By: Ted Dabrowski and John Klingner

Illinois politicians’ refusal to address skyrocketing municipal pension costs is destroying cities across the state. Some cities like Harvey and East St. Louis are beyond repair, with the Illinois Comptroller already stepping in to confiscate city revenues on behalf of the municipalities’ grossly underfunded pension plans. Most other cities are deteriorating quickly. They’re fighting ever-increasing pension costs that are swallowing city budgets and chasing residents away. More than half of Illinois’ 650 public safety plans are less than 60 percent funded.

Peoria is one of those struggling cities. No, it’s not a Harvey or an East St. Louis, but it’s certainly in a downward spiral like many other cities. Peoria officials are adding new taxes and fees to deal with the city’s struggling budget. A new utility tax was added in 2018, along with a public safety pension fee that’s being ratcheted up over the next couple of years. Their efforts to tax more are likely to be futile. The numbers justify those doubts.

To understand why, take a look at how much Peoria residents have put into public safety pensions since 2005, only to see things dramatically worsen over the decade. It’s a reality cities across the state face: retirement security for public safety workers is collapsing despite the billions of additional taxpayer dollars poured into local pension funds.

Peoria’s woes

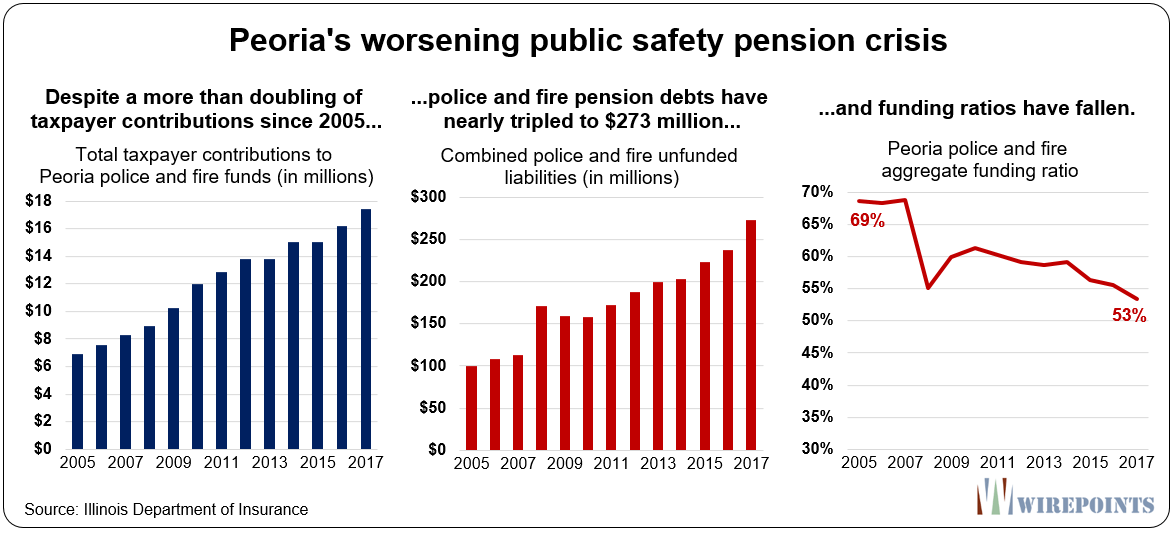

Peoria taxpayers have more than doubled their yearly contributions to the city’s police and fire pension funds, to $17 million in 2017 from $7 million in 2005. Despite all that extra funding, the combined shortfall in Peoria’s police and fire pensions have jumped 2.7 times.

Public safety pensions were “just” $100 million underfunded in 2005. But after more than $155 million in cumulative taxpayer contributions to the funds from 2005 through 2017, the shortfall in the funds nearly tripled to $275 million.

How can that happen? How can so much money go in and yet the plans get so dramatically worse? How can retirement security collapse so quickly for hundreds of city workers?

There are several drivers behind those numbers.

