By: Ted Dabrowski

Gov. Pritzker has no problem hitting up Illinoisans with tax hike after tax hike, but he won’t reform one of the richest public sector benefits in the country – Illinois’ automatic, compounded, 3-percent cost-of-living adjustments for pensions. Skyrocketing pension costs are overwhelming the state’s finances and COLAs are one of the biggest drivers.

COLAs drive up the cost of pensions in Illinois because they double a retiree’s yearly pension after 25 years. Since the state has nearly 500,000 active workers and beneficiaries who benefit or will benefit from this COLA, it’s easy to see why the state has racked up nearly $140 billion in officially-reported pension shortfalls.* Reducing COLAs through some form of means-testing can reduce the state’s unfunded liability by some $50 billion, depending on how that means-testing is applied. Wirepoints has laid out a baseline reform plan scored by actuaries here and here.

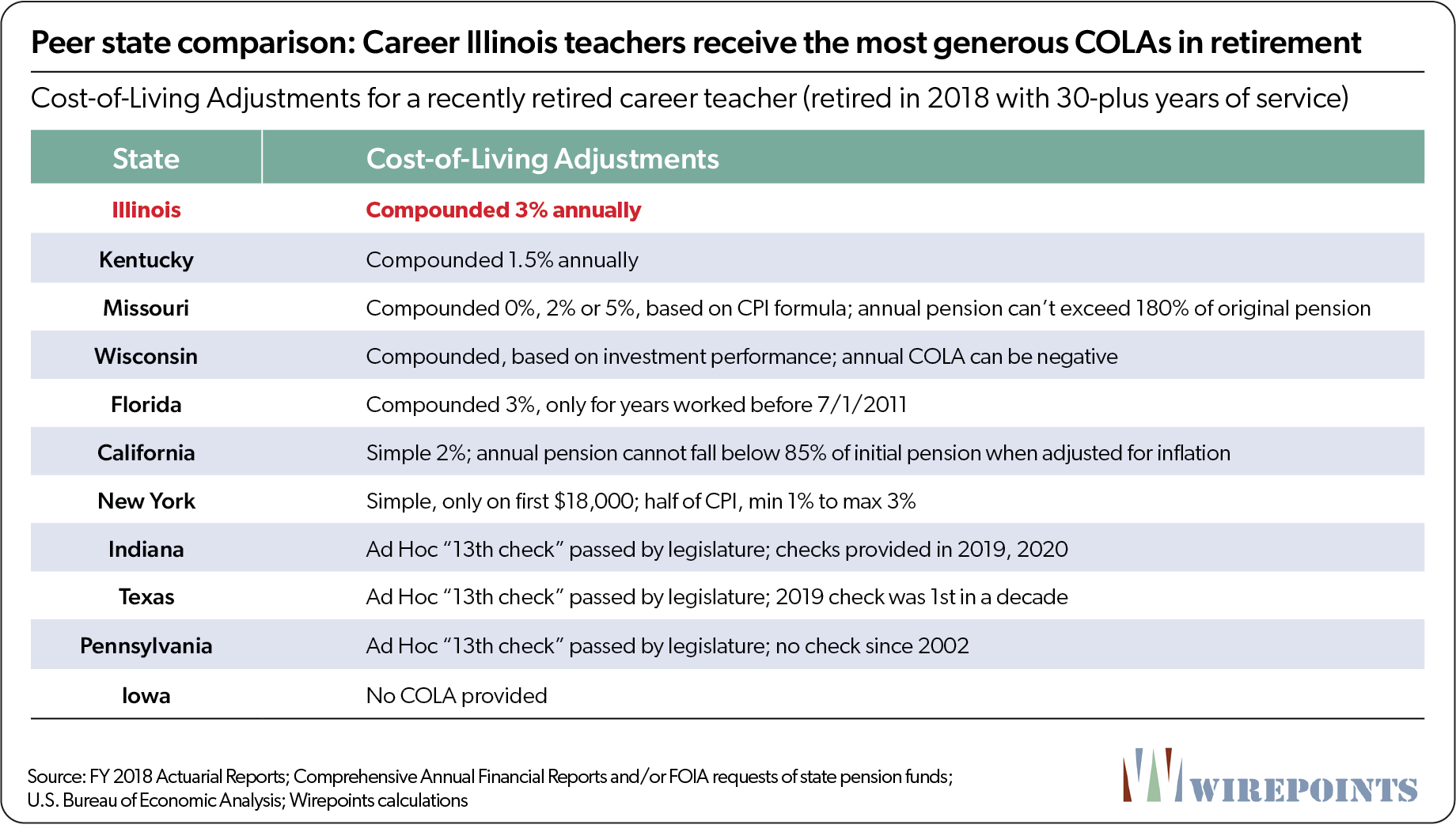

Illinois is a national outlier when it comes to COLA benefits. The state’s formula for increasing a retiree’s pension each year is simply overgenerous. A comparison of teacher pension benefits in Illinois vs. those in its peer states – Illinois’ five neighbors and the nation’s five largest states – makes that clear.

While there are many factors that impact a teacher’s overall pension benefits, cost-of-living adjustments have a major influence because they determine how much annual benefits grow in retirement, if at all.

While there are many factors that impact a teacher’s overall pension benefits, cost-of-living adjustments have a major influence because they determine how much annual benefits grow in retirement, if at all.

Illinois’ COLA started as a simple annuity increase of 1 percent. But several boosts by lawmakers have turned the benefit into a costly, compounded yearly increase that blows past inflation.

1969: COLA increased to 1.5 percent simple

1971: COLA increased to 2 percent simple.

1978: COLA increased to 3 percent simple.

1990: 3 percent COLA increase compounded annually.

To get a quick understanding of why Illinois’ COLAs are so expensive, take a look at the below chart. It shows how a career teacher’s starting $100,000 pension grows during retirement, comparing Illinois with three states with different COLA formulas.

What stands out is how much faster benefits in Illinois grow. A $100,000 pension for a teacher who retires at 61 will become $203,000 by the time that teacher turns 86. In contrast, a teacher in Kentucky with the same starting pension would see her pension grow to $143,000 after 25 years, the result of a lower 1.5 percent compounded COLA.

