By: Ted Dabrowski and John Klingner

It didn’t take long for new Chicago Mayor Lori Lightfoot to propose a plan that would wash her hands of Chicago’s pension crisis altogether. According to a recent report in Crain’s, Lightfoot wants the state to take over Chicago’s pension debts and merge them with the other pension plans throughout the state. The move would make all state taxpayers responsible for paying down the city’s debts.

The plan to shift city debts to the state would bail out the mayor from having to raise about $1 billion in additional taxes to pay for increasing pension costs by 2023. A massive tax hike is something she’s desperate to avoid.

But while Lightfoot may think the cost-shift is a solution, it will only make things worse for Illinois. She should expect significant pushback from many sides.

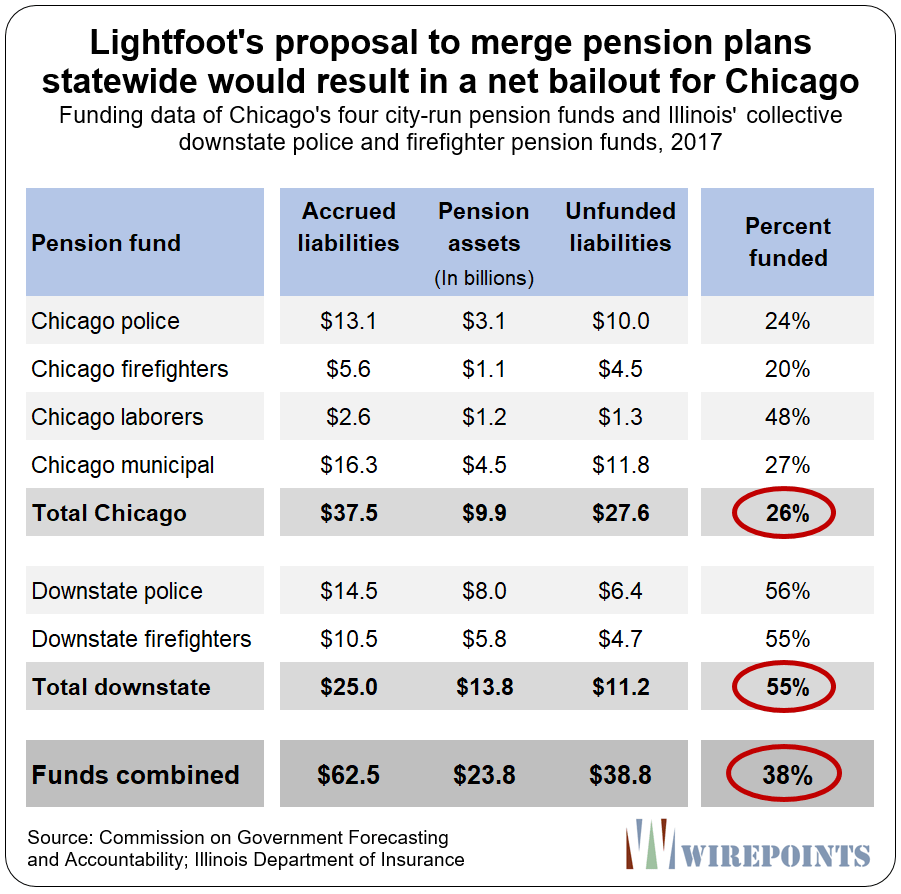

Start with downstate and suburban residents. Sure, their public safety pension funds would get consolidated under the state, too, but it’s the Chicago funds that are some of the biggest and worst-funded in the state. The four city-run funds are collectively funded at just 27 percent and face an official shortfall of $28 billion.

In contrast, the 650 downstate pension plans are 55 percent funded and have a shortfall of nearly $10 billion. The end result of any statewide pooling of pension funds will be a net bailout for Chicago.

Non-Chicagoans aren’t going to just accept yet another bailout of the city. Downstaters’ most recent bailout of Chicago came when the state’s new education funding formula locked in special subsidies for Chicago Public Schools. That included hundreds of millions in hold-harmless funding as well as $200 million-plus annually to pay for the district’s pension costs.

The mayor can expect pushback from the rating agencies, too. Illinois already has what Moody’s Investors Service calculates as a $234 billion state pension shortfall, while the state’s retiree health insurance fund has another gaping $73 billion hole.

Adding $42 billion more – what Moody’s reports as Chicago’s true pension debt – may push the state’s credit rating into junk category. That’s significant since no state in modern times has been rated junk (see Appendix for Moody’s state-by-state rating).

Lightfoot’s pension proposal might come as a surprise to some given her comments last week to the Chicago Sun-Times. According to the paper, “Mayor Lori Lightfoot said Friday she’s willing to tackle Chicago’s ‘mounting, looming, all-consuming’ pension debt once and for all, even if it means risking her political future.”

“We cannot keep asking taxpayers to give us more revenue without the structural reforms that are fundamentally necessary to make our city and our state run better. Now is the time to act,” she said.

Lightfoot has obviously given up on structural reforms. Her proposal does nothing to actually reduce the overwhelming debts of the city’s pension funds. Instead, it appears her only goal is to socialize the costs across all state residents.

That’s not “risking her political future.” Making everyone else pay for the city’s debts, if she can make it happen, is the easy way out.

Few options

Lightfoot the candidate knew what a mess the city’s finances were in. The city was already rated junk by Moody’s when she took over, while CPS was five notches deep into junk – worse than even Detroit.

But Lightfoot never signaled a plan for pension reform during her campaign. Her only commitment was that she would protect pensions: ”First, we must start from the firm position that pensions are a promise – and that protecting the retirement security of our public employees is imperative to maintaining a stable middle class and, thereby, our local economy.”

