By: Ted Dabrowski and John Klingner

Wirepoints’ recent commentary on Illinois’ skyrocketing pension benefits – “Janus v AFSCME and the truth about Illinois pensions” – left many readers questioning where that massive growth in pension promises came from.

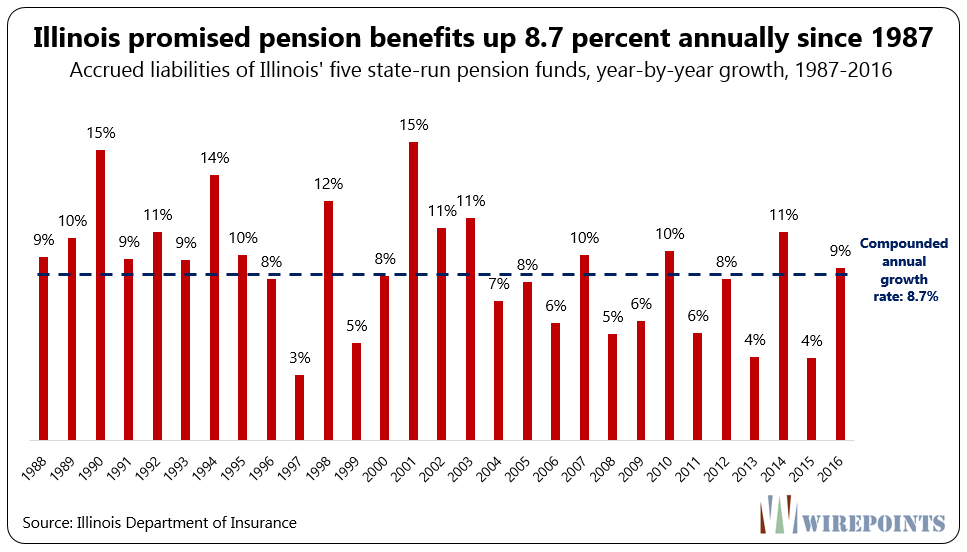

In our report “Illinois state pensions: Overpromised, not underfunded,” we showed how the growth in total pension promises to state workers and retirees has overwhelmed Illinois’ economy and residents’ ability to pay. Illinois’ total pension promises since 1987 are up 1,061 percent, 4.5 times more than the growth in the state economy.

The answer to where that growth came from is simple. The growth is due to overly generous benefits. In addition, reality occasionally forces more honest disclosure of the true cost of pension promises made. In other words, more accurate reporting also pushes the numbers up.

Illinois politicians have doled out all kinds of expensive benefits over the past few decades, from compounding cost-of-living increases to service credit for unused sick leave to early retirement ages.

That’s caused a host of problems, because the Supreme Court has declared that the pension benefits of current workers untouchable. The state’s constitution says pension benefits can’t be “diminished or impaired.”

It’s a hypocrisy. Pension perks can be increased ad infinitum, but it’s impossible to scale back benefits that existing workers haven’t even earned yet.

Take teachers and their benefits, for example. Their pension fund makes up more than half of Illinois’ promised pension obligations.

The Teachers Retirement System publishes the entire list of changes to the pension plan since 1915. Teacher pensions were generous to begin with, yet lawmakers continued to add new sweeteners and bigger benefits over time.

Below is a list of some of the biggest changes:

Cost of living increases

Overly generous cost-of-living benefits – compounded and granted automatically regardless of inflation – are what arguably cause the most fiscal stress to pensions’ solvency. What started as simple COLAs at levels approximating inflation have now become compounded yearly increases that double a retiree’s annual pension after 25 years.

- 1969 COLA increased to 1.5 percent simple

- 1971 COLA increased to 2 percent simple.

- 1978 COLA increased to 3 percent simple.

- 1990 The 3 percent annual COLA increases begin compounding annually.

Pension formula

Pension benefits for every year worked were originally calculated as 1.5 percent of each worker’s “average final salary.” The max starting pension was restricted to 60 percent of a teacher’s final salary. By 1998, that amount was increased to 2.2 percent of salary and max starting pension became 75 percent of final average salary.