New York’s COLA formula offers a simple 1 to 3 percent cost-of-living adjustment, depending on annual inflation, but only on the first $18,000 of a retiree’s pension. That means a retiree’s starting $100,000 pension can grow to a maximum of just $113,000 after 25 years.

Finally, Iowa provides no yearly COLA for members who retired after June 30, 1990. A retiree’s pension stays at $100,000 throughout retirement.

COLAs in other peer states are far less generous

COLAs in other peer states are far less generous

Texas, Pennsylvania, and Indiana only grant COLAs on an ad-hoc basis, meaning the legislature decides each year whether to grant an increase, also called a “13th check.” That rarely happens in some states. Last year, Texas gave its first increase in more than a decade and Pennsylvania hasn’t granted an increase since 2002. Indiana granted small 13th checks to retirees in 2019 and 2020.

Florida stopped offering an automatic COLA in 2011. And Wisconsin’s COLA benefit varies widely from year to year based on the fund’s investment returns, sometimes even creating negative COLAs.

Missouri provides a zero, 2 percent or 5 percent COLA depending on an annual inflation formula, but it prevents the annual pension from ever exceeding 180 percent of the retiree’s original pension.

Even big-spending California doesn’t offer COLA benefits as generous as Illinois’. California grants a 2 percent simple COLA with a special provision protecting against inflation.

COLAs vs. private sector

Illinois teachers receive far more generous benefits than their peers, but a more appropriate comparison is to the retirements of the private sector workers who pay for public sector workers. That’s where real discrepancy exists.

Private sector Illinoisans retiring today would have to have approximately $1.8 million to $2 million at the time of their retirement to get the same $2.3 million lifetime payout career state workers receive. The vast majority of ordinary Illinoisans have nowhere near that amount saved.

And the benefits provided by Social Security don’t approach the level of pensions, either. The average Social Security benefit for Illinoisans is just $17,000 a year, while the annual maximum is just $36,000. The combined benefits in the private sector from retirement accounts and Social Security don’t come close to matching the pension of a career public sector worker.

And the benefits provided by Social Security don’t approach the level of pensions, either. The average Social Security benefit for Illinoisans is just $17,000 a year, while the annual maximum is just $36,000. The combined benefits in the private sector from retirement accounts and Social Security don’t come close to matching the pension of a career public sector worker.

