By: Mark Glennon and Ted Dabrowski

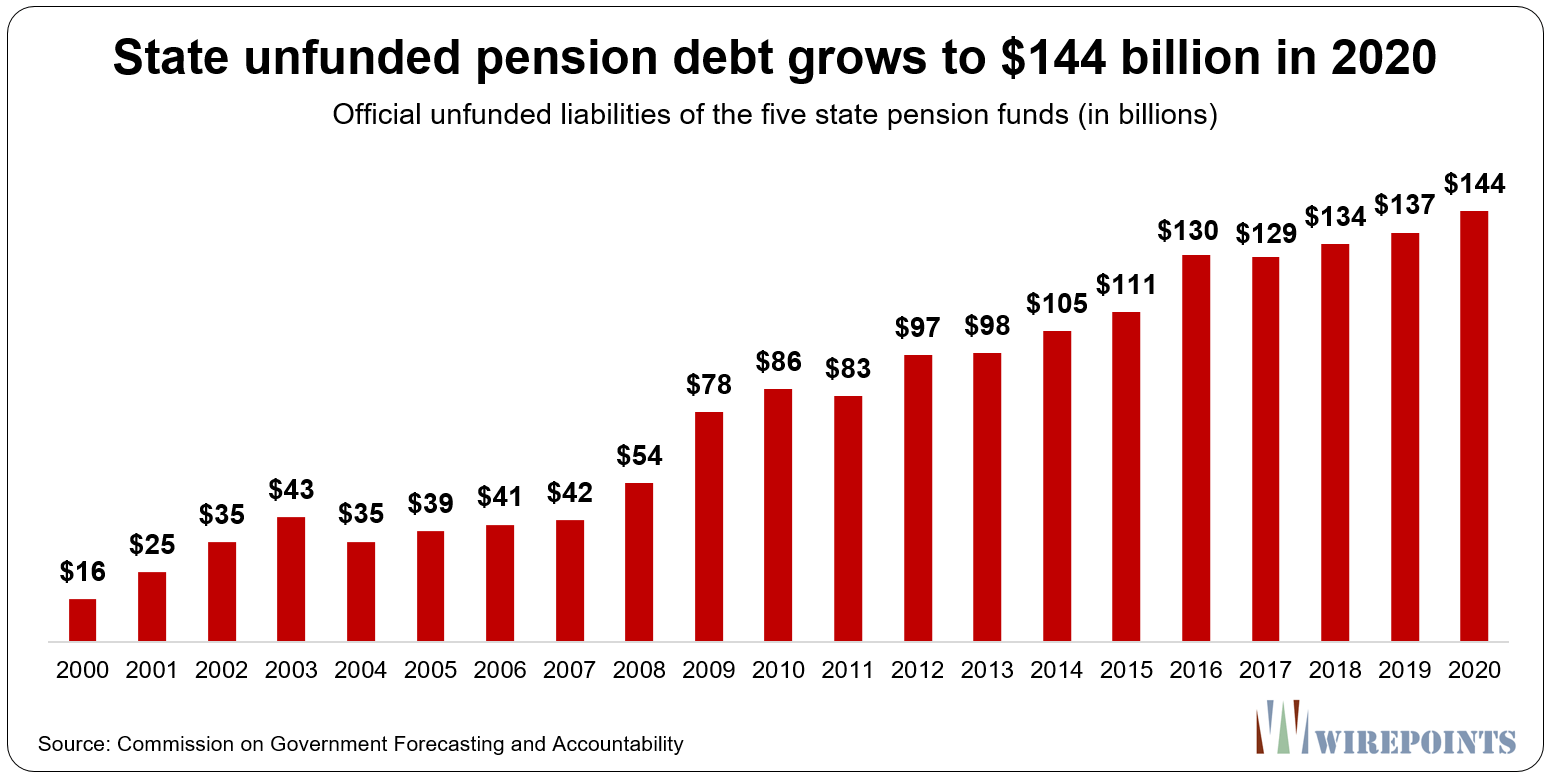

On the surface, a new report on Illinois’ state-level pensions is bad enough: The official unfunded liability of the five state pensions grew to $144 billion in 2020 – a record high, and a $7 billion increase in just one year. That’s according to COGFA, the Commission on Government Forecasting and Accountability’s latest special pension report.

We get similar, worsening news most years.

We get similar, worsening news most years.

The far worse story, however, is between the lines not covered in the new COGFA report.