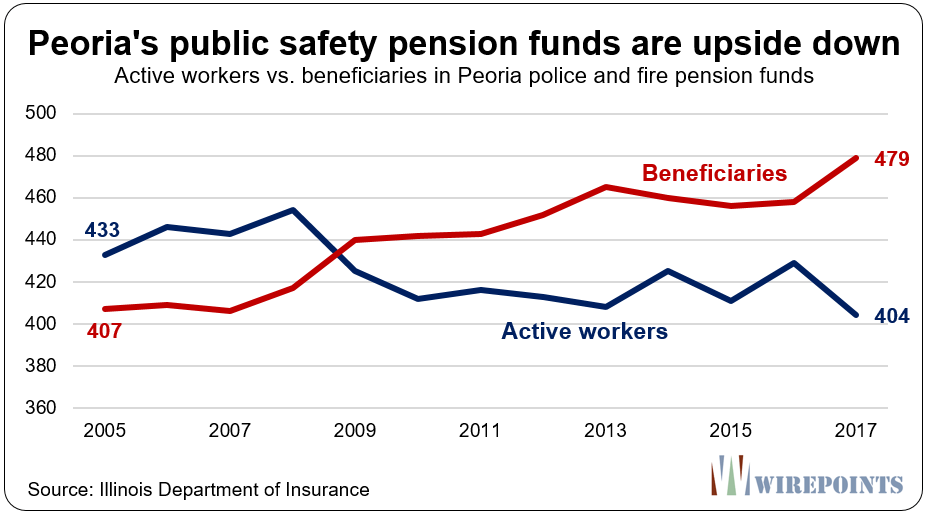

1. More retirees than actives. Start with the fact that Peoria’s public safety pension plans have 20 percent more pension beneficiaries that active participants. The plans are upside down. There are more people taking money out of the pension funds than putting money in. It’s such a common situation across the state that it’s no wonder critics of these pension funds call them Ponzi schemes.

Peoria’s combined fire and police active workforce has dropped to just over 400 workers, while the number of beneficiaries grew to almost 480 in 2017. Those numbers will get worse as the city is forced to reduce the number of active workers to free up the budget to pay for increasing pension costs. It’s a downward spiral.

Nearly 200 of the state’s 650 funds already have more beneficiaries than active workers, though the overall membership numbers for the entire state are not upside down yet. But if trends continue the number of total public safety beneficiaries will outnumber active workers by around 2021.

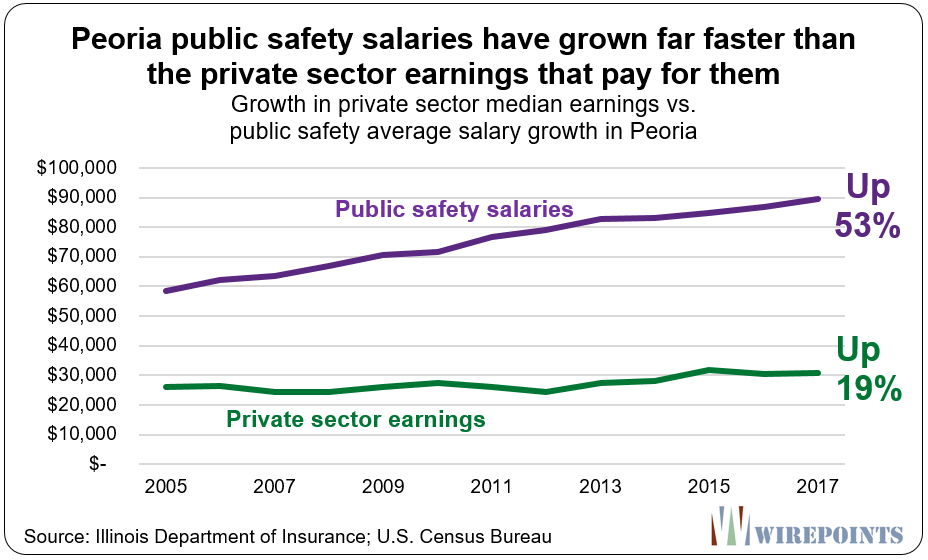

2. Salary growth. The growth in public safety salaries continue to far outpace the salaries of the residents who pay for those public workers. Higher salaries mean bigger pensions and a bigger pension hole for the city.

