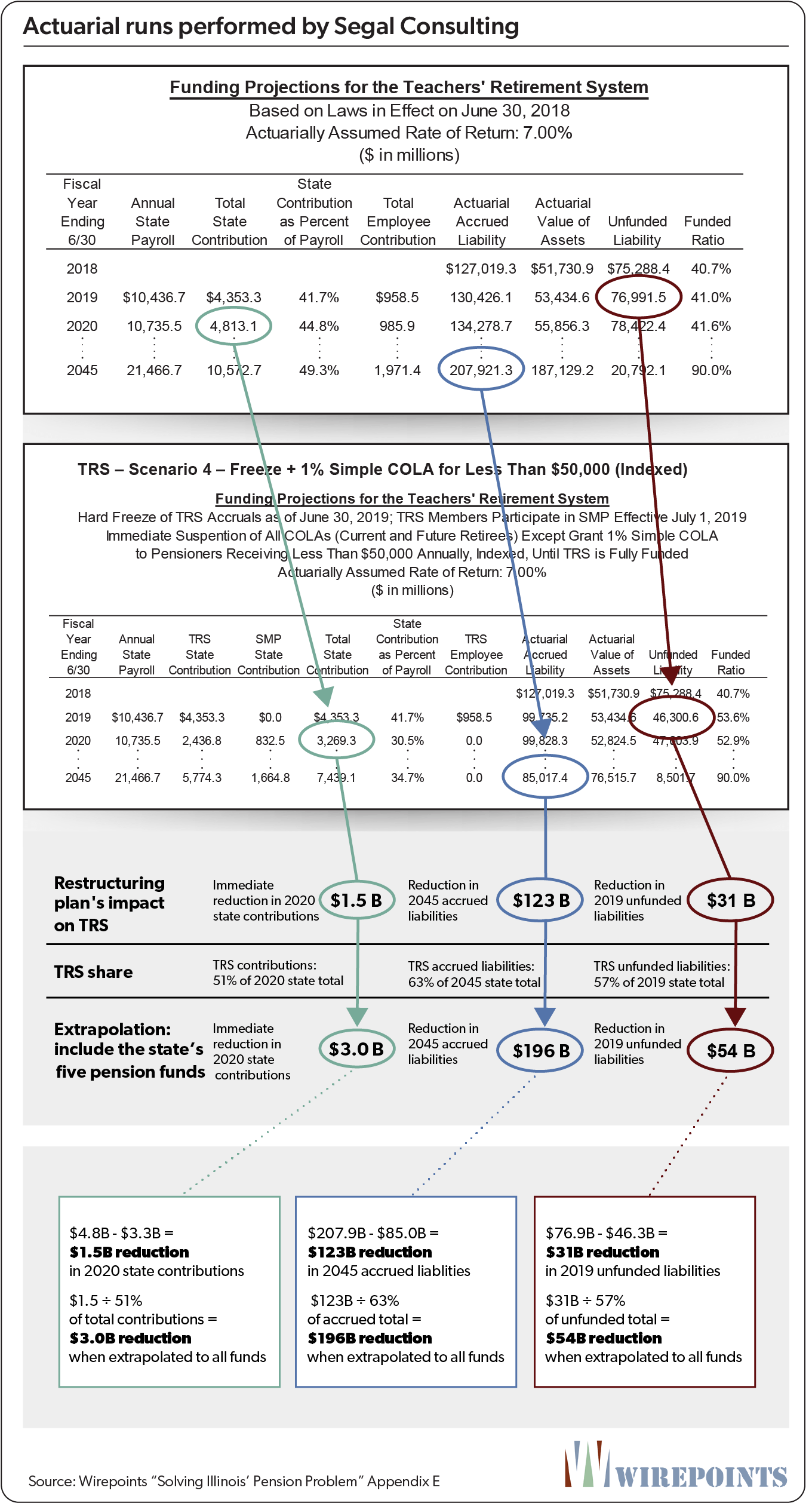

Wirepoints extrapolated the savings from the TRS run to estimate savings for a restructuring plan that includes the other four state-run pension systems. Wirepoints’ extrapolation was based on TRS’ share of the state’s total accrued liabilities, an approach confirmed by Segal as reasonable for the purposes of this report. (See Appendix C for more information.)

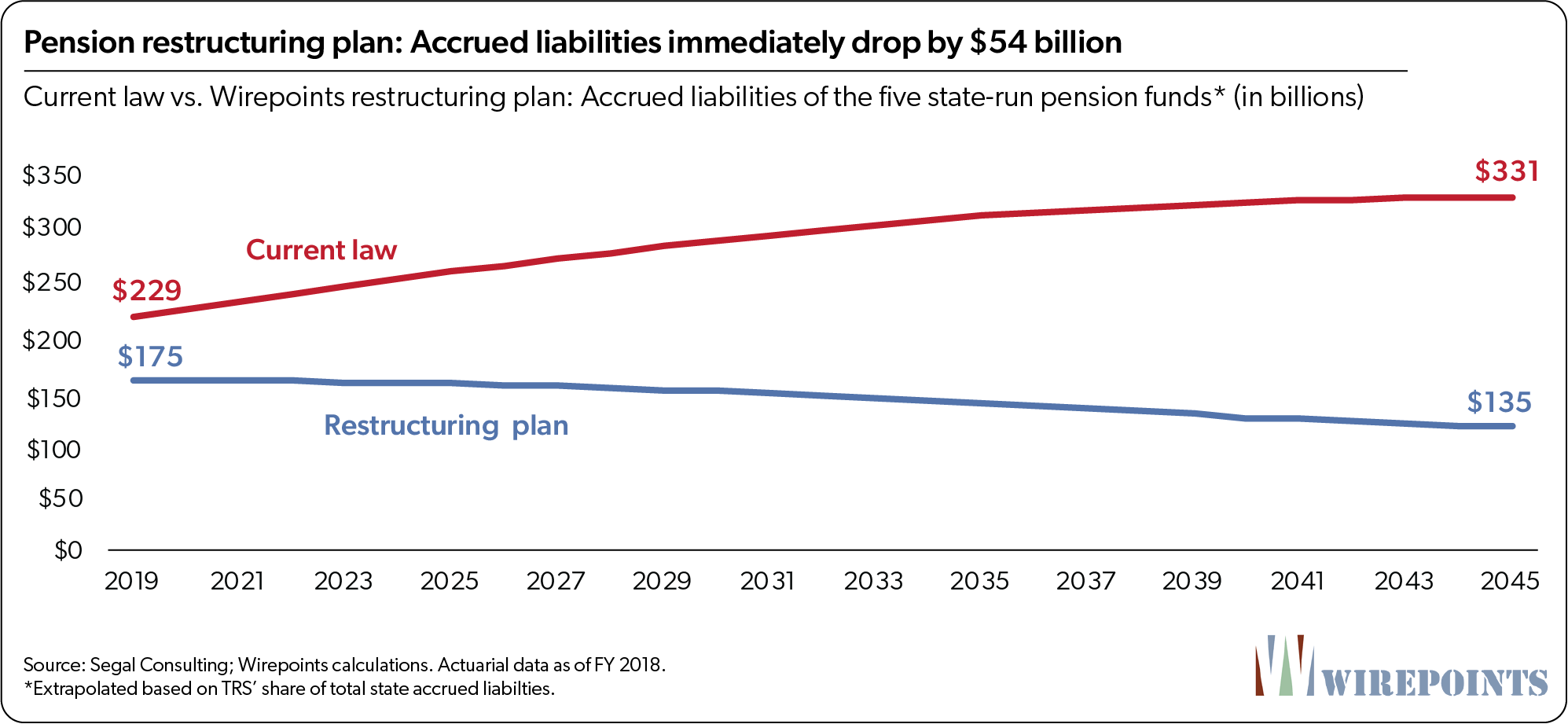

Pension restructuring plan vs. current law

Under the restructuring plan, accrued liabilities fall to $175 billion from $229 billion in 2019. That’s an immediate drop of $54 billion. Thereafter, accrued liabilities decline as more new state employees enroll in the defined contribution plan and the number of pensioners shrink. Under the plan, the state will have dramatically less accrued liabilities by 2045. Current law projects liabilities will grow to $331 billion by 2045 vs. plan liabilities of $135 billion.

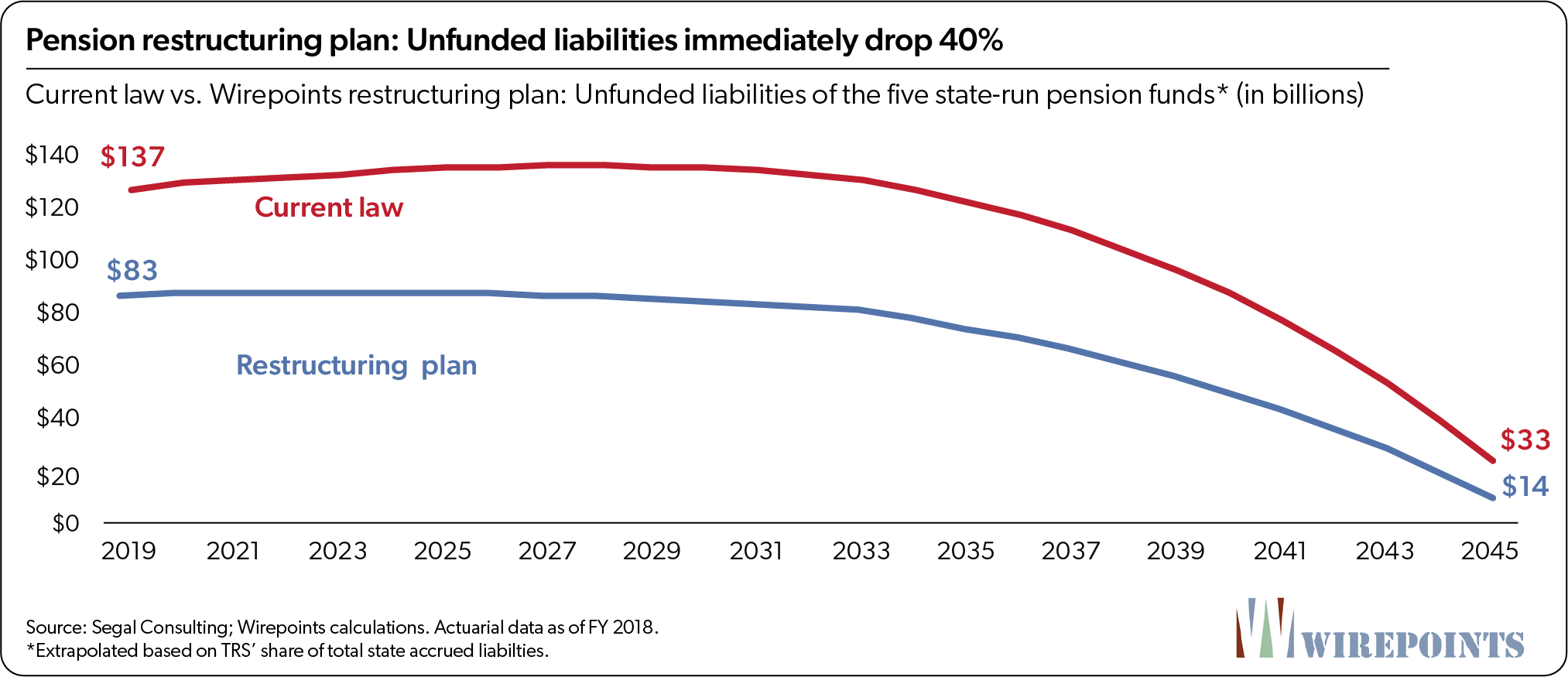

State unfunded liabilities immediately drop by 40 percent

Under the restructuring plan, unfunded liabilities drop immediately by 40 percent, to $83 billion from $137 billion. That’s a vast improvement over current law, and not just because the liability is smaller. The reform plan ends the accrual of any new defined benefits, meaning the plan is less susceptible to changes in assumptions and poor investment returns as compared to current law. Under current law, unfunded liabilities are projected to fall to $33 billion by 2045. Under the restructuring, the state’s shortfall will total just $14 billion.