First, consider the plan we are on and its trajectory. That’s the funding ramp set up by the state and its implications for taxpayers and pensioners, which is shown on page 10 of the report.

That plan, which supposedly would someday return the pensions to stability, would require state taxpayers to double their current yearly contribution to the pensions over the next 25 years. Their contribution already consumes about a quarter of the state budget.

The plan assumes the pensions will earn just under 7% on their assets. That’s far more than any expert assumes and far more than regulated private sector pensions assume. The world today is in an unprecedented low-return economy. Risk-free rates of return are under 2%, and the pensions should actually be invested in risk-free assets since pension benefits are promised as risk-free. If you corrected the pensions’ assumptions about returns on investments the unfunded liabilities would roughly double.

Even with those faults, the plan does not get the pensions to full funding, just 90%. In other words, the plan just assumes away a chunk of the problem.

Second, the new COGFA report entirely ignores future healthcare obligations owed as part of pension benefits to state retirees. They are constitutionally guaranteed in Illinois just like other pension benefits. The state’s official share of the retiree healthcare promises totals $56 billion. And here’s the kicker: They are entirely unfunded. They are on a pay-as-we-go system.

Third, the report only covers the five state-level pensions. But Illinois has some 650 additional local pensions. Most of them, too, are in impossible shape, a problem which is also officially understated. Many of those local pension obligations overlap, particularly in and around Chicago, creating havoc for many households.

Put the above together and you get a mind-blowing total of $420 billion, just 48 percent of which is for the five state-run pension plans. The details are in the chart below.

For a full analysis, see Wirepoints’ “Part 1: Illinois is the Nation’s Extreme Outlier.”

These lines in the COGFA report deserve special attention. “One of the main drivers continues to be actuarially insufficient State contributions…. [I] if all other actuarial assumptions are met, unfunded liabilities will still increase due to the State contributing an amount that is not sufficient to stop the growth in the unfunded liability. Hence, there is a distinction between contributions that are statutorily sufficient and contributions that are considered actuarially sufficient.”

What that means is that, even though pensions consume a quarter of the budget, and even if the phony return assumptions turned out right, the pensions aren’t even treading water. The unfunded liability will continue to grow.

Many state lawmakers brag every year that they made the “full, required contribution” calculated by the actuaries. No, not true. They make only the contribution the actuaries calculated based on the faulty plan – the funding ramp made up by legislators themselves. The actuaries warn each year that it’s bogus.

And it certainly isn’t that taxpayers have been skimping on their share of contributions. The problem, instead, is that total pension benefits owed by the state grew 2.5 times faster than state revenues, year after year, for nearly 30 years. See our Special Report on that, which was cited approvingly in the Wall Street Journal.

For those of you interested, here are further matters of interest from the new COGFA report along with some perspective:

– The state’s official shortfall has reached its new record level after continued growth since the turn of the century, when the pension hole was just $16 billion.