Since 2005, public safety salaries in Peoria are up 53 percent or nearly 2.8 times more than pay in the private sector, up just 19 percent. In contrast, Inflation over that time period was 25 percent. Public safety workers need to be compensated well, but the raises and overall salary levels are increasingly out of reach for the average Peoria resident.

The same is happening across Illinois. Average local public safety salaries statewide are up 51 percent compared to 2005. Meanwhile, median private sector worker earnings in Illinois (for all population 16 years and over, with earnings), are up just 17 percent.

Residents, whose own earnings are failing to keep up with inflation, are being forced to pay ever-higher public safety salaries, which not only drive up yearly operating budgets, but make future pensions costs jump even more.

3. Bargaining laws favor unions over residents. Illinois’ labor laws are the driver behind much of those salary increases. Public safety workers in Illinois can demand an arbitrator when they don’t get the contract terms they want. And that means city officials – the taxpayer’s representatives – are stripped of their negotiating power vis-a-vis the unions. Under arbitration, an outside, unelected official takes over negotiations and unilaterally determines the terms of the contract.

Unsurprisingly, the unions usually come out ahead in that process. The fear of losing in arbitration causes many officials to simply give in to demands rather than face the arbitration process in the first place.

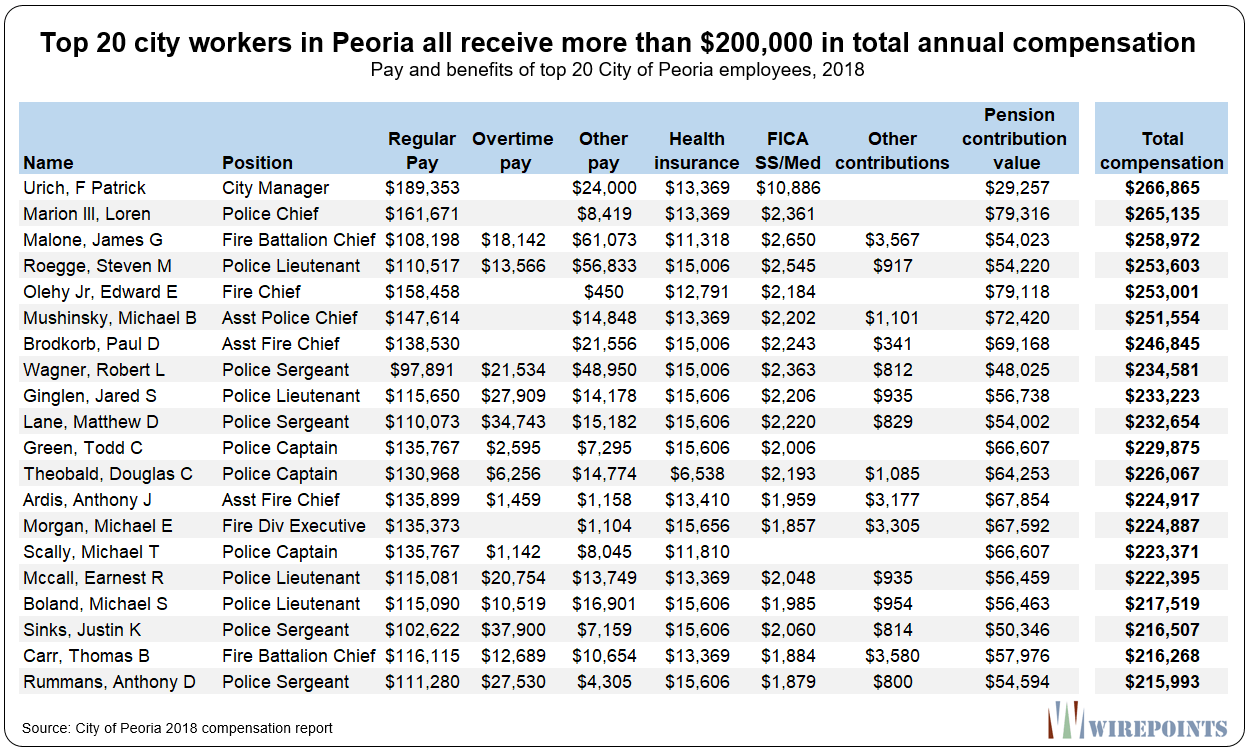

That union power has helped drive up salaries to levels far above the median salary in Peoria. A look at the city’s 2018 compensation report shows over 467 city employees make over $100,000 in total compensation a year, bolstered by high salaries. And 40 employees make $200,000 or more in total compensation a year.