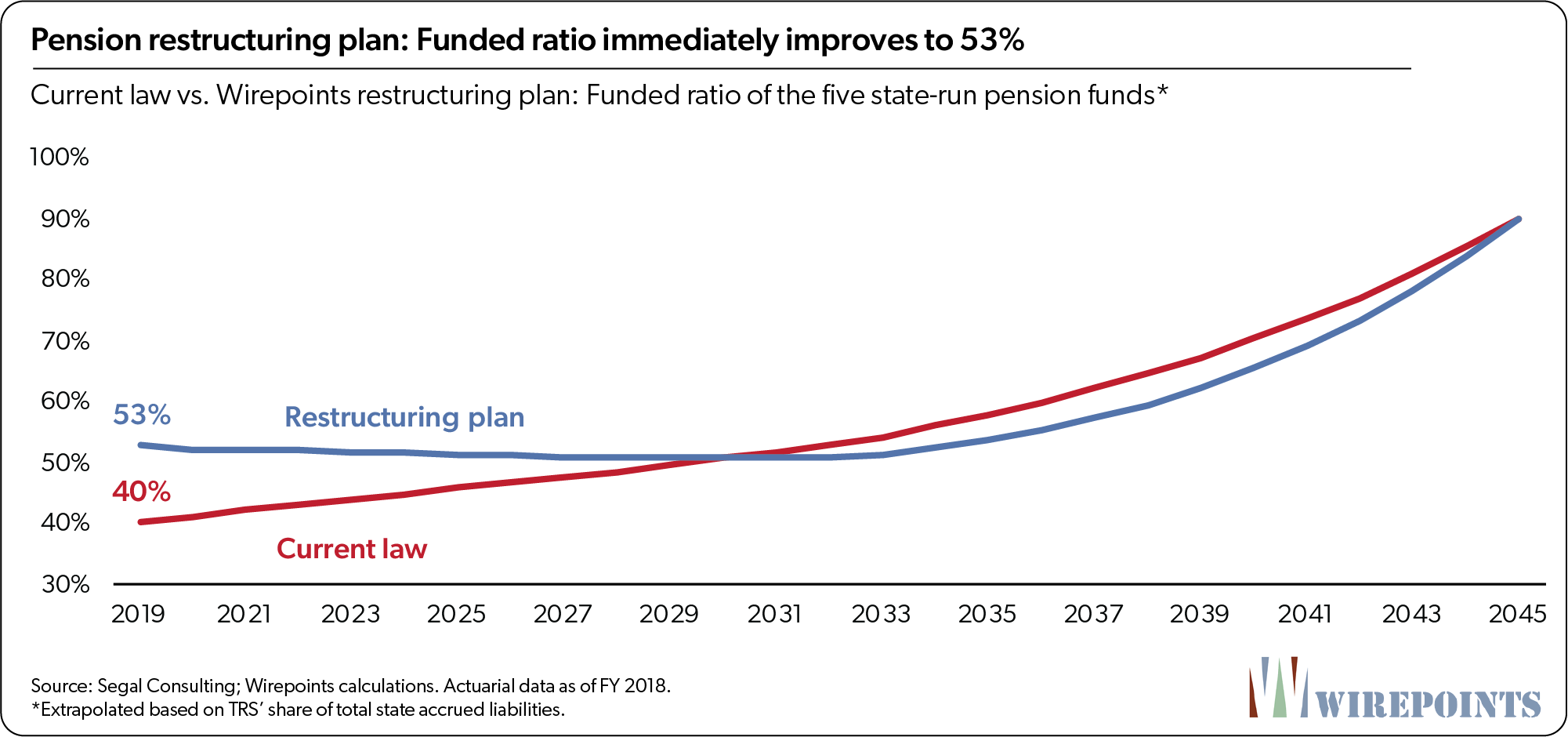

Combined funded ratio immediately improves to 53 percent

Under the restructuring plan, the funded ratio of the five state plans would immediately improve to 53 percent from 40 percent. The projected funded ratio is hardly changed from current law because the reform plan uses the same statutory payment schedule (90 percent funded by 2045).