The value of COLA reforms

Illinois won’t escape the nation’s worst pension crisis without major reforms, which first requires an amendment to the Illinois Constitution’s pension protection clause. Tax hikes won’t help, they’ll only prolong the state’s reliance on the broken retirement system.

Reforms begin with tackling COLAs, the biggest driver of the state’s overpromised pensions.

Wirepoints scored a series of COLA reforms via the state’s actuary, Segal Consulting, to determine what savings the state could generate. While there are an infinite number of potential, viable COLA reforms, Segal scored three particular baseline scenarios.

The first scenario suspends COLAs for all current and retired teachers until the Teachers’ Retirement System (TRS) returns to 100 percent funding. The reduction in the unfunded liability for TRS was approximately $35 billion, a 45 percent decrease. That reduction becomes $61 billion when the reform is extrapolated to include all five state-run funds.

The second reduces COLAs for all members to 1 percent simple going forward. That reduces the TRS unfunded liability by $26 billion, a 34 percent reduction. Grossing up those savings for the five state-run funds means the unfunded liability for the state would drop to $88 billion from $134 billion.

The final scenario means-tests COLAs. Everyone with a pension below $50,000 would receive a 1 percent simple COLA, while annual increases for those with pensions greater than $50,000 would be suspended. Savings for the state comes in-between the two scenarios above: $31 billion, a 40 percent reduction in unfunded liabilities. Illinois’ debt is cut by $54 billion when extrapolated to include the five state funds.

In all, these reforms can save the state an average of about $3-$4 billion annually which makes the “need” for a progressive tax hike moot.

Illinois needs reforms, not tax hikes

Retirement costs, including the cost of pension obligation bonds, currently consume nearly 30 percent of the state’s budget, eating into all other core government programs. Without reforms, the Commission on Government Forecasting and Accountability calculates retirements will consume at least a quarter the budget for the next 25 years.

All that seems to mean nothing to lawmakers, who have Illinoisans debating tax hikes instead of structural reforms.

*Moody’s, using more realistic actuarial assumptions than officials at the state do, calculates Illinois’ pension debt is now at $261 billion. That amount makes Illinois the nation’s extreme outlier when it comes to pension shortfalls, both in outright terms and on a per household level.

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

I actually to a pay cut this year. No raises as the company is not making money. Taxes on my home have gone up and so has the cost of everything I buy. I feel like I am being gouged every time I pay sales tax. Thank goodness that the non workers are getting a 3% raise, after all they deserve it much more than the Poor honest hard working taxpayer.

Have to go eat Mac and Cheese again tonight.

The only constitutional amendment we need is one to amend the state pension system, not one to give politicians broader taxing power!

I Know what i am doing, and that is voting for all democrat’s running in state elections, voting for all republicans in federal elections, and Voting YES on the fair tax….and Immediately moving out of this state….good luck to the rest of you suckers

EXCELLENT framing of the real problem Illinois has..

These outrageous COLAs that the unions get are immoral and an insult to working class families

Governor Slobbo is just rearranging the deck chairs. The State can’t even afford to pay the guy who follows him around with a tuba. Democrats are destroyers.

One can debate forever about 3% compounded vs 1.5% simple while their taxes climb and their real estate value stagnates. Or, they can “know when to fold them” and get the hell out. Obviously, some citizens can’t/won’t leave, but those on the fence need to realize that the unions will never loosen their strangulation hold on the throats of Illinois taxpayers until the victim is lifeless. Leaving Illinois is not an irreversible decision so if you’re on the fence give it a try. I wonder how many people that move south actually move back to the Land of Public Section… Read more »

Looking for out of state jobs as we speak!

Here’s all you need to know: While hundreds of thousands lost their jobs or took pay cuts, the state will be giving pensioners a 3% raise to not work. And they won’t pay one dime in state income taxes to boot.

Optics, my friends, optics. All your legal arguments fall flat when the unemployed’s calls IDES go unanswered, when employee bonuses vanish, when your employer ceases their 401(k) match, when your stellar year-end review simply means you stay employed with no raise. Optics.