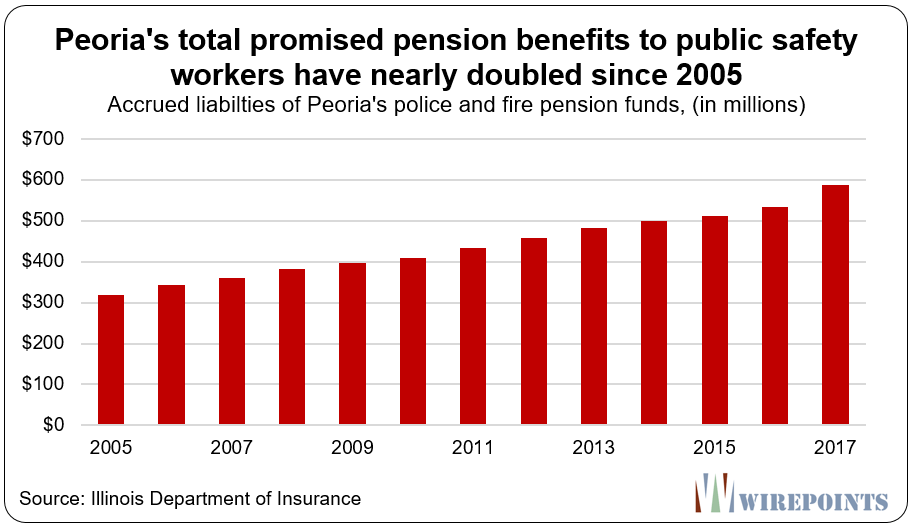

4. Fast-growing benefits. Bigger salaries mean bigger pension benefits, and that’s let pension promises grow uncontrollably despite the pension crisis in Peoria.

The value of all future pension promises to be paid out to public safety workers totaled just $320 million in 2005. By 2017, that number had jumped to nearly $600 million. That’s a jump of over 80 percent, or more than three times the pace of inflation.

It’s the main reason why taxpayer contributions can’t keep up with pension costs. Pols are doing nothing to control the growth of promises to be paid, sticking taxpayers with ever-increasing costs and ratcheting up the likelihood the pension plans will fail.

That’s true for the downstate pension crisis in its entirely. In 1987, municipalities owed a total of $2.6 billion in benefits earned to active and retired public safety workers across the state. Today, that number has jumped to more than $23 billion. That’s a jump of nearly nine times.

More to the crisis

The above analysis captures only the cost of public safety pensions in Illinois. Skyrocketing pension costs for state and municipal workers and teachers are also creating a major drag on state and municipal budgets, home prices, and out-migration numbers.