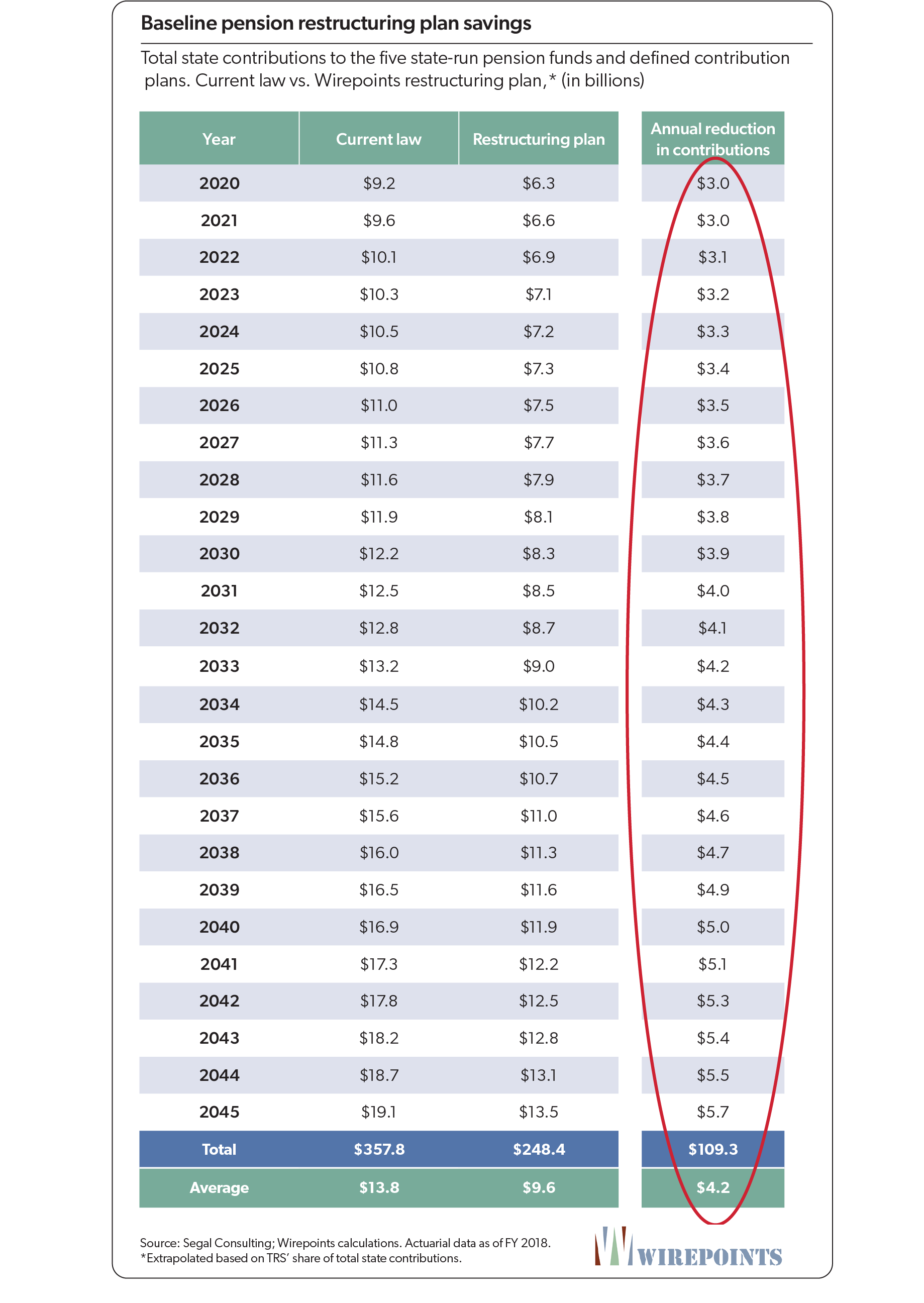

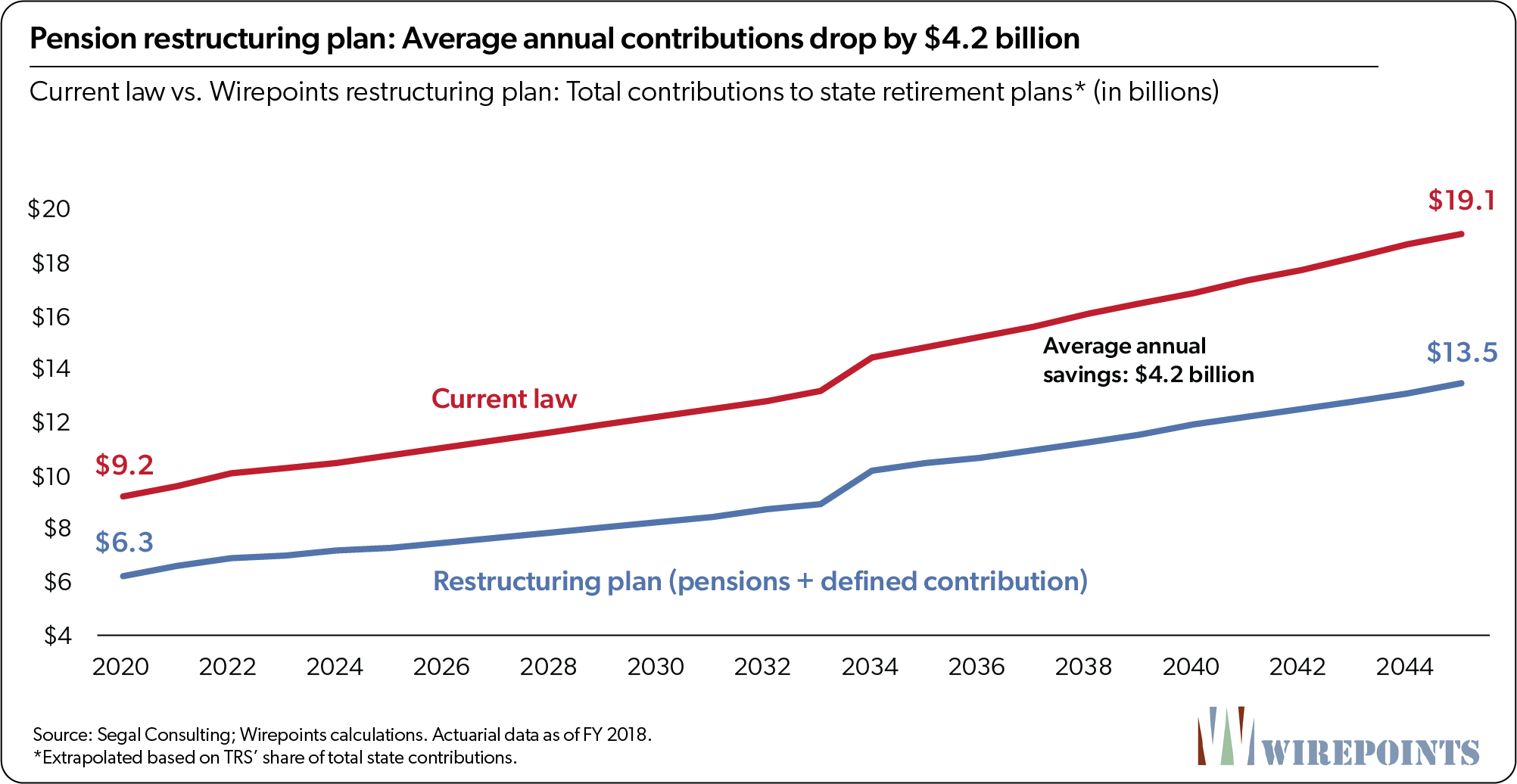

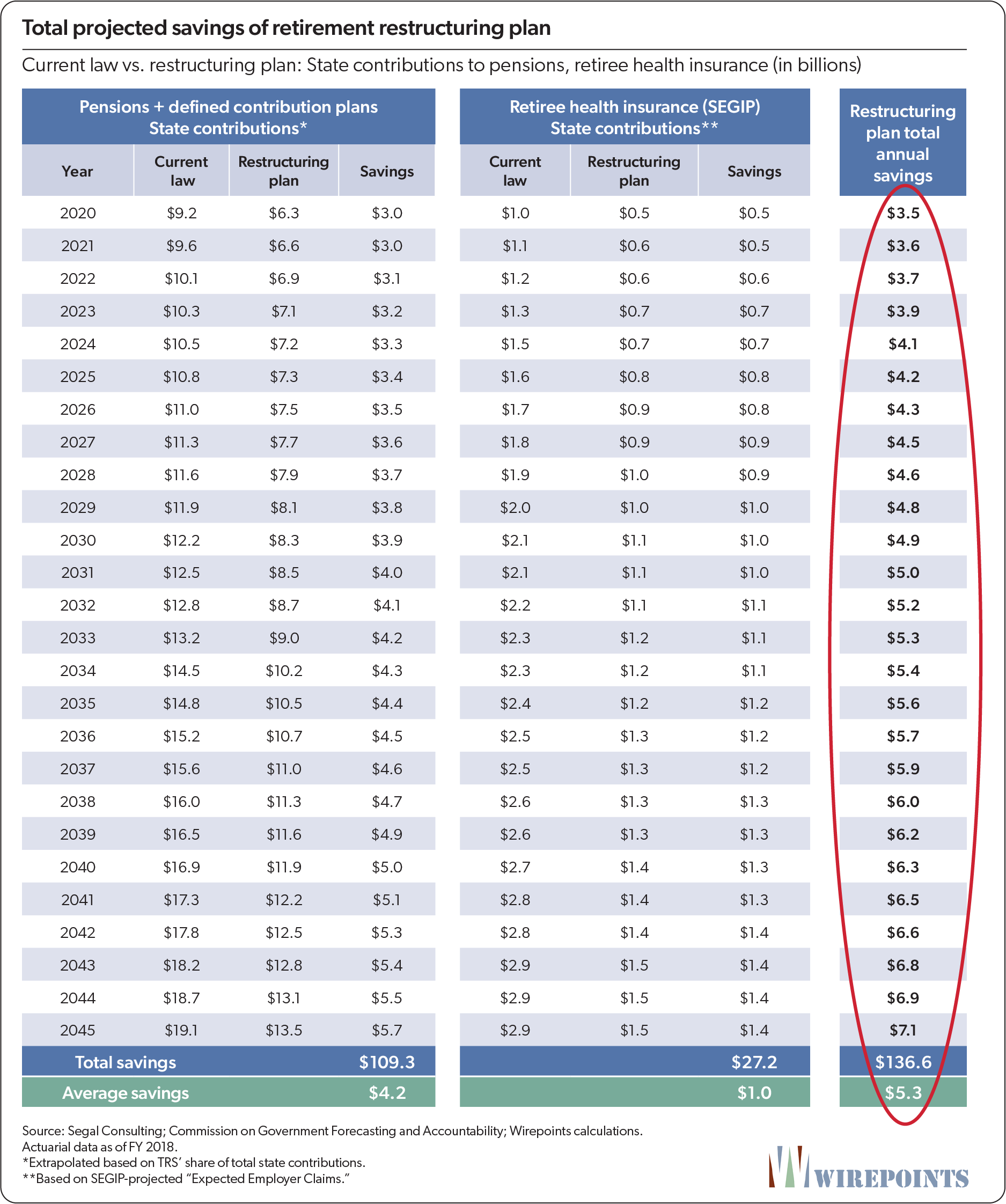

Required annual state contributions through 2045 fall by an average $4.2 billion

Under the pension restructuring plan, the state will be required to make $109 billion less in retirement contributions through 2045, an average savings of about $4 billion a year. In present value terms, that’s a saving of nearly $44 billion.

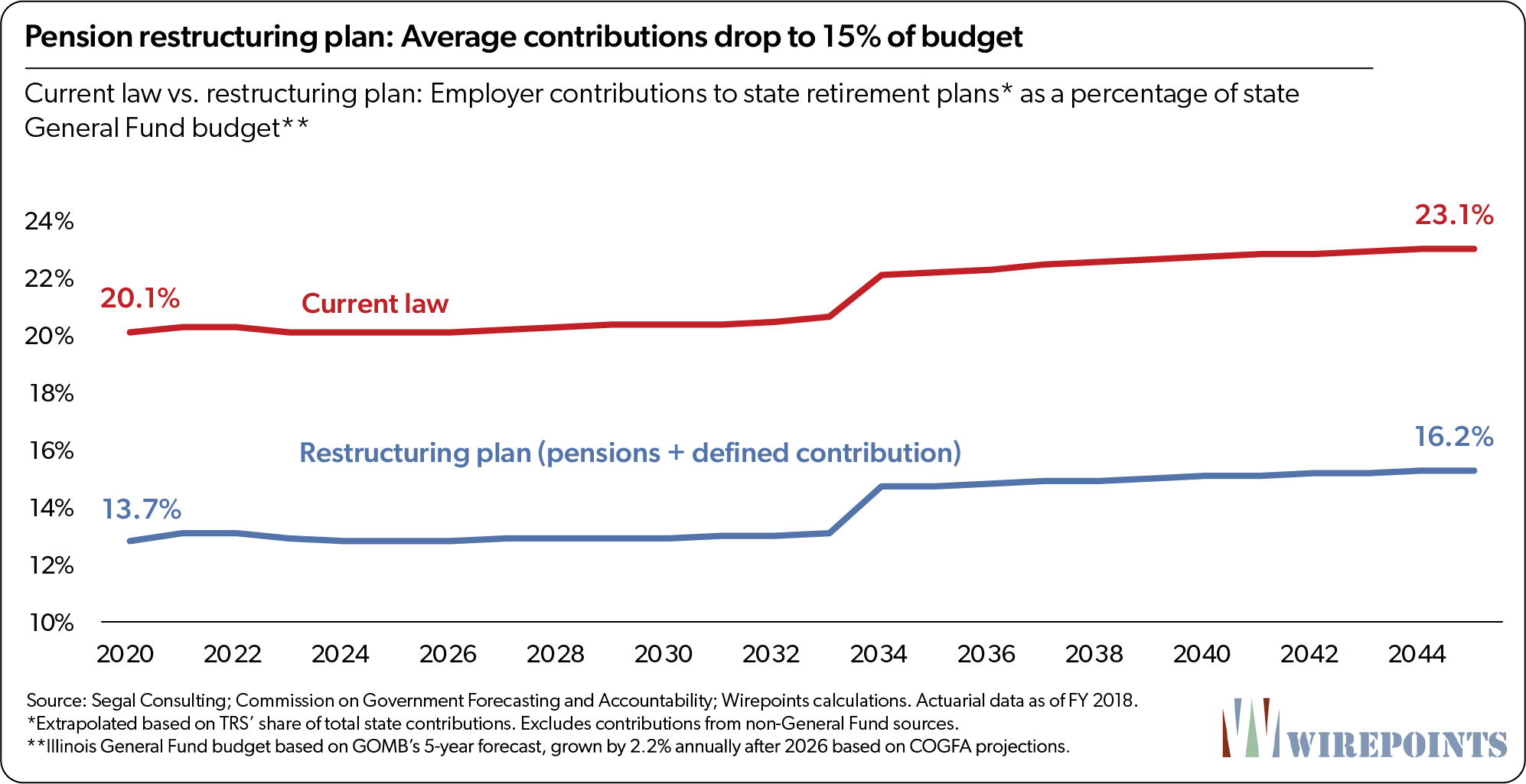

Under current law, state contributions are set to ramp up every year until the pension funds achieve 90 percent funding in 2045.Contributions are projected to grow from $9 billion in 2020 to $19 billion by 2045. In contrast, the annual contributions under the restructuring plan are far smaller. By 2045, the state would have to contribute $13.5 billion to worker retirements, about $6 billion less than projected under current law.

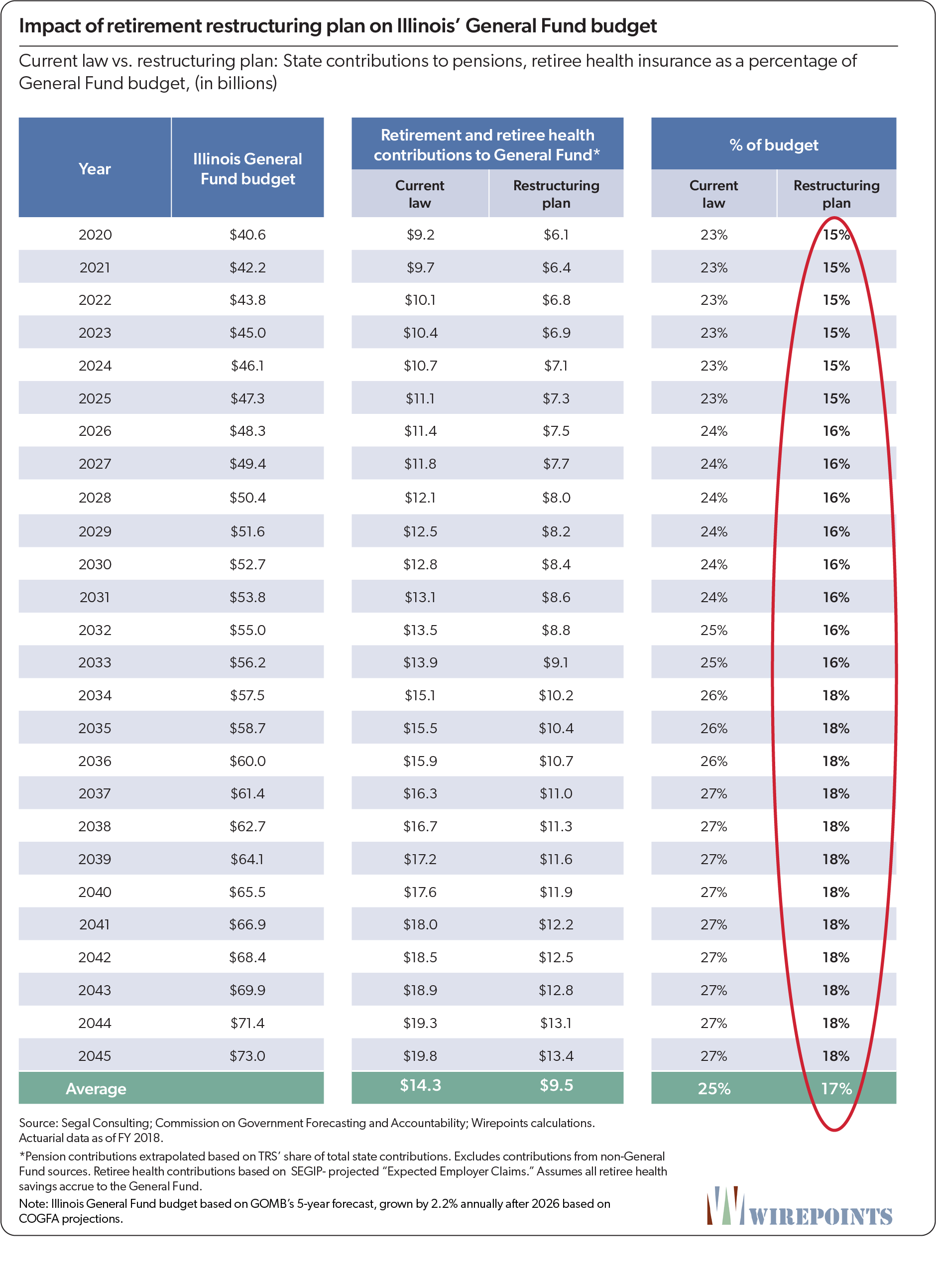

Those smaller contributions would put less pressure on Illinois’ budget as compared to current law. Currently, state contributions to pensions will consume an average of 21 percent of Illinois’ budget through 2045. Under the plan, the state’s retirement contributions would fall to 15 percent on average.