Just a reminder that in 1989, Governor Thompson signed the high COLA legislation. Click on link to see his 1989 press release touting the action. http://media.apps.chicagotribune.com/pensions/thompson_press_release.html

If you check out Sen Calvin Shuneman in 1989 on how he voted against replacing the 3% simple interest with the 3% compounding which he warned that it would inflate pensions costs down the road. I believe this was Senate Bill 95 Public Act 86-273. I am trying to find the actual written transcripts when that was passed and how the 3% was factored in. If memory serves me correct the 3% compounding starts when certain criteria are met of working at least 20 years and must be age 55 but if you continue to work past 55 the 3%… Read more »

It’s possible the the 3% compounding was only intended for lawmakers but everyone jumped on the bandwagon but not sure. This should fall under the Omnibus Pension Bill June 30,1989 starting at page 326.

It appears Chicago Tribune has the transcripts you seek but there does not seem to be a link to the transcripts. See https://media.apps.chicagotribune.com/pensions/document_narrative.html

“Senate transcripts from 1989In this transcript from June 30, 1989, state Sen. Emil Jones Jr. and his colleague Calvin Schuneman debate the merits of a bill that would end up increasing the cost-of-living adjustments to the pensions of state workers and City of Chicago employees. The bill also provided a special perk that allowed state lawmakers to boost their pensions dramatically if they served more than 20 years.”

Thank You. I checked just as a comparison the prime rate in 1989 was 10.5% but the 3% was never adjusted to any measure of inflation or interest rate which many other states did. So at that time 3% seemed appropriate but less so in these days with rates near zero.

The state thought they were clever making it 3% fixed. Obviously that doesn’t look like a good decision today. Although give it some time. The way the fed is spending money that 3% could look like a bargain again.

They could’ve said “3% compounded COLA for anyone who retired prior to 12/31/1988” or something like that. The main concern was all those teachers who retired in the 1970s with small pensions being left in the dust by inflation. 3% compounded makes sense for those pensioners. But teacher salaries really took off in the 1990s, and when combined with other pension enhancements (2.2 rule), it made no sense to give those retirees the same benefit.

SB 95 / PA 86-0273 included replacing the simple interest COLA with a compound interest COLA for the five “state” pension systems (TRS, SERS, SURS, JRS and GARS). That aspect of the law became effective January 1, 1990. However, don’t assume each of the 5 have identical 3% COLA rules. The COLA rules are on the websites of each pension system. The comments regarding Emil Jones Jr and Carl Schuneman originated from the Chicago Tribune Pension Games series of articles published in 2010 – 2012 which was written by many journalists including Jason Grotto and Ray Long. http://media.apps.chicagotribune.com/pensions/index.html The documents… Read more »

Thank You everyone. It is appreciated. Remember when this was negotiated in 1989 the world wide web was still not in place. www started in Aug of 1991 so we had to do some digging or rely on local news to see what is passed and very few really cared except for the recipients. Now the info is almost immediate.

I wouldn’t say info is almost immediate.

It takes the ILGA quite awhile to produce Senate and House Transcripts and Journals.

One has to pay to watch videos of floor proceedings, and not many committee meetings are recorded.

There’s shell bills, bill titles that don’t match contents, lousy House Rules and more.

Most legislation gets zero press coverage.

Try following say 10 pieces of legislation in the ILGA and you will learn all the problems.

There are a lot of problems in the ILGA.

Thanks for clarifying. It is still hard to get up to date info even with modern day internet but a little quicker than years ago.

Freddy the ILGA is a joke.

The Transcripts are not even searchable.

It is tedious to download multiple transcripts.

etc. etc. etc.

Correction, the transcripts are searchable but do not allow one to copy from a transcript and paste the information elsewhere.

In other words the pdfs are “secured.”

Not to insult good public school teachers (I’m sure there are some somewhere) but the most arrogant, ignorant, and poorly educated people I’ve come across are public school teachers in Illinois. It’s one of the reasons I made darn sure none of my kids ever darkened the doorway of a public school in Illinois.

Well, this isn’t racism at least. What is it—jobism? A creative lawyer might haul your little butt into court if you don’t cease and desist.

I know that progressives don’t like free speech (that they don’t approve of), but your “creative lawyer” would be rightfully sanctioned by any self-respecting court.

If you are a current or former teacher you are supporting his argument.

Regardless no crime was committed.