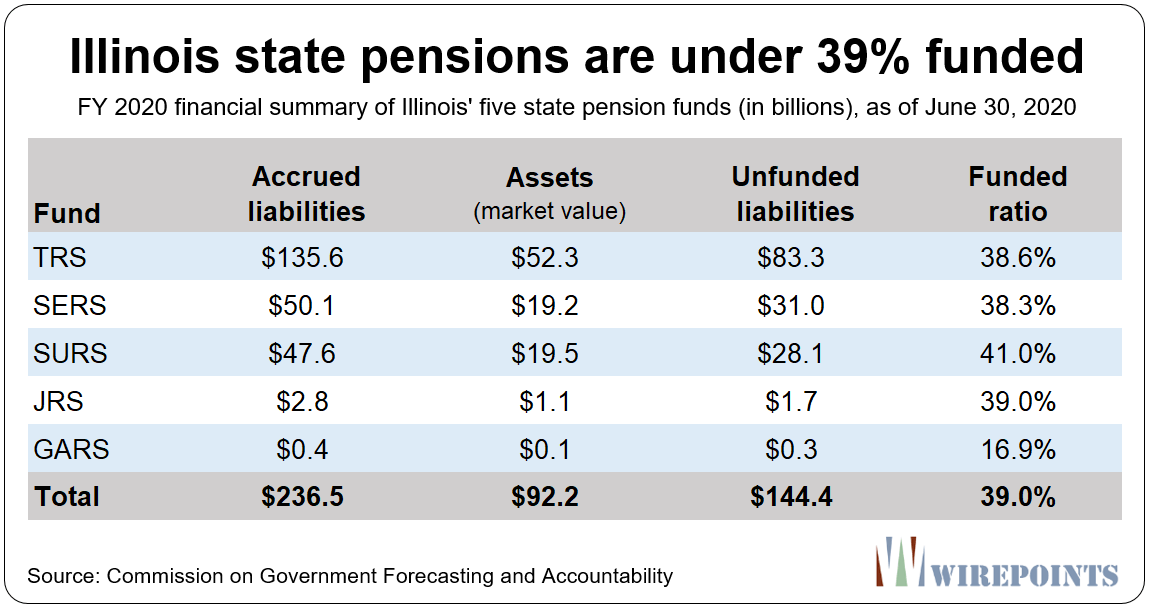

– Officially, Illinois’ five state-run pension systems have just 39 percent of the funds they need today to be able to meet their obligations in the future, down from 40.3 percent the year before.

Most notable is the funding ratio for the state lawmaker pensions. It’s just 17 percent funded, with only enough assets left to make a little more than two years’ worth of payouts. It’s insolvent by any definition.

– The fall in the state’s overall funded ratio and the increase in the shortfall are both partially due to poor investment returns for the pension systems. The systems five plans all have a June 30 fiscal year end.

– The fall in the state’s overall funded ratio and the increase in the shortfall are both partially due to poor investment returns for the pension systems. The systems five plans all have a June 30 fiscal year end.

– Like last year, all five funds failed to meet their annual investment return goals of 6.5 to 7 percent. The Teachers Retirement Fund’s investments performed the worst, barely staying positive with a return of just 0.5 percent. And the State Universities’ Retirement System managed just a 2.6 percent return versus a target of 6.75 percent.

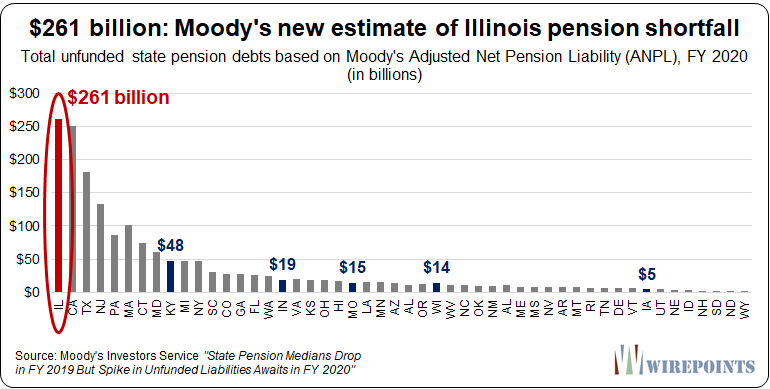

– Using more realistic investment assumptions, for the five state pensions alone, Moody’s recently estimated Illinois’ pension debts at $261 billion for 2020, the biggest pension shortfall in the nation. That’s nearly $67,000 in debt for every household in Illinois.

– Using more realistic investment assumptions, for the five state pensions alone, Moody’s recently estimated Illinois’ pension debts at $261 billion for 2020, the biggest pension shortfall in the nation. That’s nearly $67,000 in debt for every household in Illinois.

*********

*********

Unfortunately, Gov. J.B. Pritzker and Mayor Lori Lightfoot continue to reject calls for a pension amendment, with the governor calling structural reform a “fantasy.” Pritzker claims any reforms would ultimately be rejected under challenges from the federal contracts clause.

At Wirepoints, we’ve laid out why reforms would be legal under federal law, why a pension amendment and pension reforms are urgently needed and what those reforms should look like. For a summary, as well as links to all of our analysis and proposals, go to Wirepoints’ Pension Solutions.

Read more about Illinois’ pension crisis:

- Will COVID-19 lead to “pension intercepts” and cuts to core city services across Illinois?

- Solving Illinois’ Pension Problem – Special Report

- COVID-19 pushes nation’s weakest pension plans closer to the brink: A 50-state survey

- Illinois owes $68 billion in health benefits to government retirees. Politicians haven’t set aside a penny to pay for them

- Wirepoints’ Pension Solutions page

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too Audio and summary

Audio and summary  A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

A largely unasked question is becoming glaring: Is Illinois doing all it should to use artificial intelligence to make government cost less and work better? So far, the evidence says no.