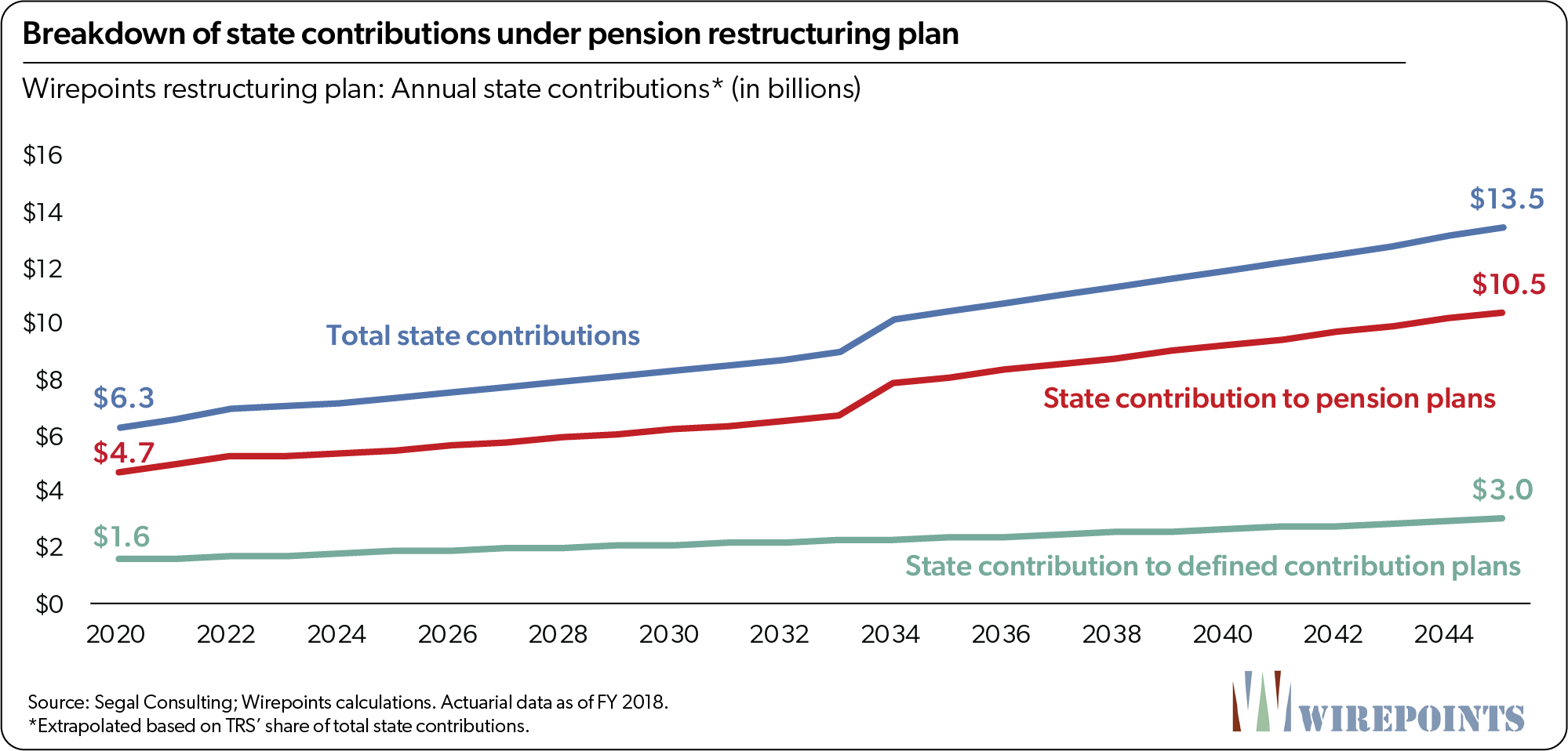

State contributions to worker retirements under the reform plan would be divided into two parts: contributions to the pension fund and payments into workers’ individual retirement accounts as part of the new defined contribution plan.

In 2020, $4.7 billion in state contributions will go toward pensions and $1.6 billion toward the defined contribution plan. By 2045, contributions will grow to $10.5 billion for pensions and $3 billion for the DC plan.

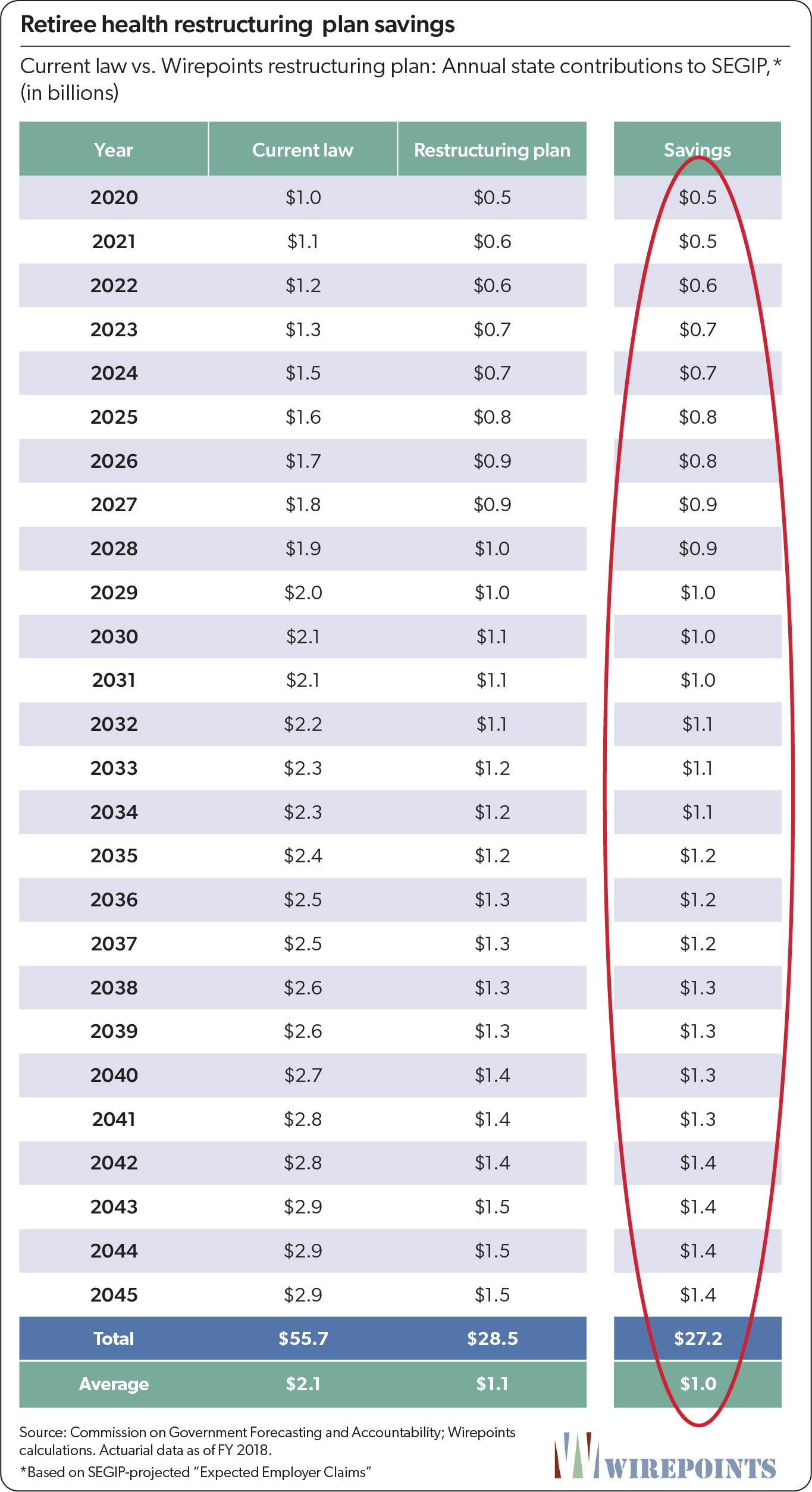

Retiree health insurance restructuring plan: Means-test benefits going forward

Wirepoints’ restructuring of the state’s retiree health insurance plan (SEGIP) does the following:

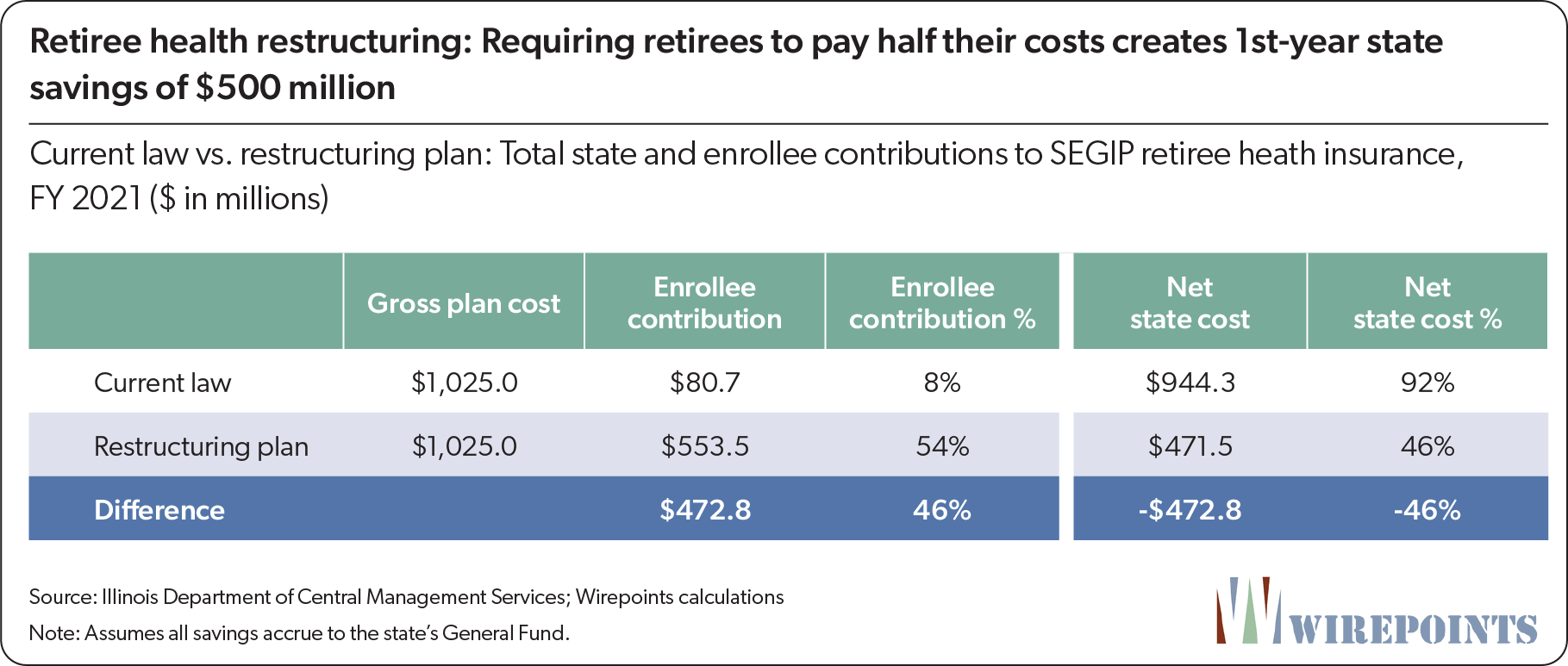

- Requires retirees to pay, on average, 54 percent of insurance premium costs – the average of employee premium contributions across the country. In contrast, Illinois’ retired state workers currently pay, on average, just 10 percent of the total cost of annual health insurance premiums.

- Achieves that 54 percent average by means-testing retirees’ individual payments based on age, years of service and annual income. The plan would reward employees for long-time service, protect low-income retirees and discourage early retirements. In practice, that means older public sector retirees with many years of service and modest incomes would, on average, see little change in their premium payments, while those retiring in their 50s with six-figure pensions would be required to cover their own costs.

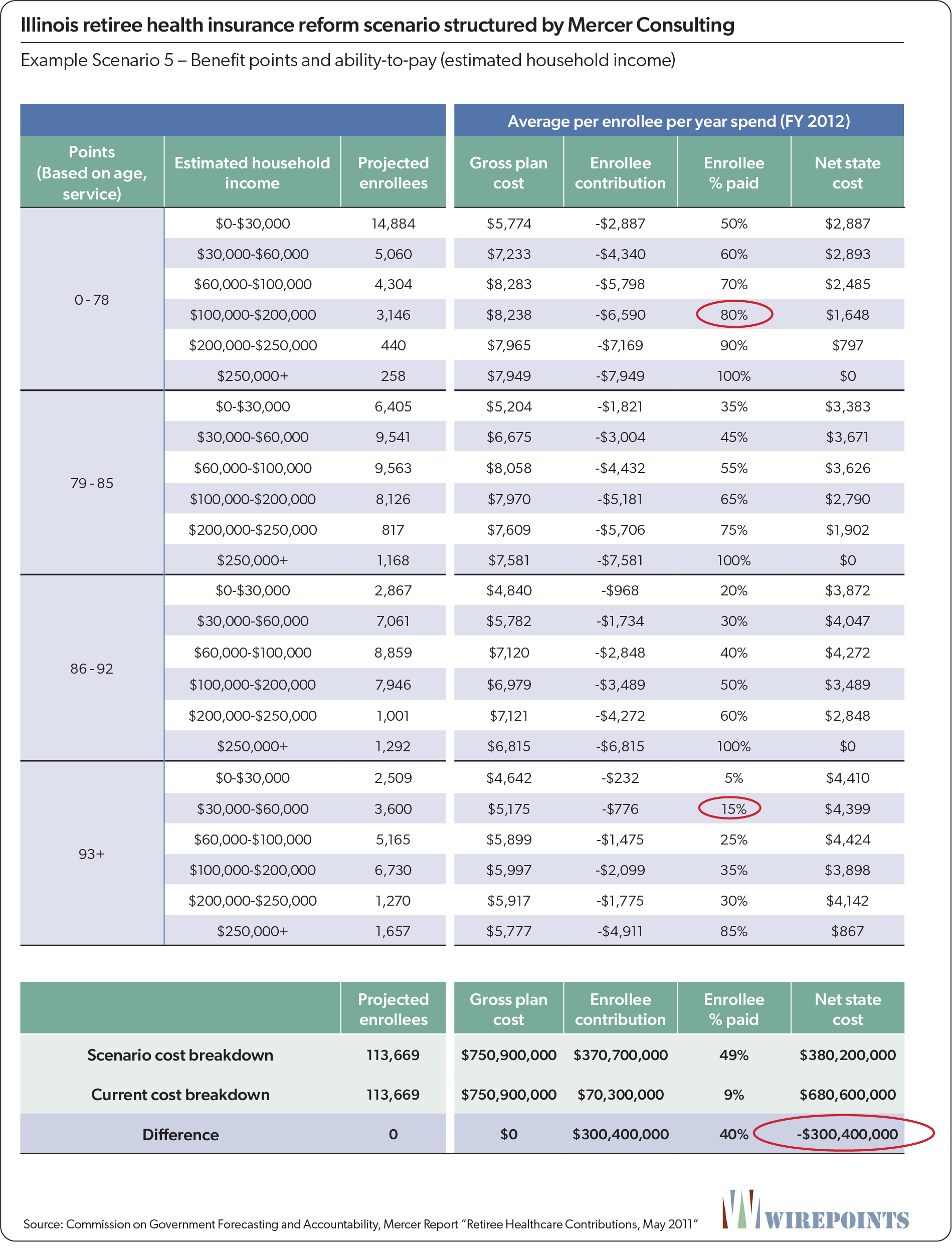

Wirepoints’ plan is based on a series of reform scenarios produced by Mercer Consulting in a 2011 retiree health insurance report for Illinois’ Commission on Government Forecasting and Accountability.