Under the original rules, a teacher had to work 40 years to get the 60 percent maximum. Today, a Tier 1 teacher only needs to work 34 years to get to a much higher 75 percent maximum.

- 1947 Pension formula: 1.5 percent of average final salary per year of creditable service. Average final salary calculated based on the last 10 years of service. Maximum starting pension as a percentage of final salary became 60 percent.

- 1971 Pension formula upgraded to 1.67 percent for first 10 years; 1.9 percent for next 10; 2.1 percent for next 10; and 2.3 percent for years over 30. Average final salary calculated based on the highest four consecutive years within the last 10 years of service. Maximum starting pension as a percentage of salary became 75 percent.

- 1998 Pension formula upgraded to 2.2 percent a year. TRS member contributions increased by 1 percent.

Sick leave benefits

Unused sick leave days in the private sector are typically use it or lose it, with some limited ability to roll over unused days to the next year. But teachers in Illinois, and many public sector workers, get much more. They can accumulate unused sick leave days over the course of an entire career – and then cash them in as years of pensionable service – an extremely generous benefit unheard of in the private sector.

- 1972 Credit for one-half year or 85 days of sick leave granted.

- 1984 Maximum of one year of service for 170 or more days sick leave credit granted

- 1998 Sick leave could be used for credit, if not compensated in any way.

- 2003 Members with up to two years of unused sick leave credits could exchange that sick leave for up to two years of service credit.

Retirement ages

Teachers can begin drawing pensions with full benefits while still in their 50’s. And a majority of teachers took advantage of this rule. Sixty percent of teachers currently collecting a pension retired in their 50’s.

- 1947 Retirement permitted at age 55 with 20 years service and at age 60 with 15 or more years of service

- 1969 Retirement permitted at age 55 with 20 years of service, 60 with 10 years service; age 62 with 5 years

Some of these increases were paid for with increased employee contributions, as outlined in the TRS document outlining the benefit increases. But many were not.

And that’s left Illinois residents holding the bag.

Telling the truth

A second reason the reported cost of Illinois pension promises have grown is because Illinois politicians are being forced periodically to measure that cost more honestly.

They are often forced to change outdated assumptions that understate those benefits. For example, retirees are living far longer than originally assumed. And assumed stock market returns are overly optimistic.

As those faulty assumptions are corrected, the amount owed to pensioners only goes up.

In 2016 alone, assumption changes contributed $10 billion of a $17 billion jump in promised pension benefits.

The combination of benefit increases and assumption changes have been going on for years, as reflected in the leading graphic of this piece.

As a consequence, the cost to taxpayers has increases year after year. The employer’s (taxpayers’) annual “normal costs” for teacher pensions has grown 5 times since 1987, far in excess of the economy. And as a percentage of payroll, employer normal costs have grown to 10.1 percent from 7.3 percent, a 38 percent increase.

Incompetence or Malice?

Lawmakers actions have driven the state into to virtual insolvency. Illinois’ near-junk credit rating, years of unbalanced budgets and steady outmigration are clear evidence of that.

A financial mess like the one Illinois politicians have created would normally be investigated.

If this state were a corporation, think Enron or Worldcom, an official inquiry would be asking all sorts of questions. How did lawmakers get pensions so wrong? Was the extreme growth in benefits due to incompetence or was it purposeful?

Either way, lawmakers hid a massive liability from Illinois residents for decades. That’s damning proof they should never have been in change of government worker retirements in the first place.

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

The article acknowledges that the normal employer cost of TRS pensions in Illinois, while having grown substantially, is still only 10.1% of payroll. Given that the state does not contribute 6.2% of payroll to Social Security, this cost seems quite modest. Consider a company like Walmart, which pays the 6.2% into SS and matches employee contributions into a 401k of up to 5% of payroll dollar for dollar. Isn’t Walmart’s normal cost higher? The difference, of course, is that Walmart was not allowed to short promised contributions in past, so its 11.2% of payroll cost is managable, while Illinois is… Read more »