Pension scenarios: 1) Fact: The Constitution pension clause prevents any impairment of promised pensions. Assumption: No change will be made to any pension Assumption: Illinois will tax, borrow and divert funds from other budgetary items to the extent necessary to pay all pensions. Conclusion: Pensioners will get every dime that they were promised. 2) Fact: Unfunded liabilities, budget deficits, unpaid bills, excess borrowing- none of which is in dispute. Assumptions: Same as above, no changes, taxes will rise and budgets cut to meet all pension payments. Conclusion: Illinois will collapse before all pensions are paid. Both scenarios are based on… Read more »

The state pensions were juiced via legislative benefit hikes and salary hikes while the pensions were already underfunded, resulting in an extremely high unfunded liability pension interest rate.

The mob’s dream would be for the state constitution to declare that the terms of mob juice loans cannot be diminished or impaired.

The mob”s dream is the State”s reality.

No need for Guido when you have the state constitution protecting your racket.

Where”s Rico?

Should be obvious Illinois is beyond the point of no return fiscally – to ‘cure’ the current fiscal mess would certainly kill the patient. The political rot is so bad in Illinois it’s unfixable.

China Joe will get some kind of Federal bailout out to the poorly run Democrat states and cities – but in Illinois and Chicago’s case, it’s just kicking the can down the road.

People need to seriously consider leaving before Illinois craters.

Add to the above list an assortment of other funds such as mass transit pension funds (CTA, RTA, Metra, Pace, etc.), retiree healthcare special deals found in employment contracts such as some Superintendents at local school districts, a mosquito district that has a plan outside of IMRF, etc.

No one has the time to compile statistics on all that and relatively speaking it is small potatoes.

But a small potatoe for an individual taxpayer adds up to a bigger potato for the beneficiary, which is the nature of these schemes.

As a comparison California has approx 977 school districts serving 6.3 M students more than 3 times that of Illinois. Florida has less than 70 unit school districts serving about 2.7M students. We have approx 868 districts serving 2M students and therein lies the problem. Way to many taxing bodies. There is too much top heavy administrative bloat costing taxpayers billions every year. School consolidation should be a priority as are combining or eliminating some of the 7,000 taxing bodies we have. Another comparison- Illinois school districts-868. Hospitals 180. More school districts than hospitals and hospitals serve all 12 M… Read more »

Right you are, Freddy! But, the practical problem which continually inhibits reducing the number of school districts is that people everywhere like local schools and local control of those schools. There are numerous towns in IL and elsewhere who discuss school district consolidations, but its a rarity to have any such vote for them passed by the local citizens. Think of all the small towns all across rural Americal whose citizens love to attend the local sporting events and general social gatherings of their local schools. When consolidations happen many of those local schools are closed, students are bussed elsewhere… Read more »

That is quite true. Probably if it is on a ballot most of those voting are employees of the potential consolidations and more often than not the referendum will be in the March primary which historically has the lowest voter turnout.

I like local sports but there has to be a way to keep those programs (scholarships.etc) even with consolidation.

Winnebago county has 11 school districts with 11 super’s dozens of ass’t supers and so on that could be combined and yet keep each individual school autonomy. Consolidating super’s/administrators would be a start.

Some are doing just that—having a superintendent shared by neighboring districts. That’s a good start even if his salary is bumped a bit as is usually the case.

Are you familiar with People who Care vs Rockford Board of Education lawsuit? I believe law schools are teaching what happened here. Even when integrated in the same school white students had their own classes-Black had their own. This was 70’s and 80’s. Good reading and jaw dropping on how bad it was. One reason our taxes are so high. Cost $250M+ LA times had a good article on Nov 9,1993

No, I never heard of it. I don’t know anything more than you’ve said, but it seems the school board had a duplicitous scheme of integrating their schools without actually integrating their classes. So, it was bound to work only for the first school day until the students went home and spilled the beans: not so bright, after all. Its a lesson in the folly of complying while ignoring the spirit of the law.

https://www.chicagobusiness.com/finance-banking/finance-capitals-imperiled-threats-beyond-working-home I found this interesting. Despite having two of the largest exchanges in the world, and being home to several large HFT firms, Chicago isn’t in the top ten for finance anymore. It was #7 in the world in 2010.