Their goal was to redesign retiree health subsidies so retirees would, on a means-tested basis, pay for half the total annual cost of their insurance. That would have saved the state $300 million in FY 2012.

Several of Mercer’s means-test scenarios used a “points” formula to determine individuals’ contributions, one of which is laid out on the next page. A retiree’s required contribution would be determined by adding up “points” based on his retirement age and years of service, then further modified based on his annual income. The greater the “points” and the lower the income, the lower the required contribution becomes.

For example, a retiree with 75 “points” (retirement age plus years of service) and an income of $110,000 would be required to pay for 80 percent of his health insurance premium.

In contrast, a retiree with 93 “points” and an income of $50,000 would be required to pay for just 15 percent of his premium.

Wirepoints’ restructuring of SEGIP benefits would impact state finances in the following ways:

- $20 billion immediate drop in accrued liabilities. The state’s $40 billion in SEGIP liabilities falls to $20 billion, a 50 percent reduction.

- $1 billion reduction in average annual contributions through 2045. Savings in 2021 under the plan would total nearly $500 million.

- $27 billion total reduction in contributions through 2045. That’s a reduction of $16 billion in present value terms.

Moving forward, the state could reduce this liability further and help remove the current incentive for workers to retire early by capping subsidies for new retirees and ending subsidies for new hires altogether.

Combined impact of retirement restructuring plans

The most obvious benefit of the restructuring plan is the immediate reduction in the state’s official debt burden. Illinois’ $192 billion in pension and retiree health insurance shortfalls – the nation’s 3rd-highest – immediately falls to under $120 billion. On a per household basis, that’s a drop to $24,000 from nearly $40,000.

That’s still high in relative terms, but moving to a defined contribution for all workers means not having to cut as much retirement debt as would otherwise be necessary. The elimination of new defined benefits and additional member contributions to retiree health means that Illinois’ per capita debt burden over time will continue to shrink compared to other states.

The immediate reduction of $4 billion in contributions means retirement costs as a percentage of Illinois’ General Fund budget will fall to 17 percent from a current nationwide high of 26 percent. Over time, that will free up resources for core services that have been crowded out by retirement costs.

The state will also have far more budget certainty. Future retirement payments will become a more known, predictable, fixed value as unfunded pension debts decline and defined contributions become a larger share of the state’s retirement costs. That also applies to Illinois taxpayers, who will have more certainty in their contributions (taxes) to worker retirements.

Beyond the benefits of helping bring an end to the state’s retirement crisis, the restructuring plan has several other advantages. The plan ends the unfair Tier 2 system, where workers hired after 1/1/2011 are forced to subsidize the benefits of Tier 1 workers and retirees. Going forward, all new and current Tier 2 workers will contribute 15 percent of their salaries (7 percent employer, 8 percent employee) toward their own retirements, not subsidize someone else’s.

The restructuring plan also ensures retirement security for workers. Defined contribution plans are controlled by workers themselves, not Illinois politicians. Politicians can’t skip payments to individual accounts like they have done to the pension systems.

The combined impact of the restructuring plan will restore a level of confidence in Illinois that has been missing for several decades. Of course, the restructuring plan alone is not enough to fully set Illinois on the right path. Debt reduction must be combined with other key reforms: local government consolidation, collective bargaining reforms, fair maps, and more so Illinois can finally escape its downward financial spiral and reestablish a competitive level of services, tax rates and economic growth for Illinois.

Retirement restructuring plan: total saving

Under the combined restructuring plan, the state will be required to make $137 billion less in retirement contributions through 2045. Those smaller contributions would put less pressure on Illinois’ General Fund budget as compared to current law. Currently, state contributions to retirements will consume an average of 25 percent of Illinois’ budget through 2045. Under the plan, the state’s retirement contributions would fall to an average of 17 percent of budget.

Other potential reforms

It’s impossible to know how severe the economic damage of the COVID-19 crisis will be. That’s precisely why the state’s constitutional language must be flexible enough to allow Illinois’ different units of government to pursue various kinds of reforms.

In addition, changes to the state’s own pensions may have to go beyond the baseline reforms Wirepoints has outlined in this paper.

Some funds may be required to change benefits – in the form of caps, tiered reductions, salary freezes, and other changes – to reduce their debts to a manageable level.