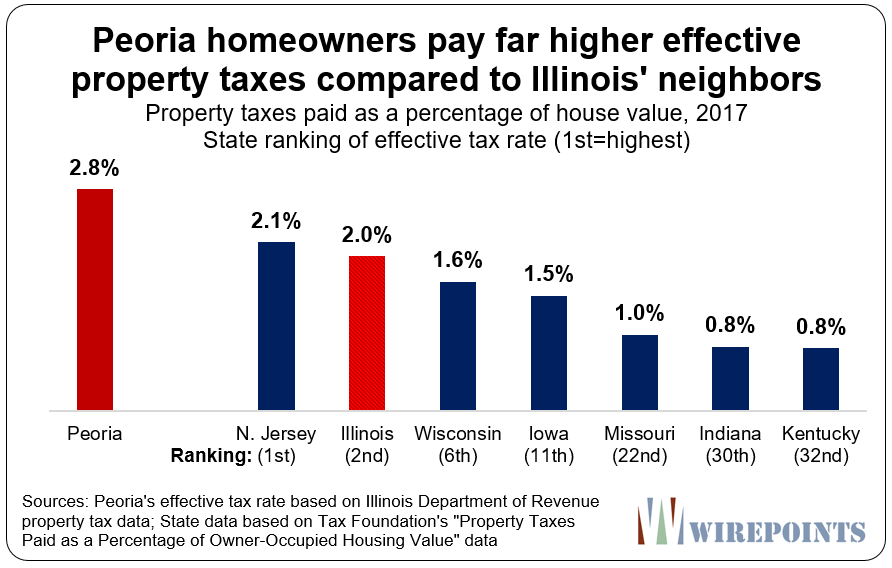

In many places, pension costs have pushed up property taxes to unsustainable levels. The Illinois Department of Revenue calculates that Peoria’s effective property tax rates based on home values has now reached 2.8 percent. No matter the research you look at, Illinois property taxes are among the highest in the nation.

What’s worse, Peoria homeowners are in deep, deep trouble. GOBankingRates found that Peoria was the most troubled housing market in the nation – the most likely to “turn ugly” according to the firm’s report. Other Illinois cities were right behind Peoria. In all, nine Illinois communities made the top 50 list of housing markets that are turning ugly.

Peoria is shaping up as a perfect storm of high property taxes, collapsing home values and growing debts – something that’s bound to drive city residents away. And as more residents leave, the bigger the bill will be on those who remain. It’s simply not sustainable.

Fixes

Illinoisans should ignore what they hear from the Illinois Municipal League and others that claim they are addressing the pension crisis by looking at pension fund consolidation. For sure, some small benefits will result from consolidation, but it has nothing to do with saving our cities and the retirement security of municipal workers.

Until you hear Illinois politicians fighting for a pension amendment, changes to labor laws, a bankruptcy option for cities and other changes that reduce the insurmountable pension debts, then they aren’t addressing the problem.

Illinois pols have already allowed too many cities to go past the point of repair. Harvey and East St. Louis are just two of them. Will pols wait till Peoria joins them before they finally act?

Read more about Illinois’ downstate pension crisis:

- Third domino falls: Illinois Comptroller set to confiscate East St. Louis revenues to pay for city’s firefighter pensions

- Illinois’ financial decay spreads to cities across the state

- Harvey, the first domino in Illinois: Data shows nearly 400 other pension funds could trigger garnishment

- Beyond Harvey: Many Illinois municipalities running out of options

- Second domino falls in Illinois: North Chicago revenues garnished for pensions –

- Third domino falls: Illinois Comptroller set to confiscate East St. Louis revenues to pay for city’s firefighter pensions

- Why a bankruptcy option for municipalities is essential

- Wirepoints/pensions – Learn more

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

Let’s not forget on how we got here.

https://www.illinoispolicy.org/the-edgar-ramp-the-reform-that-unleashed-illinois-pension-crisis/

We had a time bomb in our retirement system that was going to go off in the first part of the 21st century,” Edgar told The State Journal Register in 1994. “This legislation defuses that time bomb.” D’oh!

Let’s not forget on how we started this path.

https://www.illinoispolicy.org/the-edgar-ramp-the-reform-that-unleashed-illinois-pension-crisis/

With the Par A Dice and other casinos in Peoria you would think that should have solved all the pension problems there. It didn’t . Now there will be more casinos popping up all over like Rockford and with the political mentality going around In ILL-ANNOY this is believed to be “Manna” from heaven. Unless Jeff Bezos or Bill Gates gambles there and loses everything this will barely put a dent in the local and state pension crisis.

You mean Doing each other’s laundry, gambling and taxation are not the road to wealth? Somebody should inform the pols in Springfield, quick.

Solve the Pension Crisis (it is a CRISIS) with a U Haul.

Illinois is a goner, burnt toast. It will never solve the problem and it will only get much, much worse.

The Greed of the government employee is over whelming.

They all move to Florida and buy expensive homes, expensive cars and go out to dinner every night on the backs of Illinois Taxpayers.