Any chronically unfunded pension liability drives up the cost of the pensions due to compound unfunded liability pension interest. Legislative benefit hikes, a practice that began shortly after the pensions were created, while the pensions were already underfunded (the pensions have always been underfunded), results in compound unfunded liability pension interest. Salary hikes while pensions are underfunded results in compound unfunded liability pension interest. Adding a sentence to the state constitution that permits unlimited pension benefit hikes, and unlimited salary hikes, while pensions are underfunded to unlimited levels, and states the resulting benefits cannot be diminished or impaired, can and… Read more »

Sleepy Joe got elected. Held the House. First job done. If they win two GA Senate races, JB gets a bailout

I don’t think that rating agencies are ignorant of the information you frequently provide — nor underwriters nor actuaries nor bond-counsel nor any other “guardian” that the laws have put in place to protect … protect whom? Certainly not taxpayers. And by this time they’ve learned to draft disclosures that point out all the risks. This is a worse fraud than the unemployment insurance. Yet disclosure somewhere in a 200+ page official statement is probably sufficient to prevent convicting the participants. These are like the adhesion contracts you “accept” every time you install software. It’s a bit like “cigarettes can… Read more »

Illinois is already functionally in bankruptcy and you can tell by the yields the bonds trade at. MLF was basically a bail out bc they couldn’t have those terms in markets

if this were the private sector the company would’ve been in receivership decades ago and management team criminally liable.

Are any Illinois politicians in either party telling the residents the truth about the numbers? I’m seriously asking because I follow the mainstream news less and less these days. I watch FOX a little and follow Wirepoints. That’s about it. I’ve grown to hate the city and state I lived in my whole life. I’ve even lost interest in all the Illinois/Chicago sports teams. Hopefully I’ll start to feel connected to my new city/state in 2021. My Christmas wish is for all conservative Illinois residents to become fully aware of the Illinois death spiral and make a new years resolution… Read more »

I was very fortunate to be able to sell my Illinois home this year and relocate to one of the states with the least under funded public pensions. My recommendation for all conservatives left in Illinois who can’t relocate out of state is to sell your home and rent. At this point, it is critical to protect the equity that you have built up in your home.

Good suggestion for those who simply can’t move out of state yet.

What numbers are big enough to shock the conscience of the court in Illinois into finding a remedy?

When they can’t afford salary of government

They need to stop saying “One of the main drivers continues to be actuarially insufficient State contributions” because it implies gross negligence. Lost in that wording is the billions we contribute every year and how much of the budget it consumes. It’s a cop out that allows pension advocates to hide behind the same old “we made all our contributions on time”.

It is the main driver. You can argue all you want that pensions are too generous but mathematically if our pensions weren’t underfunded the state would have no problem making its’ yearly actuarial required contribution. If the state were to make its’ actuarial required contribution around 70% of that would be for past payments. Meaning that if pensions were fully funded then the required actuarial contribution would be in the 3-4 billion dollar range? maybe less? If the pension funds are $150 billion short that’s an estimated 10.5 billion that they could have earned at 7%. The last I checked… Read more »

You are using the same arguments made in Bell California and segregated Alabama to defend self-dealing, predatory, and unconscionable behavior by duly elected local politicians.

Why are you so adamantly opposed to an immediate cessation of the root cause: unsustainable early retirement benefits and defined benefits in general?

Shouldn’t you be arguing in favor of entirely converting new hires toward defined contribution plans without free insurance OPEBs at age 55-58? That way all funding left in Illinois could be devoted to paying you and yours.

I have made no such argument. The number 1 cause is the debt not the current cost of the pensions. If people want to support moving new hires to defined contribution plans have at it. I don’t have a pension. I am merely providing facts and truths when people love to spout emotional arguments. I don’t think the US government should wipe out student debt and I don’t think people should wipe out the states debt to pensioners either. I believe in the sanctity of contracts and honoring ones commitments. You and others on here don’t like teachers or other… Read more »

I agree with the necessity of honoring one’s contracts and commitments, for example that student debt should not be erased. But to me there is a fundamental difference here, in that student debt was personally agreed to by the debtor, with full knowledge of the contract he was entering into. That is not true of the pension obligation. Voters in 1970 approved a Constitutional provision that apparently made their children and grandchildren parties to a contract that cannot be altered. Perhaps it is only an emotional argument, but I cannot agree that this is right or just. To say that… Read more »

So your solution is that individuals can’t walk away from contracts even through bankruptcy (student loans) but the government can enter into a contract and decide not to pay? Under your argument I didn’t agree to any of the state borrowing so those debts should be erased as well. What about vendors that entered into contracts with the state? Why should my taxes go to paying them? I wasn’t part of those negotiations. Those vendors should have known they were doing business with a state that is broke so it’s their own fault. Heyjude, how do you decide which state… Read more »

The “no change” amendment did not impose any caps on benefits. In practice that means that taxpayers can be on the hook for unlimited payments into perpetuity? Of course this would result in exactly what has happened. Those who stand to benefit have banded together to push ever-increasing payments. Why would they not, since they believe they have an iron-glad guarantee? To me it is not whether teachers “deserve” the benefits, or choosing which equally “valid contract” to honor. This provision is in my mind so egregious that it needs to be eliminated. There have been many proposals on how… Read more »

Or, when you get tired of beating your head against the wall you can finally get the hell out.