Thx Professor Szakmary. I always appreciate your expertise and analysis. Your disipline of Economics lends clairity to the muddled subject of pensions. Wirepoints spins the data, calls it research, and then attempts to control the message. The message for Wirepoints is that overpromised union benifits are the root of our economic troubles, and not the chronic underfunding and pension holidays. Why? Maybe before we convince people to take away our 1st grade teachers retirement, or chop it down to 30 cents on the dollar, we must also convince people that the teachers retirement was over generous and its undeserved. Its… Read more »

Advocate, have you come up with a plan yet for how to solve our pension crisis beyond “raise taxes and cut spending”? A hallmark of the today’s left is just yelling “fake news” about facts they don’t like without any contrary evidence, as you have done. Szakmary put up something concrete and I will let the authors answer. You should try that. And those who say we are trying to steal from helpless teachers, torture puppies all the rest will rue the day when the inevitable pension haircuts start. It will be clear that denial and opposition to reform only… Read more »

” Wirepoints spins the data, calls it research, and then attempts to control the message.” (Advocate) And even the Wall Street Journal is falling for the hype. Mr. Szakmary is correct. The proper comparison of increase in pension costs is the annual normal cost, not the “Promised pension” (accrued liability). And the normal cost has increased. That is a valid factor to consider once you drop this “Promised pension” diversion. From your June 27 article: ” Wirepoints’ findings also dispel the claim that too little money in the pension plans caused the current crisis – state pension assets, buoyed by… Read more »

In a sense, it’s self-evident that too little funding caused the problem. Had we put in all that’s needed there would be no problem. But isn’t a quarter of our budget enough? Yes, that portion was lower in early years and occasionally zero, but public unions actually lobbied for that to free up cash for higher current salaries, foolishly relying on the constitutional pension protection clause to later print money. And, no, trends in normal cost mean nothing. All employees hired since 2010 have a lousy benefit with low normal cost that drags down the average. The problem is unfunded… Read more »

“a quarter of our budget” is mostly just interest on the unpaid liability (and still doesn’t catch up). Interest which would not be due ..if.. the proper contributions had been paid in the first place. Proper contributions, plus returns on investment, should have accumulated assets equal to liabilities, and the only thing due from this year’s budget would be normal costs… 10 percent of payroll, not 25 percent of the budget. “trends in normal cost mean nothing.” ? Of course they do. They are the true cost for pensions this year… 10 percent of payroll, not 25 percent of budget.… Read more »

” Advocate, have you come up with a plan yet for how to solve our pension crisis beyond “raise taxes and cut spending”? ” Leo Durocher said “You’ve got third base so screwed up nobody can play it. ” I’ve never met Advocate, but I can safely say he has no such plan. For Illinois and a few other states, it’s already too late. Still, “fake news” is a legitimate claim. For those states which may yet save their pension plans, it is important to determine the actual cause of underfunding. If this Wirepoints farce convinces enough people that increased… Read more »

Isn’t Walmart’s normal cost higher? That’s not a valid comparison. Once Walmart contributes their 12.2% (their 401k match is 6%, not 5%) towards an employee’s retirement, they immediately absolve themselves of all responsibility and risk of funding that employee’s retirement beyond that point. For a mere 2.1% premium of gross wages, that seems like a pretty good trade for Walmart. You, as with most public sector opinions on this matter, simply refuse to value risk. Furthermore, no late career promotion or pension spike will ever impact that percentage. An employee working his way up from supervisor to district/regional manager in… Read more »

As usual, the situation is always a bit more complex than what it seems. The reality is that Tier 1 employer normal costs are higher and growing. The problem with the numbers is that Tier 2 normal costs are dragging down the average normal costs of TRS. (Numbers below are for 2019.) Overall Tier 1 normal costs are 21.65 percent. Employees cover 9 percent and the remainder, 12.65 percent, is covered by the employee. Tier 2 employer normal costs, on the other hand, are projected at just 7.11 percent. Employees cover 9 percent, meaning that Tier 2 net costs for… Read more »

Back to the Walmart example: Then the employer portion of the Tier 1 normal cost is equal to an employer contributing 6.2% for social security plus offering a 6.5% employer 401k match, a generous percentage I have never seen in the private sector. And with ZERO RISK.