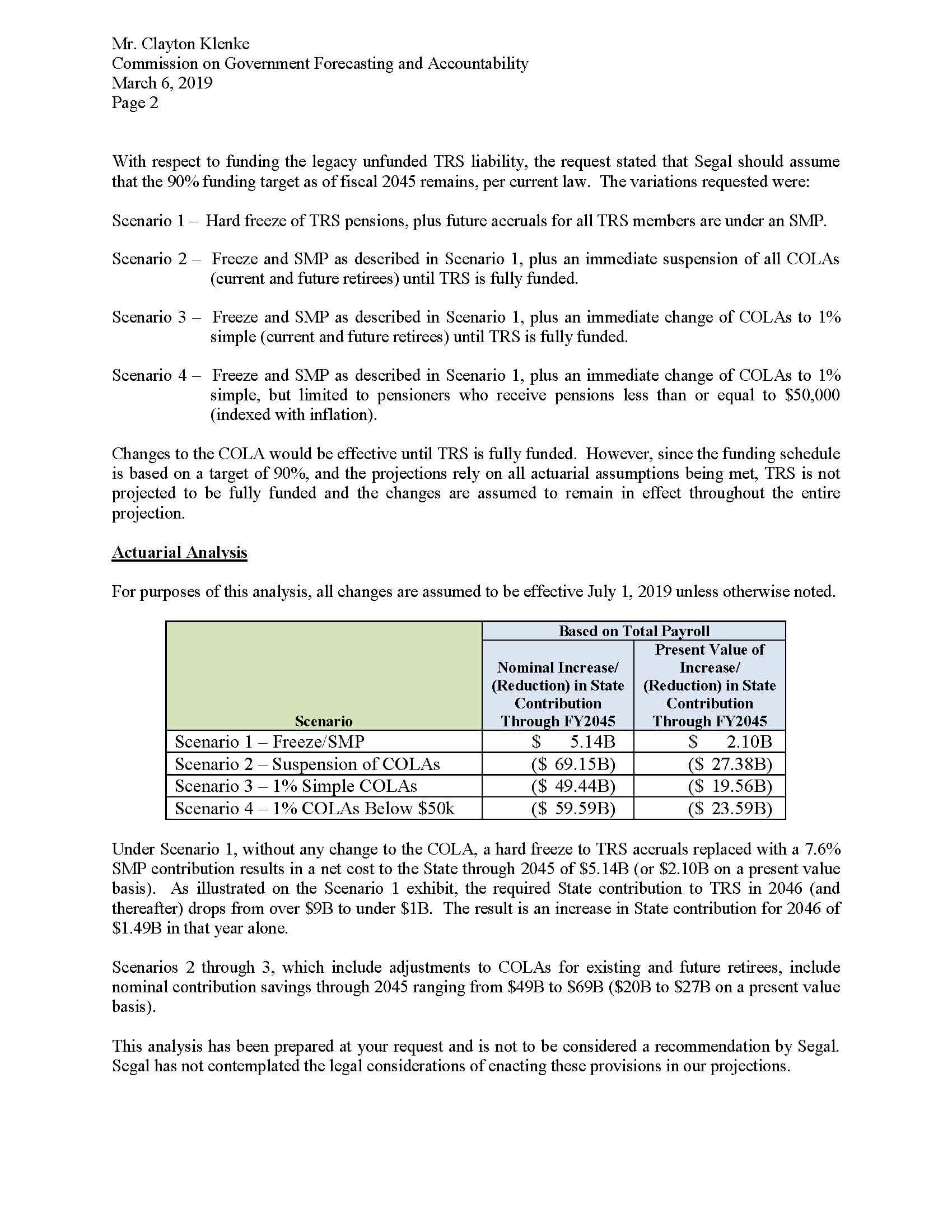

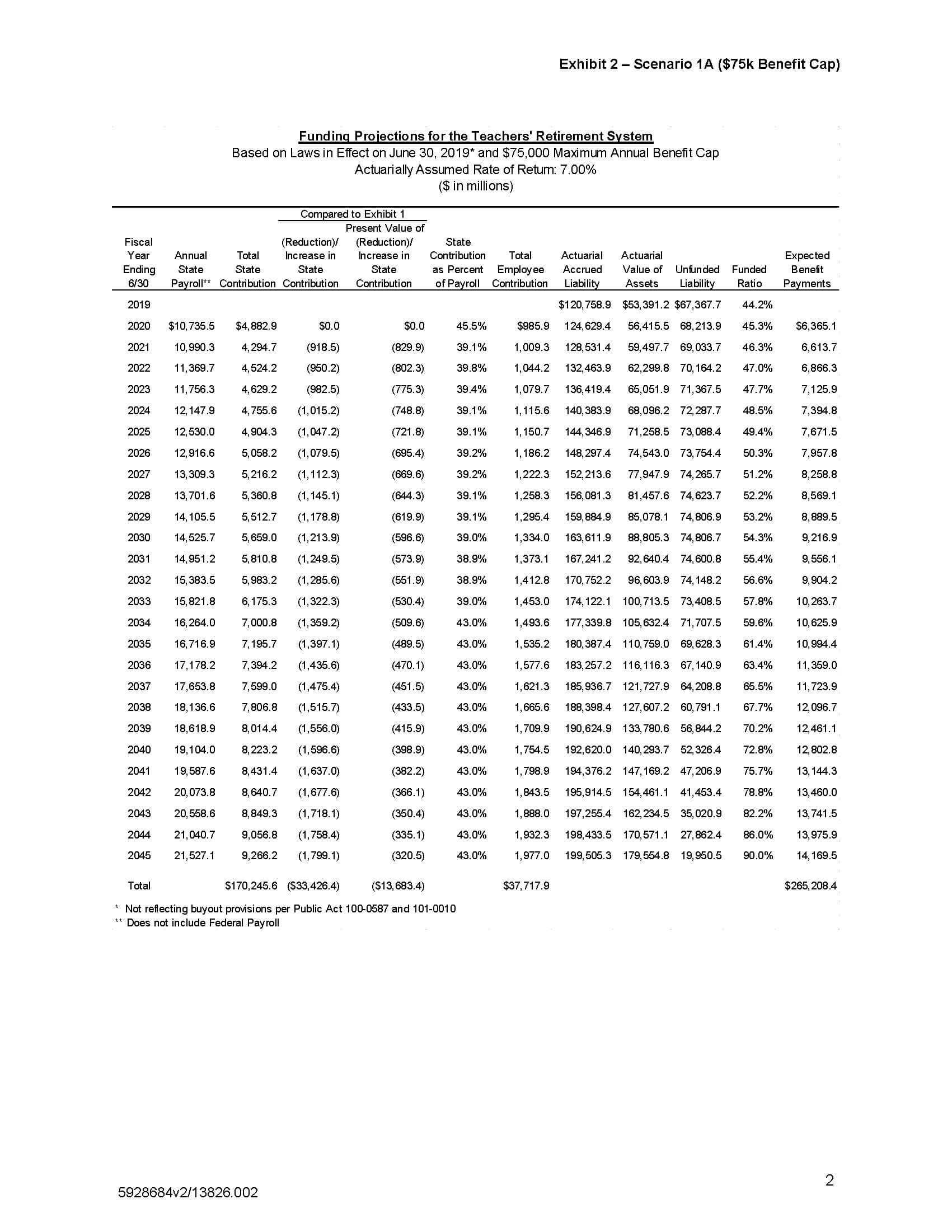

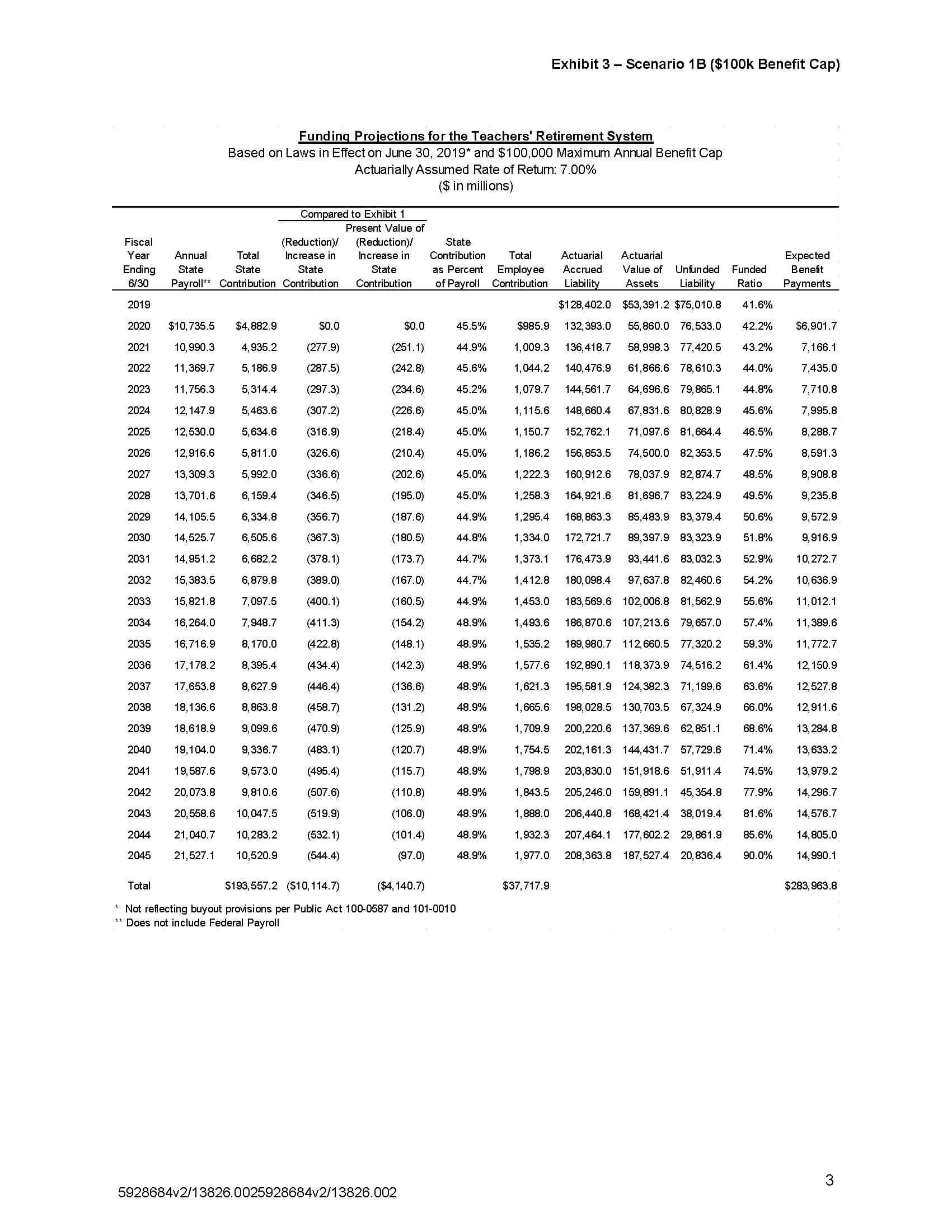

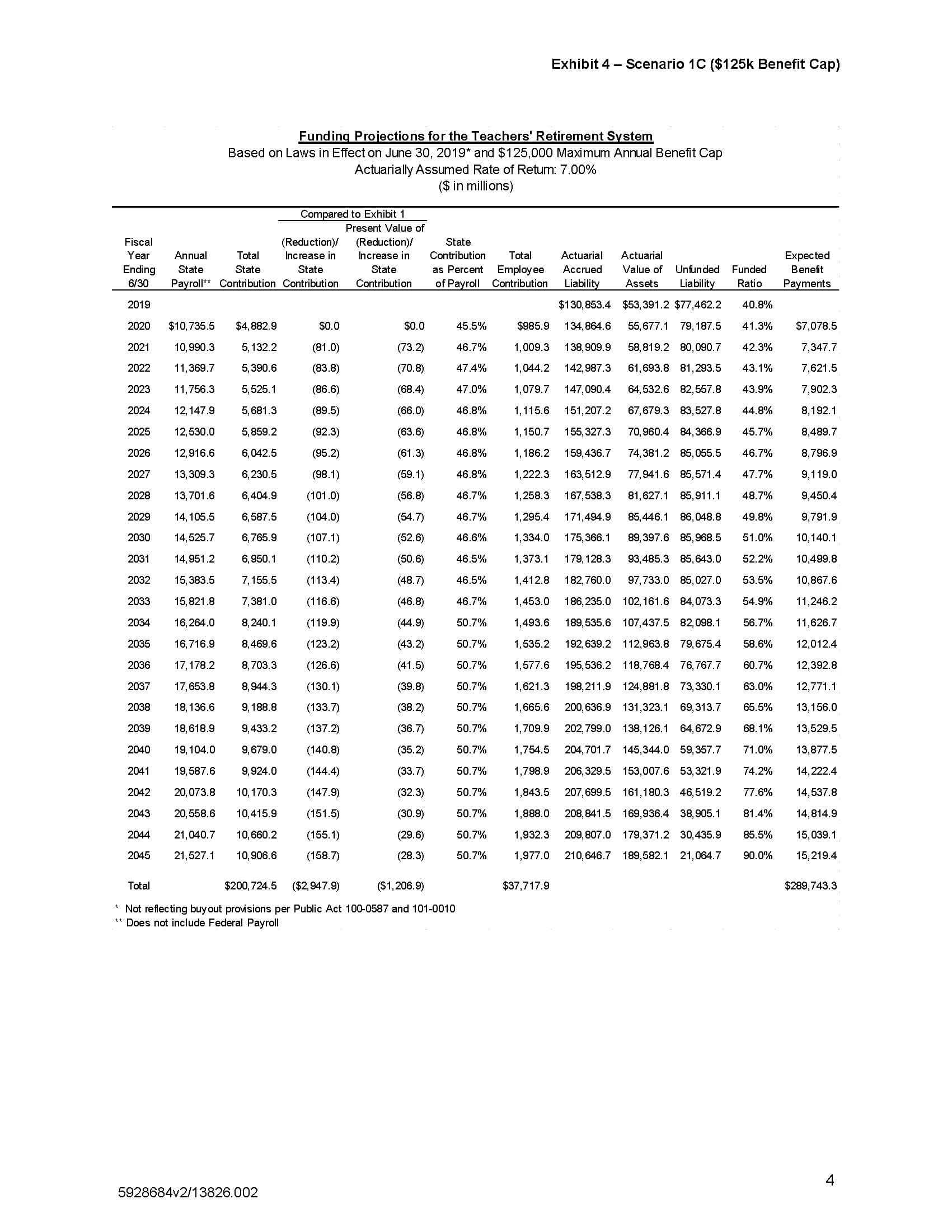

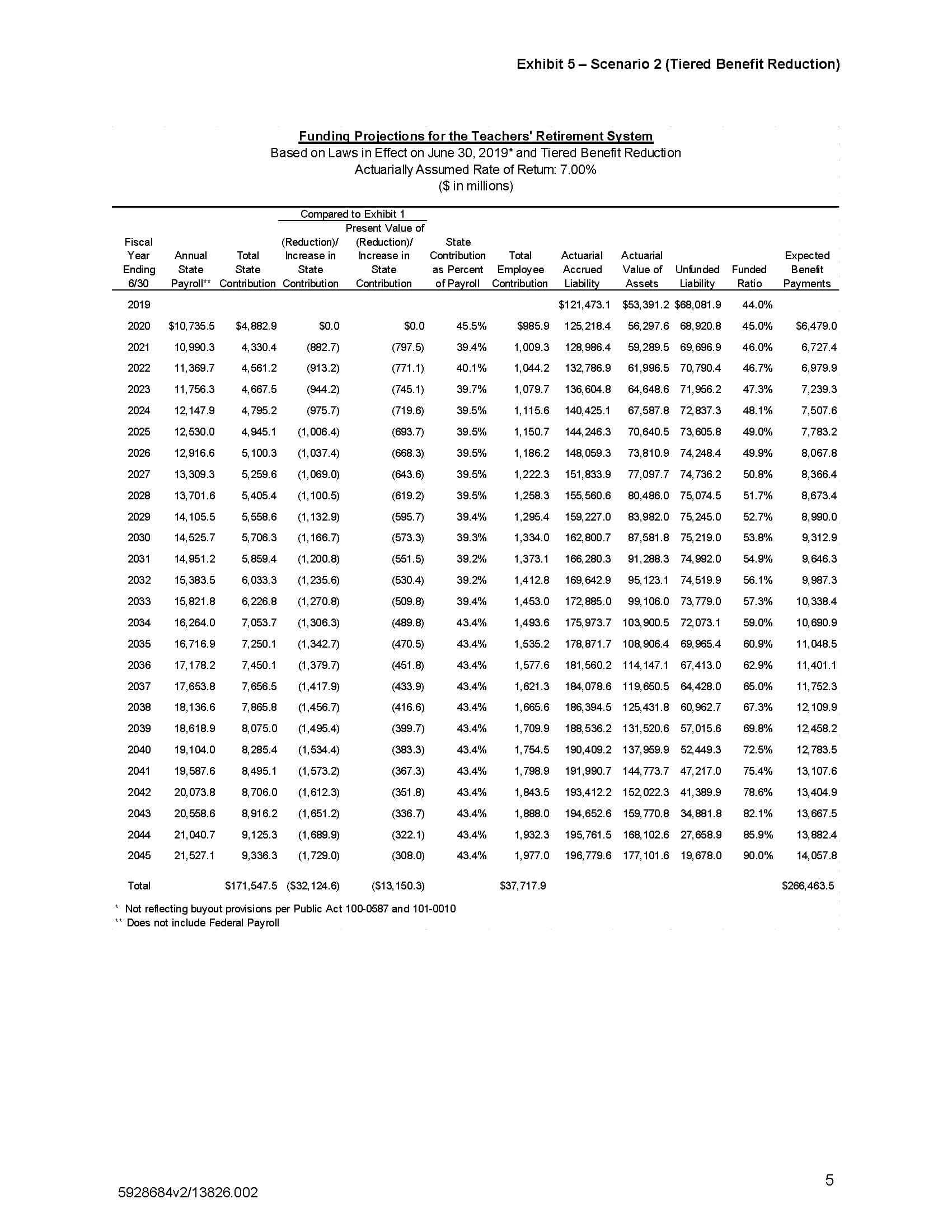

Segal Consulting scored three additional reform scenarios for state-level pensions that could provide supplemental savings or amend elements of Wirepoints’ baseline plan. Of course, the scoring of countless other variations are possible, but the high cost of actuarial consultants limited the number of scenarios. For that reason, Segal only analyzed reforms for TRS as of FY 2019 and maintained the state’s current actuarial assumptions and statutory payment schedule (90 percent funded by 2045).

It’s also important to note that Segal scored each of the reform scenarios independently from Wirepoints’ restructuring plan. The savings below are based solely on the changes listed and do not include a freeze of defined benefit plans, a move to defined contribution plans, or means-tested COLA benefits. As such, Segal’s results should only serve as a general guide of how Illinois pensions would be impacted if the state enacted any combination of the below in addition to Wirepoints’ baseline plan.