Now she’s found that, in the absence of reforms, the city is running out of options.

Reamortizations – kicking debt payments further into the future – are getting pushback from both rating agencies and public sector unions alike.

Pension obligation bonds, another kind of can kick that Rahm Emanuel pursued, have also run into opposition. Rating agencies, pension funds and actuarial associations are calling POBs what they really are: a gamble with taxpayer dollars.

City tax hikes aren’t a solution either. Chicagoans are tapped out. City residents have been hit by an avalanche of state and local tax increases over the past several years, including the state’s 2017 income tax increase and the biggest property tax hike in the city’s history. Increasing taxes yet again to get the $1 billion needed for pensions could result in severe backlash against the mayor.

Fixing things

Lightfoot’s words to the Sun-Times are all the more disappointing considering the reforms she could have called for: a constitutional amendment to the pension protection clause, changes to how the city doles out retirement benefits going forward, and tough cuts in upcoming contract negotiations with CPS and other labor unions.

Instead, her desperate plan abrogates any responsibility for the city’s largely self-inflicted retirement crisis. And more importantly, it leaves nobody better off. Despite all the tricks, Illinoisans, including Chicagoans, would still be under the same mountain of debt.

Reforms, not can kicks, are the solution to the state’s pension woes. If not, expect more and more Illinoisans to cut their share of retirement debt down to zero by leaving.

Read more about the state and Chicago’s pension crises:

- Ignoring the elephant in the room: Mayor Lightfoot skips pension reform

- Chicago’s pension funds looking more like a collapsing Ponzi scheme

- Rank Dishonesty on Pensions From AFSCME’s Executive Director

- Beyond Harvey: Many Illinois municipalities running out of options

- If a decline in births is a problem nationally, it’s a full-on crisis in Illinois

A mess of uncertainty and litigation is sure to follow.

A mess of uncertainty and litigation is sure to follow. With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

With $162 billion more from taxpayers, couldn’t you deliver a few bond upgrades, too

Pensions are like those you-tube vids about distances in the universe. It’s just as hard to imagine how much money is owed to public workers. For example if the sun were the size of a pea the distance to Proxima Centauri, the nearest star, would be 200 miles, or halfway from LA to Las Vegas.

Chicago mismanagement of funds is not our responsibility. We are trying to take care of our own communities.

The proposal is an overly complex set of ideas to screw taxpayers outside Chicago. Consolidation of Chicago pensions to IMRF can be done without shifting any responsibility to the state. That’s how IMRF operates today. IMRF currently is a locally funded consolidated pension plan. Each property taxing district is responsible for funding only it’s portion of the pension debt, with the funds pooled for investment purposes, and the state totally out of the funding picture, as it should be. Here’s the most disturbing part of the Crain’s article: “Should the state pick up part or even all of those costs,… Read more »

No

Chicago teachers chose their own pension plan!! Can’t change your mind now!!

Suddenly that 1% state-wide property tax proposal by the FedRes BoC doesn’t seem too far fetched…

.

I wish LL luck with the state take-over proposal. I think it is the best choice among several bad alternatives. Another crippling round of property tax hikes will eventually cripple Chicago. And Chicago is the economic engine for the State of Illinois. If Chicago goes down, the whole state goes down.

Will downstaters object? Of course they will. But Michael “Shut Up And Take It” Madigan will ram it down their throats.

The best choice would be for Lightfoot to use the bully pulpit to support reforms, not to kick the problem up to the state level. And actually, the state assuming Chicago’s debts could have a more dire effect than a city property tax increase. If the state is downgraded to junk, that will cause major financial repercussions that will ripple down to all local governments, including Chicago.

The numbers just won’t work without real pension reform and a long list of other reforms. Lightfoot and Pritzker boxed themselves into an impossible situation by ruling out pension reform.

Wouldn’t this impact the likelihood of passage of the Constitutional amendment regarding the progressive tax? To the extent voters understand that the tax will impact the middle class, will they really want to subsidize the City of Chicago in such a massive way? I don’t think the shift of pension liabilities to Springfield is an easy sale – both the city and the state are broke.

The Sun Times is reporting that Pritzker says no to this idea, saying the state cannot go from near junk to junk by assuming this liability.

Lightfoot is now on to taxing the services of lawyers and accountants.

This article?

Chicago Sun-Times

Lightfoot turns to service tax after Pritzker rules out state takeover of city pension funds

By Fran Spielman

Jul 1, 2019, 3:11pm CDT

“‘To be clear, the state is at just above junk status in its credit rating.

So there are not liabilities that can be adopted by the state that would not drive us into junk status.

So, that is not something that we can do,’ Pritzker said after a news conference at CTA headquarters highlighting passage of the $45 billion “Rebuild Illinois” capital bill.”

https://chicago.suntimes.com/city-hall/2019/7/1/20677755/lori-lightfoot-city-pension-funds-service-tax-jb-pritzker-general-assembly

Its not just lightfoot asking for state to bailout city pensions, sure all the unions are as well and with everything they did to get jb elected im sure they will get state to authorize aditional taxing ability beyond current home rule taxing constrains. Lightfoots just the fall guy/ gail!!

Chicago’s property taxes are low relative to.many suburbs. She has a lot of room to tax Chicago more and not dump it on the state.

I am not sure about this. There is a limit to how much property taxes can be raised on the south and west sides of Chicago, in fact, I would think can’t raise them at all. The burden will fall on those in the Loop and north and northwest. I see where you think there is room to tax more in these areas, but given the amount of revenue that must be raised, won’t those in Loop and north and northwest quickly reach a saturation point, especially given that many in these areas can’t count on public schools (meaning extra… Read more »