Run for your economic life.

Haha you fool! I am here in the south of France sipping wine living off my 700 dollar a month pension and you fools are paying it. Lol

When the high earning people paying the bills leave, Illinois will go bankrupt, and your pension goes with it. Cheers

The City of Peoria’s IMRF pension is underfunded $25,679,413 (88% funded); and the outstanding bond principal, premium, notes, and loans are $177,393,000 in the FY 2017 audit report. The audit report for fiscal year ending December 31, 2018 is not yet posted on the City’s website. http://www.peoriagov.org/finance-department/finance-administration The management letters in recent audit reports are dated June 20, 2018, August 24, 2017, October 11, 2016, June 26, 2015, July 31, 2014, August 28, 2013, and June 25, 2012. That URL also itemizes the various taxes including rates over the base. The City has about a dozen TIFs. A common misconception… Read more »

“Freedom’s just another word for nothing left to lose.”

Those that still live in Peoria have already waited too long. The word is getting out that this town has no future. It will be increasingly difficult to sell property and businesses will struggle due to potential customers avoiding the area. Don’t feel sorry for them. You don’t have time. Every second you waste brings this situation closer to your own door. Will you repeat the mistake of the remaining Peoria residents? Are you willing to risk the safety and financial future of your family when immensely better alternatives exist outside of Illinois?

Peoria will go the way of Rockford, Freeport, Joliet, Waukegan, Decatur, Marion, Elgin ….

I’m a Plumber and i go in homes all over the Chicago area and at least 6 of every ten are planning to

move out of this state. The number one state people say there going is Tenn then Texas and a tie

for the carolina’s and Florida

You guys should do something on the best states to move too

thanks for all you do

+1 I too would like to see a regular column dedicated to moving, where to move to, etc. I was confused looking at crime rates for places. Then I decided to simply look at my own crime rates here, then find a city at least that good. As for tax rates I wouldn’t know where to start, but I need to start because we are gone soon after I retire. Most people I talk to mention Tennessee, South Carolina, Florida, Arizona.

No state income tax in Washington. Exceedingly liberal politicians in the Seattle area and state legislature is Democrat controlled however some of the craziest may lose the upcoming city council election in Seattle. High housing costs in the Seattle area and lots of traffic and homeless folks in the city. However in Edmonds and north one sees lower costs and very pleasant places to live. If you want conservative politics and warmer weather check out Spokane and Wenatchee and Lake Chelan… or Walla Walla if wine and small liberal arts colleges are parts of your plans. Lots of ski resorts… Read more »

My wife and I have the same predicament. Where to move? She suggested we sell most everything and put the rest into storage temporarily get a decent size motorhome and scope out the country. This way we have a better understanding of where to put down roots. If we don’t like the neighborhood we just drive away. Lots of RV parks around and many do this. If we get a home first and don’t like it we save the hassle of buying and selling. After Illinois implodes we could buy our home back for pennies on the dollar. In the… Read more »

“After Illinois implodes, we could buy our home back for pennies on the dollar.”

After bankruptcy or some other draconian action, will taxes and user fees be significantly reduced? I doubt it. The revenues will simply be shifted to cover a number of under-funded programs. Also, the draconian action will very likely not address all of the components of high taxes and user fees, such as teachers in the Chicago area making big salaries teaching grammar-school kids for nine months a year; bloated, highly-paid school administrative staffs; and far too many school districts.

First, and obviously, don’t move to another state facing a pension crisis. Second, when you look at state rankings, question the results. Don’t just accept it. Several rankings I have seen have Illinois rated as a tax friendly state for retirees, which is ridiculous. There are a handful of other states (like Illinois) that don’t tax retirement income (401K, IRA, social security, …) but also don’t have a state income tax. Third, consider the other major taxes such as real estate tax and sales tax. Fourth, consider the weather. Fifth, if you are retiring early (pre medicare), look at the… Read more »

Home values in Peoria are not likely to go anywhere but down for generations. Probably best for those folks to get out as soon as possible. There are really no forces to Create value once your town decides to go down the road of confiscation for the benefit of another government union over the very people that built the town.