1. Impose a pension benefit cap

Segal scored the following proposal for TRS:

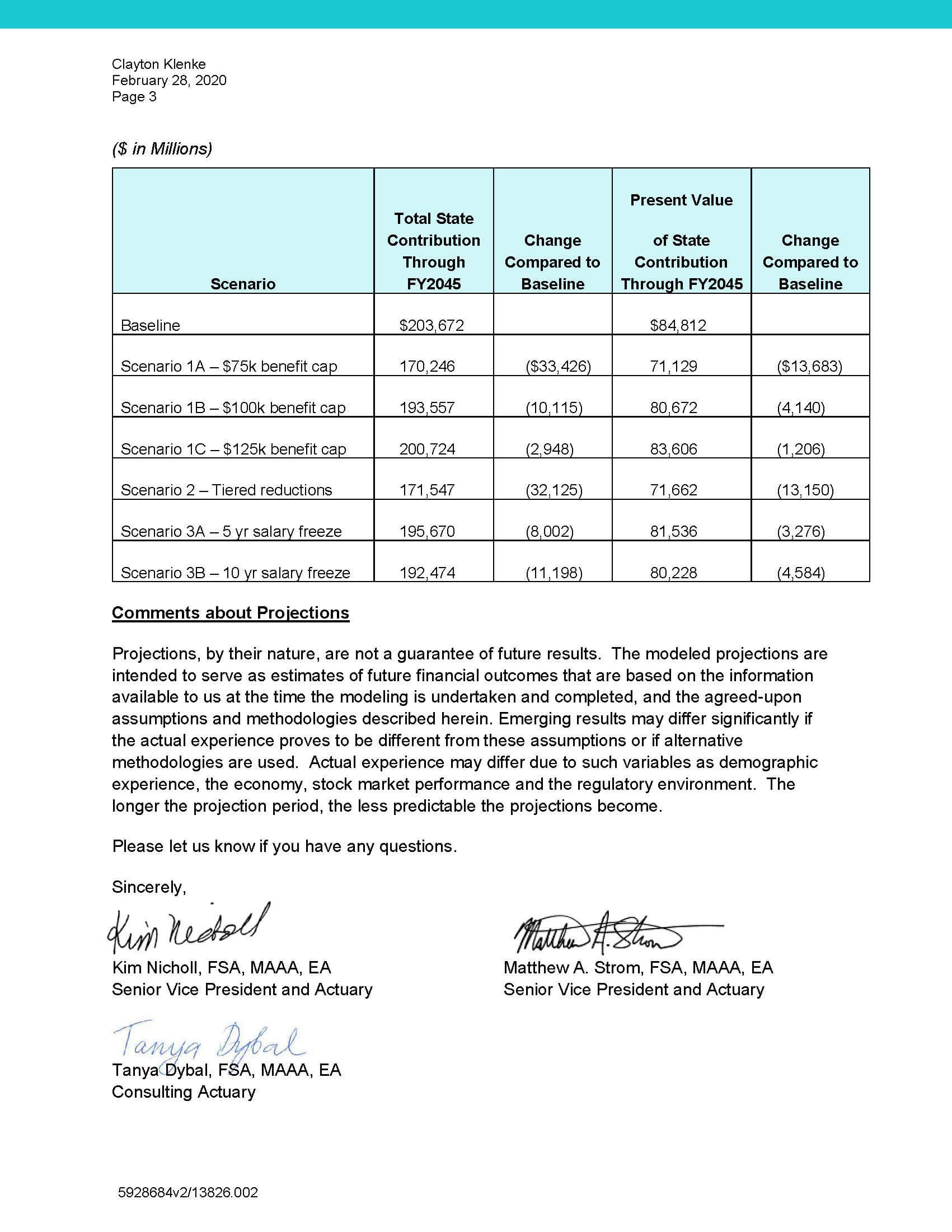

Maintain current pension laws, except: Impose a maximum benefit cap on the annual pension benefits of all current and future retirees (cap to be indexed to inflation going forward). Cap levels to run: $75,000, $100,000, and $125,000.

Current retirees with annual pension benefits above the cap would have their annual benefit immediately reduced to the cap amount.

Wirepoints has extrapolated the savings to include all five state funds, based on TRS’ share of the state’s total accrued liabilities. However, this method of extrapolation may overstate savings to a certain extent, as TRS’ mix of pension benefits differs from that of the other four state funds.

Enacting a benefit cap would reduce the present value of the state’s total contributions through 2045 by approximately $2 billion to $25 billion, depending on the size of the cap.

2. Tiered reduction in pension benefits

Segal scored the following proposal for TRS:

Maintain current pension laws, except: Immediately reduce all benefits of current retirees based on the following current annual pension amounts:

- Annual benefits of $50,000 to $69,999 reduced by 10 percent with a floor of $50,000.

- Annual benefits of $70,000 to $99,999 reduced by 15 percent.

- Annual benefits of $100,000 and above reduced by 20 percent.

Going forward, future members would have their initial annual benefits at retirement reduced based on the above brackets (Brackets to be indexed to inflation going forward).

Wirepoints has extrapolated the savings to include all five state funds, based on TRS’ share of the state’s total accrued liabilities. However, this method of extrapolation may overstate savings to a certain extent, as TRS’ mix of pension benefits differs from that of the other four state funds.

Enacting a tiered reduction of benefits would reduce the present value of the state’s total contributions through 2045 by approximately $24 billion.