You make the point about social security, but fail to acknowledge social security benefits are not guaranteed and currently projected to give retirees a 25%. And for clarity social security also tok the equivalent of a pension holiday under Obama’s Payroll tax Cut which essential allowed workers to gain social security and earnings credits without making offsetting contributions. In addition social security: – is skewed to lower income earners – reduces the benefit for those receiving more than a nominal payout by taxing up to 85% of the benefit at the highest marginal rate. – considers income from all sources… Read more »

Still confusing the issue with “promised pension benefits” (accrued liabilities). How much, in dollars, has the average public pension increased? According to Jane the actuary: (from a 2018 Pew report.) “Benefit payments have risen spectacularly” “…benefits paid out by public pension plans came in at roughly $100 billion in 2000. In 2016, they had tripled, to about the $300 billion mark.” That is semi-dramatic, but nothing like a thousand percent in thirty years. As one example of increased benefits (not benefit “promises”)… In 2001, CalPERS paid out $5,792,948,968 to 375,540 recipients. Ave. pension $15,426 In 2006, they paid out $9,236,073,498… Read more »

If anyone were interested, it should be possible to recalculate the payout to each beneficiary if none of these increases had taken place, and the money that would be in the pension fund if a higher amount had been in it and achieved investment returns. The remaining shortage would be shorting by taxpayers. In NYC, I believe that more than 100 percent of the pension deficit would be due to retroactive pension increases. In California, it is most of it. But there are pension deficits in Red States with weak unions, low taxes, and few if any pension increases too.… Read more »

“In NYC, I believe that more than 100 percent of the pension deficit would be due to retroactive pension increases. In California, it is most of it.” I don’t think so. Now you’re introducing another term. Pension deficit can occur whether pension “benefits” have increased or decreased. In the Wirepoints “promised benefits” is the same whether the plan is fully funded or grossly underfunded. From Wirepoints July 9 article: “The report proved a lack of dollars wasn’t the issue.” The report proved no such thing. Quoting a poster from another blog: “We need to see the raw annual expected benefit… Read more »

One generation took more and more out and put less and less in. The generations to follow are being forced to put more and more in despite getting less and less out. This applies to public workers, as well as taxpayers. And applies to other state and local governments, the federal government, business, and even many families as well as to Illinois. Why does no one ever suggest that the state constitution be changed and benefits for existing beneficiaries cut back to what workers were promised when they were hired? And why are union-backed politicians so willing to slash the… Read more »

Why is retirement income still exempt for Illinois state income taxes? Many people’s jobs are bound by situs. However once you are retired other states with better climates, actual things to do, and far lower property taxes and lower dining taxes strongly beckon. I know in the late 70s and early 80s out of state developers strongly targeted IL manufacturing reiterate for relocation to out of state retirement havens. Without the exemption Illinois would have had a dramatic our migration pattern decades earlier. When you think of it, there is very little to recommend IL for retirees. I suspect family… Read more »

public service unions are large, organized and well-funded (by taxpayers) and have used their massive wealth to buy politicians and judges across IL. Taxpayers are not organized, fund themselves and have little or no influence on politicians. Also, the public votes do not matter in IL elections, Madigan has his district locked up with new schools being built every year, trees in every yard, driveways shoveled every year, etc., which he is how he has stayed in the House for 35 years as the rep for the 22nd District. In the House, Madigan owns the votes of almost all of… Read more »

Richard: Fascinating, and sounds certainly 100% true. It’s surprising that the top decision-makers at the major newspapers and TV news stations, have ignored the fiscal malfeasance of the legislators, unions and courts. So the general public has remained uneducated by the press. Why has the press abdicated a key duty of theirs? Weird. It’s even true of the Wall Street Journal which I stopped paying for. They never had an article showing how Americans are overtaxed. They should have had areticles on page A-1 weekly, then the public would be more inclined to vote for the issue, after seeing how… Read more »

Illinois citizens have chosen to keep Madigan by voting for his fellow democrats in most elections. (Of course many didn’t think it important enough to even vote.) Most of the time they had a choice to vote for a non-democrat, and for reasons I don’t comprehend, continued to vote for the democrat. I can only assume that they are ok with how the state is currently being run. For the rest of us in the minority, we recognize it’s too late to fix thru normal channels. (At this point, does it really matter who the next gov is, or if… Read more »