Yes, maybe I will come to that decision in the future.

Sure, let’s get crackin’. When are you planning to volunteer to start that movement?

These pension “contracts” would have come under much greater scrutiny if they had been adequately funded 25 years ago when politicians went into overdrive kicking the can. They knew that if they raised taxes high enough to adequately fund the pensions, there would be taxpayer revolt and Tier 2 would have been necessary right then. So they doomed the state forevermore with their pension shorting. The state is in a death spiral. Hopefully no federal bailout is forthcoming. Pack your bags.

Great, start with honoring the constitution. The ORIGINAL contract.

Truth Hurts, literally speaking it’s the definition of truism to say they weren’t adequately funded: Of course they’d be fine if they were adequately funded — in a sense. But the real point is that paying through the nose is still not adequate because the benefits are unaffordable and benefit costs have blown through the ceiling. That’s why no administration, Dem or GOP, good times or bad for decades, has funded the truly required amounts.

Mark, You are correct that neither party has wanted to truly fund the pensions. Neither party wants to be honest with the taxpayers either. If they were honest they would have never started the Edgar ramp. If they were honest they would state that the flat income tax rates need to rise to 7 or 8% for all tax payers with the increase revenue going entirely for the pensions for the next 25 years. Not exactly a winning political message but it’s also why the courts won’t help. Even your site is not being honest with its’ readers. You have… Read more »

HOW DUMB IS THIS GUY?…….

Right now, pension costs eat up nearly 28% of the Illinois’s budget.

In Indiana, Pension costs just 6% of their budget.

The communist entitlement mentality rears its ugly head!

Truth stated, “Until people flee Illinois at a high enough rate to cause revenue to decline. . ..” I would add to that, “and corporations.”

Case in point – look at the major corporations that are leaving California for Texas and Florida.

We have been honest about what the RI court said. It doesn’t matter if the reductions there were temporary or permanent, large or small. Nor does it matter whether it is about a state or a city. The point of the RI case is that it illustrates the legal principle that would apply in IL, and application of that principle requires a fact test. Yes, the facts differ in IL, but that’s the point of the principle — the scope of the pension reform that is permissible has to be reasonable based on the facts in each case. We have… Read more »

Oh ,only 40 billion,well heck,thats not that much debt!-huh!?-seriously?!

You are missing the context. The point was about its size in relation to pensions/healthcare for purposes of making prorata haircuts if that were to be done.

Point taken,thank you mark!

Btw,you guys rock,love reading your articles!-keep up the great work guys!

No “Easy Button” to hit. Problem here is that, election after election, “Democracy” didn’t produce outcomes that bespoke so many people voting that the number of “wise” voters outnumbered those who didn’t vote with the common sense that God gave geese – or didn’t vote at all. Instead, we got (and too often continue to get) the Ambrose Bierce version – four wolves and a lamb voting on what to have for lunch. inevitably, we approach the point where the lambs aren’t reproducing rapidly enough to keep the wolf-pack in noontime mutton. The Truth Hurts’ view, which seems to be… Read more »

The GREEDY AND SELFISH union thugs are brainless when it comes to 4th grade math.

There are no private sector plans that if you put in 160k, you will get back 2.5 million and free health care for life.

The State pensions have been a state sponsored Ponzi scheme since the day they were created.

There was no serious attempt to freeze benefits, hold salaries to a minimum, while fully funding pensions.

That’s the Illinois Pension Scam.

No. A more accurate analogy is someone originally got a $1,000 mortgage for 50 years. They made partial payments and took out hundreds of home equity loans (legislative pension and retiree healthcare benefit hikes) and then add salary hikes. The State did not act in good faith. Pension benefit levels (the determination formula that takes into account retirement age, years worked, accrual rate, etc.) are supposed to be predictable and stable. That did not happen in Illinois. Illinois repeatedly juiced the formula and jacked up the salaries. To make matters worse the transparency of how that transpired was awful. The… Read more »

There is no level of taxation that can fund these obscene and immoral pensions

It takes an army of taxpayers to pay one retired teacher.