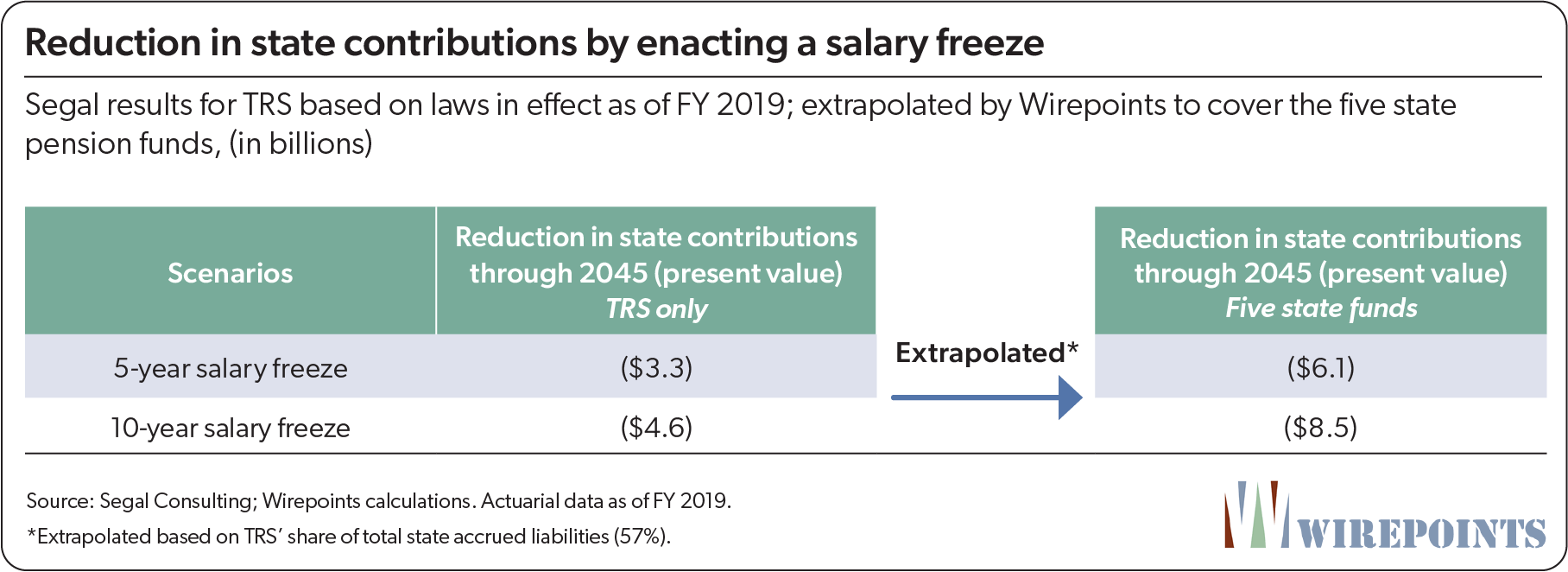

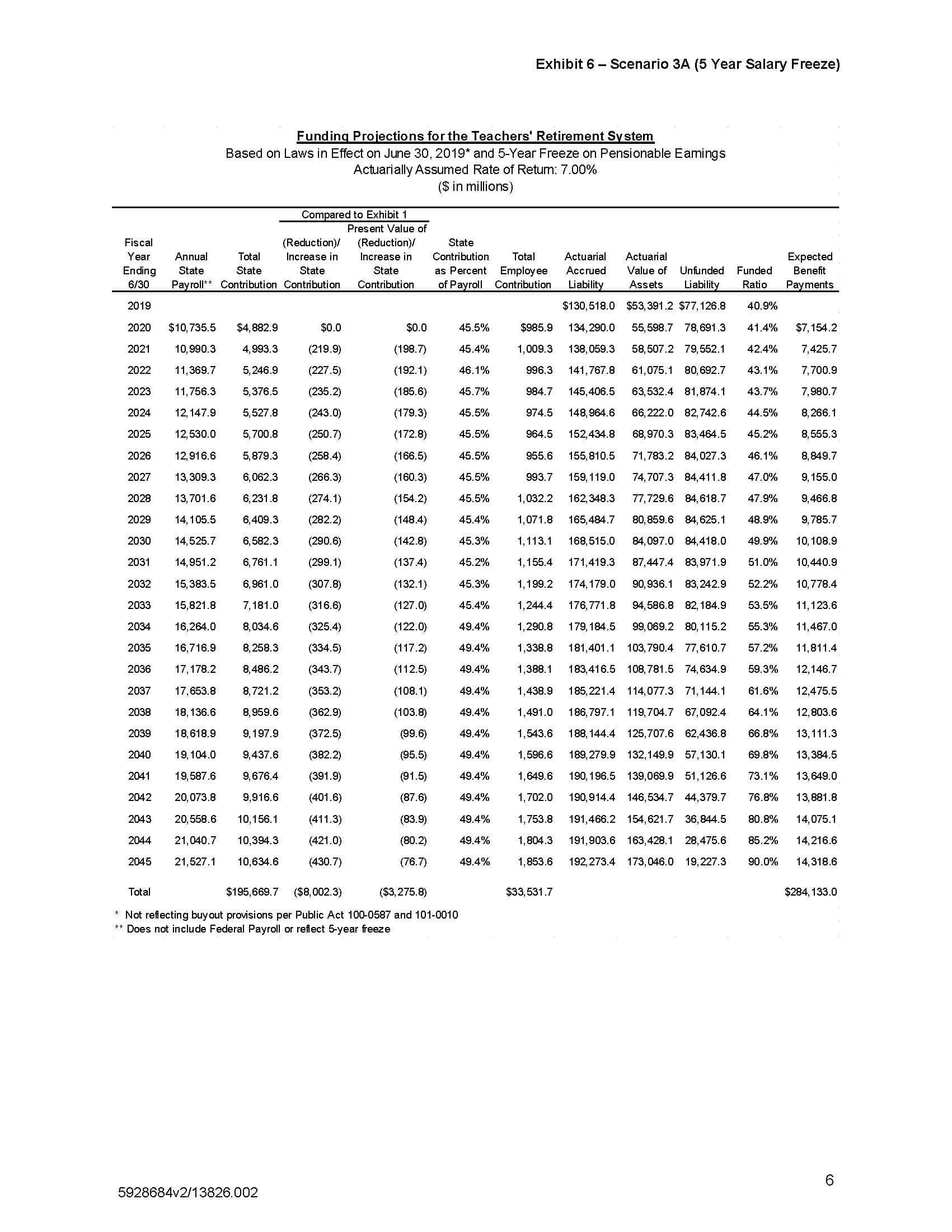

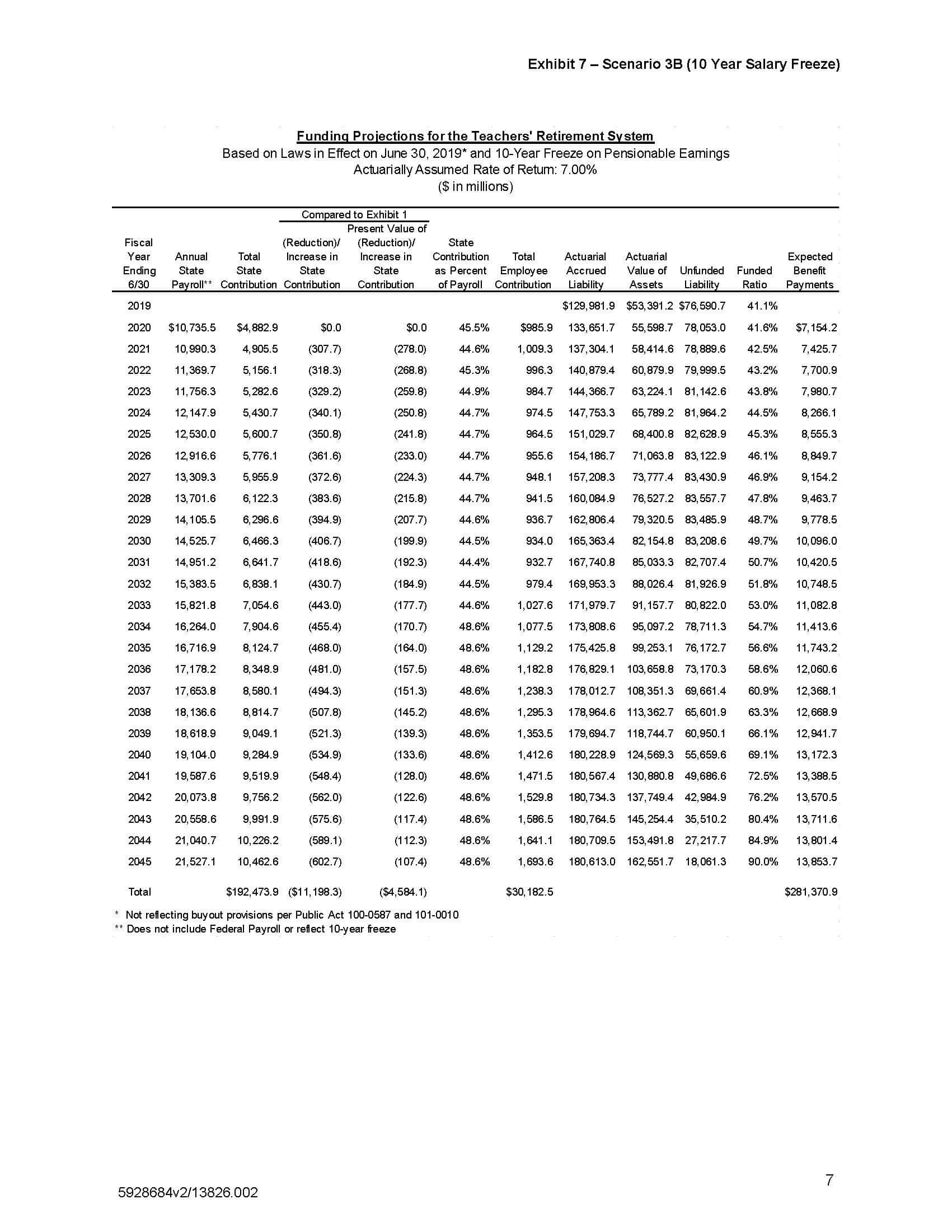

3. Pensionable salary freeze

Segal scored the following proposal for TRS:

Maintain current pension laws, except: Assume a freeze on pensionable salaries as of June 30, 2020, for all current and future active workers. Freezes to run: a 5-year freeze, a 10-year freeze.

Wirepoints has extrapolated the savings to include all five state funds, based on TRS’ share of the state’s total accrued liabilities. However, this method of extrapolation may overstate savings to a certain extent, as TRS’ mix of member salaries differs from that of the other four state funds.

Enacting a salary freeze would reduce the present value of state’s total contributions through 2045 by approximately $6 billion to $8.5 billion, depending on the length of the freeze.

Conclusion

Only 60 years ago, Illinois was a destination state for Americans and people across the globe. Illinoisans flourished alongside the state’s economic and manufacturing might, world-class universities, vast farmland, a massive transportation hub and much more.

Today, Illinois is no longer the beacon it once was. Bipartisan failure has made Illinois a national outlier – and in many cases, the extreme outlier – on the fiscal, economic and demographic measures that matter most. As a result, this state now has the nation’s worst credit rating, one of the country’s highest tax burdens and record out-migration. In this decade, Illinois has suffered the biggest population loss of any state in the country.

Too many families, entrepreneurs and small businesses don’t feel they can make it here anymore. They’ve lost confidence in Illinois’ leadership.

The state’s key influencers and the general public shouldn’t wait until Illinois becomes a failed state before finally demanding change. It’s vital to reform the state now, while it still has assets and dynamism, rather than wait until Illinois is a shadow of its former self.

Many fiscal, governance and economic reforms are needed to restore Illinois. This paper has focused on just one: the state’s overwhelming and suffocating pension debts. No state can properly serve its residents or take care of its most vulnerable if it’s constantly on the brink of a financial crisis.

No amount of higher taxes, policy Band-Aids and wishful thinking will help Illinois escape its downward spiral or become competitive again. Only a reduction in its monumental debts will.

Fortunately, more than a few voices have begun to call for an amendment to the Illinois Constitution’s pension protection clause. They include media outlets such as the Chicago Tribune and Crain’s Chicago Business; civic groups and policy organizations such as the Civic Federation, the Better Government Association and the Civic Committee; as well as political leaders including former Chicago Mayor Rahm Emanuel.

Wirepoints has made the case that an amendment to the Illinois Constitution is legal. We’ve shown why reforms are necessary and urgent. And we’ve laid out a baseline case for reform.

What Illinois needs now are leaders from all parts of the state to take the first step and push for a pension amendment.

Appendices

Appendix A. Defined contribution plans can provide

generous retirement benefits for state workers

A defined contribution plan like the one SURS provides can grant retirement benefits to state workers that are comparable to the current pension system. An investment return scenario based on actual annual returns of the stock and bond markets since 1978 is provided below. The portfolio is based on a split of the S&P 500 and Barclays U.S. Aggregate Bond Index.

Appendix B. Results of Segal-scored pension restructuring plan

Appendix C. Extrapolation of Segal-scored pension restructuring plan

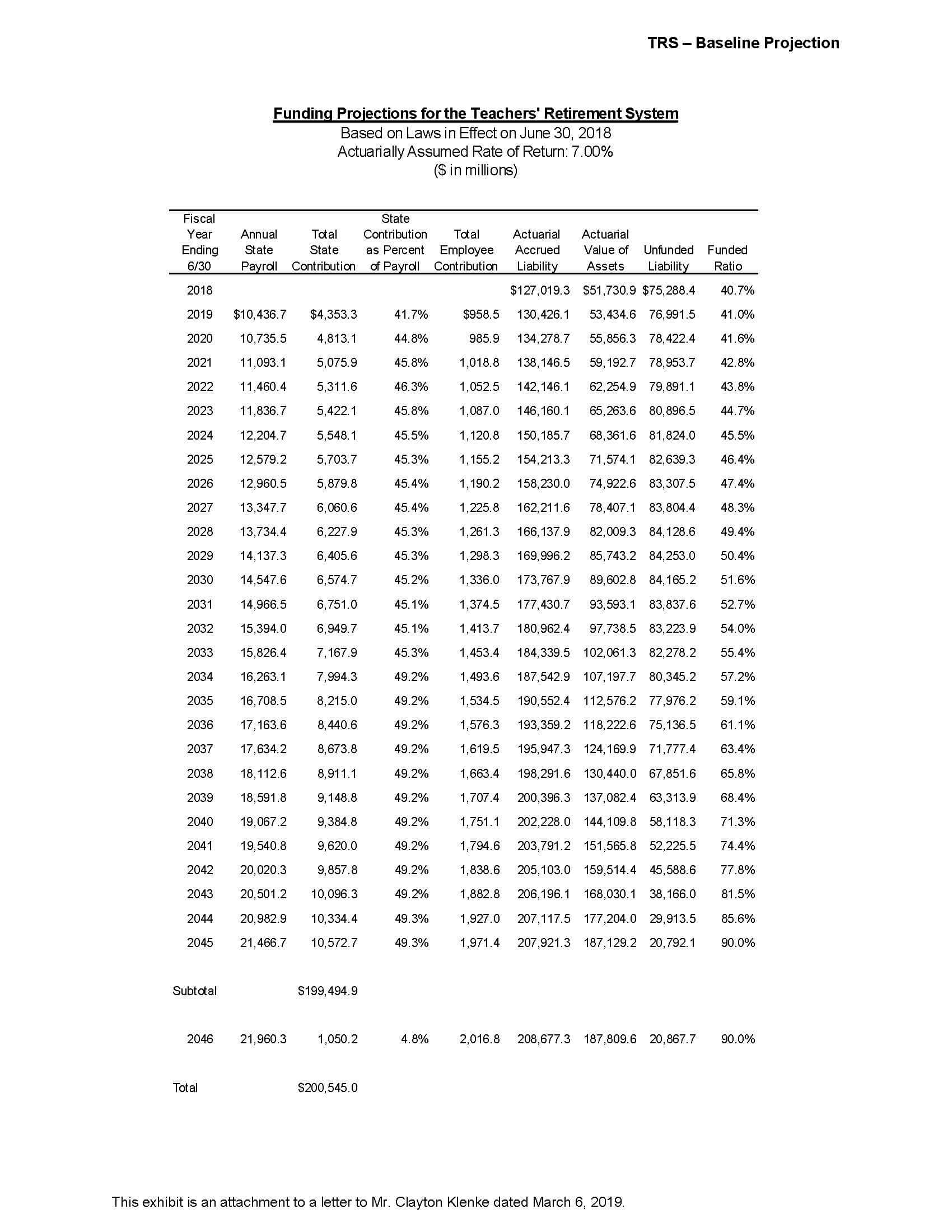

Wirtepoints’ restructuring plan was scored by Segal Consulting, the state’s actuary. The firm only ran reforms for the Teacher’s Retirement System (TRS) as of FY 2018 to limit actuarial costs. It also kept the state’s current actuarial assumptions and statutory payment formula to allow for an apples-to-apples comparison to current law.

The TRS run shows the following:

- An immediate reduction of TRS accrued liabilities to $99.7 billion from $130.4 billion in 2019.

- An immediate reduction of TRS unfunded liabilities to $46.3 billion from $76.9 billion in 2019.

- An immediate improvement of TRS’ funded ratio to 53.6 percent from 41 percent in 2019.

- Required state contributions to TRS through 2045 falling to $140 billion from $200 billion.

- TRS accrued liabilities in 2045 falling to $85 billion from $208 billion.

Wirepoints extrapolated the savings from the TRS run to estimate savings for a restructuring plan that includes SERS and SURS. Wirepoints’ extrapolation was based on TRS’ share of the state’s total accrued liabilities and employer contributions, an approach confirmed by Segal as reasonable for the purposes of this report.

Appendix D. Results of other Segal-scored potential reforms

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

Wow. I moved here in 2004 by way of AZ and IN. I currently live in Chicagoland Cook county. Sigh. With that background you know I am a former republican and with age and wisdom have become reformed. Just here for an outsider’s perspective. There is no way you can know what you are getting into until/when you move somewhere. You hear the stereotypes of IL/Chicago corruption. You kind of laugh it off until after 16 years with the help of this series you see how deep and intractable the problem is. Thanks Wirepoints for providing a solution that seems… Read more »

Congratulations and thanks again for the tireless efforts. I found only one reference to “collective bargaining” in the observation that reform would be needed. Is the thought to remove pensions and OPEB from the scope of mandatory bargaining? I understand that the issues presented would probably warrant another four-part analysis. If one assumes five to ten years of battles in the legislature and courts, and across the bargaining table, is there a way to assure that the status quo doesn’t endure for a long period and mitigate the benefits of the envisioned reforms? Collective bargaining agreements are contracts also and… Read more »

Collective bargaining wouldn’t matter much for pensions if we switched to the defined contribution plan like SURS has, as we proposed. For other purposes, the collective bargaining process does need reform, too. You needn’t wait to start getting the benefits of reform. If IL were serious about it (which it must be some day) the state could adjust its pension contributions immediately to conform to the reformed system. It could also pass legislation nailing those reforms down, to be effective contingent on passing the amendment. Yes, the federal government could help. We have written about how often. The pending bailout… Read more »

It is not a pension fund, but a HUGE PONZI SCHEME.

What a shame that all the good work you do falls on deaf ears and the only alternative left for the state residents is to no longer be one.