The last time I checked, Illinois still has elections. That means the ultimate responsibility still belongs to voters. The voters deserve this mess. Luckily, leaving the state is still allowed. When enough voters do that and pensions fail due to loss of tax base, the unions won’t believe anything the liberal politicians promise. Then just maybe, things will start to reverse course. As for me, a person in the Illinois private sector, I’m not sticking around to see how it all turns out. Bye Illinois. Have fun blaming each other and begging everyone that will listen for help (loans/bailout).

Amen. This is on the citizens. As someone who ran for public office a few times on a reform agenda I saw the voter apathy first hand. When I go to grocery store or out often people recognize me and walk up and start bitching and tell me I should run again. Of course they will do nothing to help you. Often I take their name and check it against the voter database. What I have noticed is theses very vocal people only seem to vote in the Presidential election and often not even in the primary. My experience is… Read more »

Wheaton-Warrenville had a school referendum in 2017 for $132 million – to build one new pre-school and fix 18 out of the remaining 19 other schools. There were four school board candidates who were pro-referendum and four against. We put signs all over the district saying vote “NO” and listing the four anti-referendum candidates. The tax increase was voted down (resoundingly)! But, the four union-backed, newspaper-endorsed, pro-referendum candidates won. Looking at the details, many of the “NO” voters under-voted (or left blank) the school board trustee race. The number of “yes” votes was almost the same as the number of… Read more »

Exactly. The Illinois voters (or non-voters) as a whole are responsible for this situation, and that includes me. At this point, having watched my supported candidates fail to be elected over and over, I know when I’m beaten. To all my fellow Illinois voters that usually vote for the winner, congratulations. You win. I apologize for opposing your majority values. I won’t stand in your way any longer. Enjoy your Illinois paradise and I’ll find someplace else to live. Oh, …. and thank you in advance for paying my accrued portion of the state debt.

In the 1991 AFSCME contract signed by Edgar, the state began to pick-up the employee portion of the pension contribution into SERS and SURS. I think the pick-up continued into the George Ryan administration. Proving you don’t have to directly enhance the pension benefit to enhance the pension benefit.

I was a SURS participant from 1990 to 2001, and at no point did my employer pick up my employee contribution. 8% of every single paycheck that I received was deducted for SURS.

Because you were not a member of AFSCME, as some university employees who participate in SURS were.

I agree with what you have written, but let’s not let the taxpayers off the hook. For example where were they when it came to local elections, school boards etc? Even when candidates run at the local level and made a point of making pension obligations an issue, the public sat on their hands. Citizens are suppose to direct the focus of their Government and monitor their implementation. Each citizen has a civic duty to follow their city council meetings, County Board meetings and Park District board, Township meetings and give them direction. Here is the simple truth. ALL government… Read more »

…interesting points P M about voter responsibility and accountability. Your brave to speak the plain truth about where the fault or responsibility lay. But here on wirepoints we like to blame Democrats and Union bosses for our plight. Easy targets….backroom deals boogeyman. Republicans and voters are victims in this mess. If we only had a republican assembly and republican government all of our problems would disappear….and would never have happened in the first place. Cough. Pointing responsibility back upon the voters, who voted for their own government, only leads to cries of selective institutional disenfranchisement. The Govt of Illinois,and policies,… Read more »

We have been exceptionally harsh on Republicans where they went wrong, especially Radogno, Edgar, Rauner and Durkin. We don’t have a republican form of government. It was hijacked.

Well looking prospectively, looking forward….Its always the republicans who have the better answers not democrats. Right?

There are many points on the spectrum (from far left to far right) and R vs D does not begin to capture them. However, many have observed that cities with a 40-50 year history of consistent Democratic rule are the ones that have failed their employees and their citizens most consistently. Exodus from those cities by both responsible and irresponsible citizens is a good barometer and even weathermen need a good barometer from time to time. Should I seek a public pension prophet, I’ll take Glennon over Klonsky any season of the year.