NoHope’s comment is similar to racism, castigating an entire category of people for the perception made by the actions of an extremely small subset of them that happen to be in the social network of the commenter. Legal or not it’s not a wise statement to make based upon a small sample size. We all need to have some degree of charity in the way we view our fellow man. The world would be a better place to live were that the case. You need to “walk in another man’s moccasins” before you can really understand him.

Disparaging a group of workers based on their occupation is not illegal.

Just wanted to make the clear.

There was an allegation it may be illegal.

I don’t condone the choice of words but it’s not illegal.

The comment I made about hauling a person into court was said tongue in cheek, something not readily obvious I admit. Let me be clear in that I know it’s not illegal. Still, It is unwise to be cruel or crude and do so without immediate provocation even more so, and that is a better characterization for the original comment to which I responded.

James – nice to hear about what makes the world a better place. But why would you be of the opinion the comment made would lead to legal liability? There is no cause of action I am aware of that is grounded in “I don’t like what he wrote”. Your credibility is diminished when mentioning the threat of lawsuits. Your statements first speak to a hostile legal action, which is then followed up by an explanation of what it means to be a better person. There are certainly better assertions you could have made, among them that in many environments… Read more »

Does anyone really wonder why their is a net out migration in Illinois?

Because their should be. If Darwin is right only fools will be left shortly.

The Boat is sinking and the greedy government pensioners are drilling holes in the bottom of the boat. The poor honest taxpayer and his family are doomed.

What you neglect to mention is that a specific, dedicated portion of the employee contribution in each of the state retirement systems goes towards funding the 3% automatic annual increase (AAI) in retirement. Given this structure, even if you were to succeed in repealing the pension protection clause in the state constitution, the general contracts clause and prohibitions against ex-post facto legislation in both the Illinois and U.S. Constitutions would almost certainly prevent any changes to the 3% AAI for tier 1 employees on a retroactive basis (i.e. on pensions earned prior to when the legislation was passed). At best… Read more »

Andrew, a few points. You may want to follow what happened in Rhode Island and the reductions in colas there, where cuts for all workers/retirees were successfully litigated under the federal contracts clause. We lay out why such reforms would pass legal muster in Illinois in this piece here: https://wirepoints.org/part-3-why-pension-reform-is-legal/. Yes, Tier 2 was passed, but it only started in 2011. The overwhelming majority of the 650,000 state workers are still in Tier 1. Tier 2 membership is at some 80,000…We’ll be waiting a long time for Tier 2 to make a difference. You may also want to consider the… Read more »

Two things to say here: first, Andrew correctly stated that IL governmental employees do pay for their AAI with deductions from their paychecks. It could be argued that such deductions weren’t sufficient, but legally they met was was required of them for that benefit. Secondly, I read periodically that IL is losing more residents to out-migration than any—or at least nearly any—other state. But, the number itself is somewhat meaningless unless stated and compared in percentage terms as compared to the states’ overall populations. So, I’m not necessarily disagreeing with your statement, but I do wonder if it equally true… Read more »

Illinois has the 2nd-biggest loss of people to out-migration on a percentage basis in the nation. Only New York has lost more.

Thanks: this way of expressing the idea is more impressive and more depressing simultaneously.

I have been curious about this for a long time. You are obviously intelligent and understand the problem. I will hazard a guess that you are also covered by a public pension. There is not a chance in hell these pensions can be paid as promised. Why then are those covered not shouting loudest for reform? Why do you hide behind legalese?

I’m not going to respond simply because literally no matter what I say it will start as “s..t storm” of responses that will bury me in answering each one of them only expect more of the same. If we knew each other personally I’d be happy to respond. But, generally speaking, this is group that loves US and has no tolerance at all for THEM. You get the drift.

You fail to understand the legal aspects of contracts and insolvency/bankruptcy. Anything can be changed if necessary and for the “public good.” This site has repeated over and over again that there is ample evidence we are in a downward spiral. There is no amount of taxation available to pay for this, simply because it erodes the tax base as you increase taxes. It’s already happening. So, your statements — while perhaps true — don’t reflect the ultimate solution, which is to engage in some form of bankruptcy to solve this problem. It will happen, because I and others are… Read more »

Just as a thought can’t Illinois tax till there are no more assets to grab meaning confiscation of assets? Assuming that the Judges are a part of the retirement system then would it be fair to assume that no Judge would decide in a manner that would cut their own pension? When I ponder on these things along with past Illinois election history it makes me think that the only possible solution that would be equitable to the taxpayers would come out of a Federal courtroom and not a State courtroom because otherwise I see no hope for an Illinois… Read more »

You may know that the judges’ pension system was excluded as part of SB 1, the attempt to change IL government pension systems’ retirement systems signed into law in December of 2013. Even without that law affecting their ultimate pension right, the ILSC overturned that law in May of 2015. Still, your thought that the matter should have been decided elsewhere in the federal court system has merit.

I do vaguely remember that during that time thinking that somehow that would affect the Judge’s thinking but it did not. I pondered at the time how that could actually be done; slighting one group of pensioners but not another. Even so I would find it hard to believe that a Judge would decide to lower their clerks, assistants et al pensions when they work with them every day and in some cases also have relatives within the system. I think it is hopeless to seek a solution beyond my previous tale of disasterly results outside of the Federal courtroom… Read more »

If you want to live up to you name, you need to be much more arrogant and speak in a coded language that no one understands. Then we will all know you are actually his ghost.

From what I remember — and I’m citing only from memory — the judges gave a very narrow interpretation of the Illinois Constitution, essentially weighing that the pensioners’ rights weighed more in the balance between that and the ability to tax more. In other words, the judges think that we shouldn’t consider altering this “contract” until the ability to tax has been thoroughly exhausted, with solid empirical evidence demonstrating we’ve reached peak taxation.

Judges are not economists, and this decision will ultimately prove foolish, because many believe that we are already past that point.

You are correct. Here are some of the words. “Moreover, no possible claim can be made that no less drastic measures were available when balancing pension obligations with other State expenditures became problematic. One alternative, identified at the hearing on Public Act 98-599, would have been to adopt a new schedule for amortizing the unfunded liabilities. The General Assembly could also have sought additional tax revenue.” The court views raising taxes as less drastic. They view re-amortizing as less drastic. As long as the state can raise revenue that will be viewed as “less drastic”. Also interesting. “The United States… Read more »

Great comment with lots of info!

All the more reason that going back to 1.5% simple interest, which was the original deal when employees began contributing 0.5% of wages towards AAI.

As things stand IL government worker and retirees’ pension rights cannot be reduced by restrictive new laws in IL but can be increased from the date of such employment. The presumption legally on both sides of any such negotiation does—or at least should—know that.

Yes, but the argument here is “I paid for that” when, in actuality, the “that” in question is 1.5% simple COLA, not 3% compounded.

Then, it’s up to those in the legislature to do a little math before voting, don’t you think? Afterwards it’s too late.

Unbelievable.

The final average salaries are surprisingly high.

Illinois is so screwed up.

Once again, State money that should have gone to fund pensions instead went directly and indirectly to fund salary hikes.

Perversely, the salary hikes resulted in hiked pensions and thus hiked pension unfunded liabilities.

Compounding the salary hikes and missed pension contributions over decades resulted in generous salaries and huge pension unfunded liabilities.

Part of the Illinois Pension Scam and Illinois pension Ponzi scheme.

The pension sentence in the state constitution, and various laws including what Andrew Szakmary mentions above, “protect” the State sponsored Ponzi scheme.

I always felt there was a strong argument to go back to the original deal of 1.5% simple interest AAI. It’s insane that we can’t decrease COLA during a pandemic and financial meltdown.

In California, their annual benefit adjustment can also be reduced or eliminated by the Legislature if economic conditions dictate.

Illinois State government works for the public sector unions. Period. Everyone else can go pound sand.

100 million percent.

“Ignore” is likely the wrong word to have used. He simply doesn’t know what to do about it that will pass muster with respect to court challenges that would result.

It is called stealing money from the next generation and the unborn generation.

Cops, teachers and firemen love the taxpayer like a cat love a bird.

Others on this site don’t seem to appreciate your repetition, but I, for one, get a kick out of it. The cat/bird one gave me a smile!

You’ll appreciate it for awhile, but after some period of time it will be like watching the same TV commercial for the 50th time. Then, you will “get it.”

Unfortunately there is zero chance of this happening. The Illinois Supreme Court won’t allow any changes. The reason is simple; they aren’t going to reduce their own benefits. Plus, there is no political will to address this issue. You know the answer. Start looking for states that aren’t afraid to address the pension issue and have a nice climate, like Arizona.